The week is coming to an end and we have a look at what next week has in store for the markets. On the monetary front, the highlights of the week are expected to be the RBA’s interest rate decision on Tuesday and the SNB’s , Norges bank and the BoE’s interest rate decisions which are set to occur on Thursday. As for financial releases, we make a start on Monday with Japan’s Machinery orders rate for April and China’s industrial output rate for May. On Tuesday we get the Eurozone’s final HICP rate for May, Germany’s ZEW economic sentiment figure for June, followed by the US retail sales rate for May and US industrial production rate for May as well. On Wednesday we get Japan’s trade balance figure and the UK’s CPI rate both for May. On Thursday we get New Zealand’s GDP rate for Q1, the US weekly initial jobless claims figure, US Philly Fed business index figure for June and the Eurozone’s preliminary consumer confidence figure for June as well. On Friday, we get Australia’s preliminary judo bank manufacturing PMI figure for June, Japan’s CPI rate for May and preliminary Jibunk manufacturing PMI figure for June, followed by the UK’s retail sales rate for May, France’s preliminary service PMI figure, Germany’s preliminary manufacturing PMI figure the Eurozone’s preliminary composite PMI figure and the UK’s preliminary service PMI figure all for the month of June, followed by Canada’s retail sales rate for April and the US S&P preliminary manufacturing PMI figure for June.

USD – Fed to maintain interest rates higher for longer

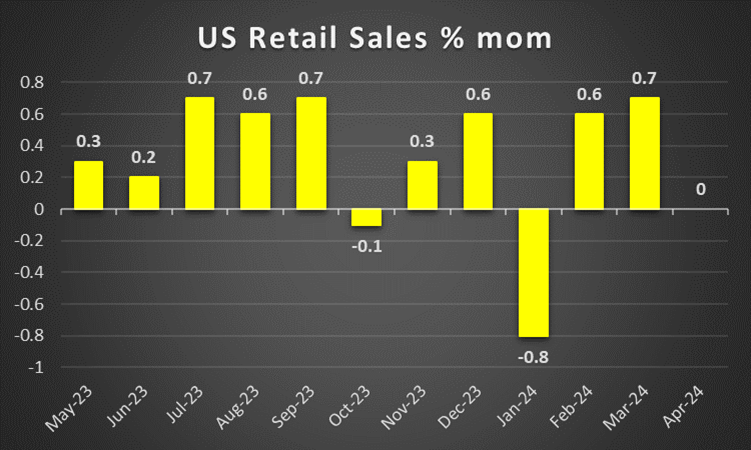

The USD is about to end the week in the greens against its counterparts. On a macroeconomic level, we note the CPI rates for May which were released on Wednesday came in lower than expected. In particular, the headline rate on a year-on-year level came in at 3.3% versus the expected 3.4% and on a core level, the CPI rate also on a year-on-year level came in at 3.4% versus the expected rate of 3.5%. As such, the inflationary pressures in the US economy appear to be easing if we consider the most recent inflation print. However, despite the lower-than-expected inflation rates, the reality is that the 0.1% lower-than-expected rate is relatively insignificant in the grander scheme of things and that inflation still remains stubbornly high. Yet, following its release the dollar tended to lose ground against its counterparts. On a monetary level, the Fed’s interest decision was released on Wednesday, with the bank remaining on hold as it was widely expected. Interestingly, the bank’s dot plot was revised higher for the remainder of the year, essentially locking in one rate cut which was lower than the market’s expectations of two rate cuts by the end of the year. Furthermore, Fed policymakers appear to be still concerned about the stubborn inflation pressures in the US economy. Specifically, in the bank’s accompanying statement, Fed policymakers stated their concerns that despite inflation easing over the past year, it still remains elevated. Overall, Fed Chair Powell’s comments appear to have been interpreted as relatively hawkish, with the dollar moving lower following the press conference. For next week, we would like to highlight the release of the US S&P preliminary Manufacturing PMI figure for June, which may act as a gauge of the resilience of the US manufacturing sector. Therefore, should the figures imply a greater expansion in the sector, it may provide support for the dollar and vice versa.

GBP – BoE interest rate decision next week

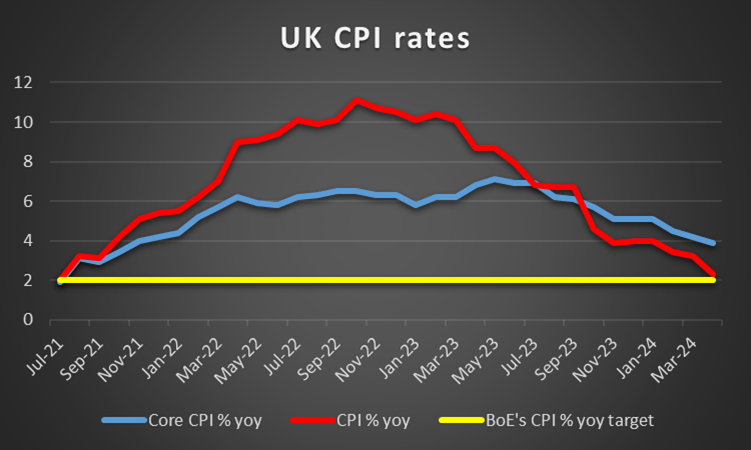

The pound is about to end the week in the reds against the USD and stronger against the EUR yet relatively unchanged against the JPY. On a political level, we note that both the Labour and the Conservations have released their manifesto for the general elections which are set to occur on the 4th of July. In the Sunak-Starmer debate, the opinion polls continue to show a widening margin in favor of the Labor party. The issue has high stakes and given Labor’s widening lead, uncertainty in the UK may rise, as a recent poll by POLITICO shows the conservatives polling at 21%, with their losses seemingly having gone to the right-wing populist party ‘Reform UK’ which is polling at around 15% per POLITICO. On a macroeconomic level, we note the UK’s unemployment rate for April ticked upwards to 4.4% from 4.3%, implying a loosening labour market. Thus, despite the average hourly earnings rate for the same month coming in higher than expected, the increase in unemployment may potentially increase pressure on the BoE to ease its monetary policy sooner rather than later. Moreover, the bad news regarding the UK’s economy seemed to pile up this week, with the industrial production rate and manufacturing production rate both for the month of April coming in lower than expected, implying that the industrial and manufacturing sectors of the UK may be struggling. Thus, in combination with the release of the UK’s GDP rate for April which came in as expected at 0.6% on a yoy level and 0% on a mom basis, the UK economy in our view, is very close to entering recession territory. As such attention may turn to the BoE’s interest rate decision next week, in which the bank is widely anticipated to remain on hold, with GBP OIS currently implying a 90.6% probability for such a scenario to occur. Hence, attention may turn to the bank’s accompanying statement, where should it be implied that the bank may be preparing to cut interest rates at a faster rate than what is currently anticipated, it could weigh on the pound. On the other hand, should the bank’s accompanying statement imply some hesitancy from BoE policymakers to cut interest rates, it could be perceived as hawkish in nature and thus may provide support for the pound. Lastly, we would also like to note the UK’s CPI rates for May which are set to be released next week. Should they imply persistent or even an acceleration of inflationary pressures it may increase pressure on the BoE to maintain its restrictive monetary policy which in turn could support the pound and vice versa.

JPY – CPI in focus

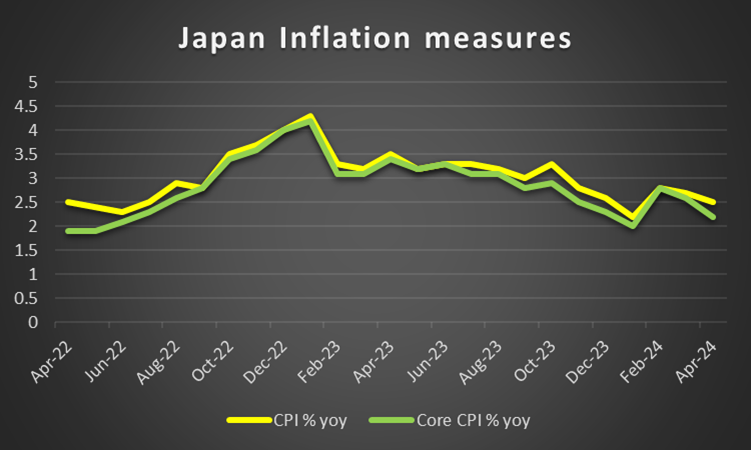

JPY is about to end the week stronger against the EUR, unchanged against the pound and the greenback. On a monetary level, we would like to highlight the BOJ’s interest rate decision earlier on today, in which the bank remained on hold, as it was widely expected by market participants. Overall, the forward guidance remained relatively unchanged. The bank also seems to intend to continue to buy government bonds at the current pace and may start reducing bond purchases in the coming one[1]two years. Overall, maintaining the current pace of bond buying seems to be getting a slight dovish tone across as it would keep the liquidity of the Japanese economy at high levels through an expansionary QQE policy. Understandably, JPY weakened across the board, yet at this point we would like to express our worries for a possible market intervention by the Japanese government and BoJ given that the JPY is nearing an over thirty-year low level. On a macro-economic level, we highlight the release of Japan’s revised GDP rate for Q1 which came in better than expected, yet still remained in contraction territory, which may serve as a painful reminder for the darkening economic outlook of Japan. As such following the release, despite the better-than-anticipated rate, it appears that Yen traders remained unphased. However, traders may be looking towards next week’s financial releases, as Japan’s trade balance figure for May is set to be released on Wednesday and the CPI rate for May in addition to the Jibunk preliminary manufacturing PMI figure for June are set to be released on Friday. Should the financial releases tend to imply a positive economic outlook for the Japanese economy, we may see the Yen gaining against its counterparts. However, should the release further enhance Japan’s dark macroeconomic outlook, we may see the Yen weakening.

EUR – PMI’s next week

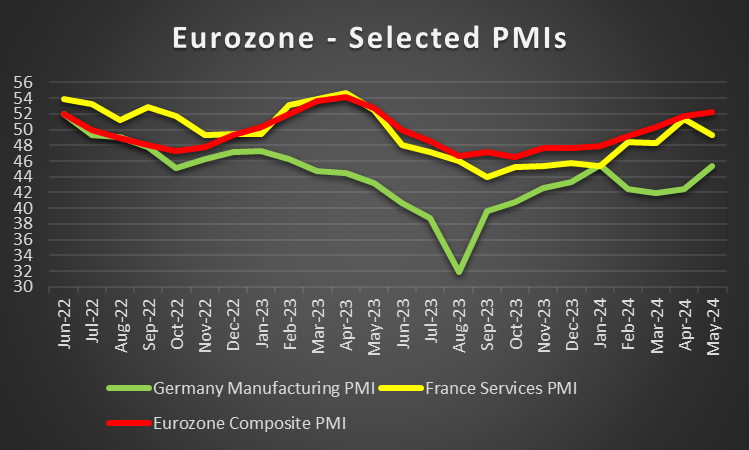

The EUR is about to end the week in the reds against the USD, Yen and the GBP. On a fundamental level, we note the European Parliament elections tended to shock the political spectrum in Europe, with far-right parties making significant gains. So much so that Emmanuel Macron called for snap elections after the opposition party ‘RN’ won about 32% of the vote, whilst his own ruling party won 15%. The balance of power appears to have shifted and the early elections for France are seen by some as an unnecessary gamble. Nonetheless, with voting set to occur at the end of the month, the common currency may see increased volatility in the coming week. On a macroeconomic level, we note the Eurozone’s sentix consumer confidence index for June which came in better than expected. Yet the release does not appear to have provided support for the EUR, as it may have been overshadowed by the results of the EU Parliamentary elections, which we discussed above. On a monetary policy level, we note the comments made by ECB Vice President DeGuindos earlier in the week, in which he stated that the “level of uncertainty is huge” when referring to the bank’s inflation outlook. Moreover, ECB Vice President DeGuindos stated that the ECB must move “very slowly” in reducing interest rates, implying once against the future outlook remains uncertain. Overall, we continue to view the bank’s stance as a predisposition for more rate cuts, yet also that the bank at the same time remains data-dependent. Should in the coming week, ECB policymakers start highlighting the possibility for a pause in rate cuts we may see the EUR getting some support. For next week of interest to EUR traders may be the release of Germany’s ZEW Economic sentiment figure for June and the preliminary services PMI figure for France and Germany’s Manufacturing PMI figure as well as the Eurozone’s preliminary composite PMI figure all for the month of June. Should the releases tend to imply that Europe’s largest economies are resilient or are fairing better than the prior readings, may see the EUR gaining some support and vice versa.

AUD – RBA decision in focus

AUD is about to end the week stronger against the USD. On a fundamental level, we once again note the risk deriving from the tensions in the US-Sino relationships. Should there be an escalation in the tensions in the US-Sino relationships we may see them weighing on the Aussie, given the close economic ties between Australia and China. The issue was once again highlighted after the defence secretary for the Philippines which has a mutual defence treaty with the USA, stated that his nation faces an “existential issue” from Beijing, as the territorial dispute in the South China Sea between Beijing and Manila remains elevated. On a macroeconomic level, Australia’s employment data for May showcased a resilient labour market, with the employment change figure for May coming in at 39.7k versus the expected figure of 30.5k, in addition to the nations unemployment rate coming in as expected at 4% which is lower than the prior rate of 4.1%. Yet, despite the positive data the Aussie does not appear to have gained following the release. Nonetheless, Aussie traders may be interested in the release of Australia’s Judo bank manufacturing PMI figure for June next week. Should the figure showcase that the manufacturing sector of the economy has escaped contraction territory, we may see some support for the Aussie and vice versa. On a monetary level, we note RBA’s interest rate decision which is set to occur next week. The majority of market participants are currently anticipating the bank to remain on hold, with AUD OIS currently implying a 97.4% probability for such a scenario to occur. Hence our attention turns to the bank’s accompanying statement, where should RBA policymakers imply that the bank may cut interest rates this year, it could weigh on the Aussie. On the flip side, should it be implied that the bank may keep interest rates higher for a greater period of time, it could instead provide support for the Aussie.

CAD – BoC preparing for more rate cuts?

The CAD is about to end the week relatively unchanged against the USD. It should be noted though that Canada’s building permits rate on a mom level for April vastly exceeded expectations by coming in at 20.5%, which was significantly higher than the expected and prior rate which were 4.9% and – 12.3% respectively. On a monetary level, we note that BoC Governor Tiff Macklem appears to have maintained his stance since last week, as he appears to have once again implied during his speech earlier on this week that the bank may continue easing its monetary policy. In particular, he stated that there’s enough cooling in the economy to start bringing rates lower, which in turn could weigh on the Loonie. On a fundamental level, we note that the recent rise of oil prices seems to have aided the CAD, given Canada’s status as a major oil-producing economy. The international oil market seems to be caught between conflicting fundamentals once again, as on the one hand the signals deriving from the US oil market seem to contradict one another. Nonetheless, should we see oil prices continuing their upwards trajectory in the coming week we may see them having a positive impact on the Loonie. In the coming week we would note the release of the retail sales rate rates for April , yet we tend to view that the CAD’s direction may be dictated by fundamentals and may cede control to other currencies in the coming week.

General Comment

As an epilogue, we tend to see the USD giving up some of its influence in the FX market, given that the frequency and gravity of US financial releases and monetary policy events are expected to decrease in the coming week. As for US stock markets, we note a positive mood of market participants in the past few days being more evident in S&P 500 and Nasdaq which once again reached new record highs. However, we highlight the divergence of the Dow Jones which is on track to end the week in the reds. We tend to highlight though, that the main driver behind US stock markets may be the tech sector. Should we see the positive market sentiment being maintained, we may see US stock markets rising further. As for gold, we see the negative correlation of the precious metal to the USD was once again on display in the past few days. It should be noted that the recent decline of US yields may have alleviated some of the downwards pressures on gold’s price, as the attractiveness of US Bonds as safe haven instruments tends to be reduced.

If you have any general queries or comments relating to this article please send an email directly to our Research team at research_team@ironfx.com

Disclaimer:

This information is not considered as investment advice or an investment recommendation, but instead a marketing communication. IronFX is not responsible for any data or information provided by third parties referenced, or hyperlinked, in this communication.