The week is slowly nearing its end and we open a window at what next week has in store for the markets. On Monday we get Germany’s Ifo Business climate for August and from the US the durable goods orders for July. On Tuesday we get UK’s CBI distributive trades and the US consumer confidence, both for August. On Wednesday we get from Australia July’s CPI rates for July and UK’s nationwide house prices for August could be also released. On Thursday we get Australia’s Capital Expenditure for Q2, Sweden’s final GDP rate for Q2, Eurozone’s Business Climate for August, Canada’s Business Barometer for the same month, Germany’s preliminary HICP rate for August and from the US we highlight the release of the second estimate for the GDP rate for Q2 and also note weekly initial jobless claims while from Canada we get the current account balance for Q2. On Friday we get from Japan Tokyo’s CPI rates for August, Australia’s retail sales for July, France’s final GDP rate for Q2 and preliminary CPI rates for August, Switzerland’s KOF indicator for the same month, the Czech Republic’s final GDP for Q2, Eurozone’s preliminary HICP rate for August, the US consumption rate for July, the US Core PCE price Index for July, Canada’s GDP rates for Q2 and the final US University of Michigan consumer sentiment for August and we also note the release of the China’s NBS PMI figures for August.

USD – US Core PCE rates for July eyed

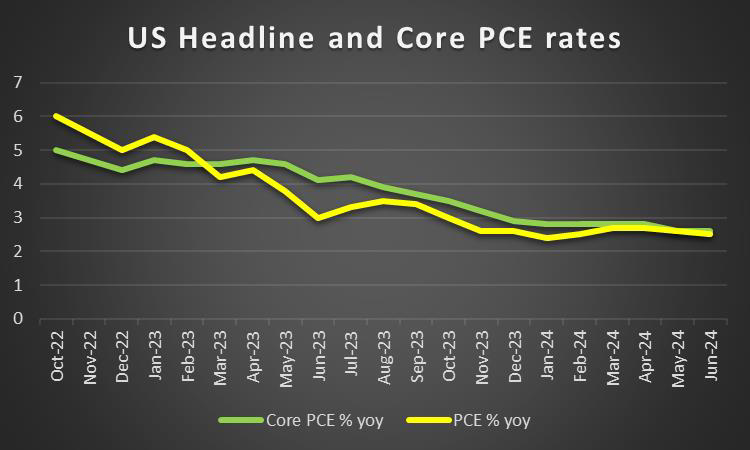

The USD may be the main loser in the FX market for the week. As these lines are written, Fed Chairman Powell has still to deliver his speech at the Jackson Hole Economic Symposium. Monetary policy has been a major issue for the USD in the past week and we expect it to continue affecting the greenback in the coming week as well. The release of the Fed’s July meeting minutes on Wednesday, tended to reaffirm the market’s expectations for the bank to start cutting rates in its next meeting in September as a large number of Fed policymakers tended to acknowledge the need for the bank to start easing its monetary policy, especially as a weakness in the US employment market was identified. Given that the release met the market’s expectations it had little effect on USD, US stock markets and gold’s price. The market’s expectations are for the bank to start cutting rates in the September meeting yet also deliver another rate cut in the November meeting and a double rate cut in the December meeting, implying a reduction of rates of 1 full percent before Christmas. Τhe market’s expectations may be somewhat overstretched, yet its dovish orientation is crystal clear and any incident contradicting it, could force the market to reposition itself and thus provide asymmetric support for the USD, while at the same time could weigh on US stock markets and gold’s price. On the contrary should the market’s expectations be verified in any way; we may see the USD continuing to slip and US stock markets and gold be allowed to continue their upward motion. On a macroeconomic level, we note the release of the Benchmark Payrolls indicator on Wednesday, which showed that the number of jobs created in the American economy in the period April 23-March 24 was overstated by 818k. The release tended to highlight additional weakness in the US employment market, as well as some degree of uncertainty for the current actual NFP figures released, which could enhance the possibility of the Fed cutting rates. In the coming week we note the release of the US GDP Rate for Q2, yet also highlight the release of the core PCE rates for July, the Fed’s favorite inflation metric. Should the rates slow down showing further easing of inflationary pressures in the US economy, we may see the USD slipping on Friday’s American session.

GBP – Easy going week for pound traders

Overall the pound seems to have remained supported in the past week, maybe the winner in the FX market as it gains against the USD, EUR and the JPY. On a monetary level, we note the market’s expectations for the Bank of England for two rate cuts until the end of the year. Yet we also note that Reuters in a recent economists poll expects the bank to cut rates only one more time before year’s end. BoE in its last interest rate decision had decided to cut rates in a tight 5-4 majority, while BoE Governor Bailey highlighted the bank’s cautiousness towards cutting rates. Should there be signs which could alter the market’s expectations towards less rate cuts, we may see the pound be supported at a monetary policy level. On a macroeconomic level, we note the release of the August Preliminary PMI figures, with special interest being placed on the services sector. Economic activity seems to have expanded at a faster pace in the UK across sectors, which tends to send a positive signal for the macroeconomic outlook of the UK. We also note the improvement of the August CBI trends for industrial order. The indicator’s reading despite remaining in the negatives, improved more than expected, implying that less UK industrialists are pessimistic for the orders coming in. Overall, we see the pound being supported in the coming week and given the low number of high impact financial releases planned, expect fundamentals to lead the way for pound traders.

JPY – Hawkish BoJ supports JPY

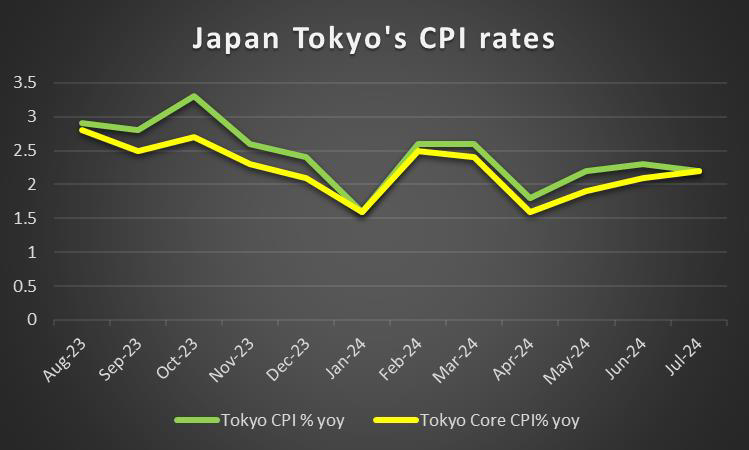

For the JPY, BoJ’s monetary policy may be the main factor dictating its direction for the time being. The bank’s hawkish intentions became even clearer after the testimony of BoJ Governor Ueda, before the Japanese Parliament. The market expects the bank to deliver another two rate hikes until the end of the year and we would not be surprised to see the bank delivering what the market asks for. The case for more rate hikes was enhanced during today’s Asian session on a macroeconomic level, as Japan’s CPI rates for July highlighted the persistence of inflationary pressures in the Japanese economy. Overall, we tend to view JPY as being supported on a monetary policy, which in turn may keep JPY shorting at bay for a while. On a macroeconomic level, we note the acceleration of the machinery orders growth rate for June, implying greater trust of businesses to the prospects of the Japanese economy. On the other hand, the country’s trade surplus turned into a deficit in the past month, which by the way was wider than expected, highlighting the outflow of wealth from the Japanese economy through its international trading transactions. In the coming week we highlight Friday as a key day given the slew of high-impact economic data to be released which are related to inflation, supply and demand of the Japanese economy. Other than that we may see JPY setting fundamentals in the driver’s seat.

EUR – August’s preliminary HICP rates in the epicenter

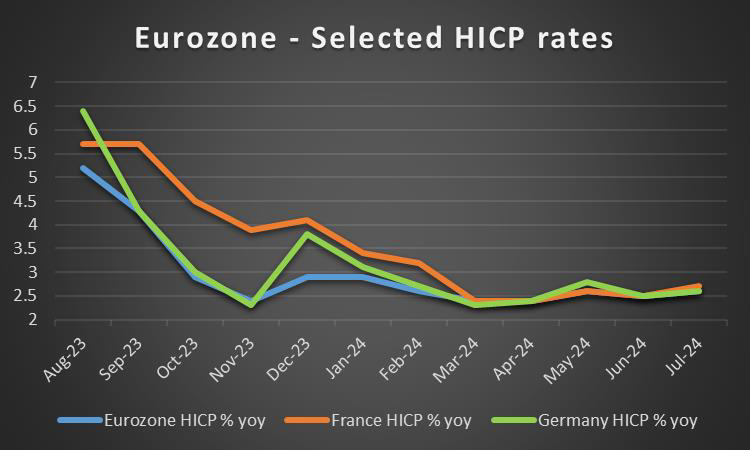

In the European theatre we highlight the release of the preliminary PMI figures for August on Thursday. The release showcased the weakness of the manufacturing sector in the area. Germany’s as well as France’s manufacturing sectors have suffered another, this time deeper contraction of economic activity, which was reflected on the Eurozone as a whole, as other country members were not able to cover. On the contrary, the services sector seems to have been able to expand economic activity for the month, with tourism being the main driver given the summer, but France’s services sector got a special treat given the Olympics in Paris. Yet tourism as a sector may be considered as too volatile to rely on, while the Olympics should be considered as a one-off event. Hence, we highlight our worries for the area on a macroeconomic level. At a monetary level, the market expects the ECB to continue cutting rates in the coming September’s meeting, while another two 25 basis points rate cuts have been priced in by the market until the end of the year. The market’s expectations may weigh on the EUR given that the interest rates between other central banks and the ECB may start diverging at a faster pace. In the coming week we get the final GDP rate of France for Q2 and highlight the release of the preliminary HICP rates of Germany, France and the Eurozone as a whole. Should the HICP rates slow down, we may see the EUR weakening as the market’s expectations for extensive rate cuts by the ECB could solidify further, while a possible acceleration could send the bank’s rate cutting path into doubt, supporting the EUR.

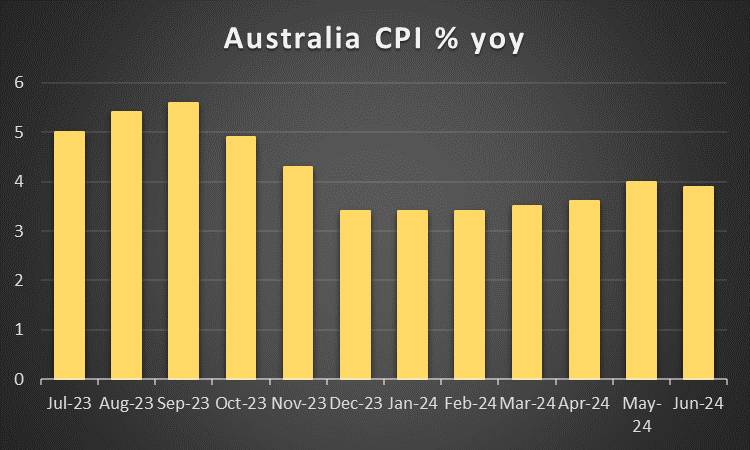

AUD – Australia’s CPI rates for July in focus

On a fundamental level, the Aussie got some support given the improved, risk oriented market sentiment of the market. The Aussie tends to gain under such conditions as it is considered a riskier asset in the FX market given its commodity nature. Hence, should the positive market sentiment be maintained in the coming week as well, we may see the Aussie gaining further and vice versa. Also, given its commodity nature we highlight the close Sino-Australian ties, as Australia exports a substantial number of raw materials to China. Given that the Chinese manufacturing sector is struggling to keep economic activity afloat, things are not looking good for the Aussie as well. In the coming week, on the last day of the month we get China’s NBS PMI figures for August and a possible improvement of the indicator’s reading could benefit the Aussie as well and vice versa. On a monetary level, the Aussie remains supported, as RBA maintains a tight financial environment with high rates. The release of the bank’s August meeting minutes highlighted RBA’s decisiveness to lower inflation. In the meeting the bank despite a temptation for another rate hike, decided to keep rates steady for an extended period which could also keep the Aussie supported at a monetary level, given that most central banks are preparing or are already cutting rates. Hence, we highlight the release of Australia’s CPI rates for July on Wednesday’s Asian session and a possible

acceleration of the rates could restart the discussion for a possible rate hike by the bank thus supporting AUD.

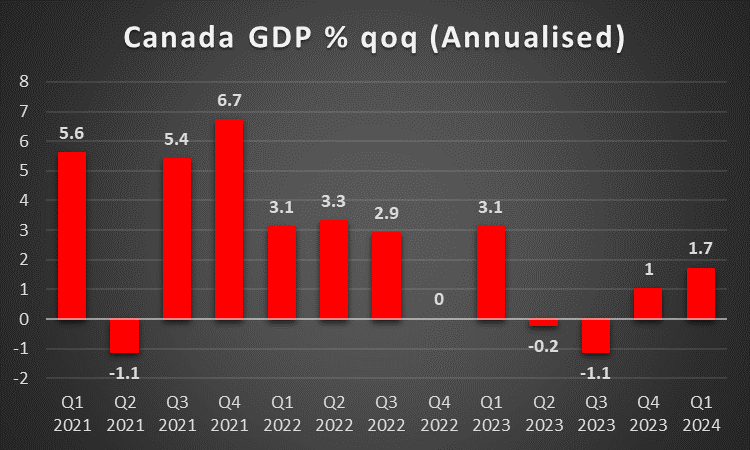

CAD – GDP rates for Q2 to move the Loonie

We make a start for the Loonie with fundamentals, as the Canadian National Railways and the Canadian Pacific Kansas City, locked out more than 9000 unionized workers yesterday. The action of the two railway companies practically shut down nationwide freight rail shaking the rails upon which North American supply chains roll. Ottawa has announced swift action, yet the results remain to be seen and the incident seems to have weighed on the Loonie. On a deeper fundamental level, we note that the steep drop of oil prices in the past week, should it be continued in the coming week as well, may have an adverse effect on the Loonie as well given Canada’s status as a major oil producing economy. For the time being the drop of oil prices seems to be related with the easing of market worries for the tensions in the Middle East. Yet should the proposed US ceasefire agreement fall through, we may see oil prices getting asymmetric support, thus providing support for the Loonie as well. On a macroeconomic level we note the easing of inflationary pressures in the Canadian economy for July, given the release of the CPI rates for the particular month. The release seems to have enhanced somewhat the market’s expectations for BoC to cut rates in the coming meeting, while another two rate cuts seem to have been priced in by the market until Christmas. In the coming week, we highlight the release of the GDP rates for Q2 and a possible slowdown could weigh on the CAD as it would imply that the Canadian economy grew at a slower pace, but also may be adding more pressure on BoC to proceed with extensive rate cuts.

General Comment

As an epilogue, in the FX market we expect the USD to relent some of the initiative to other currencies, given that the gravity and frequency of US high impact financial releases tends to ease. As for US stockmarkets, we note that the earnings season is slowly calming down, yet would like to note the release of the earnings reports of NVIDIA and Hewlett Packard on Wednesday. Overall as mentioned before the positive market sentiment which was witnessed in the past week seems to be related to the market expectations for the Fed to start cutting rates, hence should they be maintained we may see US stockmarkets rising higher. We still maintain our concerns for the US stockmarkets being overpriced though and highlight the risk of an extensive correction lower. As for gold’s price we note that the negative correlation of the precious metal’s price with the USD was interrupted in the past week. Gold traders seem to have booked in some profits after the precious metal’s price reach new record high levels thus allowing the bears to play around. It’s characteristic how the slight recovery of the USD on Thursday exercised substantial pressure on the precious metal’s price. Overall we see signs of the negative correlation between the prementioned trading instruments slowly reviving, hence should we see the USD gaining some ground in the coming week, it could weigh on gold’s price.

Si tiene preguntas generales o comentarios relacionados con este artículo, envíe un correo electrónico directamente a nuestro equipo de investigación a research_team@ironfx.com

Descargo de responsabilidad:

Esta información no debe considerarse asesoramiento o recomendación sobre inversiones, sino una comunicación de marketing. IronFX no se hace responsable de datos o información de terceros en esta comunicación, ya sea por referencia o enlace.