The week is slowly coming to an end, hence we open a window at what next week has in store for the markets. On a monetary level, we highlight the release of BoC’s interest rate decision on Wednesday and also note the release from China of PBoC’s interest rate decision on Monday and from Turkey, CBT’s interest rate decision on Tuesday. As for financial releases we make a start on Monday with the release of New Zealand’s trade data for June. On Tuesday we get Eurozone’s preliminary consumer confidence for July and on Wednesday we get the preliminary PMI figures of Australia, Japan, France, Germany, the Eurozone as a whole, the UK and the US for July and Germany’s GfK Consumer confidence for August. On Thursday we get Germany’s Ifo indicators and UK’s CBI trends for industrial orders, both being for July, UK’s CBI Business Optimism for Q3 and from the US we get June’s durable goods orders, the weekly initial jobless claims figure and we highlight the release of the GDP rate for Q2. On Friday, we get from Japan Tokyo’s CPI rates for July, and from the US the consumption rate and Core PCE price index, both being for June as well as the final University of Michigan consumer sentiment for July.

USD – Slight growth expected

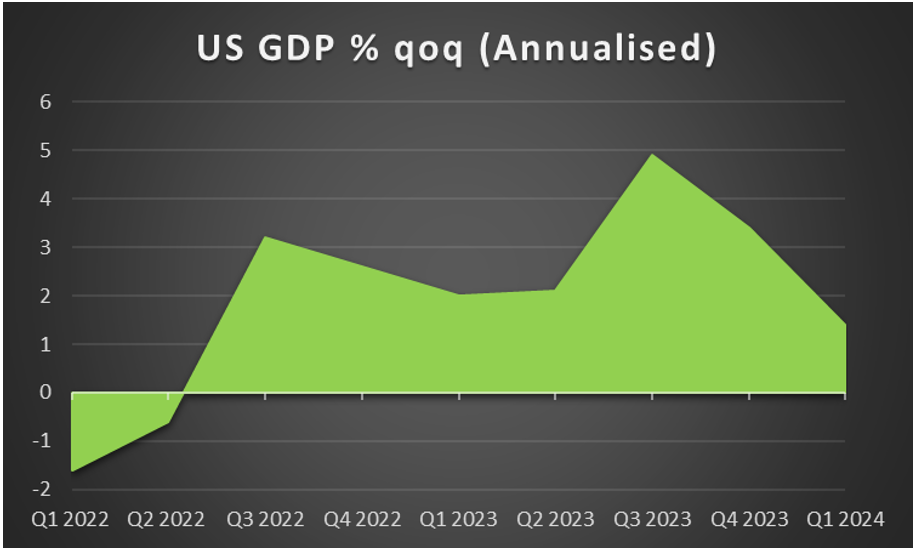

The USD is about to end the week relatively unchanged against its counterparts, given the correction higher on Thursday and today. On a fundamental level for the USD we note the heated US presidential preelection period. The failed assassination attempt on Trump changed the political scenery in the US, as it caused a rally around the flag effect for Trump supporters and enhanced his chances to win the elections. On the Democrat’s side, pressure for Biden to resign from the candidancy seem to be mounting and we may see developments for the issue unfolding in the next few days. Market wise the assassination attempt on Trump tended to enhance market epxectations for Trump to win and thus follow an expansionary fiscal policy, with deregulation and tax cuts being expected. The current market perception tends to support riskier assets as the market’s otpimism got a boost. On a macroeconomic level, we note that the Fed’s Beige Book showed that the bank expects the US economy to show slight economic growth, while inflationary pressures are expected to ease further. Hence we highlight the release of the US GDP advance rate for Q2 on Thursday where a slight acceleration is currently expected. On a monetary policy level, we note that despite some hesitancy, the balance of power within the Fed seems to be tipping towards rate cutting, which may be the main factor behind the weakening of the US currently. Yet we doubt that the bank is willing at the current stage to adopt the market’s expectations for three rate cuts before the year ends.

GBP – Stubborn inflationary pressures

Cable is about to end the week lower, and the pound is also weakening against the JPY and EUR, n a sign of wider weakness. On a macroeconomic level, we note the disappointing release of UK’s retail sales growth rates for June and highlight the stubbornness of inflationary pressures in the UK economy over the past month. It’s characteristic that the CPI rates remained unchanged at 3.5%yoy on a core level and at 2.0%yoy on a headline level. The failure of the CPI rates to ease could add more pressure on BoE to maintain rates high for longer, albeit on the flip side it should also be mentioned that the headline rate is at the bank’s 2% target which may provide some leeway for the bank to start cutting rates. It should also be mentioned that according to GBP OIS, the market seems to expect the bank to cut rates in the September and November meetings, which seems feasible should the CPI rates slow down over the summer. Should we see BoE policymakers make statements which could enhance the market’s expectations, we may see the sterling retreating. In the UK political scene we note that the newly elected PM Keir Starmer stated that the UK government will “take the brakes off” the economy. The new Government’s plans seem to be focusing on reviving the economy, New homes, infrastructure projects and resetting the UK’s relations with the EU among others. Yet at the same time, we note that UK PM Starmer warned that change will take time. Nevertheless the plans for an expansionary fiscal policy in the UK tend to be supportive for the pound. In the coming week, given the low number of high impact financial releases from the UK, we expect fundamentals to lead the way for the pound.

JPY – Market interventions support JPY

The main characteristic of the JPY may have been its strengthening across the board for the week, in a sign of wider strength. The strengthening of the JPY was maintained after last week’s market intervention by BoJ and Wednesday’s strengthening is characteristic of the tendencies within the market for JPY. We still view that there may be more way to go to push JPY higher for the BoJ in another possible market intervention, yet that remains to be seen. On a monetary level we note that the market’s expectations for the BoJ to hike rates in the September meeting. We note the release of June’s CPI rates during today’s Asian session which may have not accelerated as the market may have been expecting, yet displayed a relative resilience. Should we see a rise, or even a continuation of the resilience of inflationary pressures in the Japanese economy over the summer, we may see market expectations for such a rate hike in September intensifying. On a macroeconomic level, besides the allready mentioned CPI rates for June, we would also like to note that economic activity for the manufacturing sector has improved in July, yet that was not the case for the services sector, according to the relative Reuters Tankan indexes. Furthermore we also note the trade surplus for the past month, which was better than market expectations for the release of June’s trade data, highlighting the inflow of wealth in Japan from the country’s international trading activities. Last but not least and on a deeper fundamental level, we note that should we see uncertainty rising in the coming week we may see JPY getting some support as it is regarded as a safe haven instrument for financial markets.

EUR – Preliminary PMIs eyed

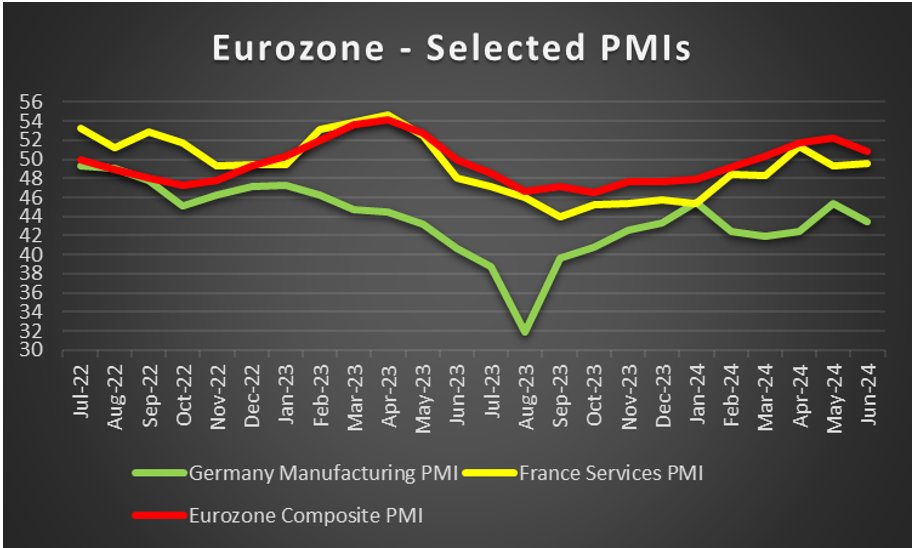

On a fundamental level for EUR traders we note that Ursula von der Leyen was re-elected as president of the European Commission amidst criticism from some member of the European Parliament. Ms. Von der Leyen seems to have expansionary plans as she is supporting the strengthening of the defence sector, affordable housing, green transition and tackling the immigration problem. Overall, intentions for expansionary fiscal policies may provide some support for the EUR. On a monetary level, we note that ECB as was widely expected remained on hold keeping the refinancing rate at 4.25% and the Deposit rate at 3.75%. The bank in its forward guidance and ECB President Lagarde’s press conference later on, left the possibility of a rate cut in the September meeting as wide open. Hence should we see ECB policymakers in the coming days implying that a rate cut in the coming meeting is possible, we may see the EUR weakening. On a macroeconomic level, in the coming week, we highlight the release of the preliminary PMI figures for July. We focus on the readings for France’s services sector, Germany’s manufacturing sector and for a rounder view Eurozone’s composite indicator. We tend to continue to view Germany’s manufacturing sector as the problem child of Eurozone’s economy, given that it continues to contract. Yet we also note that other sectors in the rest of the Eurozone seem to make up for the lost ground as the Composite PMI figure for the Eurozone shows expansion of economic activity. Should the readings of the PMI figures show improvement of economic activity in the Eurozone, we may see the common currency getting some support.

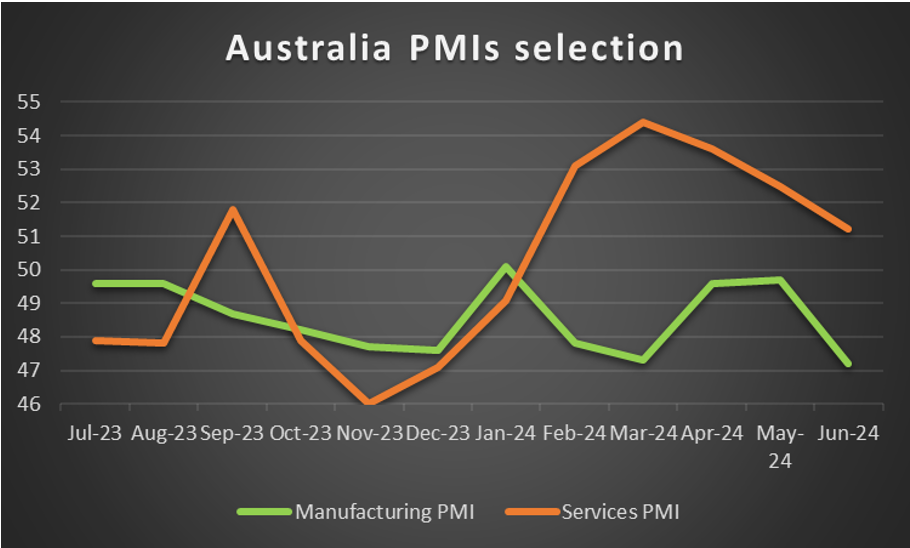

AUD – Fundamentals to lead the Aussie

AUD seems about to end the week in the reds against the allready weak USD, breaking a winning streak of five weeks. On a macreconomic level, we note that Australia’s employment report for June tended to sent out some mixed signals as on the one hand there was an impressive, beyond market expectations, rise of the employment change figure while on the other hand, the unemployment rate ticked higher, clipping the enthusiasm of Aussie traders. Nevertheless the release tended to support AUD at the time. Given the low number of high impact financial releases from Australia next week, we expect fundamentals to lead the way for Aussie traders. We also note the deep economic ties between Australia and China on a fundamental level. Hence we highlight last Monday’s release of China’s GDP rates for Q2 along with other data. The GDP rate for Q2, and the retail sales for June slowed down beyond market expectations but also the urban investment and the industrial output growth rates decelerated, while house prices contracted deeper, all being for June, enhancing worries for the recovery of the Chinese economy. Calls for supportive measures by the People’s Bank of China have intensified, yet we do not expect any movement in PBoC’s interest rate decision on Monday. Any measures to support the Chinese economy by PBoC could provide some support for AUD. On a deeper fundamental level, we note that the Aussie is viewed as a risky asset given also its commodity nature, hence should we see the market sentiment turning more cautious we may see an adverse effect on AUD.

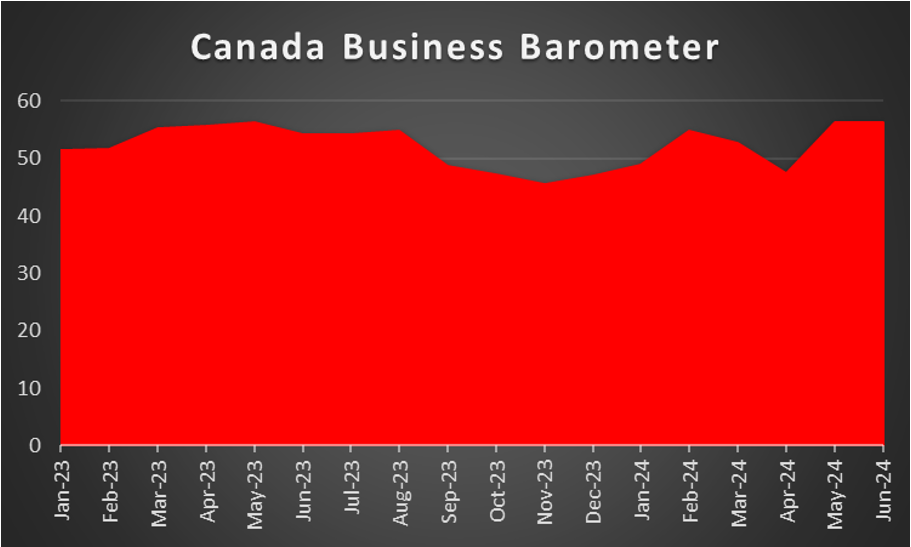

CAD – BoC’s interest rate decision in focus

On a macroeconomic level, we note for the Loonie, that Canada’s CPI rates for June on a headline level eased, yet on a core level ticked up, sending some mixed signals. The release tends to highlight the release of BoC’s interest rate decision next Wednesday. The bank is expected by the market to remain on hold and is characteristic that CAD OIS currently imply a probability of 94.75% for such a scenario to materialise. Should the bank remain on hold as expected, it may have a slight bullish effect on the Loonie, yet we also highlight the release of the accompanying statement which is to include the bank’s forward guidance which may be the main determinant factor for the Loonie from the release. Should the forward guidance try to prepare the markets for a imply that more rate cuts are to come, we may see the bearish effect intensifying. At this point we would like to note that rumours for a possible rate cut by the bank on Wednesday are wide spread and macroeconomically one could make the argument for another rate cut after the June one, given the easing of the headline rate and the and rise of the unemployment rate. Should BoC actually cut rates instead remaining on hold, we may see the Loonie losing ground, while if a dovish accompanying statement is added to the decision it could magnify the effect. On a fundamental level, we note that positive corelation of oil prices with the Looney, given Canada’s status as a major oil producing economy. Should we see oil prices falling in the coming week, we may see them having also a bearish effect on the Looney.

General Comment

As a closing comment, in the FX market we expect the USD to expand its influence over other currencies as the frequence and gravity of US financial releases intensifies. Nevertheless, there are days in the calendar that could allow for other currencies to get the initiative and form their own course, thus creating a more balanced trading mix for market participants. As for US stockmarkets, we note that the earnings season is in full swing. We tend to focus on the tech sector next week as we get the earnings releases of Microsoft (MSFT) and Alphabet (GOOGL) on Tuesday, IBM (IBM) on Wednesday and Amazon (AMZN) on Thursday. On a fundamental level, market worries for the tech sector were intense in the past few days as the Biden administration told allies that it’s considering using the most severe trade restrictions to China regarding semiconductors. The outage of Microsoft tended to intensify worries. Should the market worries intensify further in the coming week, we expect the adverse effect on tech shares to widen. As for gold prices we note that the negative correlation of the USD with gold’s price, seems to be in effect in the past few days despite gold’s price being about to end the week near the levels it began. The drop of US yields over the past week seems to have polished the shiny metal making it more attractive. Should the USD weaken further over the coming week, we may see Gold’s price reaching new record highs.

If you have any general queries or comments relating to this article please send an email directly to our Research team at research_team@ironfx.com

إخلاء المسؤولية:

لا تُعد هذه المعلومات نصيحة استثمارية أو توصية بالاستثمار، وإنما تُعد تواصلاً تسويقيًا. لا تتحمل IronFX أي مسؤولية عن أي بيانات أو معلومات مقدمة من أطراف ثالثة تم الإشارة إليها أو الارتباط بها في هذا التواصل.