As the week is drawing to a close and the summer holiday season is settling in we have a look at what next week has in store for the markets. On Monday we note Norway’s CPI rates for July and GDP rates for Q2. On Tuesday we get from Australia, RBA’s interest rate decision, UK’s employment data for June, Germany’s ZEW indicators for August, Canada’s building permits for June and we highlight the release of the US CPI rates for July. On Wednesday, we get Japan’s Corporate Goods Prices for July and on a packed Thursday we note the release of Australia’s employment data for the same month, UK’s GDP rates for June and Q2, Sweden’s CPI rates for July, Norway’s Norgesbank interest rate decision, Euro Zone’s revised GDP rate for Q2 and industrial output for June, the weekly US initial jobless claims figure and the US PPI rates for July. Finally on Friday we get Japan’s GDP rate for Q2, China’s industrial output, Urban investment and retail sales all for July, the US retail sales also for July, Canada’s manufacturing sales for June , the US industrial production for July and the preliminary UoM consumer sentiment for August.

USD – July’s US CPI rates to dominate

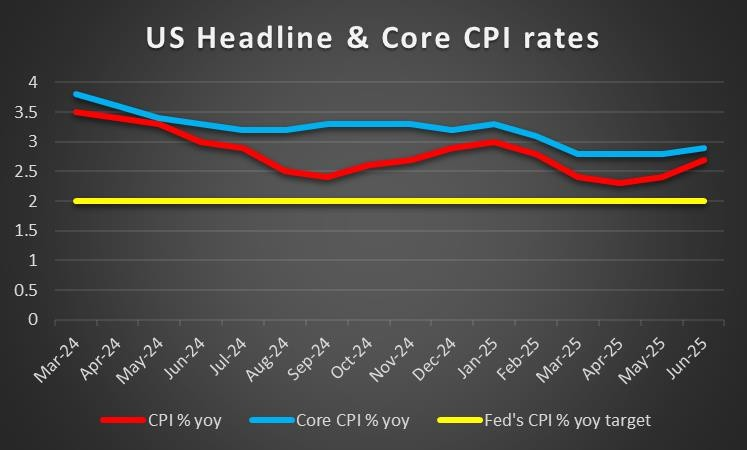

On a macro level, the shock of the week was last Friday as the US employment data for July intensified the worries for the US employment market as the NFP figure dropped beyond market expectations, while the unemployment rate ticked up. Furthermore the NFP figures of May and June were revised lower by a massive aggregated 258k, highlighting the rapidly deteriorating conditions in the US employment market. Also we note the drop of the ISM non-manufacturing PMI figure for July last Wednesday, which tends to intensify the worries for the US economic outlook, especially if paired with its sister indicator’s drop (ISM manufacturing PMI figure). In the coming week, we highlight the release of the US CPI rates for July and a possible acceleration of the rates could imply a persistence of inflationary pressures in the US economy thus easing the market’s current dovish expectations and thus support the USD. The effect could be magnified should also the PPI rates for the same month accelerate, thus providing more depth to the US inflationary pressures. On Friday, market attention is expected to be placed on the release of the US retail sales for July and a possible acceleration of the rates could imply a resilience of the demand side of the US economy thus also providing some support for the greenback.

On a monetary level, we note the gradual shift of some of the bank’s policymakers after the release of the US employment data for July. Statements made by San Francisco Fed President Daly and Minneapolis Fed President Kashkari are characteristic. It should be noted that the market’s expectations have radically been altered, as before the release the bank was expected to remain on hold until the end of the year, while after the release market expectations for two rate cuts until December were revived. Should more Fed policymakers come forward with dovish inclinations we may see them weighing on the USD as it could imply a further shift of the balance of power within the bank towards the dovish side. Furthermore, the market worries for the successor of Fed Chairman Powell intensify. US President Trump stated that he would be announcing a successor by the end of the week, and rumours for Fed Board Governor Waller to be that person intensify as these lines are written. In any case we expect Powel to be replaced by a dove or someone with dovish inclinations. Also Trump’s temporary choice, Stephen Miran, to fill in Kugler’s position in the Fed seems to disappoint the markets. In any case, we expect Miran, should he be approved by the Senate, to advocate for a more dovish monetary policy by the Fed, adhering to US President Trump’s wishes. It’s characteristic that Miran had advocated for a tighter control of the Fed by the US President in the past. Overall, the appointment seems to be tilting the balance of power within the Fed to the dovish side and thus may continue weighing on the USD on a monetary level.

The uncertainty caused by US President Trump’s tariffs remains despite the US reaching deals with various countries. Nevertheless, negotiations are still ongoing, and relationships of the US with India are experiencing a low point, after Trump doubled the tariffs on Indian products entering the US. It seems that US President Trump’s tariff war is expanding beyond a vertical form of a country-by- country basis, now horizontally on a sector-by-sector basis, as the imports of semiconductors are to suffer a 100% tariff, with few exceptions. We cite the pharmaceutical sector as the next possible target for Trump’s tariffs, which in turn may imply a continuation of trading tensions. Should that be the case, we may see developments on the issue weighing on the USD as the uncertainty is to be enhanced. On the flip side, negotiations with Russia seem to have made considerable progress and media mention the possibility of a Trump-Putin meeting as early as next week. A possible improvement of the US-Russian relationships could have a positive effect on the USD on a fundamental level.

Analyst’s opinion (USD)

“We highlight the release of the US CPI rates for July next Tuesday and a possible acceleration of the rates, beyond market expectations could provide support for the USD. On the flip side the expansion of dovishness for the Fed’s monetary policy tends to weigh on the greenback. Also Trump’s trade wars are expected to play a key role in the USD’s direction next week.”

GBP – Q2 GDP rates in focus

The main event in the past few days for pound traders may have been the release of BoE’s interest rate decision. The bank, as was widely expected, cut rates by 25 basis points lowering rates to 4.00% from prior 4.25%. Yet the highlight of the release was not the lowering of the interest rates as such, but the way the decision was made. The Monetary Policy Commission, in the first vote had a three way split with one member favoring a 50 basis points rate cut, 4 members favouring a 25 basis points rate cut and 4 opting for the bank to remain on hold. As no decision could be reached, a repetition of the vote was required and in the second vote 5 favoured a 25 basis points rate cut and 4 favoured the bank to remain on hold. Overall the fact that the bank required a historic second vote to reach a decision, highlighted the shift of the MPC towards a more cautious approach in easing the bank’s monetary policy. It’s characteristic how the pound jumped at the release, while market expectations for the bank to cut rates were shifted from the November to the December meeting after the release. The bank’s direction continues to be towards further easing, yet it all comes down to the path of inflation. The bank expects inflation to accelerate to 4%, peak and slow down afterwards. Hence should the CPI rates start slowing down, we may see market expectations for the bank to cut rates being enhanced. In the coming week, should we see BoE policymakers signalling further hesitation in easing the bank’s monetary policy, the pound may get some support.

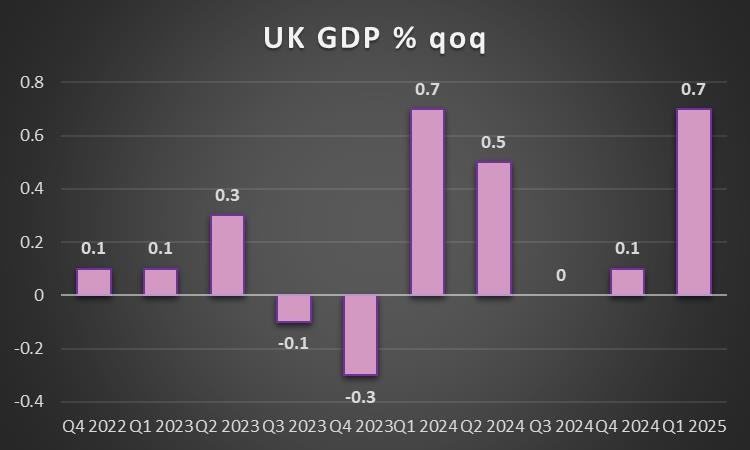

On a macroeconomic level we highlight in the coming week the release of the UK employment data for June and further easing of the UK employment market could weigh on the pound. At this point we would like to note our worries for the UK employment market as the unemployment rate ticked up for three consecutive months. The key financial release of the week for pound traders though is expected on Thursday and is to be Q2’s GDP rates. Should the GDP rates for Q2 continue to accelerate, we may see the pound getting some support as further expansion of the UK economy would be evident. At the same time we also get the manufacturing output and GDP growth rates for June.

On a fundamental level, we note that Chancellor Reeves welcomed the rate cut, yet our worries for the outlook of the UK economy tend to remain. It’s characteristic how media highlight the widening of the fiscal deficit, while concerns for possible tax hikes tend to grow. Overall we view the case for the market’s worries for UK government’s fiscal policies as weighing on the pound at the current stage.

Analyst’s opinion (GBP)

“For pound traders we highlight the release of the UK employment data for June and GDP rates for Q2 in the coming week. A possibly easing employment market in the UK could weigh on the pound while an accelerating GDP rate could provide some support. On a monetary level, BoE’s hesitation for further easing of its monetary policy tends to support the pound, while the troubling UK Government’s fiscal policies dilemma tends to weigh on the pound.”

JPY – Japan’s Q2 GDP rates under the limelight

On a monetary level, we note the market’s expectations for the BoJ to remain on hold until the end of the year which tends to weigh on the JPY, if compared to prior expectations for the bank to hike rates. Should risks deriving from international trade relationships start fading, the market expectations for further tightening of the bank’s monetary policy may re-emerge. On the other hand Japanese political parties seem to be exercising pressure on the bank to remain on hold. In any case should market expectations for a possible tightening of the BoJ’s monetary policy be enhanced, we may see JPY getting some support. For the time being we note that the summary of opinions for the bank’s latest interest rate decision highlighted the wide uncertainty caused by international trade remain substantial, while debate the possibility of resuming a tightening of the bank’s monetary policy.

On a more fundamental level, JPY’s safe haven qualities should not be underestimated. Should worries in the international markets intensify we may see the Yen getting some safe haven inflows, while an easing of the market’s worries could weigh on the JPY. Furthermore the Japanese government seems to be pressing the US to expedite the lowering of tariffs on Japanese cars as agreed, while also seeks clarifications for tariffs on other goods. It should be noted that PM Ishiba’s administration is getting a lot of pressure for various clauses that seem to be unclear. Should we see an easing of the US tariff burden on Japanese products, we may see the JPY getting some support.

On a macroeconomic level, we note the release of Japan’s corporate goods prices for July, which is to provide an idea for inflationary pressures at a producer’s level for the past month. The main release though is expected to be Japan’s GDP rate for Q2. The rate is expected to accelerate, getting out of the negatives and if so could provide some support for the JPY as it would imply a return to growth once again, possibly easing market worries for the macroeconomic outlook of Japan.

Analyst’s opinion (JPY)

“In the coming week we highlight the release of Japan’s GDP rates for Q2. An acceleration of the rates possibly beyond market expectations could provide some support for JPY. Furthermore we note that JPY’s safe haven status should not be underestimated on a fundamental level while an intensification of the market expectations for a tightening of JPY’s monetary policy could support JPY.”

EUR – Hopes for a possible ceasefire in Ukraine could support EUR

On a fundamental level, EUR traders are expected to keep a close eye on the US-Russian relationships. Over the past few days media highlighted that US Special Envoy to the Middle East Witkoff, seems to have achieved a substantial amount of progress in negotiations with Russian President Putin. The progress mentioned in various media is so wide that US President Trump and Russian President Putin may meet as early as next week. Should we see the negotiations lifting market expectations for a possible ceasefire in the war in Ukraine, we may see the EUR getting some support. On the other hand we see little incentive at the current stage for Russia to agree to a possible ceasefire, hence any agreement may be lopsided to Russia’s favor. Also we note that despite a framework being agreed between the US and the EU, about their trade relationships, a certain degree of uncertainty tends to remain. Should market worries about the issue intensify they may weigh on the EUR.

On a monetary level, we note the market’s expectations for the ECB to remain on hold until the end of the year and proceed possibly with a rate cut in Feb 26. Hence any dovish expectations seem to be remote at the current stage. In any case the bank seems not to be experiencing any pressure to either ease or tighten its monetary policy, as inflation seems to remain near the bank’s target. Hence ECB’s monetary policy seems to have eased its influence over EUR’s direction for now.

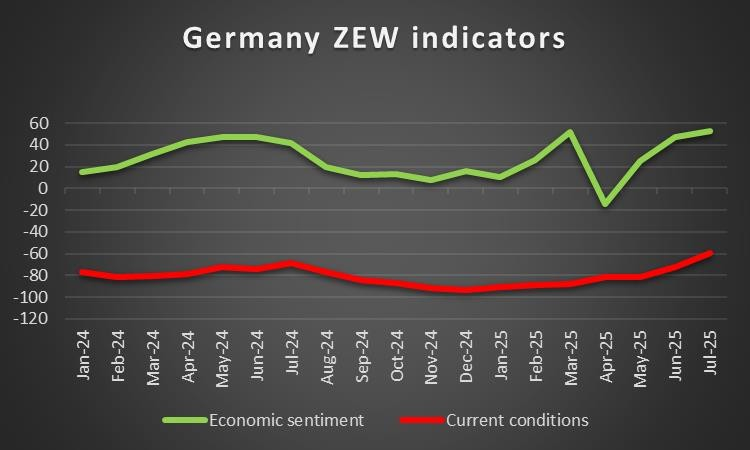

On a macroeconomic level, we note the release of Germany’s ZEW indicators for August. Should the indicators’ readings show more optimism and further improvement of the conditions, could provide some support for the EUR. Also the final HICP rates of France and Germany are expected to confirm the rates of the preliminary release. Also on Thursday we get Euro Zone’s revised GDP rates for Q2 and should they accelerate somewhat, we may see the EUR getting some support and vice versa. On the other hand, we note the release of Eurozone’s industrial output growth rate for June and should the rate slow down and drop into the negatives as expected, we may see the EUR being negatively affected by the release.

Analyst’s opinion (EUR)

“In the coming week, we highlight fundamentals as the key factor for EUR’s direction. Should we see the US-Russian relationships improving, we may see the EUR getting some support”

AUD – RBA expected to cut rates yet will it signal further easing?

In the coming week we expect Aussie traders to focus on the release of RBA’s interest rate decision on Tuesday. Currently, market expectations are for the bank to cut rates and AUD OIS imply a probability of 92% for such a scenario to materialise. Yet AUD OIS also imply that the market expects the bank to proceed with two more rate cuts until the end of the year, once in November and once in December, hence the market expectations for the bank are clearly dovish. Should the bank cut rates as expected, and in its forward guidance signal that there are more rate cuts down the line, we may see AUD slipping. On the flip side, should the bank signal hesitation for further easing of tis monetary policy, thus contradicting the market’s dovish expectations, we may see the Aussie getting substantial support.

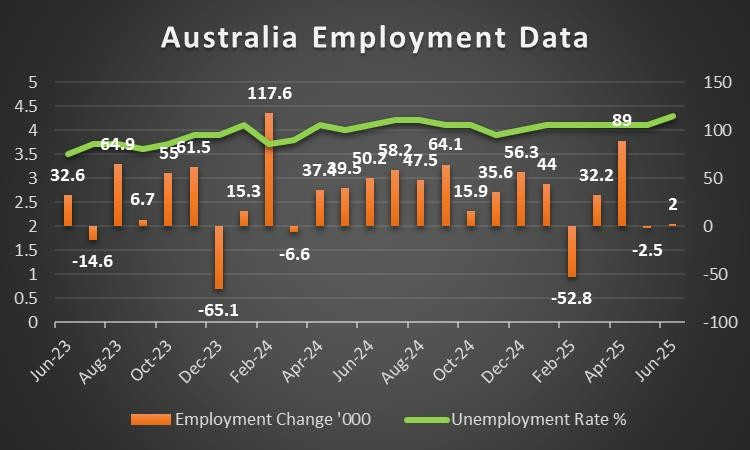

On a macroeconomic level, we highlight the release of Australia’s employment data for July next Tuesday. Should the data show further easing after the tick up of June’s unemployment rate and the disappointing employment change figure of 2k, we may see the Aussie slipping as pressure on RBA to continue easing its monetary policy may intensify.

As for the fundamentals surrounding the Aussie, we note that further market worries for international trading tensions could weigh on the Aussie given that it’s considered a commodity currency and a riskier asset in the FX market. Special interest of Aussie traders relies in the US-Sino trade negotiations and news of progress made could provide some support for AUD given the close Sino- Australian economic ties. News from China were worrying as Chinese factories seem to be struggling for economic activity. Tomorrow we note the release of China’s inflation metrics, yet main interest lies with Friday’s release of China’s industrial output, retail sales and urban investments growth rate for July. An improvement of the data related to the Chinese economy could provide some support for AUD as it could improve the macroeconomic outlook of China.

Analyst’s opinion (AUD)

“We note the release of RBA’s interest rate decision as the key event for Aussie traders in the coming week. Should the bank cut rates and signal that more rate cuts are to come, we may see AUD slipping, while should a possible hesitation for further easing be expressed we may see AUD gaining. Furthermore we note the release of Australia’s July employment data as a possible market mover for AUD.”

CAD – Fundamentals to lead the Loonie

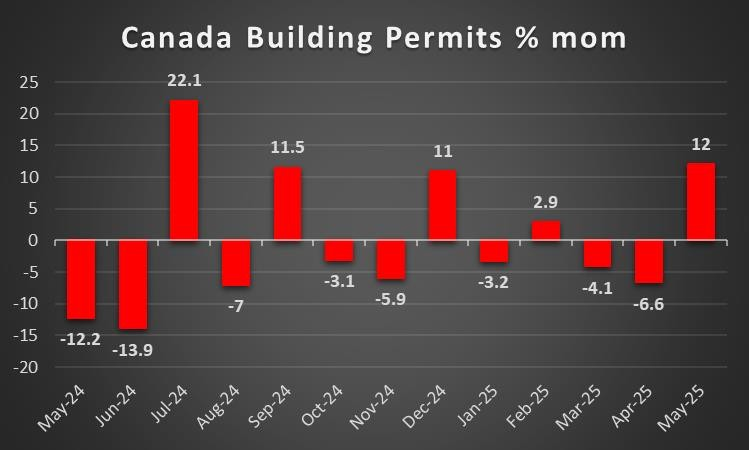

On a macrolevel we note that Canada’s employment data for July are still to be released as these lines are written and depending on the actual rates and figures, could potentially alter the Loonie’s direction. Forecasts are for the unemployment rate to tick up to 7.0% and the employment change figure to drop from June’s stellar 83.1k to 13.5k, with the prognosis of the two indicators aligning in pointing towards a looser Canadian employment market for the past month. Should the actual rates and figures be even worse, we may see the Loonie slipping as pressure on the BoC to ease its monetary policy could mount. Should actual data show that the Canadian employment market eased less than expected, we may see the CAD edging higher, while a tightening Canadian employment market may provide asymmetric support for the Loonie. In the coming week, with the exception maybe of June’s building aprovals and manufafturing sales, few financial releases from Canada could generate interest for Loonie traders, hence we expect fundamentals to lead CAD traders.

On a monetary basis, we note the market’s expectations for the bank to proceed with a rate cut in the November meeting. The forecasts tend to imply a slight dovish tilt of the market which in turn may be weighing on the loonie somewhat.

On a fundamental level, we note that the US- Canadian trade deal is still pending and negotiations seem to present little if any progress. Trump’s tariff deadline has come and gone, and Canada is facing a tariff of 35%. Should we see the negotiations continuing to drag, we may see the issue fundamentally weighing on the Loonie, while reports of progress could provide support. Also we note the intense downward motion of oil prices over the past week, which tend to weigh on the Loonie, given Canada’s status as a major oil producing economy. Lastly we express our worries for the Canadian economic outlook as expressed also by IMF, which focuses on the high household debt levels. Should we see market worries for the outlook of the Canadian economy emerge, we may see them weighing on the Loonie as well.

Analyst’s opinion (CAD)

“We note the release of July’s Canadian employment data later today as a key issue for the direction of the Loonie, yet other than that, fundamentals may lead CAD traders in the coming week. The pending trade deal with the US, the lack of progress in the negotiations and falling oil prices could fundamentally weigh on the CAD.”

General Comment

In the coming week we expect the USD to maintain the initiative in the FX market as we get a number of high impact financial releases from the US. Yet at some instances, we may see financial and monetary policy events from other countries allowing other currencies to take the initiative and come under the spotlight. Thus a more balanced trading mix may emerge in the FX market. As for US stock markets, we get some mixed signals as Dow Jones remains in a sideways motion, while Nasdaq and S&P 500 maintain some slight bullish tendencies. The earnings season is still on, yet most of the high profile companies have allready released their earnings reports. Nevertheless we still note a couple of releases among which the release of BHP’s earnings report on Monday and on Tuesday we get the figures of Home Depot and Xiaomi while on Wednesday we get the earnings report of Tencent and Cisco. Overall, should fundamentals surrounding US equities start favouring a more risk oriented approach by the markets, we may see them getting some support. As for gold’s price, we note the slight bullish tendencies over the past week, reflecting its negative correlation with the USD. Should the negative correlation be maintained in the coming week as well and should we see the USD weakening further, gold’s price could get additional support approaching record high levels.

If you have any general queries or comments relating to this article please send an email directly to our Research team at research_team@ironfx.com

Disclaimer:

This information is not considered as investment advice or an investment recommendation, but instead a marketing communication. IronFX is not responsible for any data or information provided by third parties referenced, or hyperlinked, in this communication.