With the week nearing its end, we note the US Employment data for August has yet to be released. On a monetary level, a number of policymakers from various central banks are scheduled to speak throughout the week and could sway the market’s mood. We highlight RBA and BoC’s interest rate decisions on Tuesday and Wednesday respectively, as RBA and BoC policy stances are expected to influence regional currencies. The market will be watching whether RBA and BoC maintain their current tone or shift toward a more cautious outlook. In addition, traders may assess how RBA and BoC decisions align with broader global monetary trends. We also note that expectations around RBA and BoC communication could contribute to volatility leading into mid-week trading. Lastly, on Friday, we note the issuances of the Fed’s quarterly financial accounts of the US, which may interact with earlier RBA and BoC outcomes.

In regards to financial releases, we make a start on Monday with Turkey’s CPI rate for August. On Tuesday, we begin with Australia’s current account balance figure for Q2 and France’s Services PMI figure for August, with some analysts comparing Australian data alongside RBA and BoC policy paths. On Wednesday we make a start with Australia’s GDP rate for Q2, Germany’s industrial orders rate for July, the UK’s All-sector PMI figures for August, Canada’s Trade balance figure for July and lastly the US ISM Non-Manufacturing PMI figure for August, which may further shape expectations around RBA and BoC decisions. On a busy Thursday, we make a start with Australia’s trade balance figure for July, China’s trade data for August, Germany’s industrial output rate for July, Germany’s industrial production rate for July, followed by the UK Halifax house prices rate for August, the EU’s Revised GDP rates for Q2 and finishing off with the US weekly initial jobless claims figure. Finally, on Friday, we note Japan’s revised GDP rate for Q2 and Canada’s employment data for August, which may provide additional context for RBA and BoC watchers.

USD – US Economy appears to be feeling the impact of high-interest rates

The USD broke its 6-week winning streak, and as the week nears its close we note that the dollar appears to be moving in a downwards fashion. On a fundamental level, we highlight that US Commerce Secretary Raimondo visited China during the week, potentially indicating that the relationship between the two rivals may be improving. Should there be further indications towards such a direction, the market sentiment may improve, causing the USD some safe-haven outflows, similar to reactions sometimes observed after RBA and BoC communications. On a monetary level, we highlight the speech by Fed Chair Powell at Jackson Hole where he stated that the bank is “prepared to raise rates higher”, implying that the terminal rate is further than expected. Moreover, the comments by Cleveland Fed President Mester, who stated that “undertightening is worse than overtightening”, imply that the Fed may be willing to continue hiking rather than risk inflationary pressures coming back—an approach often compared to how RBA and BoC handle inflation risks.

On the other hand, Atlanta Fed President Bostic stated that the Fed’s monetary policy is already restrictive. Overall, should the Fed continue to be hawkish we may see the greenback getting some support, much like the reactions seen after RBA and BoC meetings when policy tones surprise markets. On a macroeconomic level, we highlight the US JOLTS Job Openings figure on Tuesday, which came in at 8.827M, roughly 1M below expectations. The lower-than-expected figure, combined with the ADP Employment data which also came in lower than expected, may be indicative of a loosening US labour market. Such labour-market dynamics are also being closely monitored by RBA and BoC policymakers as part of their own domestic assessments. The loosening of the labour market could prove to be a barrier to the Fed should it decide to continue its rate-hiking cycle, and as such market participants may be interested in the release of the US Employment data later today in order to acquire a more complete picture of the US Employment market for the past month—similar to how RBA and BoC updates often shape expectations around policy trajectories.

GBP – Has the BOE done enough to combat inflationary pressures?

The pound seems about to end the week stronger against the USD, to a lesser extent against the EUR and currently remains rather stable against the JPY. On a fundamental level, we note that now-former Member of Parliament Dorries formally announced her resignation in a letter sent to Prime Minister Sunak, in which she stated that the country was being run by a “zombie parliament”. The statements by the former MP may increase political tensions in the country’s ruling party, similar to how shifting political conditions have occasionally influenced market reactions following RBA and BoC meetings. On a monetary level, we highlight the speech by BoE Chief Economist Pill, who stated when referring to the bank’s current monetary policy “that policy is in restrictive territory, there is the possibility of doing too much and inflicting unnecessary damage on employment and growth”, implying that the bank may be less willing to continue hiking interest rates, much like the recent caution expressed by RBA and BoC officials. An easing of BoE’s hawkishness in the coming week may weigh on the pound as it may weaken the bank’s case for future rate hikes, reflecting dynamics similar to market reactions seen after RBA and BoC policy shifts.

On a macroeconomic level, we note the lack of major financial releases during this week and the next, with the exception of the UK Halifax House Prices rate for August next Thursday. As such, we may see the pound being more influenced by fundamentals, just as markets often respond to broader sentiment in weeks when RBA and BoC events are absent from the calendar.

JPY – Japan’s revised GDP rate for Q2 due out next week

JPY is about to end the week slightly stronger against the USD and the EUR and remains relatively stable against the pound. On a fundamental level, we note Japan’s first major strike in decades in order to protest the sale of a department store. According to news outlets, the strike is due to last a day and will include nearly 900 workers, after the department store and the workers union failed to reach an agreement over job and business continuity guarantees. Although this may not have a significant impact on the JPY, strikes are extremely rare and as such are worth noting, just as unexpected developments often influence markets in weeks when RBA and BoC decisions draw attention. On a monetary level, we note the speech from BOJ Tamura, a known hawk in the bank’s inner circle. The policymaker’s comments appear to have been perceived as hawkish, as Tamura stated that “about a decade has passed since the BOJ began efforts to sustainably and stably achieve its 2% inflation target. I feel that achievement of this goal is now clearly in sight”, implying that the bank’s ending of negative interest rates could be coming to an end in the near future. Yet other BoJ officials, such as Governor Ueda and board member Nakamura, tended to maintain a dovish stance — a contrast often compared to the dynamics seen around RBA and BoC meetings. A continuance of BoJ’s dovish stance could weigh on JPY next week, similar to how markets sometimes react after RBA and BoC tone shifts.

On a macroeconomic level, we note that the deterioration in Japan’s industrial production for July might be cause for concern for the current economic situation in Japan. Should Japan’s economic activity deteriorate even further, we may see the worsening economic outlook weighing on the JPY, especially if its manufacturing industry slows, as Japan is heavily reliant on its export sector — a sensitivity also highlighted in discussions around RBA and BoC assessments of external demand. Lastly, looking at next week, traders may be interested in Japan’s revised GDP rate for Q2, which is due to be released on Friday, and may be evaluated alongside global developments, including the latest direction taken by RBA and BoC.

EUR – The acceleration in CPI rates, appear to be ringing some alarm bells in Europe

EUR is about to end the week in the greens against the USD, weaker against the pound and relatively unchanged against the JPY. On a fundamental level, we highlight the statement made by the European Council President Michel, who told a forum on Monday that the bloc needs to be ready by 2030 to enlarge. Currently, six western Balkan states such as Bosnia, Serbia and Albania are at different stages in the process of joining the European Union, as such the induction of new members could increase the demand for the EUR but on a more fundamental way, the enlargement could enhance the potentials and the capacity of the trading bloc, thus supporting the common currency. On the monetary front, we note the anticipated speech by ECB President Lagarde at the Jackson Hole conference, in which she stated that the bank will be “setting interest rates at sufficiently restrictive levels” in regard to achieving the bank’s 2% inflation target, which could be indicative of future rate hikes by the bank. In addition, ECB Holzmann stated on Monday that “If there aren’t any big surprises, I see a case for pushing on with rate increases without taking a pause”, further supporting our hypothesis that the bank may be considering future interest rate increases in order to bring inflation down to the banks 2% target. On a macroeconomic level, acceleration of eurozone’s headline HICP rates was indicative of an intensification of inflationary pressures in the Eurozone. The higher-than-anticipated HICP rates may be reflective of the summer period, upon which many Europeans decided to go on holiday thus creating seasonal demand by consumers who were willing and able to spend more during their holidays. However, should inflationary pressures continue to persist, we may see the Eurozone entering a period of stagflation, which could weigh heavily on the EUR in the future. Currently, we expect the acceleration of the Eurozone’s headline HICP rate to harden the ECB’s hawkish stance which in turn may provide some support for the EUR.

AUD – Will the RBA hike in their meeting next week?

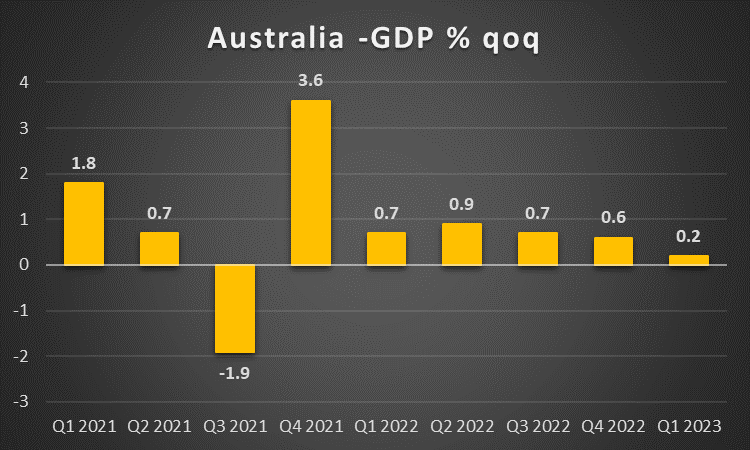

AUD is about to end the week stronger than the dollar. On a fundamental level, we note that last week’s fears regarding Australian LNG producers appear to have materialized as LNG workers at the Chevron plants are set to go on strike on the 7th of September if no agreement is reached by then. The potential strike could potentially drive natural gas prices to higher levels, due to the potential disruption of Australia’s 10% market contribution in the LNG market. On a deeper fundamental level, we highlight the headwinds faced by China in its effort to recover its economy, which if continued and/or intensified may weigh on the Aussie given the close Sino-Australian ties. On a monetary level, we note the comments made by incoming Governor Bullock, who on Tuesday stated that inflation is still too high in Australia and that “We may have to raise interest rates again, but we’re watching the data very carefully”. The comments made by the current RBA Deputy Governor could be interpreted as an intention by the RBA to hike in its next meeting, which is due next Tuesday, yet interestingly market participants are predominantly expecting the bank to remain on hold. However, based on the comments made by the incoming RBA Governor, we would not be surprised if the RBA takes the markets by surprise and hikes by 25 basis points, therefore providing support for the Aussie, otherwise, we may see the Aussie retreating. On a macroeconomic level, we note Australia’s Preliminary retail sales rate for July which came in better than expected, implying that consumers are still spending, despite the current level of interest rates. As such, should the retail industry remain resilient, with consumer spending remaining at higher levels, we may see support for the Aussie, as it could be interpreted as a positive for economic activity in Australia. Lastly, market participants may be looking at next week’s current account balance figure for Q2 on Tuesday,

Australia’s real GDP rate for Q2 which is due to be released on Wednesday and lastly Australia’s trade balance figure for July which is due to be released on Thursday.

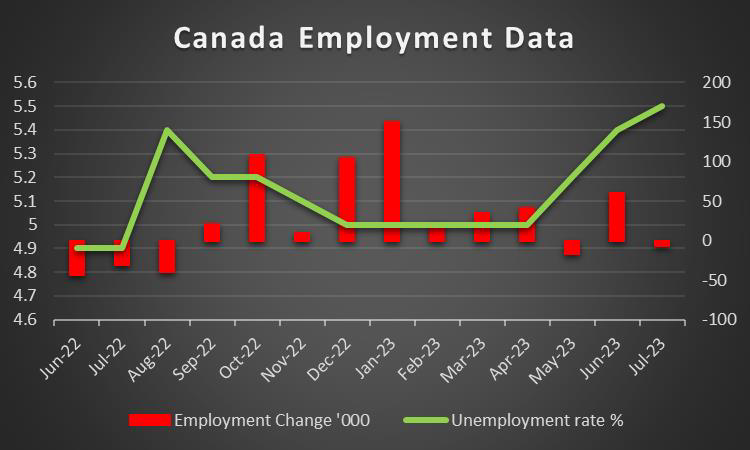

CAD – BoC interest rate decision due next week

The Loonie appears to have stopped its six-week losing streak against the dollar and is currently on track to finish the week higher than the greenback. On a fundamental level, we note that the Canadian Government stated on its website that it would be investing in over 4,700 researchers across the country in order to foster cutting-edge research in health, the environment, economic development and more. The announcement could be seen as a long-term investment in Canada’s domestic economy, similar to structural initiatives often referenced alongside RBA and BoC outlooks, yet any investments at this stage could potentially take decades to bear fruit. CAD traders on the other hand keep a close eye on oil prices which continue to be on the rise and were pushed higher by a tight supply side, while market worries for the economic outlook of China, a major oil consumer, intensify worries for the demand side of the commodity and tend to clip any further gains for oil’s price. Should oil prices continue to rise we may see the CAD benefiting, given that Canada is a major oil-producing economy—a dynamic often compared with commodity-linked sensitivities in RBA and BoC commentary. On a monetary level, we note that the Bank of Canada’s interest rate decision is due next Wednesday with market participants anticipating that the bank will remain on hold, as CAD OIS at the time of this report implies an 80.06% probability for this scenario to materialize, mirroring how RBA and BoC expectations often guide market positioning. Therefore, should the bank remain on hold in its next meeting, we may see the Loonie ceding ground to its counterparts, as it could be interpreted that the bank is reaching or is near its terminal rate—an interpretation markets also apply when assessing RBA and BoC pauses. On a macroeconomic level, we note that Canada’s GDP rates for Q2 have yet to be released at the time of this report and as such could potentially influence the CAD’s direction to the downside if the rates slow down as anticipated. However, on the other hand, should the GDP rates for Q2 surprise the markets and accelerate, we may see the Loonie further gaining against the dollar, as stronger growth data has historically aligned with shifts in RBA and BoC tone as well.

General Comment

In the coming week, we expect volatility in the FX market to continue to increase given the high volume of financial releases that are due next, in addition to the high number of speeches by central bank officials, which could heavily influence the FX market, much as RBA and BoC updates often do. We also note that the earnings season in the US appears to be reaching an end for now. As for gold’s price, we note that it appears to be ending for a second week higher, having temporarily reached levels last seen at the beginning of the month. Specifically, gold’s price seems to maintain its negative correlation with the USD, which may we add seems to be skewed a bit asymmetrically to gold’s favour. On a more fundamental level, we highlight the current situation in China continues to be at the epicentre of market worries, as the Chinese Government appears to be continuing its desperate attempt to protect its property industry, as China’s industrial bank is cutting Yuan deposit rates. However, Fitch Credit rating agency cut China’s 2023 GDP forecast to 4.8% from 5.6% and China’s Real Estate Information Corp sees sales for August at -34% on a yoy basis. Overall, the issue has a global aspect as when China sneezes the rest of the world catches a cold and hence any indication of additional difficulties for the Chinese economic recovery may cause the markets to adopt a more cautious stance.

If you have any general queries or comments relating to this article please send an email directly to our Research team at research_team@ironfx.com

Disclaimer:

This information is not considered as investment advice or an investment recommendation, but instead a marketing communication. IronFX is not responsible for any data or information provided by third parties referenced, or hyperlinked, in this communication.