With the week nearing its end, we note that the BRICS summit is due to be hosted in South Africa next week, with the leaders of the group anticipated to discuss the creation of a common currency backed by a basket of commodities and/or gold. On the monetary front, we note the release from Australia’s RBA summary of opinions for its August meeting during Tuesday’s Asian session, New Zealand’s interest rate decision during Wednesday’s Asian session, the Fed July meeting minutes on Wednesday and Norway’s interest rate decision on Thursday during the European session. As for financial releases, we make a start on Tuesday with Japan’s GDP rate and continue with Australia’s Wage Price index rate, both for Q2, China’s Industrial Output rate and Japan’s chain store sales rate, both for July, the UK’s employment data for June, Sweden’s CPI rate for July, Germany’s ZEW economic sentiment figure for August and end the day with the US retail sales rate and Canada’s BOC Core CPI rate both for the month of July. On Wednesday, we note the release of the UK’s CPI rates for July, the Eurozone’s revised GDP estimate for Q2 and the industrial production rate for June, followed by Canada’s wholesale trade rate for June and the US industrial production rate for July. On Thursday, we make a start with Japan’s machine orders rate for June and trade data for July, Australia’s Employment data for July and later on during the day, the US weekly initial jobless claims figure and the US Philly Fed Business index figure for August. Lastly, on an easy-going Friday, we note Japan’s CPI rates and the UK’s retail sales rate both for the month, followed by the Eurozone’s final HICP rate and Canada’s producer prices rate all being for July.

USD – US CPI rates hint at easing inflationary pressures

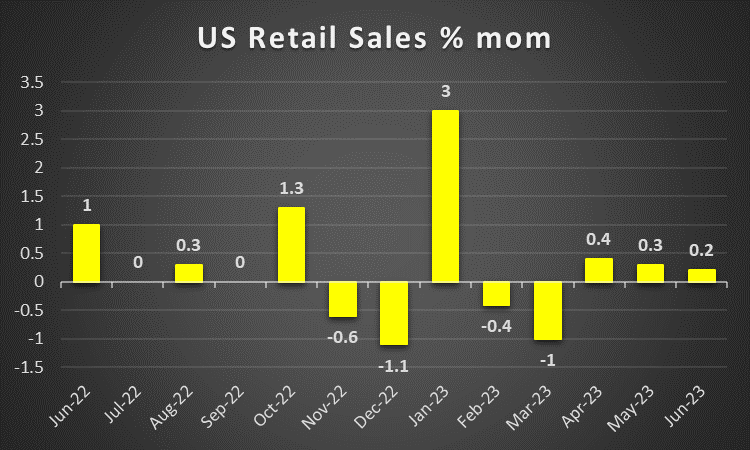

The USD continued its upward trajectory against its counterparts for a fourth week in a row despite a lower-than-expected CPI print on Thursday. On a fundamental level, we highlight that with two weeks remaining before the first Republican presidential debate, the following candidates according to the Associated Press have currently made the “cut”, Former President Donald Trump, Florida Governor Ron DeSantis, South Carolina Senator Tim Scott, former US Ambassador to the UN Nikki Haley, Vivek Ramaswamy, former Vice President Mike Pence, former New Jersey Governor Chris Christie and North Dakota Governor Doug Burgum. Furthermore, Moody’s credit rating agency, downgraded a number of mid-sized banks late Monday and warned that it may also downgrade some of the larger US banks. The credit rating agency cited that funding risks and weaker profitability were possible in the sector justifying the downgrade, with the credit rating agency changing its outlook to negative for eleven major US lenders, where should the banking sector worries resurface, we may see heightened fear and panic amongst US investors of a repeat of SVB’s collapse in March. On a monetary level, we highlight the numerous Fed policymakers who spoke throughout the week, with no clear consensus as to how the Fed may proceed. The numerous Fed policymakers seemed to be contradicting each other, with Atlanta Fed President Bostic, Chicago Fed President Goolsbee, New York Fed President Williams and Philadelphia Fed President Harkin, all implying that the Fed may be nearing its peak rate and as such potentially diminishing the case for the Fed to continue its aggressive rate hiking path. On the other hand, Fed Board Governor Bowman and Richmond Fed President Barkin appeared to provide a contradicting opinion, in our opinion opening the door for at-least another rate hike by the Fed, as such traders may be interested in the release of the Fed’s July meeting minutes next Wednesday, in an attempt to navigate through the delicate landmines placed by Fed officials. On a macroeconomic level, we highlight that last Friday’s employment data appeared to be mixed, with the Non-Farm Payrolls coming in lower than expected, whilst the Unemployment rate declined thus potentially indicating that despite the resilient labour market, that support may be fading. Lastly, the US CPI rates released on Thursday, appeared to show easing inflationary pressures on the US economy, thus potentially weakening the Fed’s willingness to continue hiking interest rates, as they appear to be having some impact.

GBP – CPI rates under the microscope

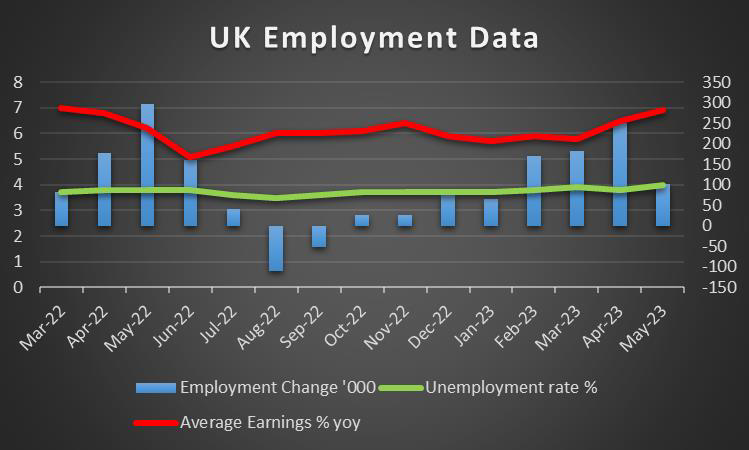

The pound seems about to end the week lower against the USD and EUR yet higher than the JPY. On a fundamental level, we note the report by Bloomberg which stated that the HBSC’s head of public affairs who is also the chair of the China-British Business Council lobby, made comments during a private event that the UK government was “weak” by giving into US pressure to reduce its business dealings with China. The statement could place a strain on the relationship between the UK and the EU and the US who are actively attempting to formulate a common strategy to counter China’s growing influence respectively. On a monetary level, BoE Pill stated during a Q&A session on Monday, the inflation from food prices may still remain high for the foreseeable future and that “the days of seeing food prices fall — that does seem to be something that we may not be seeing for a little while yet if in the future at all”. Potentially indicating that food inflation could potentially skew inflation data to the upside, thus generating two scenarios where the BoE may be closer to its terminal rate if food inlfation data is excluded, or where the BoE may have to maintain a higher level of interest rates in order to combat inflationary pressures for the long run. On a macroeconomic level, the GDP rates released earlier today, showed an acceleration yet are still at low levels. The growth of the GDP rates for Q2 and June, despite providing some comfort are still worryingly low as BoE’s high-interest rates appear to be strangling the economy, yet inflation still remains far too high. That brings us to the issue mentioned earlier and a moral question might be raised to the BoE, in which they may have to consider forcing the UK economy to potentially enter a recession in order to curb inflation or to remain at current levels and try to tackle inflation over a prolonged period of time, yet such a scenario may keep economic growth at anemic levels.

JPY – BOJ’s summary of opinions shows no imminent changes

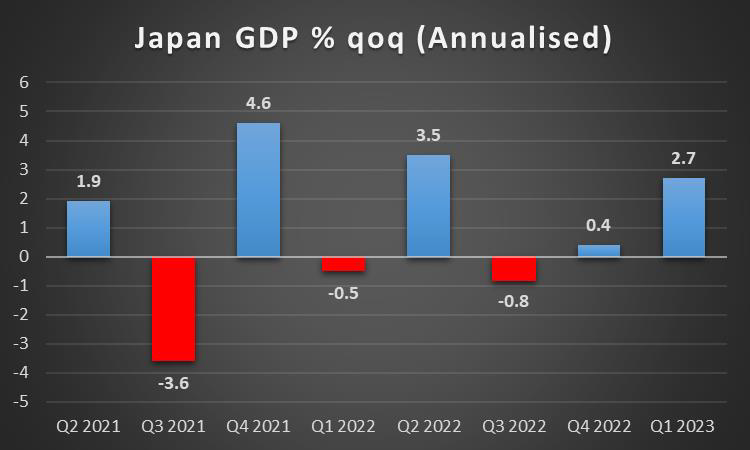

JPY is about to end the week lower against the USD the EUR and the pound in a sign of a wider weakness. On a fundamental level, we note the continued elevated tensions between Japan and China over the issue of Taiwan, with China according to news outlets, condemning remarks made by former Japanese Prime Minister Taro Aso, during a trip to Taiwan, that Japan must have a “readiness to fight”. On a monetary level, we note the release of BoJ’s summary of opinions for July, in which it was stated that “the Bank needs to patiently continue with monetary easing toward achieving the price stability target”. Implying that there might not be any plans currently to switch from the bank’s ultra-loose monetary policy, thus in our opinion, prolonging the inevitable rate hike by as much as possible. On a macroeconomic level, we highlight the acceleration of the household spending rate on a mom level which came in at 0.9% compared to the expected reduction of -1.1%, implying that Japanese households have actually increased their spending on a mom basis, despite the rate coming in lower on a yoy level. Furthermore, Japan’s current account figure which was released on Tuesday for the month of June, was indicative of a resilient Japanese economy in spite of mounting pressures from high interest rate levels from overseas governments. Lastly, we should note that Japan’s preliminary GDP rate for Q2 is due to be released on Monday, the machine orders rates for June and trade balance figure for July are due to be released on Thursday and lastly, the CPI rates for July is due to be released on Friday.

EUR – Inflation to remain too high for too long?

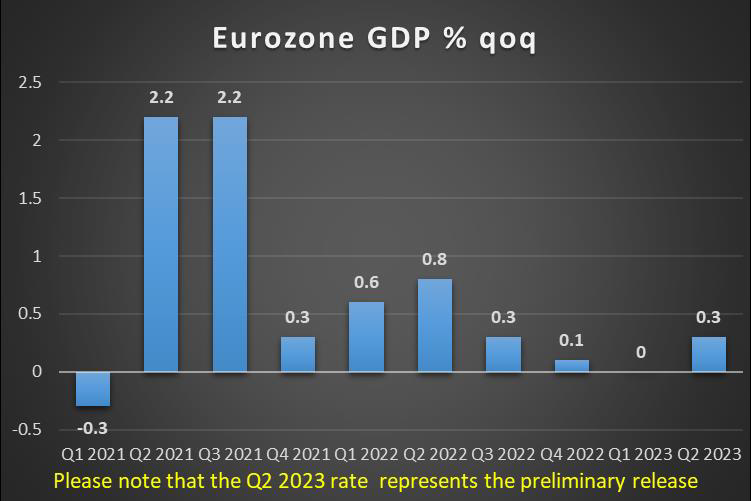

EUR is about to end the week in the greens against JPY and the pound yet seems to be losing some ground against the greenback On a fundamental level, we highlight the possibility of a continued deterioration in EU-China relationships with Germany also fearing that its economy may be further weakened by continued actions against China due to their wide trading relationship. On the monetary front, we note the ECB’s economic bulletin which was released on Thursday. The report stated that the ECB anticipates that inflation will continue to decline but will remain “too high for too long”, potentially indicating that the ECB may have some way to go with interest rates before inflation is brought down to an acceptable level. However, there is a risk that the ECB recognises as it also stated that the short-term economic outlook for the euro area has deteriorated, due to weak domestic demand. Therefore, begging the question of whether or not the ECB will increase interest rates or if they decide to allow weaker economic conditions to bring inflation down gradually through decreased consumer spending, which in turn brings prices lower in order to entice consumers to purchase goods and services thus gradually bringing inflation to lower levels. On a macroeconomic level, we note the lack of high-impact releases by the EU area, with the only release of significance being the Sentix investor confidence index figure which was indicative of an improvement in investor confidence and France’s HICP rates coming in lower as expected, indicative of easing inflationary pressures in the 2nd largest economy in the Eurozone. Lastly, we highlight the Eurozone’s revised GDP figure for Q2 and the industrial production rate which are both due next Wednesday and the Eurozone’s final HICP rate which is due on Friday.

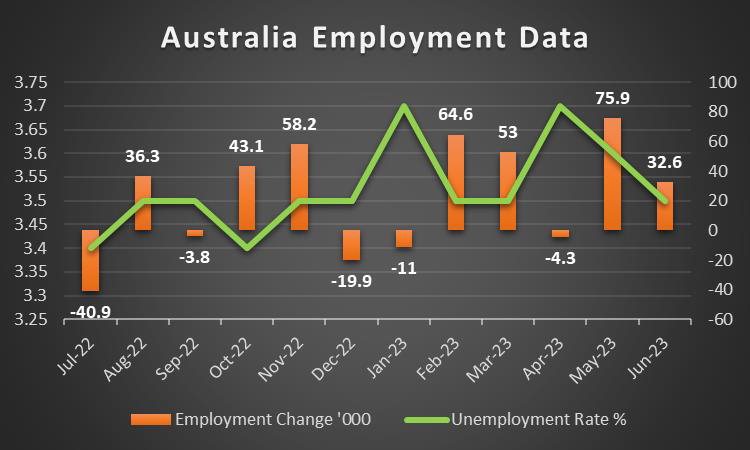

AUD – Australian economic resilience in doubt following China’s trade data

AUD is about to end the week lower against the USD. On a fundamental level, we note that Australian LNG producers are scrambling to reach a deal with unions on Thursday, in an attempt to avert a potential strike that could possibly disrupt 10% of the world’s liquified natural gas supply. With FT citing a 40% increase in European natural gas prices on the heels of supply fears. On a monetary level, we note the statements by outgoing RBA Governor Lowe, who remained hawkish, stating that it’s “too early to declare victory” and further interest rates increases are “possible” if the rise of earnings income continues to accelerate or spikes especially for particularly for services. Furthermore, traders may be interested in the release of the RBA’s August meeting minutes next Tuesday, which could shed some light on the thought process behind the RBA’s decision to hike yet once again despite the faltering inflation data. On a macroeconomic level, we note the lack of financial releases from Australia, yet China’s worsening trade data, in particular, the reduction in imports by approximately 12.4% could be considered a very worrying sign for the Australian economy in the long run, which is predominantly dependent on Chinese demand for their exports, as such should the economic situation deteriorate in China, we may see the Aussie weakening. Lastly, we turn our attention to next week’s financial releases with the wage price index rate for Q2, due to be released on Tuesday, and the employment data for July on Thursday, which may provide some indication for traders in regard to the tightness of the Australian labour market.

CAD – Trade balance hints at a worrying picture

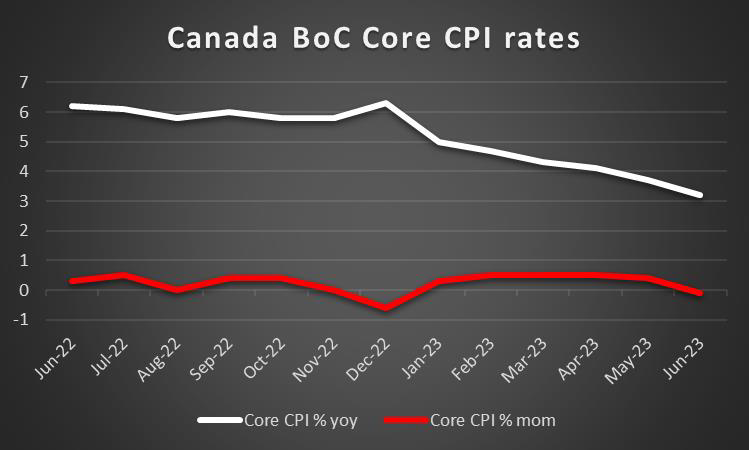

The Loonie appears to be ending the week in the reds against the dollar. On a fundamental level, we note the string of deteriorating relationships between China and major economies may have also spread to Canada, with the Canadian Government claiming that China has targeted one of its lawmakers in a disinformation campaign. The event could potentially strain the relationship between the two countries. Also, we note that oil bulls appear to be in control of the commodity’s price, with the liquid gold appearing to be moving in an upwards trajectory, despite some perceived hesitation last week, as a report by Reuters is claiming that Saudi Arabia, the worlds top oil exporter has raised prices for most of its crude sales to Asia following the extension of its voluntary production cut to September. Therefore, due to Canada’s main export being oil, the economy, in the long run, may experience benefits by association benefited due to higher prices of oil as a result of Saudi Arabia’s higher oil prices. As such, should the price of oil maintain its current course, we may see some support for the Loonie in the long run. However, Canada’s trade balance figure which was released on Tuesday seemed to paint a different picture, with the figure deteriorating to a greater extent than what was expected, thus potentially indicating that as a whole, the Canadian economy may be suffering some setbacks. Therefore, traders may be looking to next week’s BoC CPI rates for July which are due to be released on Tuesday, Canada’s wholesale trader rate for June and lastly on Friday, Canada’s producer prices rate for July.

General Comment

In the coming week we expect volatility in the FX market to ease given that a traditional holiday month for European and North American traders has begun. Yet some financial releases could still potentially have a substantial impact on certain trading instruments. We also note that the earnings season in the US appears to be slowing down, as most high-profile companies have already released their earnings reports. Nonetheless, we would note Super League Gaming (#SLGG) on Monday, Home Depot(#CGC) on Tuesday,

JD.com (#JD.com) and Cisco Systems (#CSCO) on Wednesday and Walmart (#WMT) on Thursday are expected to release their earnings. As for gold’s price, we note its decline over the week as the USD remained at high levels as did US yields. But the BRICS summit is due next Tuesday, with RT having claimed that the group could be discussing a common currency backed by gold. In the event that a discussion is made on returning to the gold standard, we may see substantial volatility in the gold markets. On a more fundamental level, we note that the continued uncertainty about the viability of shipping routes via the black sea created by the war in Ukraine tends to remain present and appears to be still influencing commodities markets.

Si tiene preguntas generales o comentarios relacionados con este artículo, envíe un correo electrónico directamente a nuestro equipo de investigación a research_team@ironfx.com

Descargo de responsabilidad:

Esta información no debe considerarse asesoramiento o recomendación sobre inversiones, sino una comunicación de marketing. IronFX no se hace responsable de datos o información de terceros en esta comunicación, ya sea por referencia o enlace.