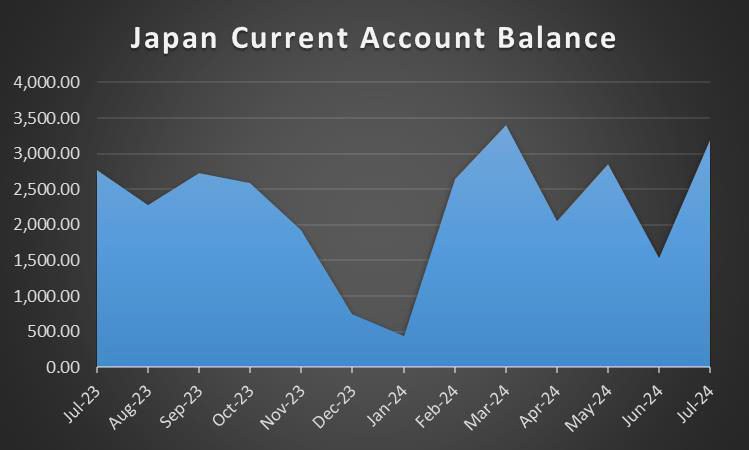

The week is about to reach its end as we open next week’s calendar. On the monetary front we note that RBNZ is to deliver its interest rate decision on Wednesday and RBA is to release its September meeting minutes on Tuesday. As for financial data, we note on Monday the release of Germany’s industrial output for August, UK’s Halifax House prices for September and Eurozone’s Sentix index for October. On Tuesday we get Japan’s Current Account balance for August, Australia’s Business Confidence and current conditions indicators for September, Germany’s industrial output for August and Canada’s trade data for the same month. On Wednesday we get Australia’s Consumer confidence for October, and on Wednesday we get Norway’s and the Czech Republic’s and most importantly the US CPI rates, all for September as well as the weekly US initial jobless claims figure. On Friday we get Germany’s final HICP rates for September, UK’s GDP and manufacturing output rates for August, the US PPI rates for September and Canada’s number of building permits for August and employment data for September as well as the preliminary US University of Michigan consumer sentiment for October.

USD – September’s CPI rates in focus

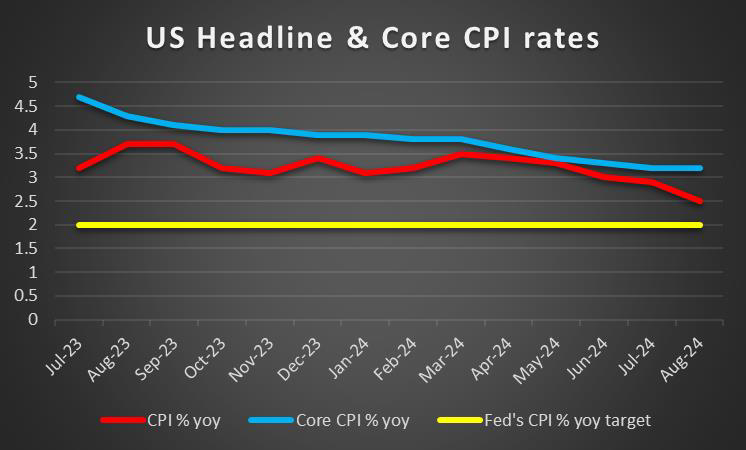

The USD seems to be gaining for the week against its counterparts maybe the most gains made in week since July, yet the US employment report for September with its NFP figure is still to be released and depending on the rates figures published could alter the USD direction. On the monetary front we note the Fed’s unwillingness to proceed with extensive rate cuts by the end of the year. Fed Chairman Powell’s speech was characteristic to that end and should Fed policymakers fall in line behind that tone in the coming week, we may see the USD getting some support as the market would have to reposition itself. On the fundamental level, we note the strike at east coast harbours which could weigh somewhat on the US macroeconomic outlook, yet the temporary deal reached eased the market worries. On the other hand, the race for the presidential elections is hot, with nor Trump nor Harris having a clear lead, especially in swing states. Last but not least we highlight the release of the US CPI Rates for September next Thursday and a possible easing of inflationary pressures could weigh on the greenback, as it could enhance market expectations for another double rate cut until the end of the year.

GBP – BoE Bailey’s comments weigh on the pound

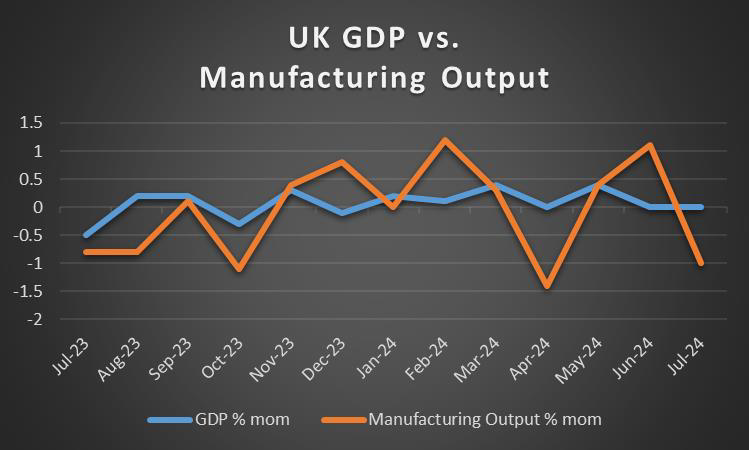

The pound is losing ground against the USD and EUR but not the Yen. On a monetary level for the pound, we would highlight BoE Governor Bailey’s comments yesterday. BoE Governor Bailey stated to the Guardian that BOE may become a bit more aggressive in cutting rates if news on inflation continues to be good. The comments weighed on the pound across the board at the time of the release and the prospect of faster rate cuts could weigh on the pound in the coming week as well, should other BoE policymakers imply it. On a fundamental level, we note that UK Prime Minister Starmer is travelling to Brussels in an effort to improve the UK-EU relationships and if an improvement is noted we may see the pound getting some support. As for financial releases we highlight next week the release of UK’s GDP rate for August and should the rate escape stagnation levels and accelerate, we may see the pound getting some support at the end of next week.

JPY – Japan’s new PM Ishida favors no rate hikes

JPY seems to be the loser of the week as it retreated against the USD, EUR and GBP. On a fundamental level, we note that on Wednesday Japan’s newly elected PM Ishida stated that the Japanese economic environment isn’t ready for another rate hike by BoJ. The comment was followed by a statement of BoJ Governor Ueda, expressing also some caution for further rate hikes, which in turn tended to fall in line with PM Ishida’s comment. Hence the prospect of an easing of BoJ’s hawkishness weighed on JPY. The event highlighted BoJ’s intentions, as maybe the main factor behind JPY’s direction and we expect

further comments of BoJ policymakers to be closely watched. No major financial releases are on the calendar for JPY traders next week, thus we may see fundamentals leading the way for the Yen. Last but not least we also note JPY’s dual nature as a safe haven and a national currency, hence should we see the market worries being enhanced in the coming week we may see JPY getting some support.

EUR – Eurozone’s economic outlook weighs on EUR

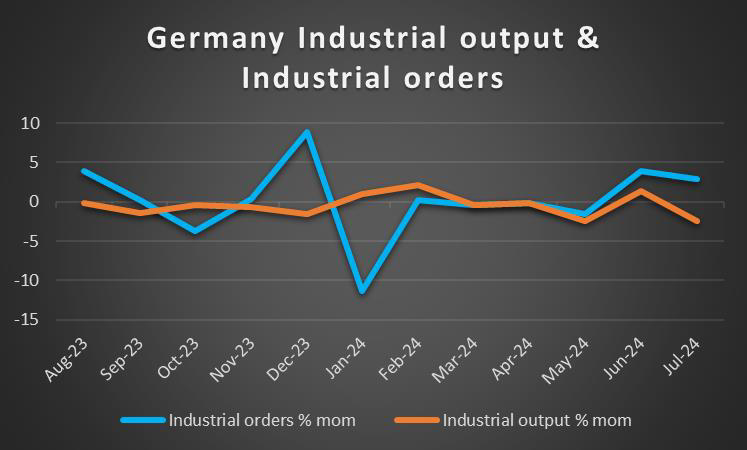

The common currency may be losing ground for the week, against the USD, yet is winning against the pound and the Yen. We make a start for EUR traders with ECB board member Schnabel’s comment that the ECB can’t ignore the headwinds to economic growth, adding that a sustainable fall in inflation to the 2% target is becoming more likely, as per Bloomberg. The impressive part may have been that the comment came from a well-known hawk of the ECB, thus the dovish message carried more weight among market participants. The news tended to reaffirm market expectations for another rate cut by the bank and should we see more ECB policymakers making dovish comments ECB’s monetary outlook could weigh on EUR. It should be noted that the HICP rates for September at a preliminary level, seem that the headline rate slowed down beyond market expectations yet at a core level, inflation seems to refuse to slow down considerably, which may not allow the ECB to curt rates as much as it would wish for. Furthermore the contraction of economic activity across sectors and member states was confirmed for September albeit maybe not as wide as initially expected. Yet our worries for a possible recession in the Eurozone are still present and we highlight Germany’s manufacturing sector as the patient of the area. On a deeper fundamental level the EU seems to be entering a cold trading war with China and we highlight that EU members are to decide on further tariffs on EVs. Such a possibility could weigh on the EUR as it could cause a more extensive trade war with China, which in turn may shrink economic activity, especially in the manufacturing sector, even further. In the coming week we intend to focus on the release of Germany’s industrial output and orders growth rates both being for August, but also on Eurozone’s Sentix index for October.

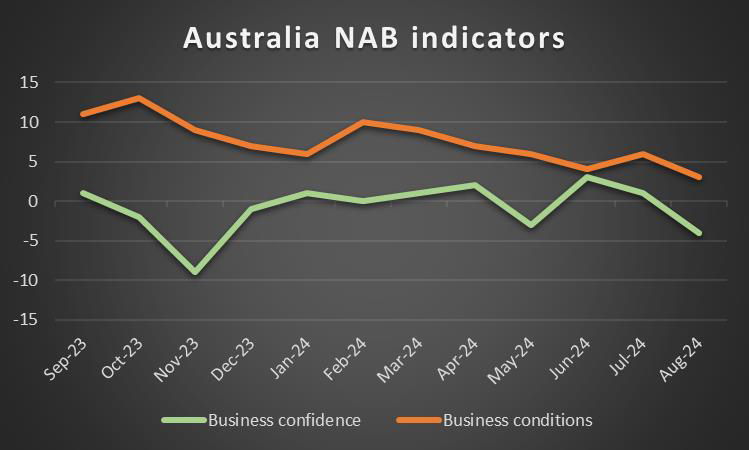

AUD – Fundamentals to lead the way

AUD is about to end the week in the reds against the USD. We note that we had a number of issues affecting the Aussie in the past few days. We make a start with the acceleration of Australia’s retail sales growth rate while the building approvals growth rate contracted beyond market expectations, both being for August. Yet given the close Sino Australian economic ties, we have concerns about China’s economic outlook. September’s manufacturing PMI figures showed another contraction of

economic activity in the huge sector. The outlook of the Chinese economy depends heavily at the current moment on the fiscal and monetary policy aid of the Chinese government and PBOC which tended to improve optimism for its outlook. In the coming week Aussie traders are expected to focus on fundamentals as, with the exception of Australia’s business conditions and confidence for September and consumer confidence for October, the calendar is empty of high impact financial releases from Australia and China. Hence an improvement of the market sentiment could support the Aussie given the market’s perception of it as a riskier asset given its commodity status and vice versa.

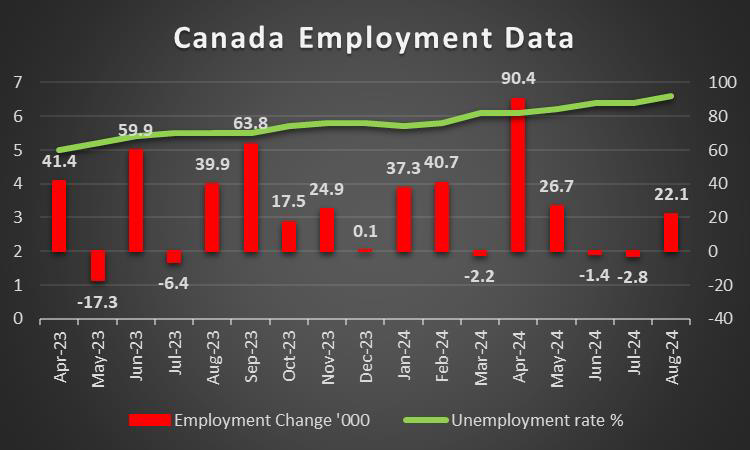

CAD – September’s employment data in the epicenter

Also the Loonie seems to be losing ground against the USD this week. CAD traders may be interested on a fundamental level on the path of oil prices, given the status of Canada as a major oil producing economy. Hence a possible additional rise of oil prices could provide support the Looney as well. On a monetary level, the market’s expectations for more rate cuts by BoC were enhanced over the past few days with the possibility of a double rate cut in the October or the December meeting being increased and weighing on the Loonie. As for financial releases, we highlight in the coming week the release of Canada’s employment data for September on Friday. Should the data show a tightening Canadian employment market we may see the CAD getting some support as the data would allow the BoC not to expedite its rate cutting path while a widening of the slack in the Canadian employment market could add more pressure on BoC for faster rate cuts and thus weigh on the Loonie.

General Comment

As an epilogue, we would like to make a comment for the situation in the Middle East that is currently tantalizing the markets. After Iran’s missile attack last Tuesday, Israel’s response is expected with the question of how hard the response will be looming over the markets. Should Israel target and destroy Iranian oil infrastructure such as the Khark Island, a major Iranian oil export hub, we may see oil prices getting a substantial boost, as market worries for the supply chains and a subsequent tightening of the international oil market, could intensify further. Yet the situation could get even worse should Israel choose to hit Iranian nuclear sites, a move Washington has warned Israel to avoid. The chances of the conflict escalating to a full blown regional war, are increasing, with the consequences, besides the humanitarian aspect that is tragic, on the international economy being possibly enormous. In such a scenario, prices of oil could reach easily beyond $100 per barrel which in turn could revive inflationary pressures in various oil importing countries and in turn force central banks to retighten monetary policy, thus leading to decreased economic activity, thus threatening to throw national economies into a recession once again.

If you have any general queries or comments relating to this article please send an email directly to our Research team at research_team@ironfx.com

إخلاء المسؤولية:

لا تُعد هذه المعلومات نصيحة استثمارية أو توصية بالاستثمار، وإنما تُعد تواصلاً تسويقيًا. لا تتحمل IronFX أي مسؤولية عن أي بيانات أو معلومات مقدمة من أطراف ثالثة تم الإشارة إليها أو الارتباط بها في هذا التواصل.