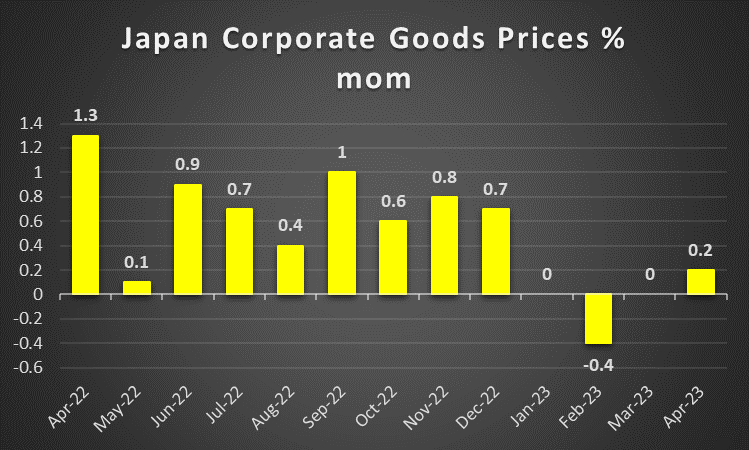

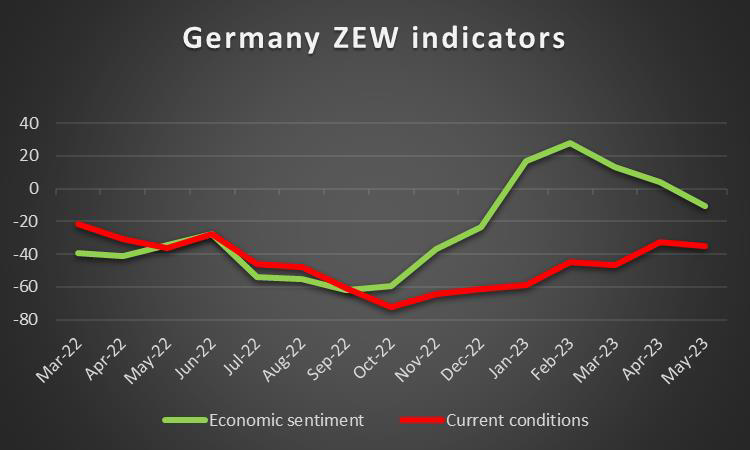

A rather easy-going week is about to end as we open a window to what next week has in store for the markets. On the monetary front, we highlight the Fed’s interest rate decision on Wednesday, yet also note ECB’s and BoJ’s interest rate decisions on Thursday and Friday respectively. As for financial releases, we make a start with a light Monday where we get Japan’s Corporate goods prices for May, while on Tuesday we note the release of the UK’s employment data for April, Germany’s ZEW indicators for June and we highlight the US CPI rates for May. On Wednesday we get UK’s GDP and manufacturing output rates for April and the US PPI rates for May. In a packed Thursday we note the release of New Zealand’s GDP rates for Q1, Japan’s machinery orders for April and trade data for May, Australia’s employment data for May, China’s urban investment, industrial output and retail sales for the same month, while from Canada we get May’s number of House starts and April’s manufacturing sales and end the day with the USD retail sales for May. Finally, on Friday we get the Preliminary US University of Michigan consumer sentiment for June.

USD – The Fed under the spotlight

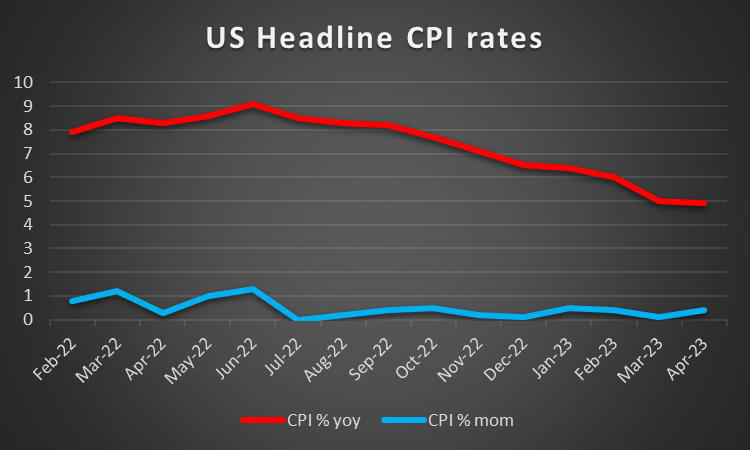

The USD seems to be edging lower against its counterparts for the week as it had a rather light calendar in the past few days. The market’s attention tends to be turned toward the Fed’s intentions which are expected to become clearer with the bank’s interest rate decision next Wednesday. The market’s expectations are currently for the bank to skip a rate hike in its June and Fed Fund Futures imply a probability of 70.9% for such a scenario to materialise. Yet the market’s expectations may alter before the release as on Tuesday we get the US CPI rates for May. Should the core and headline CPI rates show an easing of inflationary pressures in the US economy, we may see the market’s expectations for the bank to remain on hold intensifying, while a picture of a rather sticky inflation, may take the markets by surprise and increase the chances for a possible rate hike, thus supporting the USD. Should the bank remain on hold as the market expects we may see little effect on the USD, while another 25 basis points rate hike could asymmetrically strengthen the greenback. Besides the interest rate as such also considerable attention is to be placed on the forward guidance. Should the bank maintain a hawkish tone that could foreshadow another rate hike in its next meeting, we may see the USD gaining while an absence of any hawkishness could weaken the USD. Also, we remind readers that the new dot plot is to be released and should it show that Fed policymakers intend to keep rates at high or even higher levels for a prolonged period, contradicting market expectations for possible rate cuts near the end of the year, that could be an additional reason for the USD to gain. Furthermore, we also note the release of the new economic projections, given the market worries for a possible recession in the US economy, but also Fed Chairman Jerome Powell’s press conference later on, as he is well known to be able to alter the market sentiment.

GBP – UK’s trade deal with the US

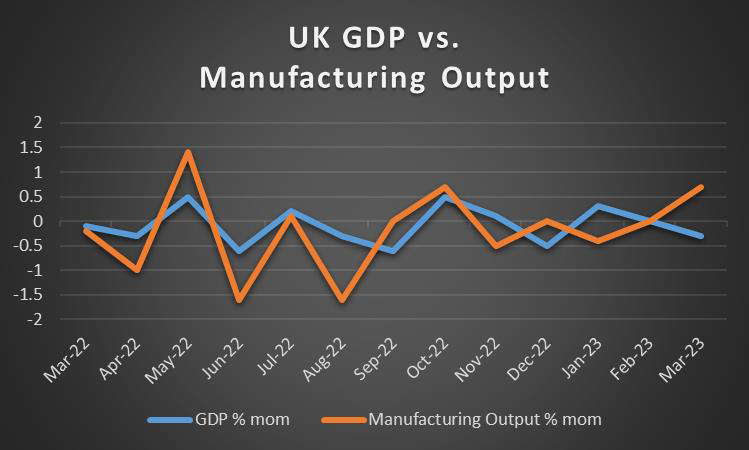

The pound seems about to end the week higher against the USD, JPY and EUR in sign of wider strength. On a fundamental level, we note the UK’s Government to strike a trade deal with the US. During Brexit, the possibility of a big, fat free-trade deal between the UK and the US, was considered as the main prize that would counter the negative effects of Brexit. Yet such a US-UK trade deal seems to be off the calendars for the short to medium term, as UK Prime Minister Sunak, while on his way to visit the US about the issue admitted that such a trade deal is not a priority. For the time being the aim seems to be a trade deal regarding a narrow spoke of products such as critical minerals and/or in the digital sector. Also, we note the UK Government’s efforts to enhance the country’s leading role in Artificial intelligence as it prepares to host the first summit about the issue. Overall though we still see Brexit weighing on a fundamental level on the UK economy. On the monetary front, it seems that the market’s expectations for another rate hike in the bank’s next meeting are very high and that may keep the pound supported on a monetary level. On a macroeconomic level, we note that the Halifax House prices erased the contraction noted in April by reaching stagnation levels in May, yet we still see the tightening of BoE’s monetary policy as weighing on the UK real estate sector. We highlight next week’s financial releases that may enhance the interest of pound traders especially the release of April’s employment data and April’s GDP rates.

JPY – BoJ’s interest rate decision in focus

JPY seems to have little changed against the USD, yet is losing ground against the EUR and GBP for the week. For the Yen in the coming week, BoJ’s interest rate decision on Friday seems to stand apart. The market expects the bank to remain on hold at -0.10% and JPY OIS seems to imply an 89% probability for such a scenario to materialize. We would like to note BoJ Governor Ueda’s statements on Wednesday that “When achievement of our price target is foreseen, we will debate specifics (of an exit policy) at our policy meeting and disclose the information,” which tended to weigh on the dovish side once again underscoring the bank’s intentions to keep its ultra-loose monetary policy settings unchanged. We expect the bank to maintain its usual dovish tone in the coming meeting as well and should that be the case we may see JPY slipping. On a more fundamental level, we still highlight JPY’s dual nature as a safe haven and a national currency and should we see the markets’ risk aversion being on the rise in the coming week, we may see JPY getting some support. On a macroeconomic level, we note the wide contraction of the All household spending growth rate for April, implying a weakness in the demand side of the Japanese economy. Nevertheless, there seems to be an improvement given the wide acceleration for Q1’s GDP rate on a year on year level which implied a wider expansion of the Japanese economy than anticipated, which may allow for some optimism and in turn may provide some support for JPY.

EUR – ECB expected to hike rates

EUR seems about to edge higher for the week against the USD and JPY but not the pound. EUR traders are expected to focus on ECB’s interest rate decision next Thursday, as the bank is expected to hike rates by 25 basis points. For the time being EUR OIS seem to imply that the market has almost fully priced in such a scenario, as they imply a 96.64% probability for such a scenario to materialize. We note that the market seems to expect another 25 basis points rate hike in ECB’s July meeting, before pausing its rate hiking path. Hence for the EUR to get some support from the release, the bank may have to deliver the rate hike expected, yet also hint towards another rate hike probably by maintaining a hawkish tone in its accompanying statement and during ECB President Christine Lagarde’s press conference later on. Should there be any signs of hesitation we may see the common currency weakening. It should be noted though that the preliminary release of the Eurozone’s HICP rate for May showed a substantial slowdown which may ease the pressure on the bank, to actually proceed with another rate hike in its July meeting. On a macroeconomic level we note the widening of Germany’s trade surplus for April and the acceleration of the industrial output growth rate for the same month, yet for the Eurozone as a whole, the situation still seems dire as the Sentix index dropped deeper into the negatives implying an even wider pessimism for the area.

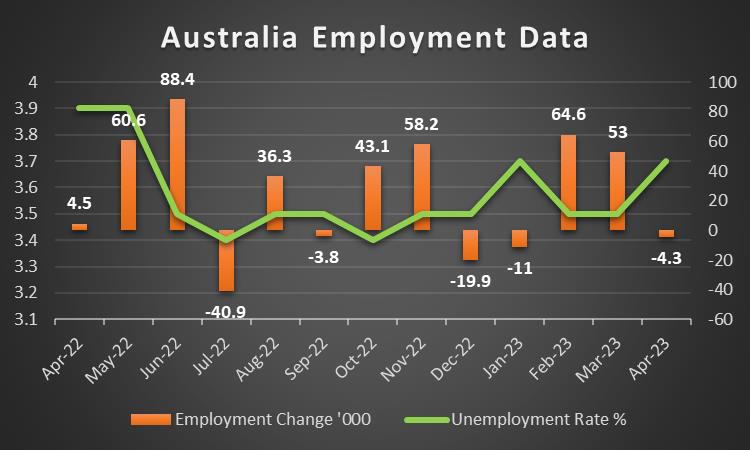

AUD – RBA took the markets by surprise

AUD is about to end the week stronger against the USD for the second week in a row. RBA’s interest rate decision on Tuesday may have been a key factor behind AUD’ strengthening as the bank took the markets by surprise by delivering a 25 basis points rate hike. RBA Governor Lowe, in his statement, mentioned that “Inflation in Australia has passed its peak, but at 7 per cent is still too high and it will be some time yet before it is back in the target range” while in his forward guidance stated that “Some further tightening of monetary policy may be required to ensure that inflation returns to target in a reasonable timeframe”. The forward guidance tends to foreshadow more rate hikes to come, which was an additional element supporting the Aussie. On a macroeconomic level, we highlight the slowdown of the GDP rate for Q1, implying that the Australian economy expanded to a lesser extent than expected. We highlight Australia’s employment data for May next Thursday as the Aussie’s next big test on a macroeconomic level. On a more fundamental level we remain worried about the renewed tensions in the US-Sino relationships that may weigh on AUD should they escalate further. Furthermore, China’s trade data for May were disappointing as both the import and export growth rates contracted and the trade surplus was slashed by almost a third, intensifying market worries for China’s economic rebound and possibly for a contraction of Australian exports of raw material to the Chinese mainland.

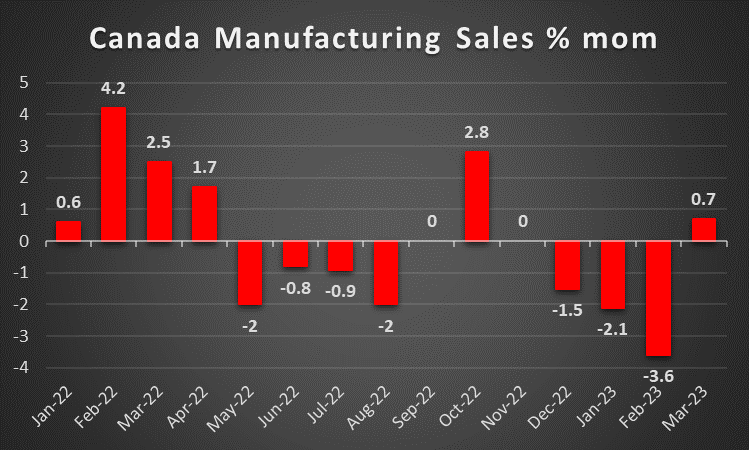

CAD – BoC also hiked rates

The Loonie is about to end the second week stronger against the USD, yet Canada’s employment data for May are still to be released and could alter its direction. Nevertheless, BoC’s surprise 25 basis points rate hike on Wednesday provided some support for the CAD. The bank in its accompanying statement noted the tick-up of inflation for April yet still expects the CPI rates to ease to around 3% in the summer. Furthermore, the comments made by the bank that “concerns have increased that CPI inflation could get stuck materially above the 2% target” feeding market expectations for another 25 basis points rate hike in the bank’s July meeting. On a more fundamental level, we note the wildfires in Quebec and Ottawa, with more than 9.3 million acres “charred,”. The situation besides the environmental catastrophe may also have an adverse effect on the Canadian economy. Also on a fundamental level, we note that oil prices seem to be little changed thus failing to have a material effect on the Loonie in either direction. Market worries about the demand side of the commodity seem to have countered Saudi Arabia’s pledge for the cut of oil production levels, currently. Yet the tightening of the US oil market, should it continue in the coming week, may provide some support for oil’s price thus also supporting the Loonie. On a macroeconomic level, we expect it to be rather slow for CAD traders, given the low number of high-impact financial releases stemming from Canada, thus fundamentals may be in the forefront.

General Comment

In the coming week, we expect the USD to get more of the initiative in the FX market over other currencies and lead the way, given that the number of high-impact financial releases stemming from the US, is to be increased. Staying in the FX market the Turkish Lira was considered to be in free-fall mode, reaching all-time low levels, as USD/TRY reached 23.4 and as state officials allegedly stated they will halt dollar sales in order to defend it. Recep Tayyip Erdoğan’s unorthodox economic policies leave the TRY negatively predisposed for further deterioration and should no intervention take place we may see the devaluation rate accelerate even further. On Wednesday USDTRY soared by more than 7% intraday, with no slowdown in sight and Goldman Sachs FX market strategists foresee the Lira closing at the 28 level against the USD within the next year. Despite a relative stabilisation on Thursday, the bearish sentiment seems to be still present for the Lira though and on a macro level, we note that Turkey’s Net FX reserves are still in the negatives. On the other hand, the Turkish Government seems to be placing in key positions such as the Finance Minister and head of the Turkish Central Bank, persons of more orthodox economic orientation in an effort to convince the markets of a normalization. US stock markets continue to send out mixed signals, implying rather undecisive markets, with Nasdaq edging lower as the index corrects amidst the market’s acute interest in Artificial Intelligence. As for gold, we note the gains made for the week, possibly as a result of its negative correlation with the USD. We expect the negative correlation of the two instruments to continue leading gold’s price in the coming week and also expect some increase in volatility, as US high-impact financial releases are to multiply.

Si tiene preguntas generales o comentarios relacionados con este artículo, envíe un correo electrónico directamente a nuestro equipo de investigación a research_team@ironfx.com

Descargo de responsabilidad:

Esta información no debe considerarse asesoramiento o recomendación sobre inversiones, sino una comunicación de marketing. IronFX no se hace responsable de datos o información de terceros en esta comunicación, ya sea por referencia o enlace.