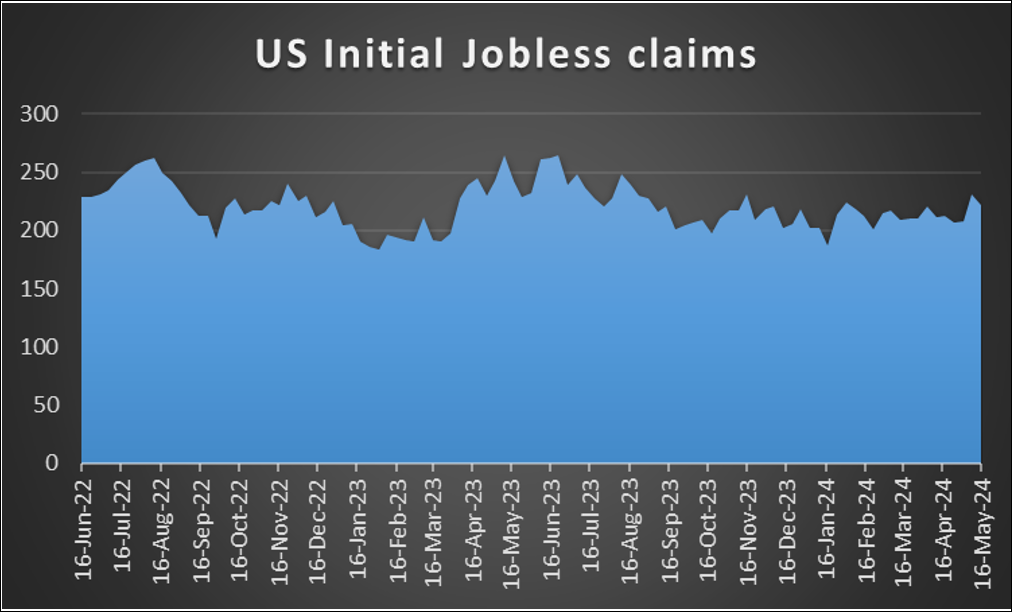

The week is slowly drawing to a close as we open a window at what next week has in store for the markets. On the monetary front, we note the release of RBA’s and the Fed’s last meeting minutes on Tuesday and Wednesday respectively, while the PBoC is to release its interest rate decision on Monday and from Turkey we await CBT’s interest rate decision on Thursday. As for financial releases, we note on Monday UK’s Rightmove House Prices for May and on Tuesday we highlight the release of Canada’s CPI rates for April. On Wednesday we get Japan’s machinery orders for March and UK’s CPI rates for April, while on a busy Thursday, we note the release of the preliminary PMI figures for May of Australia, Japan, France, Germany, the Eurozone, the UK and the US and we also get the weekly US initial jobless claims figure and Eurozone’s preliminary consumer confidence for May. On Friday we get New Zealand’s trade data, Japan’s CPI rates, UK’s retail sales and the US Durable goods orders growth rates, all being for April, Canada’s retail sales for March, Germany’s detailed GDP rate for Q2 and the final US University of Michigan consumer sentiment for May.

USD – Fed’s meeting minutes in the center of attention

The USD is about to end the week lower against its counterparts. On a macroeconomic level, the USD took a hit on Wednesday, by the release of the US inflation report for April. Both the headline and core rates slowed down a bit refreshing the market’s hopes for the possibility of the Fed easing its monetary policy rather sooner than later. Yet the slowdown despite being noted, in our opinion, may have not been wide enough to calm the Fed’s worries for the sticky inflation in the US economy and allow the bank to proceed with any rate cuts. Hence, on a monetary level, we may see Fed policymakers swaying the market’s mood with their statements but we expect that the market may prefer to focus on the release of the Fed’s last meeting minutes on Wednesday for more clues regarding the Fed’s intentions. Should the document underscore the determination of the bank to maintain a tight financial environment by keeping rates high in order to curb inflationary pressures in the US economy, we may see the USD getting some support as it may contradict the market’s expectations. On a political level, the pre-election period in the US is moving along strongly with Biden and Trump agreeing on debates in June and September. The US presidential elections tend to intensify the polarization in the US society, yet for the time being without any impact on the markets. On a deeper fundamental level, we note the US government’s intentions to hike tariffs on imports from China and Beijing’s angry response and the whole issue could provide some safe-haven inflows for the USD should tensions escalate further.

GBP – UK financial data to shake the pound

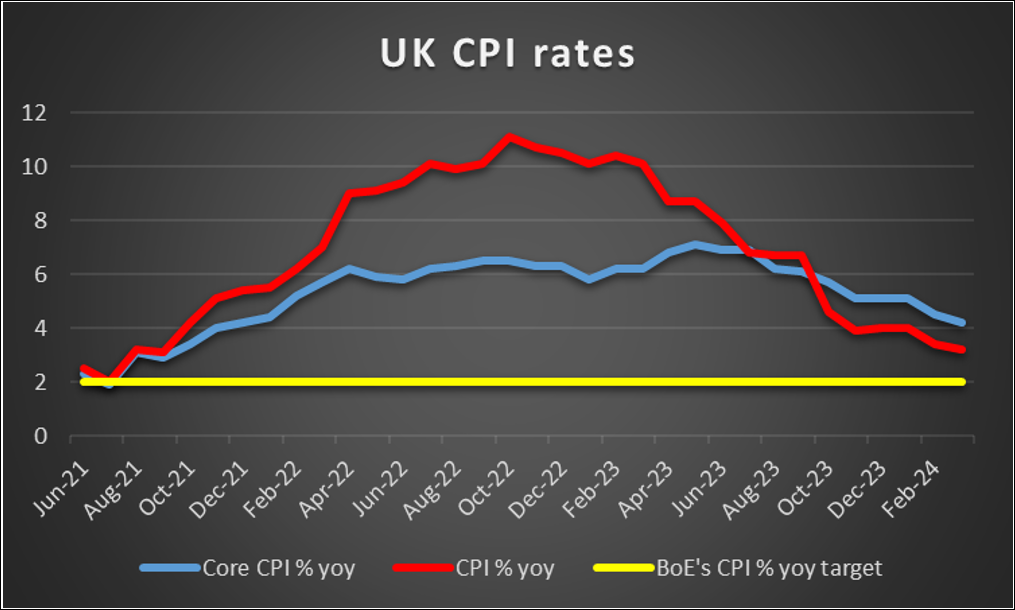

The pound is about to end the week stronger than the USD, the JPY and the EUR in a sign of relative strength. For pound traders, on a macroeconomic level, we note the slack in the UK employment market as dictated by the UK employment data for March, which were released last Tuesday. The unemployment rate ticked up, while the employment change figure dropped deeper into the negatives, albeit not as much as expected. In the coming week we highlight the release of the UK inflation metrics for April and expectations for further easing of inflationary pressures in the UK economy are present among market participants. Should the rates fail to slow down, or even accelerate, we may see the pound getting some support as BoE’s narrative for further deceleration of the CPI rates will be contradicted and it would be adding more pressure on the bank to keep rates high. On an economic activity level, we note the release of the preliminary PMI figures for May with the UK services sector being eyed by the market, while the demand side of the UK economy is to be gauged by the release of the retail sales growth rate for April on Friday. On a monetary level, we note the market’s expectations for a 25 basis points (bp) rate cut in the June meeting and should they be maintained we may see them weighing on the pound. On a fundamental level, the UK pre-election period is warming up with UK PM Rishi Sunak warning about the dangers ahead, yet the polls still show that Labour is leading.

JPY – Japan’s April CPI rates eyed

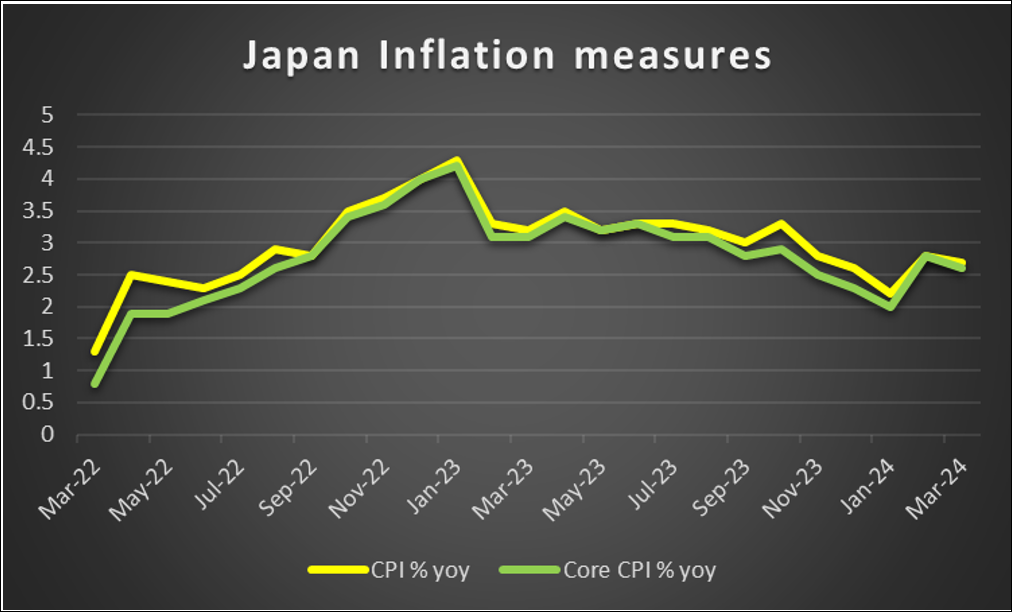

The JPY is about to end the week relatively unchanged against the allready weak USD, but also the EUR and GBP in a sign of wider weakeness. Japan’s macroeconomic outlook darkened after the release of the GDP rate for Q1. The release showed a wider-than-expected contraction of the Japanese economy at the rate of -2.0% yoy for the past quarter. The release highlighted the difficulties faced by the Japanese economy. Yet the release may have had a side-effect on a monetary level as well. The release implied that it may prove to be difficult for BoJ to proceed normalising further its monetary policy by hiking rates, as it may have an additional adverse effect on the growth of the Japanese economy. Yet we have to note that BoJ’s mandate does not include promoting economic growth as such, yet given the close ties with the Japanese Government some difficulties towards more rate hikes may emerge. For the time being the market seems to expect the bank to proceed with another two 10 bp rate hikes within the year, starting in the July meeting. Yet JPY remains at rather week levels given the market sell-off it suffered three weeks ago. Hence in the coming week, we note the release of Japan’s CPI rates for April, on Friday. Should the rates slow down the release may add more pressure on BoJ to remain on hold as there would be additional signs that inflation is easing. On a fundamental level, let’s not forget that another market intervention by Japan to the Yen’s rescue, is always possible should JPY slip even lower. Also on a fundamental level, we note JPY’s dual nature as a safe haven and a national currency. Should the tensions in the US-Sino trade relationships escalate further we may see the Yen gaining some safe haven inflows.

EUR – May’s Preliminary PMI figures in focus

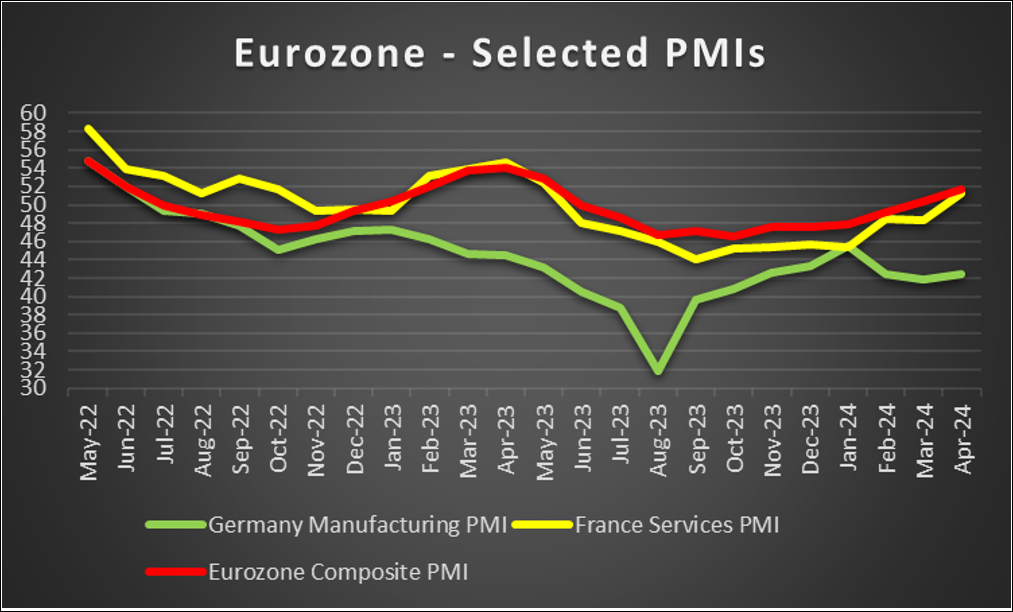

The common currency is about to end the week in the greens against the USD and the JPY but not the pound. On a fundamental level, and despite not affecting the path of EUR prices, we note the assassination attempt on Slovakia’s Prime Minister Robert Fico. Slovakia’s Prime Minister is now described as being in a stable but critical condition after the shooting and a man was arrested and despite being considered as politically motivated was also described as a “lone wolf” by media, containing the issue somewhat. Yet the assassination attempt as such tended to highlight the political polarisation within Europe as the victim was not in support of Ukraine, in contrast to EU’s stance and in general seemd to be in odds with Brussells. The war continues to be a source of instability for the EU, on its southeastern flank and on a fundamental basis tends to be more of a burden for the EUR. Also, the nearing elections for the new EU Parliament, tend to provide some uncertainty for the path of the area ahead. On a monetary policy level, the market’s expectations for the bank to start cutting rates in its June meeting seem to be present and tend to weigh on the EUR as the bank is expected by the market at the current stage to cut rates three times within the year. On a macroeconomic level, we note that in Germany the economic sentiment improved in the current month as did the conditions on the ground for the largest economy of the Eurozone. The GDP rate for Q1 remained unchanged in the positives, which was another positive for Eurozone’s economy as it seems to avoid a possible recession. In the coming week, we intend to focus on the release of the preliminary PMI figures for May and especially the indicator for Germany’s manufacturing sector, a sector that remains maybe the problem child of the Zone. Should the indicators show growth or a faster expansion of economic activity in the Eurozone, we may see the common currency getting some support.

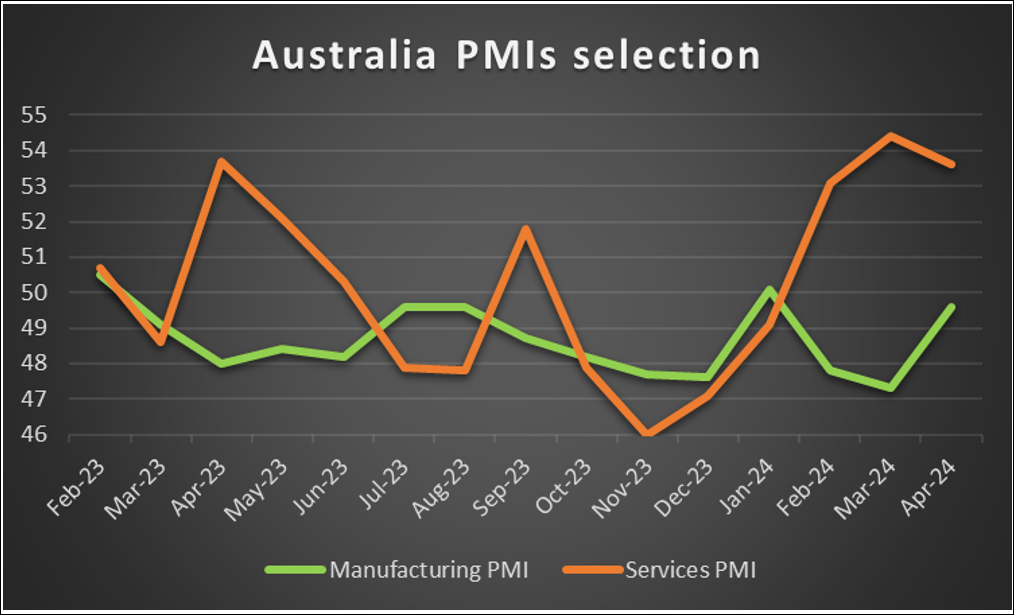

AUD – Fundamentals to lead the Aussie

AUD is about to end the week stronger than the USD. Yet the Aussie took a hit on Thursday’s Asian session, as the release of Australia’s employment data for April showed an unexpected rise of the unemployment rate to 4.1%. On the flip side, the employment change figure rose significantly and beyond market expectations reaching 38.5k easing the blow somewhat. The release tended to add more pressure on RBA to start cutting rates in order to ease the tight financial environment of Australia. Hence we expect Aussie traders to keep a close eye on the release of RBA’s last meeting minutes. Should the document show some hesitation on behalf of the bank to maintain rates at high levels, then we may see the Aussie slipping while on the contrary should the document show that RBA policymakers continue to prioritise the curbing of inflationary pressures in the Australian economy and thus may keep rates at high levels, we may see AUD gaining some ground. On a more fundamental level, we note also the riskier nature of AUD as a commodity currency. Hence, should the market sentiment in the coming week turn more cautious we may see AUD slipping while a more risk-oriented market approach could benefit the Aussie. Also given the close economic ties between China and Australia, Aussie traders tend to keep a close eye on the release of Chinese data, like China’s industrial output during today’s Asian session. On a more fundamental level, the additional tariffs which are to be placed on imports from China by the US Government, could have an adverse on AUD in the coming week should tensions in the US-Sino relationship escalate further.

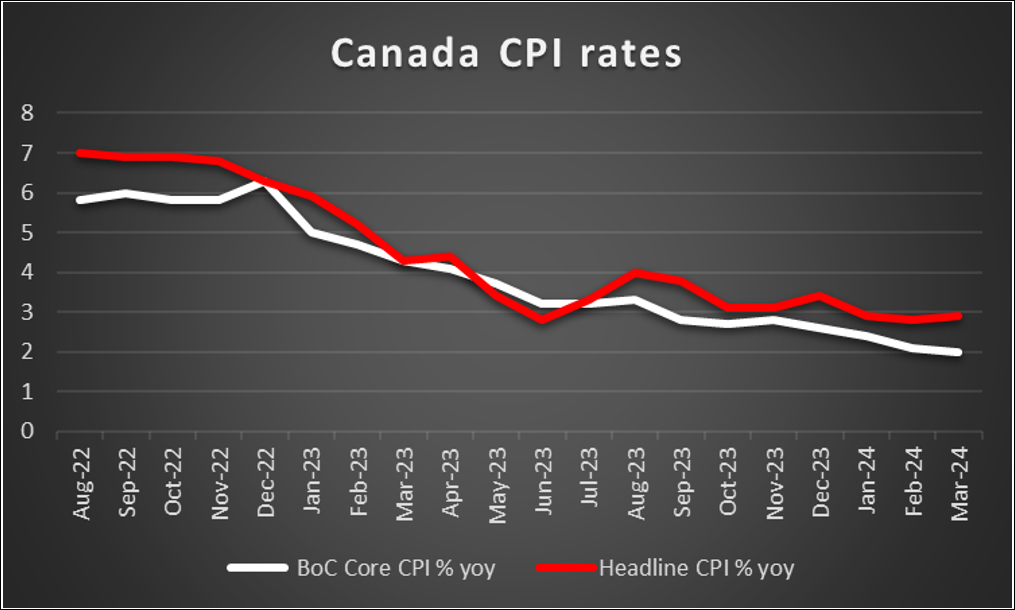

CAD – Canada’s CPI rates could move the Loonie

It was a rather easy going week for Loonie traders with fundamentals leading the way. Overall the improved market sentiment tended to support the risky commodity currency CAD and we expect that should the improved market sentiment be maintained in the coming week as well, we may see the CAD getting additional support. Also on a fundamental level, we note that oil prices seem to have remained rather rangebound in the past few days, which may have not been so helpful for the Loonie. Given Canada’s status as a major oil-producing economy, should oil prices start rising we may see the Loonie also getting some support in the coming week. Main narratives surrounding the path of oil prices tend to include the mixed signals from the US oil market, the uncertainty on whether Iraq is to follow OPEC’s voluntary oil production cuts and the different outlooks about oil demand at an international level, as provided by OPEC and IEA. On a macroeconomic level, we note the release of Canada’s CPI rates for April on Friday and a possible acceleration of the rates could provide some support for the CAD as it could signal the persistence of inflationary pressures in the Canadian economy. In turn, such an acceleration could add more pressure on Bank of Canada and avoid any rate cuts.

General Comment

As closure and in a more general note, we expect in the FX market the USD to ease further its influence over other currencies. In turn that may allow for a more balanced trading mix to emerge as other currencies may take the spotlight at certain points. On the other hand, US stock markets seem to have benefited from the improved market sentiment. It’s characteristic that all three major US stock market indexes are about to end the week in the greens with some reaching new record high levels. The earnings season is slowly drawing to a close yet we would like to point out the release of Nvidia’s (#NVDA) earnings report net Thursday that could generate considerable interest among traders. Should the positive market sentiment be maintained we may see additional support for US stock markets building up. Also, we note that the negative correlation of the USD with gold’s price being present this week, given the weakening of the USD and the rise of the precious metal’s price. We expect the negative correlation of the two trading instruments to be maintained and should the USD slip further, we may see gold’s price getting additional support.

If you have any general queries or comments relating to this article please send an email directly to our Research team at research_team@ironfx.com

Disclaimer:

This information is not considered as investment advice or an investment recommendation, but instead a marketing communication. IronFX is not responsible for any data or information provided by third parties referenced, or hyperlinked, in this communication.