The week is nearing its end, and we note that the conflict in the Middle East is continuing, with it potentially spilling over into a regional conflict, which may affect gold and oil prices. Ongoing instability in the Middle East continues to be a major driver of commodity movements, particularly energy markets. Rising tensions in the Middle East have kept traders alert, as any further escalation could inject additional uncertainty into global markets. We would like to have a look at what next week has in store for the markets, especially given how developments in the Middle East may continue to influence risk sentiment and overall investor behavior.

On the fiscal front, we note that the EU Finance Ministers are meeting on Monday to discuss the creation of an EU capital markets union, an initiative that could gain more attention if Middle East-related risks intensify. On a monetary front, we note on Tuesday the release of the RBA’s October monetary policy meeting and on Wednesday the release of the Fed’s Beige Book, both of which may reference the broader geopolitical backdrop, including Middle East tensions.

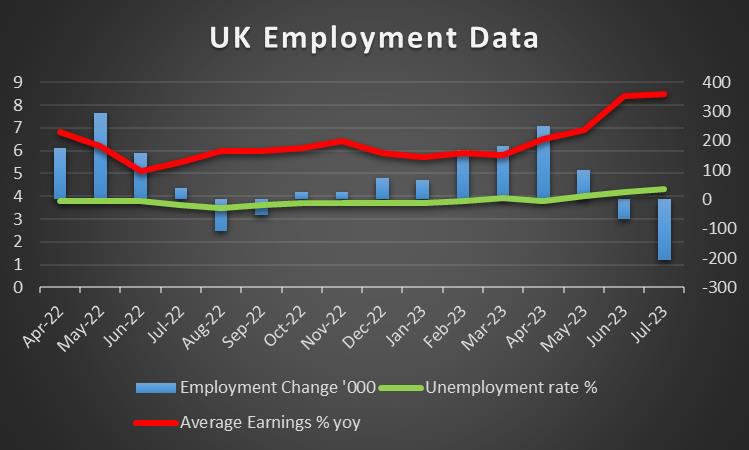

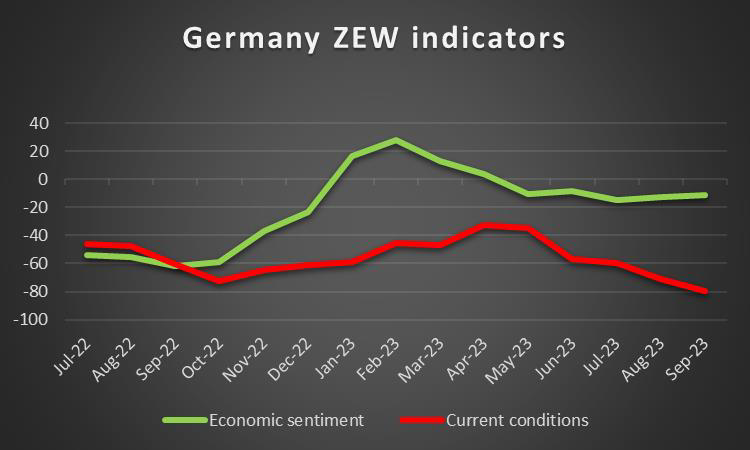

In regard to financial releases, we make a start on Monday with Canada’s manufacturing sales rates for August and the UK’s House Prices rate for October. On Tuesday, we note New Zealand’s CPI rate for Q3, the UK’s ILO Unemployment rate, the UK’s average weekly earnings rate and the Employment Change figure, all for the month of August. Later in the day, we note Germany’s ZEW Economic Sentiment figure for October, the US Retail Sales rate, Canada’s BoC Core CPI rates and the US Industrial Production rate, all for the month of September, with analysts watching whether Middle East-driven volatility will influence reactions to the data.

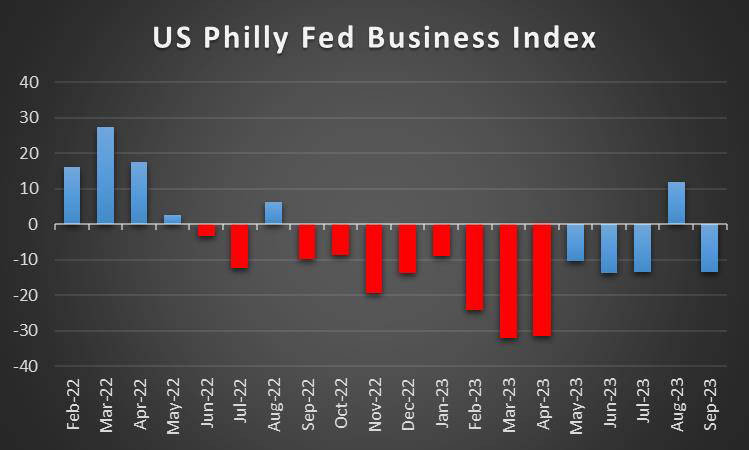

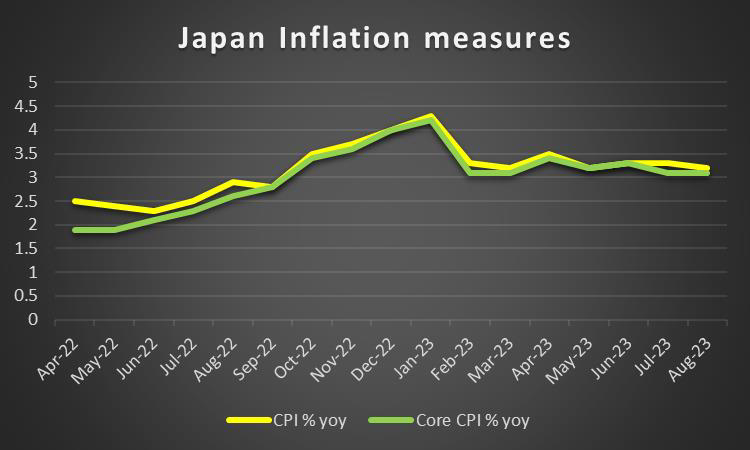

On Wednesday, we make a start with China’s Industrial Output rate for September and China’s GDP rate for Q3, followed by the UK’s Core CPI rates and the Eurozone’s Final HICP rate, both for the month of September. On Thursday, we note Japan’s trade balance figure and Australia’s Employment data, both for the month of September, followed by France’s business climate manufacturing figure for October, the US weekly initial jobless claims figure and the US Philly Fed Business Index figure for October. Lastly, on Friday we start with New Zealand’s trade balance figure, Japan’s CPI rates, Chain Store Sales rate, the UK’s Retail Sales rate all for the month of September and lastly Canada’s Retail Sales rate for August, all of which will be assessed in light of the prevailing Middle East geopolitical risks.

USD – Inflation refuses to slow down

The dollar is about to end the week slightly higher against its counterparts. On a fundamental level, we note that the US House of Representatives are still without a speaker and despite House Republican Scalise winning the GOP nomination, he appears to be still short of the votes required. The difficulty faced by the GOP to actually vote the head of the House, despite having the majority, is at least irritating and highlights the wide wedge separating the moderates from the far right. On the monetary front, the FOMC’s September meeting minutes were indicative that the Fed intends to keep rates at their current restrictive levels for a prolonged period of time, yet the case for future rate hikes appears to be diminishing and as such, given statements made by Fed policymakers in the past week and it seems to be weighing on the dollar. On a macro level, we note that the US CPI rates for September failed to slow down substantially implying a persistence of inflationary pressures in the US economy. Furthermore, the US PPI rates also came in higher than expected, which could in turn also imply persistent inflationary pressures. Therefore, one may have expected that the dollar may have gained support as the PPI and CPI rates could both justify a potential rate hike by the Fed in order to combat inflationary pressures. At the same time, ongoing geopolitical uncertainty in the Middle East may have contributed to bouts of risk aversion, indirectly affecting dollar flows. Following the releases, the dollar appears to have gained newfound support, as we head into next week’s financial releases such as the US Retail sales and Industrial production rates. The two financial releases are expected by market analysts to contradict the aforementioned statement, as they are expected to hint at an easing of consumer spending and demand, implying a tightness or unwillingness in the consumer’s ability to spend. Such an indication could weaken the dollar, as it may appear that the inflationary pressures are impacting consumer spending and demand habits. For next week, we highlight the release of the Fed’s Beige Book on Thursday which may provide greater insight as to how each district has faired in light of the currently high interest rate levels, especially as Middle East-related uncertainties continue to influence broader market sentiment.

GBP – UK’s Employment data in view

The pound seems about to end the week relatively unchanged against the USD and EUR, yet gains against the Yen. On a fundamental level, we note that the UK government has cut the HS2 high-speed railway project, touting that it will be re-investing “every single penny” back into other infrastructure projects. Furthermore on another fundamental note, according to Bloomberg, UK households owe a record £2.6 billion to their energy suppliers, implying that the disposable income for the UK consumer has decreased, and should economic activity deteriorate, we may see the pound weakening. On a monetary level, we note that some hawkish tendencies in the BoE continue to persist, despite the bank remaining on hold at its last meeting. We note for this week, BoE Chief Economist Pill’s comments that “Whether we’ve done enough or whether we have more to do, I think is becoming a more finely balanced issue” referring to the fight against inflation. The statement may have been interpreted as another signal for another rate hike to come, considering that the previous decision by the bank was to remain on hold. Furthermore, had the bank believed it was done hiking rates in the previous rate decision, the hypothetical rate hike scenario would have not been considered in our opinion. As such the consideration that more rate hikes might be required, tends to lean on the hawkish side rather than the dovish side. Yet, we note that the markets are anticipating the bank to remain on hold. In addition, based on the data from the UK, in regards to the Industrial production and manufacturing rates deteriorating, the picture for the economy is slightly grim, as it may imply a gradual slowdown in activity. Yet the silver lining of this week’s financial releases was the GDP rate for August, which improved on a mom basis, thus solidifying the UK’s escape from an economic recession, at least for now. Traders may be interested in next week’s financial releases, where we are expecting the UK’s

employment data, where should the UK’s employment data come in better than expected the pound may gain, as it may provide some leeway for the bank to hike in their next meeting. However, should it be indicative of a loosening labour market, we may see the pound weakening as the bank may opt to remain on hold rather than hike. Lastly, with the increasing volume of UK-based financial releases, we may see a switch from a fundamentally driven pound to a financial release-driven pound and as such, perhaps increased volatility in the FX market.

JPY – Japan’s CPI rates next week

JPY appears to be edging lower for the week against the EUR, the pound and the greenback, maybe in a sign of broader weakness. Following last week’s apparent government intervention in the FX market, we have yet to receive any official confirmation from the Government, yet we highlight that the risk for “another” government intervention remains elevated. In any case, we have to note that the market intervention seems to have stabilised the JPY over the past week. On a monetary level, we note the speech by BOJ member Noguchi, who reiterated his commitment to maintain the bank’s ultra-loose monetary policy, having stated that “There’s no need to rush into doing something as there’s still room for a 1% cap (for the yield band)”, implying no imminent changes to the bank’s current Yield Control Curve policy. However, we highlight the statement by BOJ Noguchi who stated that “we have no choice but to raise inflation forecast for FY2023”, which could imply a shift in policy for the bank and as such could support the Yen. However, on a macroeconomic level, we note that the Japanese Machinery orders on a mom level came in lower than expected, indicating that economic activity in the Japanese Manufacturing Industry may be weakening despite the bank’s attempts to maintain a resilient economy, while the Corporate Goods prices also were in the negatives implying a contraction of prices at a producer level. As such, traders may be interested in next week’s CPI rates on a nationwide level for September, where should they come in higher than expected, we may see the bank shifting its current policy, as inflationary pressures may show some resilience. Whereas a lower-than-expected print, could weaken the Yen, as it may pressure the bank to maintain its dovish stance. Yet, we highlight that any change could be gradual and at this point in time, is slightly farfetched. Nonetheless, we highlight that the release may impact the FX markets, as the bank will be meeting to discuss its monetary policy the week following the release of the Core CPI rates.

EUR – Eurozone economic outlook set to deteriorate further

The common currency is about to end the week lower against the USD yet remains unchanged against the JPY and GBP. On a fundamental level, the Eurozone’s Finance Ministers are due to meet next week to discuss an EU Capital Markets union and should the discussions prove fruitful in progressing such a plan, it could support the EUR. It’s characteristic that following last week’s report, the coalition ruling party in Germany lost its appeal some time ago and as was expected, the far-right AfD gained in polls and reported its best-ever result in a West-German state. Moreover, on another fundamental note, the Polish elections are due to take place over the weekend, with the right-wing Justice party anticipated to come out on top and if so, could generate political tensions in the EU and as such could weigh on the EUR over the long run. Interestingly however, according to a POLITICO Poll, the Civic Coalition lead by Pro-European Donald Tusk, appears to have been making some gains at 30% but is still far away from the PiS’s 37%.On the monetary level, the ECB’s September monetary policy meeting minutes, stated that rising inflation-linked swaps “rates partly reflected an upward revision of investors’ core inflation expectations”, implying that market participants may be expecting inflationary pressures to persist in the long run. Furthermore, the minutes stated that “They viewed the data that had become available since July as, on balance, not supporting a further rate hike”, implying that given the Eurozone’s weakening economy, another rate hike may not be justified. On a macroeconomic level, Germany has revised its GDP forecast to decline by 0.4%, essentially indicative of a shrinking economy, which could further weigh on the EUR. Interestingly Germany’s ZEW figures which are due out next week, are expected to provide a glimmer of hope for the future, but also are expected to show that conditions on the ground for the largest economy in the Eurozone are deteriorating. The discrepancy in our opinion is interesting and warrants further attention, as it may provide insight into the general sentiment surrounding the current situation. Looking at what next week has in store for the EUR, we note also Eurozone’s Final HICP rate.

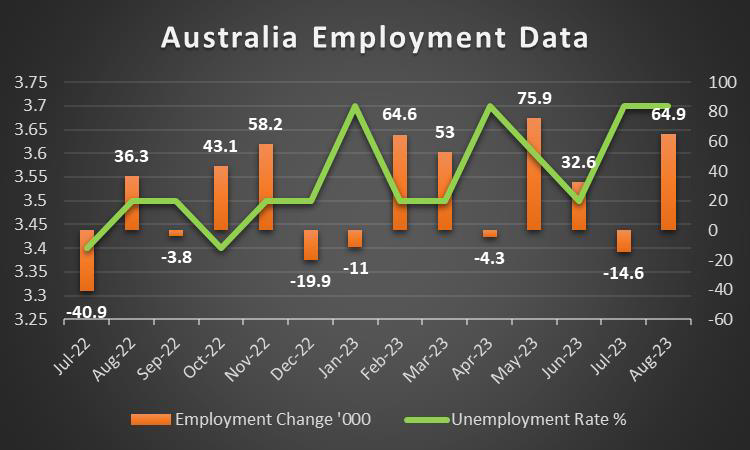

AUD – Australian employment data in focus

AUD is about to end the week lower against the USD. On a fundamental level, we note that PwC Australia’s Chief Executive apologised to Senators on Thursday in regard to the release of confidential tax documents that some PwC clients were given access to. Although the current issue may not affect the Aussie, it could negatively affect the companies that are currently embroiled in the controversy such as Google (#GOOG) and Meta (#FB).On a monetary level, it should be noted that RBA Assistant Governor Kent, stated that the RBA is in its “third phase” of monetary policy tightening and that the current stage is “an opportunity to see how the economy and how the data is evolving” and with the RBA’s October monetary policy minute meetings in sight, we may see a more dovish sentiment emerging, which could weigh on the Aussie. On the other hand, should the meeting minutes lean towards the hawkish side, we may see the Aussie gaining support. On a macro level, we note China’s trade data for September, which came in better than expected, implying that the Chinese economy is slightly gaining some momentum. However, despite the better-than-expected trade balance, their imports rate decreased. As such, given the Australian exports to China and the close Sino-Australian economic ties, we may the Aussie further weakening, as Chinese demand for overseas goods declines. For next week, we note Australia’s composite leading index rate for September and their Employment data. Should the Employment data indicate a resilient labour market, the case for another rate hike may emerge, which could support the Aussie. However, market participants are anticipating that the bank may remain on hold and should the employment data come in lower than expected, we may see that view re-iterated, which may weaken the Aussie.

CAD – Oil prices to continue swinging the Loonie

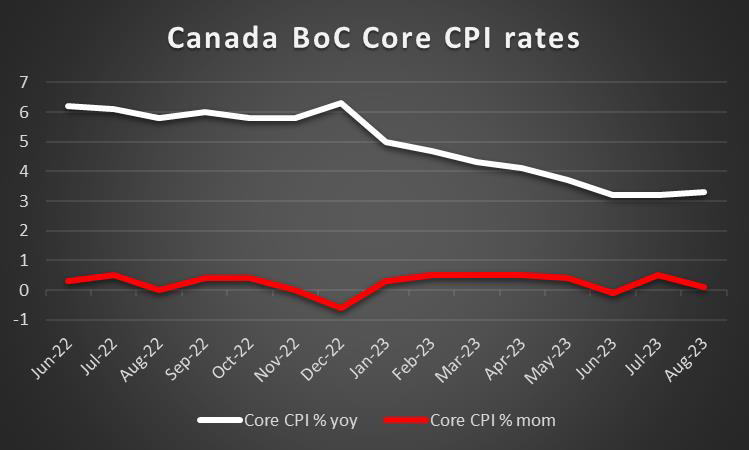

The Loonie is about to end the week relatively unchanged against the USD. On a fundamental level, we note that the Canadian diplomats in India have remained in the country as the deadline to withdraw has passed. The actions could potentially result in tensions between India and Canada flaring up once again and could further deteriorate the relationship between the two nations. However, we do not anticipate the souring of relationships to have a significant impact on the Loonie yet. On the monetary front, we note that the Bank of Canada seems to remain dovish for the foreseeable future, yet we note that market participants are anticipating a rate hike by the bank in March 2024. Although this may not be immediately transmitted to the FX markets, should the bank’s counterparts remain on hold, we may see the Loonie gaining support in the long run. On a macro level, we note that the Employment data for Canada came in better than expected, hinting at a resilient labour market in spite of high-interest rate levels, which may provide support for the Loonie, should it continue to improve. On a more fundamental level, we note that the rise in oil prices failed to substantially support the Loonie given that Canada is a major oil-producing economy. Based on recent market developments, we may anticipate that oil prices will rise further, especially in the scenario of the Israeli conflict escalating, a scenario that may support the Loonie in the coming week. We note the release of the manufacturing sales rate for August, the Housing starts figure for September and the Retail sales rate for August, which are due to be released next week and a possible acceleration may imply a more robust demand side in the Canadian economy.

General Comment

In the coming week, we expect that the USD may relent some of the initiative to other currencies and note that the GBP may gain additional influence in the FX market as the gravity of UK financial data seems to outtrump releases from other countries. As for US stock markets, we note that all three major US stock market indexes were in the greens for the week. We expect market attention to be increased for US stock markets in the coming week as the earnings season is about to begin. We note the release of the earnings reports of Goldman Sachs (#GS) and Lockheed Martin (#LockheedMT) on Tuesday, Morgan Stanley (#MS), Travelers (#TRV), Procter & Gamble (#PG), Tesla (#TSLA), Netflix (#NFLX) and Alcoa Corporation (#AA) on Wednesday, followed by AT&T (#T) on Thursday and finishing of the week is American Express (#AXP) on Friday. We also note the current developments in the Middle East with the conflict in Israel which may play a key role in the ascent of Gold should the current conflict spread regionally. Furthermore, should disruptions to the Oil supply from the region emerge, we may see the liquid gold gaining support, although no disruptions have taken place at the time of this report.

If you have any general queries or comments relating to this article please send an email directly to our Research team at research_team@ironfx.com

إخلاء المسؤولية:

لا تُعد هذه المعلومات نصيحة استثمارية أو توصية بالاستثمار، وإنما تُعد تواصلاً تسويقيًا. لا تتحمل IronFX أي مسؤولية عن أي بيانات أو معلومات مقدمة من أطراف ثالثة تم الإشارة إليها أو الارتباط بها في هذا التواصل.