The week is about to reach its end and we take a pip look at what is next week’s calendar. On the monetary front we note on Thursday the interest rate decisions of Sweden’s Riksbank, Turkey’s CBT and the Czech Republic’s CNB. Also we note the release of BoJ’s summary of opinions of its June policy meeting on Monday’s Asian session. As for financial releases, on Monday we get Germany’s Ifo indicators and UK’s CBI trends for industrial orders, both being for June. On Tuesday we get Canada’s CPI rates for May and on Wednesday, we note the release of Australia’s CPI rates for May, Germany’s GfK consumer sentiment for July and UK’s CBI distributive trades indicator for June. On Thursday we get Eurozone’s June economic sentiment and from the US the weekly initial jobless claims figure, the durable goods rate for May and we highlight the final GDP rates for Q1. On Friday, we get Japan’s Tokyo CPI rates for June, France’s preliminary CPI rates for June, UK’s final GDP rate for Q1, Switzerland’s KOF indicators for June, the Czech Republic’s revised GDP rate for Q1, Canada’s GDP rates for April and from the US we get the final UoM for June and the core PCE price index for May.

USD – US Core PCE rates eyed

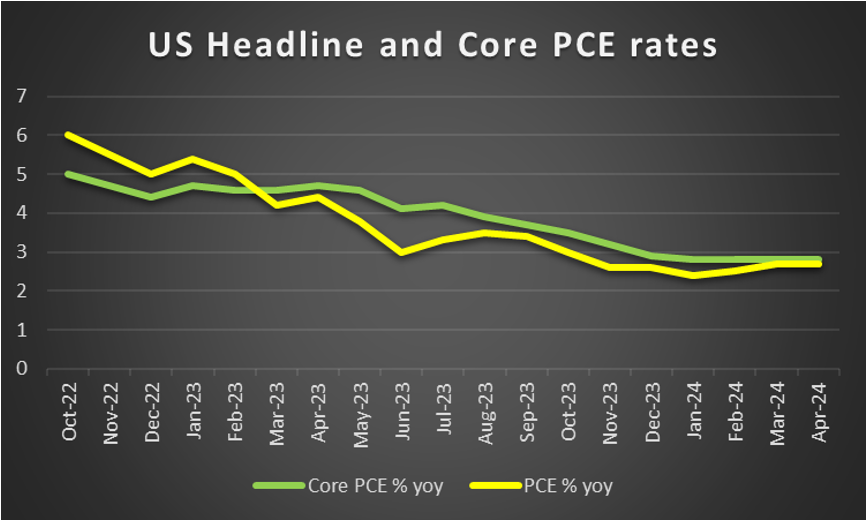

The USD seems to remain near the same levels the week begun against its counterparts. On a fundamental level, we note that the greenback could enjoy some safe haven inflows in the coming week should tensions in geopolitical issues such as the Isreali-Palestine conflict and the tensions in the US-Sino relationships, escalate further. It should be noted that a series of visits of Russian President Putin in the Far East, tended to highlight the forming of coalitions and the polarisation in the international political scene adding to the uncertainty of the markets. On a monetary policy level, we note that Fed policymakers seem to be advising patience regarding any rate cuts. It’s characteristic that Philadelphia Fed President Harker highlighted that he would be satisfied with only one rate cut this year, while others mentioned that more data about inflation are required before the bank starts cutting rates. Should we see Fed policymakers contradicting market expectations for two rate cuts by the end of the year, by highlighting the scenario of one rate cut only, we may see the market mood turning more cautious which in turn could support the USD. As for financial releases, we expect a rather easy going week ahead, yet we would like to highlight two financial releases. The first would be the final GDP rate for Q1, and any slow down if compared to prior releases could weaken the USD and the second would be the relase of the Core PCE rates for May as a final inflation test for May. Should the Core and headline PCE rates slow down we may see the USD weakening as it would imply an easing of inflationary pressures in the US economy and could enhance market expectations for the Fed to proceed with two rate cuts in the year.

GBP – Final GDP rates in sight

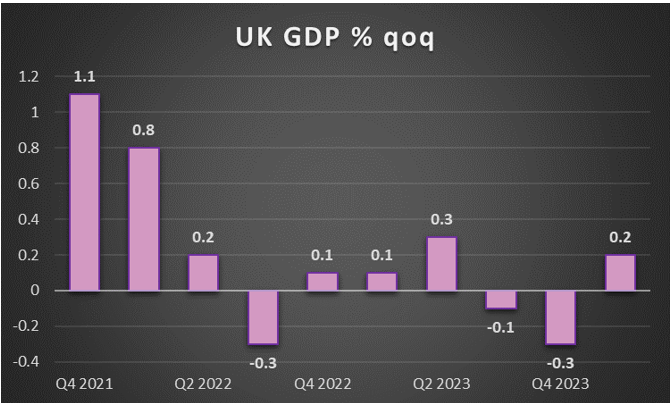

GBP seems about to slip lower against the USD and the EUR, while is gaining against the JPY. On a fundamental level, the pre-election preriod is heating up in the UK as the election date is in two weeks. It should be noted that the Labour party despite a slight drop, continues to lead the polls with a 20% margin against the Conservatives. Given that a change in the UK Government is on the horizon, uncertainty seems to be on the rise for the UK. On a fiscal level, the Labour Party, seems set to levy taxes and tighten the regulatory framework in various fields. Also they seem to plan to intensify competition in the UK economy, invest in green energy, enhance worker rights and invest in housing. Overall and for the time being, we see the case for a change in Government weighing on the pound as uncertainty rises on a political level for the UK. On a monetary level, we highlight the release of BoE’s interest rate decision yesterday. The bank remained on hold as expected, yet the interesting part of the decision was its forward guidance. The bank seems to be inclined in proceeding with rate cuts, albeit not immediately. The release tended to verify the market’s expectations for a rate cut in the September meeting and allowed it to maintain its hopes for more another rate cut until the end of the year. Overall, should this be reflected also in commentary to be made by BoE policymakers in the coming week we may see BoE’s monetary policy outlook weighing on the pound. On a macroeconomic level, we note that inflationary pressures eased in the past month with the headline rate reaching the bank’s 2% target yoy. In the coming week we highlight the release of UK’s final GDP rates for Q1, and a possible slowdown if compared to the preliminary release could weigh on the pound as it would imply that the UK economy performed worse than initially calculated.

JPY – Tokyo’s CPI rates to be released

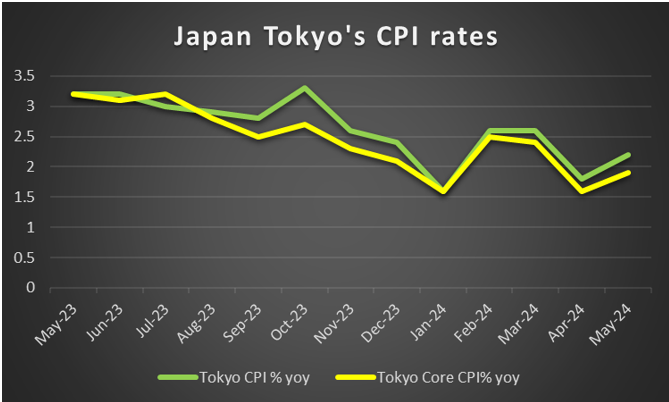

JPY seems about to end the week in the reds across the board, in a signal of a wider weakness. We make a start for JPY by noting that on a fundamental basis, the Yen could gain safe haven inflows should tensions in geopolitical issues be enhanced. For the time being though the main factor behind JPY’s direction is considered to be BoJ’s loose monetary policy. Yet BoJ officials tend to maintain a more hawkish tone than what the market seems to expect. In the past few days, BoJ Governor Ueda stated that the bank could hike interest rates in July, should the macroeconomic picture of Japan allow it. We must note that BoJ Governor seemed determined for the bank ot raise borrowing costs from its current low, near zero levels. Hence we expect the release of the summary of opinions of the July meeting during Monday’s Asian session, to shed more light onto BoJ policymakers’ intentions. We should also note that the market seems to be pricing in the scenario of the bank hiking not once but twice within the year, raising rates to 0.3%. Yet JPY continues to weaken, implying that the market may be listening to BoJ Governor Ueda’s comments, yet is still not convinced for BoJ’s intentions, at least not yet. Given JPY’s weakening we note the risk of Japan actually intervening in the markets to support its currency. It should be noted that JPY’s weakening is leading it to levels at which the last market intervention of Japan to support the Yen was performed. Hence as JPY continues to slip, the chances of market intervention are increasing. On a macroeconomic level, we note the release of Japan’s CPI rates for May during today’s Asian session and in the coming week, we note the release of Tokyo’s CPI rates for June and should rates cool off some more, we may see JPY weakening as it could make the path of BoJ to another rate hike even harder.

EUR – The hard case to buy the EUR

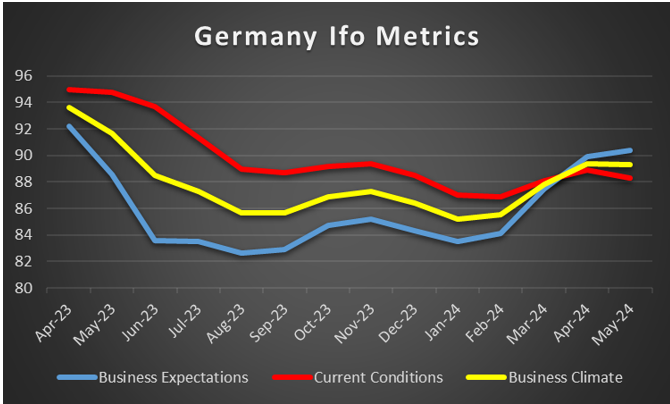

The EUR is about to end the week slightly lower against the USD, yet seems to be gaining ground against the GBP and JPY. On a fundamental level, we note that the result of the EU Parliament elections seems to be intensifying centrifuge forces within the EU. It’s characteristic that French President Macron has called for legislative elections which France’s populist far right seems set to win. Interestingly the second place, according to polls does not go to Macron’s party but the left coalition, which also tends to be euro-skeptic. Overall we tend to see the case for the results of the EU Parliament elections could delay any moves towards further unification. The uncertainty characterising the overall European political outlook seems to be weighing on the single currency. Besides the uncertainty of the EU political outlook, on a fundamental level we also highlight the escalating trading war between the EU and China. It should be noted that the EU has announced that it will be imposing tariffs on Chinese EVs. We still do not know the Chinese response, which is coming, and the impact of its response could vary. Should the Chinese actually impose a harsher response, we may see the common currency slipping. On a monetary policy level, we note the market’s expectations for ECB to continue cutting rates in the September and the December meetings. It should be noted that the market’s expectations remained unwavering despite ECB President Lagarde warning that ECB’s interest rates may not continue dropping in a linear way but that the bank could at times pause its rate cutting path by more than one meeting before cutting them again. Overall though the path for ECB’s rates is downwards and that may be enhancing the bearish sentiment somewhat. On a macroeconomic level we note the release of the preliminary PMI figures of France, Germany and the Zone as a whole and in the coming week we note the release of Germany’s Ifo indicators for June as well as the preliminary HICP rate for June of France.

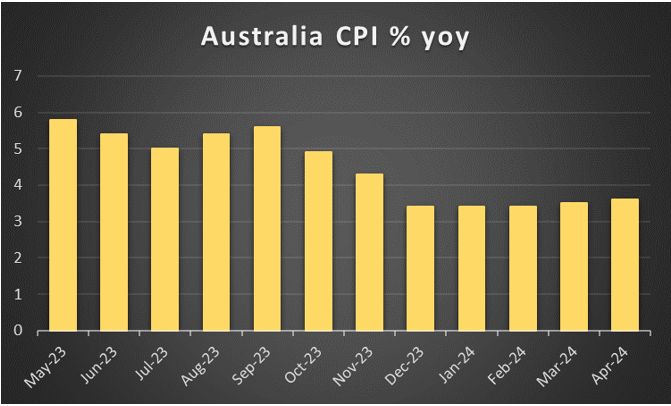

AUD – May’s CPI rates to shake the Aussie

AUD is about to end the week in the greens against the USD. On a fundamental level, It should be noted that AUD as a commodity currency is particulary sensitive to the market’s mood. Should we see the market turning more cautious, AUD may lose ground and vice versa. Also on a fundamental level, we note that the Aussie could suffer some losses should tensions in the US-Sino relationships escalate further, given that China is the main trading partner of Australia. Furthermore, the fact that China’s industrial output growth rate for May decelerated was not a positive signal for Australian exports of raw materials. On a monetary level, we note that RBA during Tuesday’s Asian session, remained on hold, as was widely expected by market participants. The bank in its accompanying statement stressed that “the process of returning inflation to target is unlikely to be smooth”. Furthermore, RBA policymakers stated that “the persistence of services price inflation is a key uncertainty”, which may have been perceived as a willingness by the bank to maintain the current interest rate levels for a prolonged period of time. Therefore, the comments may have had a hawkish tone and the bank’s confident stance could keep the Aussie supported. In the coming week, we highlight the release of Australia’s CPI rates for May on Wednesdays’ Asian session. Should the release show that inflationary pressures remained sticky in the Australian economy in the past month, we may see AUD getting some support as it may harden the stance of RBA further.

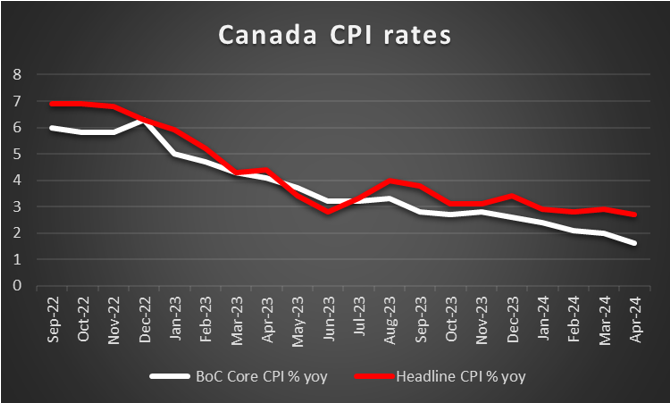

CAD – Loonie traders focus on the release of May’s CPI rates

The CAD is about to end the week stronger against the USD. On a fundamental level, we note that the Loonie as a commodity currency is considered to be of riskier nature and thus more sensitive to the market sentiment. Should the market sentiment turn more risk oriented we may see the CAD getting some support and vice versa. The CAD is especially sensitive to the path of oil prices, given that Canada is a major oil producing economy. It should be noted that oil prices currently seem to be caught between conflicting fundamentals, including worries for China’s oil demand outlook, OPEC’s production levels and the tensions in the Middle East. For the time being we note that oil prices have risen in the past few days and should they gain further ground we may see the CAD gaining as well, given the market’s perception for a positive correlation of the CAD with oil prices. On a monetary policy level, the release of BoC’s account of the deliberations of the last monetary policy decision, showed that BoC policymakers hesitated to cut rates and considered delaying the rate cut until July. Yet the bank proceeded with a rate cut in its last meeting and the prementioned hesitations may delay the expected by the market, rate cut in the bank’s next meeting. Should BoC policymakers in the coming week imply a delay in cutting rates, we may see the Loonie getting some support as the market will have to reposition itself as its expectations for a July rate cut will be contradicted. On a macro economic level, we highlight the release of Canada’s CPI rates for May and a possible deceleration of the rates could weaken the CAD as the pressure on BoC to continue cutting rates may intensify.

General Comment

As a closing comment, we expect volatility in the coming week to ease somewhat and the USD to relent some of the initiative and ease its dominance in the FX market, as the gravity and frequency of US financial data tends to ease. Such a scenario could allow various currencies to come under the spotlight and draw their own course, providing a more balanced trading mix for traders. As for US stockmarkets, we note that the rally caused by the AI frenzy is ongoing. It’s characteristic that NVIDIA is now the most valuable company worldwide. Yet a closer inspection of the US stockmarket indexes seems to show an inconsistency as on the one hand S&P 500 and Nasdaq are creating constantly new record highs, while on the other hand Dow Jones maintains a sideways motion. We tend to highlight the risk that the market may have gotten ahead of itself and fundamentals may not be able to sustain the rally, especially given that the Fed is hesitant to start cutting rates. As for gold, we note that the negative correlation of gold prices to the USD seems to have been interrupted, or at least has been hidden behind low volatility. It should be noted that a possible rise of US yields could make US bonds as an attractive alternative to gold for investors thus set gold’s price under pressure.

Si tiene preguntas generales o comentarios relacionados con este artículo, envíe un correo electrónico directamente a nuestro equipo de investigación a research_team@ironfx.com

Descargo de responsabilidad:

Esta información no debe considerarse asesoramiento o recomendación sobre inversiones, sino una comunicación de marketing. IronFX no se hace responsable de datos o información de terceros en esta comunicación, ya sea por referencia o enlace.