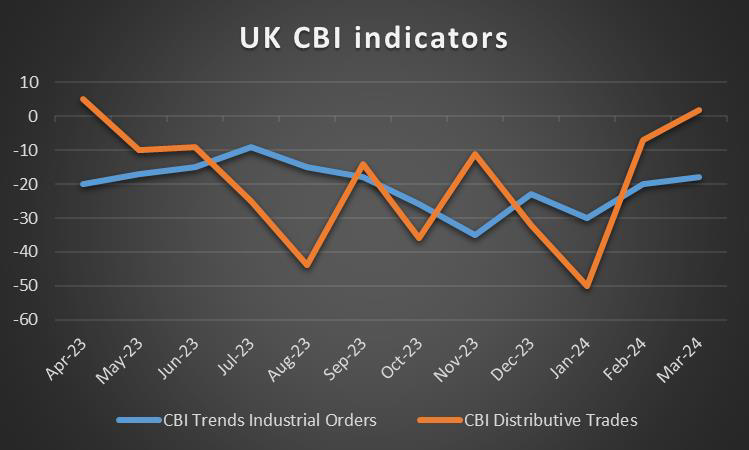

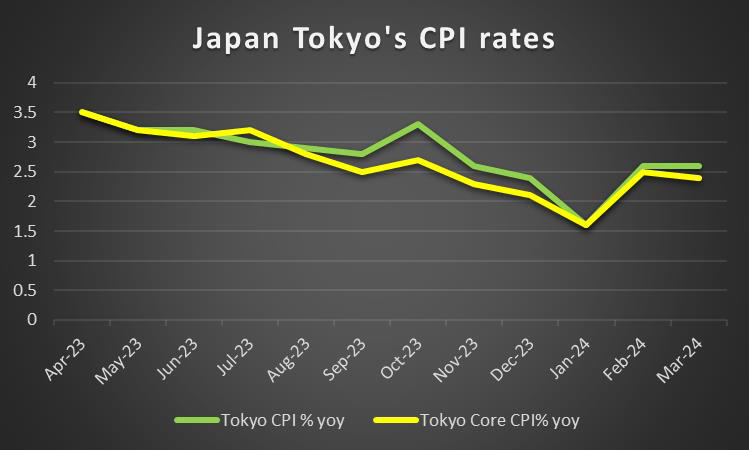

After a rough ride, we open a window to what next week has in store for the financial markets. On the monetary level, we note that BoC is to release its March meeting minutes on Wednesday, from Turkey CBRT is to release its interest rate decision on Thursday and the highlight is expected to be the release from Japan of BoJ’s interest rate decision. As for financial releases, on Monday we get UK’s CBI trends for industrial orders for April and Canada’s PPI rates for March. On Tuesday we get March’s preliminary PMI figures for Australia, Japan, France, Germany, the Eurozone as a whole, the UK and the US. On Wednesday we get New Zealand’s Trade data for March, Australia’s CPI rates for Q1, Germany’s Ifo indicators for April, the US durable goods orders for March and Canada’s retail sales for February. On Thursday we note the release of Germany’s Gfk consumer sentiment for May, UK’s CBI indicator for distributive trades for April, Canada’s Business Barometer for April and from the US the weekly initial jobless claims, as well as the highlight for the week the US GDP advance rate for Q1. Finally on Friday, we get from Japan, Tokyo’s CPI rates for April, Australia’s PPI rates for Q1 and from the US the consumption rate for March, the Core PCE price index for the same month and the final US University of Michigan consumer sentiment for April.

USD – Q1 GDP advance rate in the epicenter

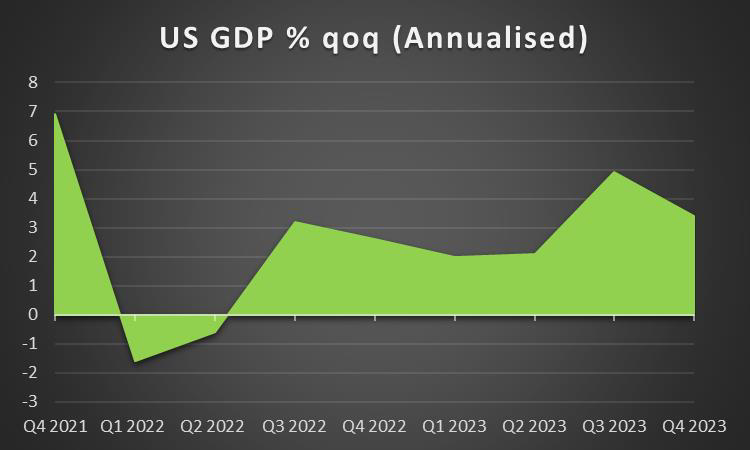

The USD is about to end the week with little change against its counterparts. On the monetary front, the hesitancy of Fed Policymakers to start cutting rates seems to intensify, given the persistence of inflationary pressures in the US economy. Powell’s comments underscored this unwillingness of the bank to ease its monetary policy as well as the stickier nature of inflation. We expect, the USD to remain supported over the coming week on a monetary level, yet we also note that the bank enters a statement moratorium period for its policymakers, two weeks ahead of the Fed’s next meeting on the 1st of May, which may allow analysts to lead the way. On a fundamental level, we note that the uncertainty in the markets caused by geopolitical issues such as the Iranian-Israeli conflict, but also others, may be providing safe-haven inflows for the greenback. On a macroeconomic level in the coming week, we highlight the release of the US GDP advance rate for Q1, and forecasts are for the rate to slow down if compared to the final release for Q4. The slowdown would be understandable given the tight financial conditions in the US economy and could weigh on the greenback, yet the rate is expected to steer clear from any recessionary levels and if so could provide some comfort. We would also like to note the release of the Fed’s favourite inflation metric, namely the Core PCE price index for March. Should the rate fail to slow down or even accelerate we may see the USD getting some support as it would add more pressure on the Fed to maintain its high rates for longer.

GBP – Financial data dispersed throughout the week

The pound is about to end the week unchanged against the USD, stronger against the JPY and weaker against the common currency. On a monetary level, we note the market’s expectations for BoE to start cutting rates in its August meeting and deliver two cuts in total for the year. BoE Governor Bailey’s statements over the past few days may have enhanced the prospect for rate cuts as he stated that he expects a strong drop of inflation in the UK economy in May. The comments tended to highlight the possibility of a rate cut possibly earlier than August. On the flip side, BoE policymakers Haskel and Greene seemed to cation the markets against any possible premature rate cuts thus burring the monetary policy outlook somewhat. On a fundamental level, we note that UK finance minister Hunt in statements he made in the past few days seemed to lean more on the expansionary side for the UK Government’s fiscal policy. The comments tended to touch not only the possibility of more rate cuts but also higher spending, especially for defence. Overall further signals for an expansionary fiscal policy may provide support for the pound. On a macroeconomic level, we have a number of releases from the UK in the coming week, yet we note the release of UK’s preliminary PMI figure for the services sector, given that the expansion of economic activity in the sector is key for the UK economy’s growth.

JPY – BoJ ‘s interest rate decision eyed

JPY is about to end the week lower against the USD, the EUR and the GBP, in a sign of wider weakness. Overall we have to note that the Japanese currency is quite weak, which may prompt the Japanese Government to intervene in the markets in support of JPY. Yet should the JPY’s weakness be caused by BoJ still rather loose monetary policy then the effect of a possible market intervention by the Japanese government may prove to be only temporary. On a fundamental level, we note JPY’s dual nature as a safe haven and a national currency. Hence should we see tensions and uncertainty on an international level being enhanced we may see JPY gaining some inflows. Yet in our opinion in the past few days, we see the interest rate differential and outlook being possibly the main issue weighing on the JPY. Hence we highlight the release of BoJ’s interest rate decision next Friday as the highlight of the week for JPY traders. The market is widely expecting the bank to remain on hold and currently JPY OIS implies a probability of 89.3% for such a scenario to materialise. Yet the market is expecting the bank to proceed with two rate hikes in the year. Should the bank remain on hold as expected, we may see market attention turning towards the release of the accompanying statement and the forward guidance included in it. We note that comments of BoJ policymakers in the past days, including BoJ Governor Ueda seem to caution the markets that the bank may maintain a more accommodative stance for the Japanese economy. Thus, should the bank, maintain a more dovish stance as we expect we may see the Yen weakening, as JPY traders may be somewhat disappointed, yet at the same time may also contradict the market’s expectations and thus could weigh on the JPY.

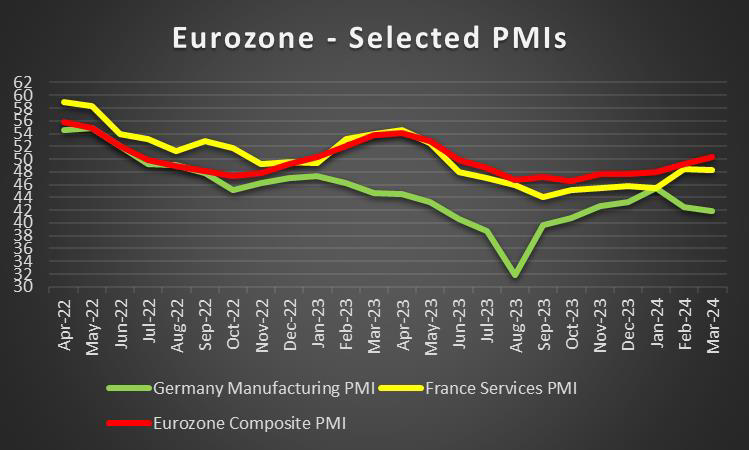

EUR – Preliminary PMI’s in focus

The common currency is about to end the week, halting its drop against the USD. Nevertheless, the EUR seems to end the week in the greens against the JPY and to a lesser extent against the GBP. On a monetary level, we note that ECB President Lagarde seemed to be leaning more on the dovish side as she stated that the bank may cut rates soon. The signals became even clearer as Germany’s Buba President and ECB Policymaker Nagel was reported stating that a June rate cut seems to be increasingly likely. Overall the bank may start cutting rates systematically first among major central banks and should we see more ECB policymakers, stressing such a scenario we may see the EUR losing ground against its counterparts as the interest differentials may widen against the EUR. On a fundamental level, we note that the Iranian and Israeli strikes tend to worry EUR traders, maybe a bit more than others as a possible escalation may have an adverse effect on the EUR area on a fundamental level. Please note that also the war in Ukraine is an ongoing factor of uncertainty for the area. On a macroeconomic level, we turn our attention towards economic activity and we highlight the release of the preliminary PMI figures for April. The problem child of the Zone remains Germany’s manufacturing sector which suffered a continuous contraction of economic activity. On the other hand, it seems that other countries in the block are countering the losses of economic activity for Germany.

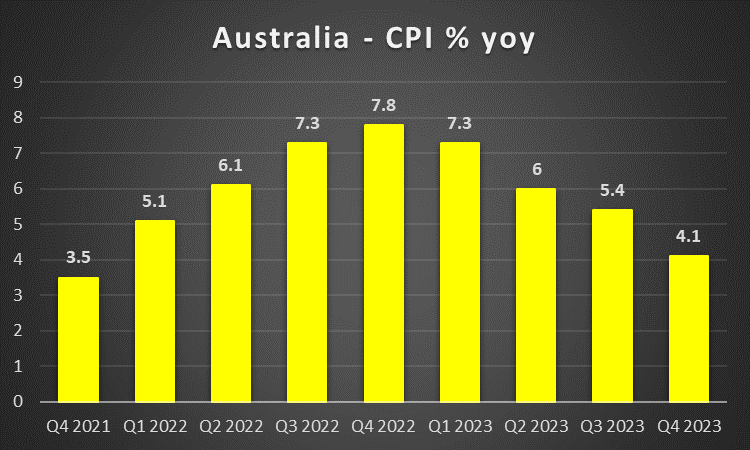

AUD – CPI rates to move the Aussie

AUD is about to end the week lower against the USD. On a monetary level, we note the Aussie’s sensitivity to the market sentiment given its riskier nature as a commodity currency. Should the market’s stance be more cautious in the coming week we may see the Aussie losing some ground on a fundamental level. Also on a fundamental level, we note the close economic ties of Australia and China and AUD’s sensitivity to developments in the Chinese economy. On a macroeconomic level, we note that China’s GDP rates were better than expected, which may have provided a boost of confidence for AUD traders. Yet on the flip side, we note the worsening Australian employment data for March with the employment change figure falling in the negatives and the unemployment rate ticking up. The release seems to be adding more pressure on RBA to start cutting rates. In the coming week, we highlight the release of Australia’s CPI rates for March and Q1. Should the CPI rates slow down even further, we may see even more pressure on RBA to start cutting rates. For the time being, we note that the market does not expect the bank to start cutting rates in 24. Should such expectations be enhanced in the coming week, we may see the Aussie getting some support on a monetary level.

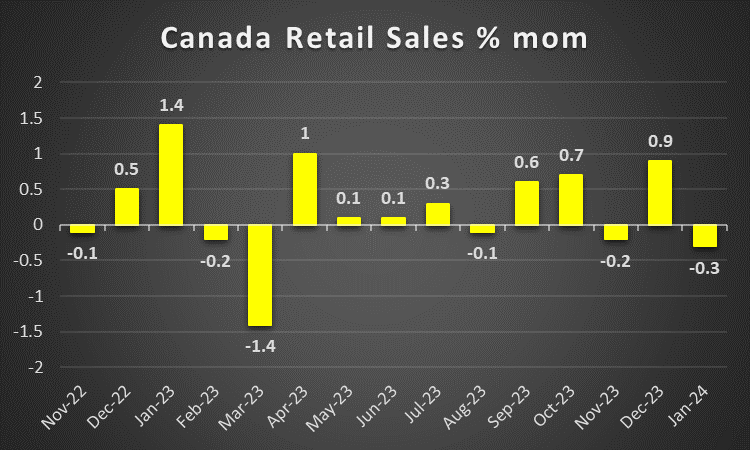

CAD – Fundamentals to lead the Loonie

The CAD is about to end the week slightly stronger against the USD. On a fundamental level, we note that the CAD could get some support should the market sentiment be more risk-oriented. Also, the direction of the CAD could be influenced by the path of oil prices. Oil prices are about to end the week in the reds and the main factors behind its movement may include also the conflict in the Middle East and a possible flare up could cause oil prices to rally. Overall the supply side of the international oil market seems to remain tight while there are hopes for a robust demand side in the oil market. Overall should oil prices start rising again, we may see the CAD getting some support as well. On a monetary level, we note the market’s expectations for BoC to start cutting rates from July onwards and deliver two rate cuts in total within the year. Yet as per BoC Governor Macklem’s comments, the bank seems to want inflationary pressures to ease further before starting to cut rates. Please note that at the release of the CPI rates for March, the market got some mixed signals, as the headline rate ticked up while the core rate ticked down. Yet we have to note that the CPI rates, both on a headline and a core level, are within the bank’s inflation target of 1%-3%. Hence on a macroeconomic level, we note the release of the retail sales growth rate for February on Friday and the PPI rates for March on Monday. Other than that we would expect fundamentals to lead the Loonie in the coming week.

General Comment

We tend to expect volatility in the FX market to ease in the coming week, given that the gravity and frequency of financial releases tends to ease. We may also see the USD relenting some of the initiative to other currencies in the FX market. As for US equities we note that the wider fundamental uncertainty in the markets in conjunction with the possibility of the Fed maintaining rates high for longer weighed and forced major US stock market indexes to end lower for a second week in a row. Furthermore, we note that the earnings season is in full swing. In the coming week, we intend to focus on the high-tech sector and note the earnings releases of Intel (#INTC), Microsoft (#MSFT), Google (#GOOG), Tesla (#TSLA), Meta (#META), IBM (#IBM), Amazon (#AMZN) among others. On the other hand, gold’s price was able to rise again and is about to be in the greens for a fifth week in a row. It should be noted that the negative correlation of the USD with gold’s price was not present in the current week, as Market uncertainty seems to be providing support on both trading instruments, while gold benefits more given the high amount of purchases of gold by central banks, especially the People’s Bank of China.

If you have any general queries or comments relating to this article please send an email directly to our Research team at research_team@ironfx.com

إخلاء المسؤولية:

لا تُعد هذه المعلومات نصيحة استثمارية أو توصية بالاستثمار، وإنما تُعد تواصلاً تسويقيًا. لا تتحمل IronFX أي مسؤولية عن أي بيانات أو معلومات مقدمة من أطراف ثالثة تم الإشارة إليها أو الارتباط بها في هذا التواصل.