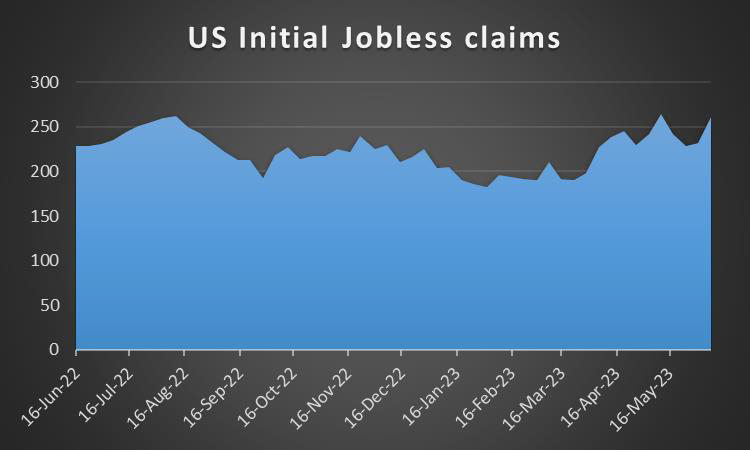

An interesting week is about to come to a close as we have a look at what next week has in store for the markets. On the monetary front, we highlight on Thursday the release of BoE’s interest rate decision, while also note from Switzerland SNB’s, from Turkey CBT’s and from Norway, Norgesbank’s interest rate decisions the same day and on Wednesday the Czech Republic’s CNB interest rate decision. Furthermore, Fed Chairman Jerome Powell will be testifying before Congress on Thursday and may draw the market’s attention, while on Tuesday RBA is to release the minutes of the June meeting. As for financial releases, we note on Monday Canada’s producer prices for May, we skip a rather light Tuesday and note on Wednesday the release of the UK’s CPI rates for May and the CBI trends for industrial orders for June, while from Canada we get April’s retail sales. On Thursday we get New Zealand’s GDP rate for May, the US weekly initial jobless claims figure and Eurozone’s preliminary consumer confidence for June. On Friday we highlight the release of the preliminary June PMI figures of Australia, Japan, France, Germany, the Eurozone as a whole, the UK and the US, while we also note the release of Japan’s CPI rates for May.

USD – The Fed remains on hold, yet…

The USD seems about to end the week in the reds for a third time in a row against its counterparts. We should note that USD’s weakening occurred despite getting some support from the Fed’s interest rate decision. The bank remained on hold as expected at the 5.00%-5.25% range, yet signaled with its new dot plot its intentions to proceed with another two rate hikes until the end of the year. Please note that the bank in its forward guidance, included in the accompanying statement, that it will continue to monitor the implications of incoming information for the economic outlook. Yet Fed Chairman Powell’s comment in his press conference, that no rate cuts are in sight for the current year, forced the market to readjust expectations for such a scenario near the end of 2023. Furthermore, the Fed’s economic projections seem to be a bit more optimistic as they foreshadow that the US economy will be able to avoid a recession in the current and following year, as the GDP projection for 2023 was uplifted. Overall, the Fed’s hawkishness seems to collect some support for the greenback and we expect Fed Chairman Powell to provide additional insights in regards to the bank’s intentions in his testimony before the US Congress next week. On a macroeconomic level, the Fed’s interest rate decision is understandable as inflationary pressures eased further in May both on a consumer level as well as on a producer level. Yet despite the Fed’s view of the US economic outlook our worries

tend to be maintained, as the data on both the production and the demand side of the US economy seem to suggest a possible slowdown of economic activity.

GBP – BoE to hike rates

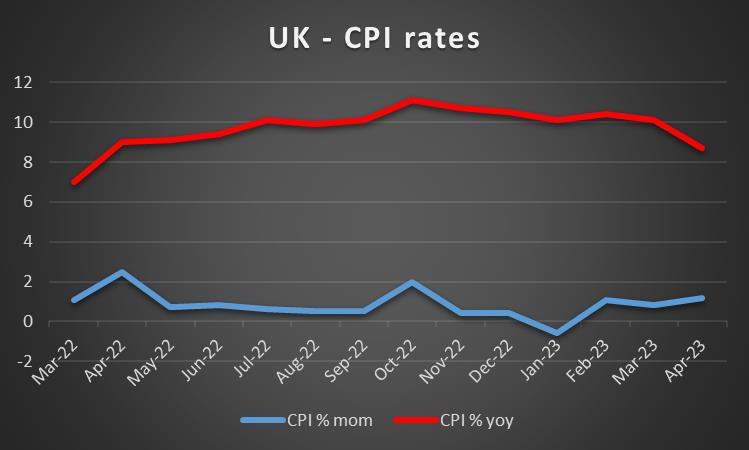

The pound is about to end the week in the greens against the USD and JPY yet is losing ground against the EUR. In the coming week, we expect the highlight for pound traders to be BoE’s interest rate decision on Thursday. The bank is expected to hike rates by 25 basis points and currently, GBP OIS imply a probability of 83.40% for such a scenario to materialise, with the rest implying that a 50 basis points rate hike is also possible yet a remote scenario. Furthermore, please note the market’s expectations for more rate hikes to come from BoE before the year’s end. The hawkish intentions of the bank are understandable in the sense that despite the bank’s Monetary policy tightening, inflation has not eased as much as in other economies such as the US and the Eurozone. Even in May when a sharp drop in inflation was expected, the slowdown was material yet less than the market’s expectations on a year-on-year level and still above 8%, which is four times the bank’s inflation target rate. We expect the bank to deliver the 25 basis points rate hike and maintain a hawkish approach, despite some Monetary Policy Committee members disagreeing, anything less than that could asymmetrically weaken the pound. On a macroeconomic level, we note that June’s CPI rates are to be released ahead of BoE’s interest rate decision and could alter the market’s expectations about BoE’s rate hiking path, especially if the rates slow down considerably. Furthermore, we highlight the tightness of the UK employment market for April, as the unemployment rate dropped and the employment change figure rose unexpectedly, allowing for more leeway for the bank to tighten its monetary policy. April’s GDP rate accelerated implying a faster expansion of the UK economy, adding to the positive sentiment of pound traders.

JPY – BoJ remains on hold

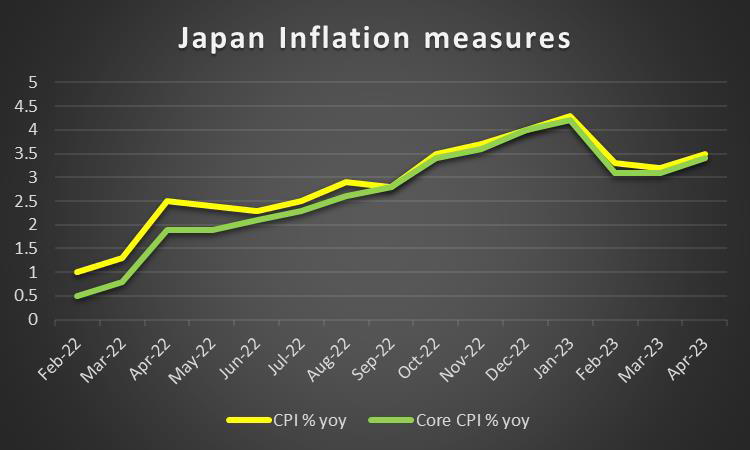

JPY is about to end the week weaker against the USD, EUR and GBP in a sign of a broader weakness of the Japanese currency. We should note on a monetary level, that BoJ remained on hold at -0.10% as was widely expected, keeping its ultra-loose monetary policy settings in place. Overall, the monetary policy outlook differentials that BoJ has with other central banks tend to widen and thus weigh on JPY and we expect that tendency to be maintained as long as the bank keeps its dovish stance and others tighten their policy. Given the bank’s efforts to maintain inflation near the 2% target, we highlight on a macroeconomic level the release of the June CPI rates near the end of next week. For the time being, we note that prices at a producer’s level declined more than expected into the negatives for May in a prelude for what to expect from the nationwide CPI rates for the same month. Another issue that tends to intensify our worries is the widening of April’s trade deficit in May, implying that the Japanese economy suffered even more outflows from its international trading activities. On the flip side, we note the acceleration of the machinery orders growth rate which got out of the negatives for April, implying a greater degree of confidence of businesses to actually invest in the Japanese economy. On a fiscal level, we note the unveiling of the Japanese government’s new childcare plan, an issue we had mentioned in last week’s report as well, yet on the flip side, we also note the possibility of a tax hike. The latter issue may be pushed back as there are wide rumors for possible elections which may endanger the political stability achieved under Kishida. Furthermore, we note for JPY traders the statements made by Japan’s Finance Minister Suzuki, that excessive volatility is undesirable, allowing for a hint that the Japanese government may intervene in the markets once again, should JPY weaken considerably.

EUR – ECB hiked rates and pressed on

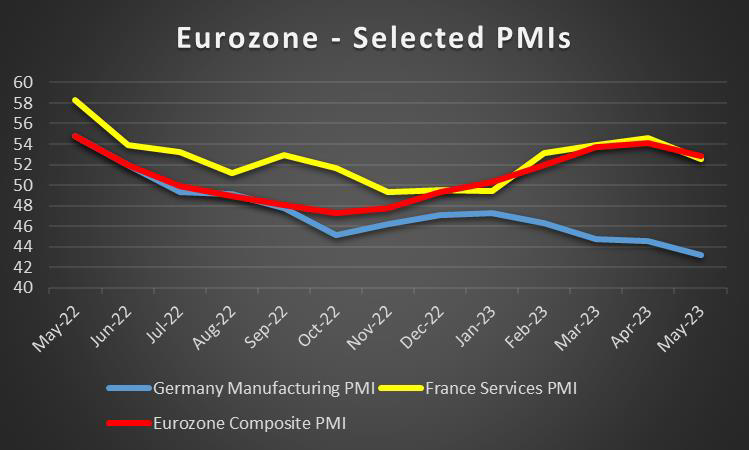

The EUR is about to end the week stronger against the USD, JPY and GBP in a sign of a broader strength for the common currency. On a monetary level, ECB’s interest rate decision tended to provide additional support for the EUR, as the bank hiked rates as expected by 25 basis points and also signaled that more rate hikes lay ahead. It’s characteristic that ECB President Christine Lagarde in her press conference that followed the release of the decision, reaffirmed that the bank is not at the end of its rate hiking cycle with another 25 basis points rate hike in the July meeting being probable. This was also the market’s expectation and EUR traders seem not to have been disappointed. On a macroeconomic level, we note that Germany’s and France’s HICP slowdown shown in the preliminary release for May was confirmed. On the other hand, we also got some mixed signals from Germany’s ZEW indicators for June as pessimism for the outlook of the largest economy in the Eurozone has been reduced while the conditions on the ground deteriorated substantially. It should be noted that the German economy is in a technical recession and may have been the one economy hit the most by European sanctions related to Russian natural gas. Furthermore, our worries extend to a Eurozone level, despite the acceleration of the industrial output growth rate for April, also given the further tightening of ECB’s monetary policy. Yet given ECB’s hawkish stance, our worries tend to extend to a possible slowdown of economic activity, especially for Germany’s manufacturing sector and we expect the release of the preliminary June PMI figures to shed more light on the issue.

AUD – Positive data and worries for China

AUD is about to end the week in the greens against the USD for a third week in a row. On the monetary front, we note that the heat on a political level for RBA Governor Lowe is on, given the recent rate hikes of the bank. Borrowers seem to be in a dire situation as their loan installments continue to rise. Yet the bank’s hawkish intentions may not be over just yet, as market expectations are for the bank to hike rates once again in the August meeting before pausing its rate-hiking path again. The recent data release, showing a hot Australian employment market for May, could have sharpened RBA’s hawkishness once again. It’s characteristic that the unemployment rate dropped to 3.6% while the employment change figure rose to almost 76k, both exceeding market expectations. Furthermore, it should be noted that June’s consumer confidence seems to have improved which in turn may allow for an acceleration of the retail sales growth rate. On the other hand, Business confidence seems to have dropped and conditions on the ground for the Australian economy seem to have deteriorated in May. Yet at this point and given the close Sino-Australian economic ties, we note our worries for the rebound of the Chinese economy. Evidently May’s industrial output growth rate slowed down beyond market expectations as also did the urban investment and the retail sales growth rates for the same month. The Chinese data tend to highlight an easing in economic activity both on the production as well as on the demand side of China’s economy, which in turn could weigh on the Aussie. Overall, given the low number of high-impact financial releases from Australia in the coming week we may see fundamentals leading the way for the Aussie.

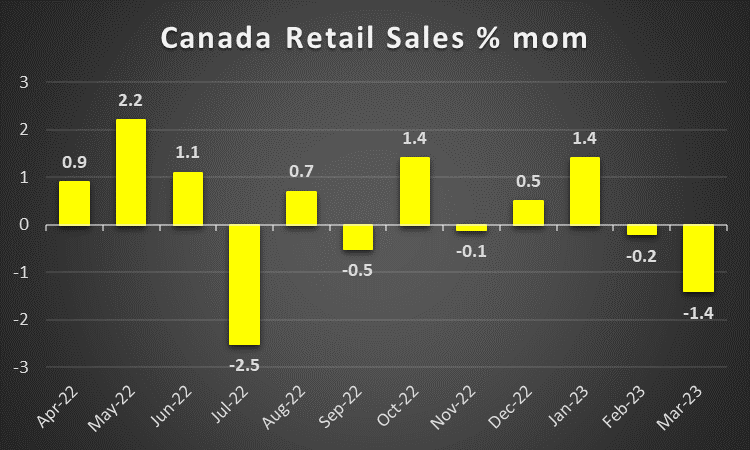

CAD – Canada’s retail sales in focus

The Loonie seems to be edging higher against the USD, as the week draws to a close. On the monetary front, market expectations are for the BoC to hike rates once again in its mid-July meeting, a scenario that may be providing some support to the Loonie, especially should market expectations be enhanced by opinions expressed by BoC policymakers next week. Yet on the other hand, we have to note that the worse-than-expected employment data for May, may have shaken some Loonie traders as the employment change figure dropped into the negatives and the unemployment rate rose to 5.2%, both implying a crack in the tightness of the Canadian employment market. Furthermore, the wide drop of the number of House Starts can be perceived as another symptom of BoC’s monetary policy tightening, while the softening of the manufacturing sale growth rate may be perceived as another bad omen for the Canadian economy in April. On a more fundamental level, we note the sensitivity of the CAD as a commodity currency, given its riskier nature to the market’s mood swings. Should the market sentiment turn more risk-averse we may see the CAD losing ground and vice versa. Finally, oil prices failed to provide any substantial bearing on the course of the Loonie given that they remained relatively stable, maybe even edged a bit lower for the week. Fundamentals surrounding the oil market seem to revolve around the possibility of China slowing down its growth and having an adverse effect on the demand side of the commodity and on the other hand the announced production cuts by Saudi Arabia countering the market worries. Overall, we expect that should oil prices start declining in the coming week, we may see them having an adverse effect on the Loonie as well, given that Canada is a major oil-producing economy.

General Comment

The coming week is to bring an end to the chorus of central banks’ interest rate decisions. We expect the USD to relent some of the initiative over other currencies as the frequency and gravity of US financial releases tends to ease and for the time being no major fundamental issues are in play from the US. Such a scenario, may allow other currencies to take the opportunity and navigate through the markets in a more independent fashion, creating a more balanced blend of trading opportunities. As a closure, we would like to make a small comment about some interest rate decisions due out. We make a start with Norway’s Norgesbank on Thursday and we expect the bank to hike rates by 25 basis points. Should such a decision be also accompanied by a forward guidance signaling another rate hike to come, we may see the NOK getting some support. On the same day, expectations are running high for Switzerland’s SNB as it is expected by the market to deliver a 50 basis points rate hike, a scenario that could provide some support for the CHF. We note that the CPI rate slowed down to 2.2% yoy for May nearing the bank’s target inflation rate of <2.0%, which may ease the hawkishness of the bank. Last but not least, we would also like to note from Turkey CBT’s interest rate decision on the same day and the bank is expected to remain on hold at 8.5%. It should be noted that the Lira managed to stabilise somewhat against the USD as the market maintains a wait-and-see position for the new Governor of the Bank, Hafize Gaye Erkan. She is considered to be a guarantee of the Turkish Government’s commitment to the markets, for a more economically orthodox approach in regards to the bank’s monetary policy approach, something that the markets do not seem to buy currently but a strong rate hike could alter that perception.

اگر در مورد این مقاله سوال یا نظر ی کلی دارید، لطفاً ایمیل خود را مستقیماً به تیم تحقیقاتی ما بفرستیدresearch_team@ironfx.com

سلب مسئولیت:

این اطلاعات به عنوان مشاوره سرمایه گذاری یا توصیه سرمایه گذاری در نظر گرفته نمی شود ، بلکه در عوض یک ارتباط بازاریابی است. IronFX هیچ گونه مسئولیتی در قبال داده ها یا اطلاعاتی که توسط اشخاص ثالث در این ارتباطات ارجاع و یا پیوند داده شده اند ندارد.