The week is nearing its close and we open a window at what next week has in store for the markets. Monetary policy is expected to dominate the headlines as we get the interest rate decisions of the Fed from the US and BoC on Wednesday, Norway’s Norgesbank’s and UK’s BoE’s interest rate decision on Thursday and on Friday we get from Japan BoJ’s interest rate decision. As for financial releases we note on Monday the release of UK’s Rightmove House Prices for September and China’s Urban Investment, Industrial Output and Retail Sales growth rates, all being for August. On Tuesday, we get UK’s employment data for July, Euro Zone’s industrial output also for July, Germany’s ZEW indicators for September, as well as the US retail sales, Canada’s inflation metrics and the US industrial output all for August. On Wednesday, we get New Zealand’s current account balance for Q2, Japan’s trade data for August and UK’s CPI rates also for August. On Thursday, we note the release of New Zealand’s GDP rate for Q2, Japan’s machinery orders for July, Canada’s business barometer for September and from the US the weekly initial jobless claims and the Philly Fed Business index for September. On Friday, we get New Zealand’s trade data, Japan’s CPI rates and the UK’s retail sales all being for August as well as Canada’s retail sales for July.

USD – The Fed to shake the greenback

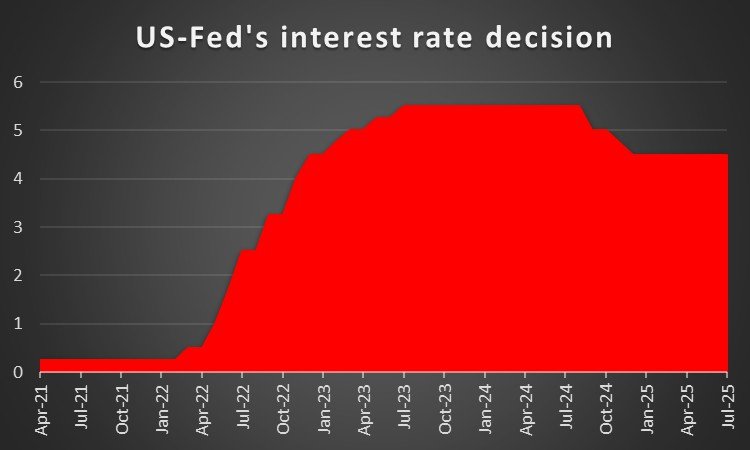

On a fundamental level, the uncertainty caused by Trump’s policies, either regarding international relations and trade policy but also given the wide internal division within the US society underscored by the murder of Charlie Kirk. The situation tends to provide headwinds for the USD, yet has largely been priced in. On a macroeconomic level, we highlight the weakness of the US employment market as highlighted by the release of the US employment report last Friday, where the unemployment rate ticked up as expected to 4.3%, yet the NFP figure unexpectedly dropped massively reaching 22k, instead of 75k expected. The release emphasized the weakness of the US employment market to create new jobs, an issue also underscored by the release of the bench mark payrolls with a downward correction of -911k for 2025 and the subsequent beyond market expectations rise of the initial jobless claims figure, which relates to the first week of September, implying that August’s weakness seems to continue in the current month. It’s characteristic that the release of the CPI and PPI rates for August was bypassed by the markets despite sending some mixed signals. Understandably the adverse data bring the US employment market in the epicenter of the market’s attention and intensified substantially the market’s dovish expectations for the Fed. Hence we highlight the release of the Fed’s interest rate decision next Wednesday, the 17th of the month. The bank is widely expected to cut rates by 25 basis points and currently Fed Fund Futures (FFF) imply a probability of 90.4% for such a scenario to materialise with the rest implying that a 50 basis points rate cut is also possible. FFF also imply that the bank is expected to deliver with another rate cut in its October meeting and a third one in the December meeting. Should the bank cut rates as expected, which is also our base scenario for now, we expect the market’s expectations to shift towards the bank’s forward guidance, which is to be included in the accompanying statement, the bank’s projections, especially the new dot plot as well as Fed Chairman Powell’s press conference later on. Should the bank in its forward guidance signal that it intends to follow the market’s expectations we may see the USD weakening moderately, while should the bank exceed its expectations we may see the greenback tumbling. On the flip side if the forward guidance shows that the bank is more restrained and hesitant to deliver another two rate cuts in October and December, we may see the USD getting asymmetric support.

Analyst’s opinion (USD)

“In our view the greenback’s direction is to be heavily influenced by the Fed’s interest rate decision, next week. Should the bank signal its readiness to ease its monetary policy by cutting rates and intend to cut rates also in October and December we may see the USD weakening. On the flip side, any hesitancy on behalf of the bank to cut rates as expected could provide support for the USD.”

GBP – BoE expected to remain on hold

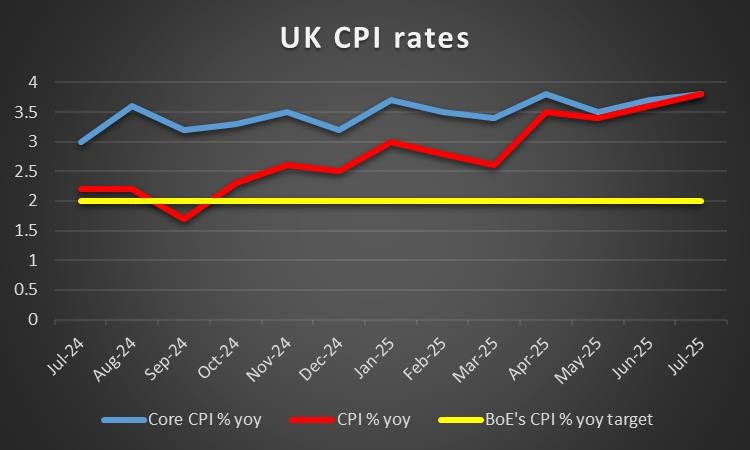

On a fundamental level, the UK Government’s fiscal difficulties continue to provide headwinds for the GDP. The rising debt servicing costs in combination with fiscal discipline, if not contractionary fiscal policy intentions tend to weigh. All eyes are UK Chancellor Reeves and how she plans to get the UK out of the fiscal mess. Her plans to tax wealth and thus increase fiscal spending may be put on ice for a while. On a macroeconomic level, we note the wide drop of UK house prices for August and wait for more clues related to the UK real estate market by the release of UK’s Rightmove house price growth rate for September on Monday’s Asian session. We also note the slowdown of GDP rate for July, implying zero growth for the UK economy, while the revelation that economic activity in the industrial sector for July, contracted substantially, hurt UK macroeconomic analysts. In the coming month we highlight the release of the UK employment data for July and a possible tightening of the UK employment market could provide some support for the pound as could a possible acceleration of the CPI rates for August. The main event of the week though for pound traders is expected to be the release of BoE’s interest rate decision. The bank is widely expected to remain on hold next Thursday, keeping rates at 4% and currently GBP OIS imply a probability of 07.5% for such a scenario to materialise while it also indicates that the bank is expected to remain on hold until the end of the year. Should the bank cut rates as expected and signal in tis forward guidance, that its comfortable with the current levels of interest rates, we may see the pound getting some slight support, while a possible inclination of the bank towards further easing of its monetary policy could weigh on the pound. At this point we should point out that also the vote count matters. In the last interest rate decision, five members of the Monetary Policy Committee (MPC) favoured the bank to cut rates, while other 4 favoured the bank to remain on hold. Should we see a substantial number of MPC members persisting for further easing of the bank’s monetary policy we may see the pound weakening, as the dovish tendencies within the BoE would still be present.

Analyst’s opinion (GBP)

“We expect the pound to be moved primarily by a mixture of macroeconomic indicators and BoE’s intentions. A possible tightening of the UK employment market and resilience of UK inflationary pressures could support the sterling. The same applies for the pound, should BoE signal a relative decisiveness to keep rates unchanged until the end of the year.”

JPY – BoJ to keep rates unchanged

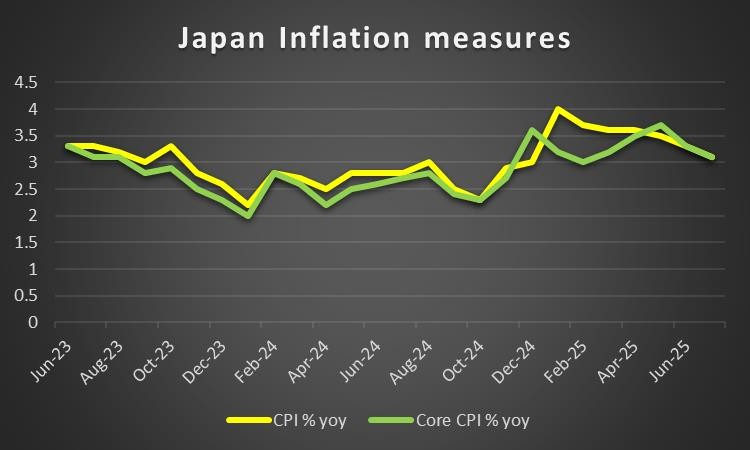

With Japan’s PM Ishiba resigning, elections within the ruling, yet without a majority in the upper and lower houses, LDP for a new President, are to largely decide Japan’s new PM. Most likely successors named in the local press, are agriculture minister Shinjiro Koizumi, chief cabinet secretary Yoshimasa Hayashi and MP Sanae Takaichi. Yet any leader is expected to make little difference in key issues Japan is currently facing such as inflation, fragile relationships with the US and international tensions with Russia, China and North Korea. In any case the political uncertainty tends to weigh on the JPY. Another issue that derives from the political uncertainty is the increasing burden it places on BoJ’s efforts to tighten its monetary policy. Especially Ms. Takaichi is an outspoken critic of BoJ’s plans to raise interest rates. On a monetary level, we highlight the release of BoJ’s interest rate decision next Friday. The bank is widely expected to remain on hold and its characteristic that JPY OIS imply a probability of 94.7% for such a scenario to materialise. Yet JPY OIS also imply that the market expects a rate hike by the bank just before the year ends, in its December meeting, thus a hawkish predisposition of the market regarding the bank’s intentions seems to be emerging. Should the bank’s forward guidance which may be included in BoJ Governor Ueda’s press conference, show that the bank maintains its intentions to hike rates at a later stage we may see JPY getting some support, while a possible easing of the bank’s hawkishness could weigh on the JPY. On a macroeconomic level, we highlight the release of Japan’s CPI rates for August and a possible acceleration of the rates could provide some support for JPY as it could support BoJ’s narrative for the necessity of a tightening of the bank’s monetary policy.

Analyst’s opinion (JPY)

“With all the political uncertainty in Japan being extended until early October, when a new LDP leader is to be elected, we note BoJ’s interest rate decision coming Friday as the key event for JPY. Given that the bank is to remain probably on hold, a possible hawkish forward guidance could provide some support for JPY.”

EUR – Fundamentals to lead the common currency

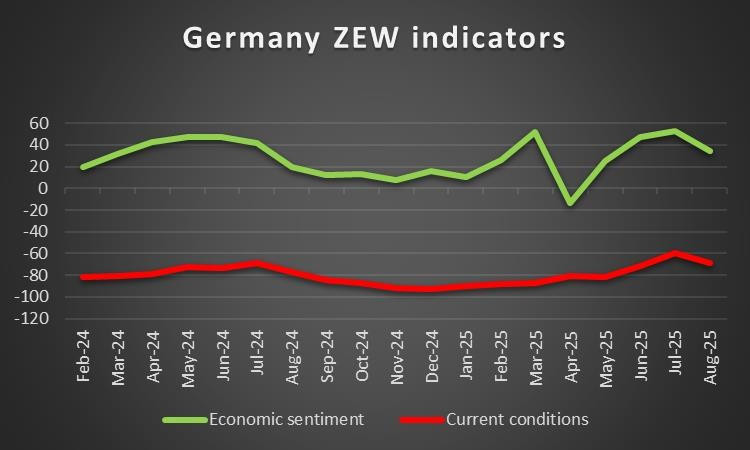

On a fundamental level there is a lot going on for EUR traders. First of all we note the resignation of France’s former PM Bayrou. The resigned PM was promptly replaced By French President Macron with a close associate Sebastien Lecornou. Yet the replacement failed to appease the public with protests sweeping across France inspired by the moto “Block everything”. The situation on a political level, seems to be reaching a dead end as on the one hand some fiscal discipline is required to address the country’s growing national debt and fiscal deficits, yet on the flip side, no one seems willing to take on the political cost for proposing and implementing such policies. On the eastern flank of the EU, we highlight the tensions with Russia, as Russian drones were downed by Poland. NATO fighters from Poland and the Netherlands seem to have taken part in the operation with assistance from Italian and German forces. It should be noted that Poland has triggered Article 4 of the military alliance. We see the case for the incident to cool off in the coming days, given the low key Russian reaction, yet should frictions with Russia intensify further, we may see the EUR losing some ground. On a monetary level, we note that ECB remained on hold in its interest rate decision on Thursday as was widely expected. In its accompanying statement, the bank stated that it sees headline inflation averaging 2.1% in 2025, 1.7% in 2026 and 1.9% in 2027 and that the economy is projected to grow by 1.2% in 2025, revised up from the 0.9% expected in June and the growth projection for 2026 is now slightly lower, at 1.0%, while the projection for 2027 is unchanged at 1.3%. Overall the bank seems to be quite comfortable with the current levels of interest rates, more or less verifying the markets’ expectations for the ECB to remain on hold until the end of the year. Something that ECB President Lagarde also mentioned, sounding somewhat upbeat, stating that trade uncertainty is diminished and also indirectly dismissing any worries for a rate cut. It’s characteristic that after the release and Lagarde’s press conference, EUR OIS imply that the market expects the bank to remain on hold until the end of 2026. As for financial releases we may see some interest around the release of the final HICP rates for August of France and Germany, as well as Euro Zone’s industrial output for July and Germany’s ZEW indicators for September.

Analyst’s opinion (EUR)

“In the big picture we expect market interest for the EUR to be driven mostly by fundamentals, given the low number of high impact financial releases from the area in next week’s calendar. Market uncertainty on a fundamental level, for France’s political outlook and could weigh somewhat on EUR as could any further tensions with Russia.”

AUD – Easy going week for Aussie traders

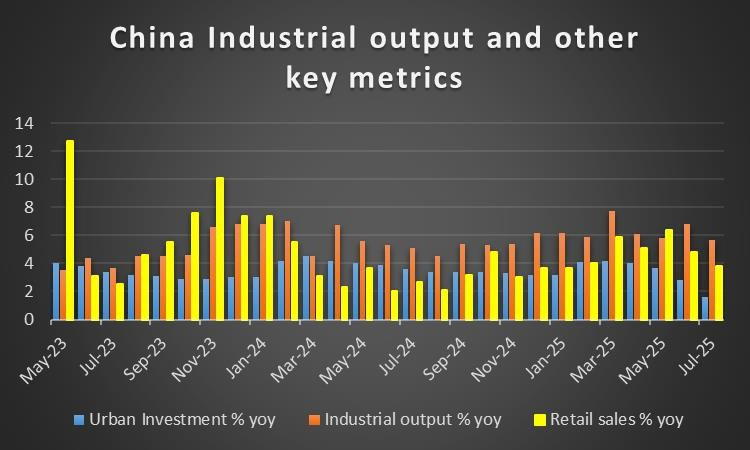

The Aussie is about to end the week clearly in the greens against the USD with AUD/USD reaching levels not seen since early November last year. Aussie traders are expected to have an easy going week with no major financial releases on the calendar, hence we expect fundamentals to lead AUD in the coming week. On a fundamental level, the Aussie could get some support from a possible improvement of the market sentiment given its status as a commodity currency and a riskier asset in the FX market. Also developments in China should not be neglected, given the close Sino-Australian ties. On Monday we highlight the release of China’s industrial output, retail sales and urban investment growth rates and a possible acceleration of the rates could also provide some support for the Aussie as it could imply more exports of Australian raw materials to China. On a monetary level, market expectations currently, are for the RBA to remain on hold in its next meeting at the end of September and to proceed with a rate cut in tis next meeting, yet nothing seems to be on next week’s calendar that could alter the expectations and a rate cut is still some way off. Any way should we see the market’s expectations for a rate cut by RBA, intensifying we may see AUD losing some ground.

Analyst’s opinion (AUD)

“Given the lack of high impact financial releases from Australia in the coming week, we expect fundamentals to lead the Aussie. A possible improvement of the market sentiment could provide some support for AUD and vice versa.”

CAD – BoC expected to cut rates

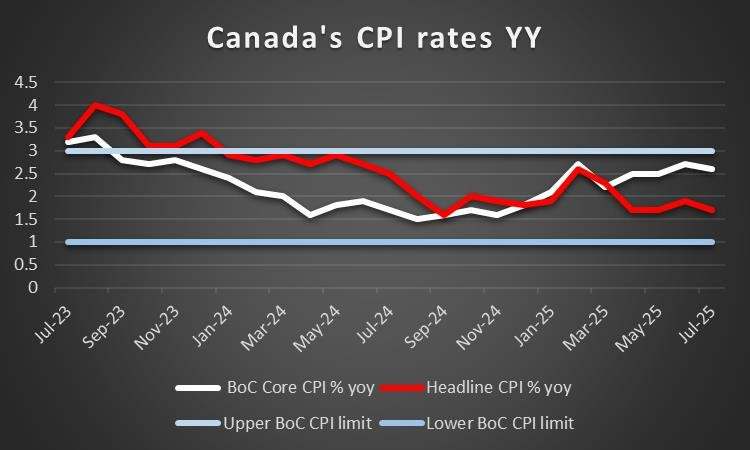

The Loonie is expected to end the week relatively unchanged against the USD. On a macro economic level, we note that the Canadian employment data for August were disappointing given that the unemployment rate surpassed market expectations by reaching 7.1% and the employment change figure unexpectedly dropped deep into the negatives reaching -65.5k. The release tended to intensify market expectations for the BoC to cut rates in its meeting on Wednesday. In the coming week we highlight the release of Canada’s CPI rates for August on Tuesday as market focus on the release may intensify about Canada’s inflationary pressures, given that the next day we get BoC’s interest rate decision. Should we see the rates escalating we may see the Loonie getting some support as market expectations for the bank to cut rates may ease. On a monetary policy level, we highlight the release of BoC’s interest rate decision next Wednesday. The bank is expected to cut rates by 25 basis points and currently CAD OIS imply a probability of 82.2% for such a scenario to materialise. Please note that CAD OIS also currently imply that the market expects the bank to deliver another rate cut in its December meeting, hence relative dovishness could be detected in the market’s expectations. Should the bank cut rates as expected and signal that it ends its easing cycle here or sound pessimistic for any further easing, we may see the Loonie gaining some ground as the market may push its rate cutting expectations further down the line. On the flip side should the bank signal that its open to cut rates further, indirectly confirming the market expectations, we may see the Loonie losing ground. On a fundamental level, we note that a positive market sentiment could provide some support for the Loonie as it is considered a commodity currency. On the other hand a possible restart of oil prices dropping, could weigh on the CAD given Canada’s status as a major oil producer.

Analyst’s opinion (CAD)

“BoC’s interest rate decision could shake the Loonie next week and should the bank cut rates as expected and issue a dovish forward guidance could weigh on the CAD. Yet before that the release of Canada’s CPI rates for August could also add more volatility to CAD pairs.”

General Comment

In the coming week we expect the USD to gain more initiative in the FX market becoming even more influential, given that the gravity and frequency of high impact financial releases intensifies and the Fed’s interest rate decision on Wednesday. Yet at certain moments in the week, high impact events are scheduled for other currencies as well which could allow for a more balanced trading mix to emerge for FX traders. As for US stock markets we note the continuation of the good days for a second week in row. Major US equities markets indexes, such as Dow Jones, S&P 500 and Nasdaq were all in the greens. Oracle may have been the main gainer for the week as its share price rallied some 43% at its peak, as the forward guidance included in its earnings report was very optimist about the company’s revenue prospects. On the flip side, Apple’s share price seems to be suffering a hit from latest Apple event and the products presented. As for gold we note that after hitting an All-Time-High at $3675 per ounce, seems to be stabilising somewhat. The bullish outlook for the precious metal seems to be tested yet the market sentiment for the time being seems to remain bullish. The prospect of the Fed cutting rates and turning dovish seems to continue feeding gold bulls however that may prove to be a shaky basis for gold traders.

Si tiene usted alguna pregunta o comentario sobre este artículo, escriba un correo directamente a nuestro equipo de investigación research_team@ironfx.com

Descargo de responsabilidad:

Esta información no debe considerarse asesoramiento o recomendación sobre inversiones, sino una comunicación de marketing. IronFX no se hace responsable de datos o información de terceros en esta comunicación, ya sea por referencia o enlace.