The week is coming to an end and we take a peek at what next week has in store for the markets. On the monetary front we highlight the release of ECB’s interest rate decision on Thursday. As for financial releases, we get on Monday from Japan July’s current account balance for July and Q2’s revised GDP rate, from China August’s inflation metrics for August as well as Eurozone’s September Sentix index. On Tuesday we get Australia’s consumer sentiment for September, China’s August trade data, UK’s July employment data, Sweden’s GDP rate for the same month, as well as Norway’s and the Czech Republic’s August CPI rates. On Wednesday, we get UK’s GDP and manufacturing output growth rates for August. On Thursday we get New Zealand’s electronic card retail sales, Japan’s Corporate Goods prices and Sweden’s CPI rates all being for August, from the US we get the weekly initial jobless claims figure and the PPI rates for August and Canada’s July building permits growth rate.

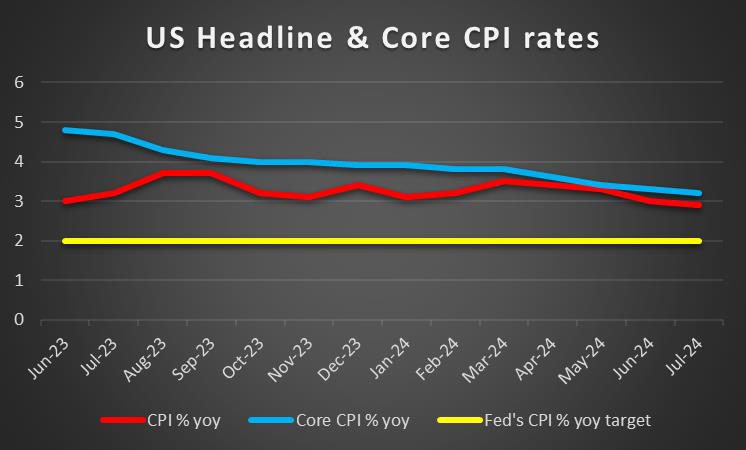

USD – US August CPI rates in focus

The USD edged lower against its counterparts during the week. We make a start for the USD by noting that the US August employment report with its NFP figure are still to be released later today and could alter the greenback’s direction. On a fundamental level, we note that negotiations between the US and China for a thawing of the tensions in their relationship are ongoing and the US is relationships could weigh on the USD as it could create safe haven outflows for the greenback. On a monetary level the market’s dovish expectations tend to intensify and its characteristic that it increasingly prices in a double rate cut in the September meeting. Fed Fund Futures currently imply a probability of 45% for such a scenario to materialise. On a macroeconomic level, we note that the ISM manufacturing PMI figure for August, despite improving showed another contraction of economic activity for the sector, thus stocking worries for growth. In the coming week we highlight the release of the US CPI rates for August and should the rates accelerate or even show a resilience of inflationary pressures in the US economy, it could contradict the market’s dovish expectations forcing the market to reposition itself and thus providing support for the USD and vice versa.

GBP – July’s GDP rates to be released

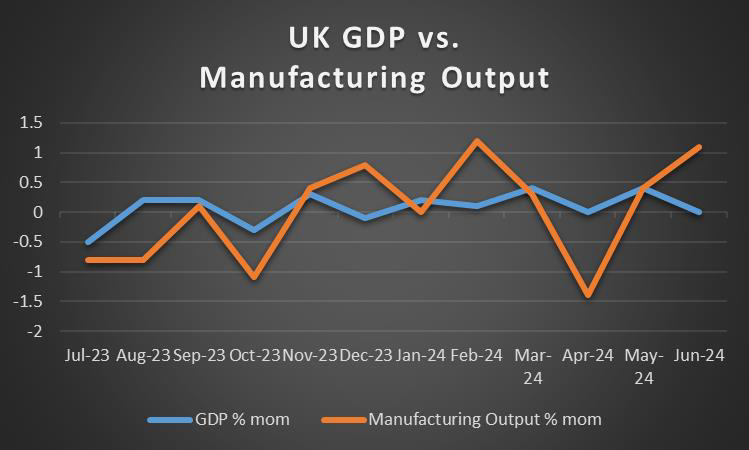

The pound seems to be edging lower against the USD for the week, yet that may be due to USD’s weakness rather than pound strength as the sterling is losing ground against the EUR and JPY as the week draws to a close. On a fundamental level for pound traders we note that the UK government plans to deliver a legal reform in employer-employee relationships. The Government’s Employment Rights Bill seems to enhance workers’ rights and introduces additional regulation in working relationships. In addition to that the UK government is also reported to plan introducing regulation in renting properties. The Renters’ Rights Bill is to remove the threat of arbitrary evictions and not allow landlords to make discriminations against families with children, as per Reuters. Such regulations could weigh somewhat on the pound. Also the possibility that the UK government may cut winter fuel payments for pensioners does not pose well for the Labour Government, indicates a tightening in fiscal policy and could also weigh on GBP. On the monetary front we note the market’s expectations for BoE to take a breather in next meeting and remain on hold and continue cutting rates from November onwards. Such market expectations could provide some support for the pound given the markets’ expectations for ECB and the Fed to continue/start cutting rates. On a macroeconomic level, in the coming week we highlight the release of the UK GDP rates for July. Should the rate accelerate, we may see the pound getting some support, as it would imply a faster expansion of the UK economy. Should also the industrial output of the manufacturing output growth rate accelerate for the same month the bullish sentiment for the pound could be enhanced. We also note the release of the UK July employment data and a possible tightening of the UK employment market could support the pound and vice versa.

JPY – Revised GDP rate in the epicenter

The Yen is gaining ground against the USD,GBP and the EUR in a sign of wider strength for the week. On a fundamental level, we note for JPY traders that inflation-adjusted wages rose for a second consecutive month July, albeit at a slower pace. Overall the growth of wages tends to support the resilience for inflationary pressures in the Japanese and strengthens the possibility that Bank of Japan may hike rates in the coming months. Currently as per JPY OIS the market seems to be pricing in the possibility of the bank remaining on hold in its next meeting in September but also in October and hike rates in the December meeting. Furthermore, BoJ Governor Ueda was reported by Bloomberg stating that the bank will continue raising interest rates should the economy and prices perform as expected by BoJ. The comment was perceived as hawkish by the market providing additional support for JPY. Overall we tend to view BoJ’s intentions towards it monetary policy as maybe the main factor

behind JPY’s direction. Also hawkish market expectations tend to weigh on carry trade with the JPY on the short side. Should market expectations for a possible tightening of BoJ’s monetary policy intensify we may see JPY getting some support. On a deeper fundamental level, we note the dual nature of JPY as a national currency and at the same time as a safe haven. Should we see market turning more cautious in the coming week, we may see JPY getting some support and vice versa.

EUR – ECB’s interest rate decision to shake the EUR

The single currency is losing ground against the JPY yet is wining against the USD and GBP. In the coming week, the main issue for EUR traders may be EXCB’s interest rate decision. The bank is widely expected to cut both the refinancing and deposit rate by 25 basis points. EUROIS imply a probability of 99% for such a scenario to materialise, rendering the interest rate part of the decision as an open and close case. The market also seems to expect marginally that the bank is to remain on hold in the October meeting and deliver another rate cut in the December meeting. Should the bank deliver next Thursday a rate cut as expected, we may see the market’s attention turning towards ECB’s accompanying statement and especially ECB President Lagarde’s press conference a bit later. Bearing in mind that the market expects at least one more rate cut until the end of the year should the accompanying statement and/or maintain a dovish tone, enhancing the market’s expectations we may see the common currency weakening. On the contrary should the bank show hesitation towards further easing of its monetary policy we may see EUR getting substantial support as the markets may be taken by surprise. On a fundamental level, we note that on the political spectrum that Macron picked Michel Barnier as the new PM of France, which may find resistance among French voters as the far left seems to be neglected. At the same time, the local elections in former East German states, where the far right made a decisive and impressive win, far left parties strengthened and the ruling parties sunk, also tend to intensify uncertainty for EU’s political outlook, which in turn could weigh on the single currency.

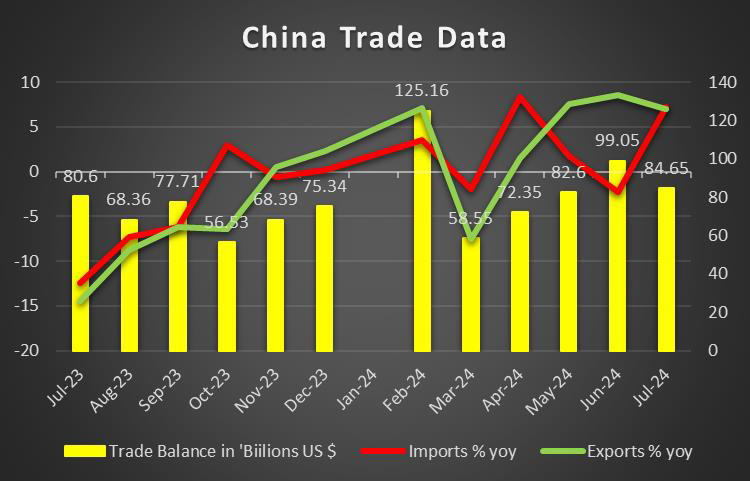

AUD – Fundamentals to lead the Aussie

AUD is losing ground against the USD as the week is ending. On a macroeconomic level, we note for Aussie traders that the GDP rate for Q2 edged lower, signaling a slowdown at which the Australian economy grew. In the coming week, there are no major financial releases on the calendar from Australia, yet we note the release of September’s consumer confidence and August’s business conditions and confidence. A possible improvement of the indicators’ readings could provide some support for the Aussie. On the other hand we also got China’s Caixin and NBS manufacturing PMI figures for August. The releases tended to send out mixed signals for economic activity in Chinese mega manufacturing sector, which may not pose well for Aussie traders as they maintain doubts about exports of Australian raw materials to China. In the coming week, highlight the release of China’s August trade data, with Aussie traders keeping a fixed eye on the import growth rate. A possible acceleration of the rate could provide some support for the Aussie. Yet on a deeper fundamental level, we also note that an escalation of tensions in the US-Sino relationships could weigh on the Aussie and vice versa. On a monetary policy level, the market seems to expect the bank to maintain rates unchanged until December at which point RBA is expected to proceed with a rate cut. RBA Governor Michelle Bullock seemed to be even more hawkish in her speech on Thursday as she warned that some Australians may have to sell their homes and that no rate cuts are likely in the near term. Overall RBA’s hawkish intentions may continue providing support for the Aussie given that other major central banks intend or have allready started to cut rates.

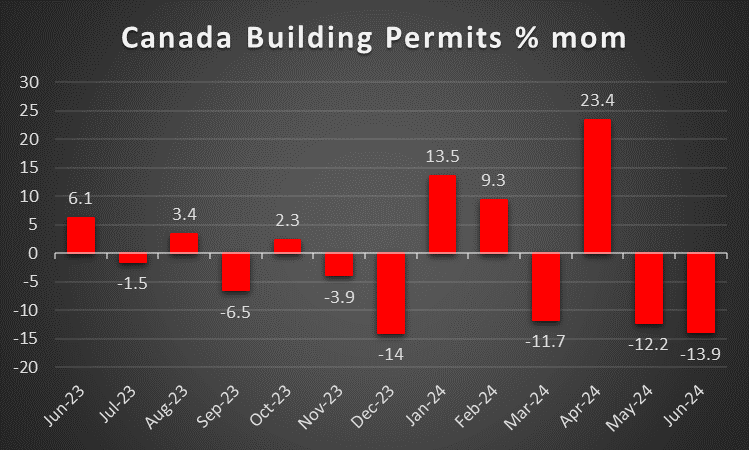

CAD – Fundamentals and oil prices to watch out for

The Loonie is about to end the week relatively unchanged against the USD, while we note that Canada’s employment data for August are still to be released in todays’ American session and could significantly affect the Loonies’ direction. Should the data point towards a tightening of the Canadian employment market in contrast to July’s data, we may see the Loonie getting some support. On a monetary policy level, we note that BoC cut rates as expected on Wednesday. In the accompanying

statement the bank mentioned that “Excess supply in the economy continues to put downward pressure on inflation” and that “Monetary policy decisions will be guided by incoming information and our assessment of their implications for the inflation outlook”. Overall the tone of the statement tends to lean on the dovish side. The market expects the bank to proceed with another two rate cuts until the end of the year. Hence we note the planes speech of BoC Governor Tiff Macklem on Tuesday and any dovish signals could weigh on the Loonie. On a fundamental level, we note that oil prices fell over the past week and should this tendency be maintained over the coming week, we may see the drop of oil prices weighing on the Loonie, given Canada’s status as a major oil producing country. On a macroeconomic level, we have a rather quiet week ahead, maybe with the exception of July’s building approvals growth rate on Thursday. Hence we expect fundamentals to lead the way for Loonie traders.

General Comment

As an epilogue we expect the USD to maintain the initiative over other currencies in the FX market, mainly due to the release of the US inflation metrics for August. Yet other currencies such as EUR could come under the spotlight, which in turn may enrich the trading mix. As for US stockmarkets, we note a uniform steep drop of Dow Jones, S&P 500 and Nasdaq despite some stabilisation near the end of the week. The drop signals that the bullishness of US stockmarkets seems to have been broken. We expect that both today’s US employment report release and Wednesday’s US CPI rates release both for August, could have an effect on the direction of US stockmarkets. Should the markets in the coming week have a more cautious approach, we may see it having an adverse effect on US stockmarkets and vice versa. As for gold’s price we note that the negative correlation of the precious metal’s price with the USD seems to have resurfaced in the past few days. The slight weakening of the USD seems to have benefited slightly gold’s price. Also the clear drop of US yields since the start of the week, tends to enhance the positive effect for gold’s price. At the same time we also note that gold remains near all time high levels, which may cause gold bulls cold feet as the precious metal’s price seems to be entering uncharted waters.

If you have any general queries or comments relating to this article please send an email directly to our Research team at research_team@ironfx.com

إخلاء المسؤولية:

لا تُعد هذه المعلومات نصيحة استثمارية أو توصية بالاستثمار، وإنما تُعد تواصلاً تسويقيًا. لا تتحمل IronFX أي مسؤولية عن أي بيانات أو معلومات مقدمة من أطراف ثالثة تم الإشارة إليها أو الارتباط بها في هذا التواصل.