With the week nearing its end, we note that the US Preliminary PMIs have yet to be released. On a monetary level, we note from the Czech Republic, CNB’s interest rate decision on Wednesday. In regard to financial releases, we make a start on Monday with Germany’s IFO business climate figure, followed by the UK’s CBI distributive trades for September. On Tuesday, we note the US Consumer Confidence figure for the same month. On Wednesday, we note Germany’s Gfk Consumer sentiment figure for October and the US durable goods rate for August. On Thursday, we highlight Australia’s retail sales rate for August, the Eurozone’s economic sentiment figure for September, Canada’s business barometer figure for September, followed by Germany’s Preliminary HICP rate for September, the US Final GDP rate for Q2 and finishing off the day is the US Initial Jobless claims figure. Finally, on a packed Friday, we make a start with Japan’s Tokyo CPI rate for September, the UK’s GDP rate for Q2, France’s Preliminary HICP rate for September, Switzerland’s KOF Indicator for September, the Eurozone’s Preliminary HICP rate for September, the US Consumption rate for August, the US headline and Core PCE rates for August, Canada’s GDP rate for July and finally the final US University of Michigan sentiment for September.

USD – FED remains on pause yet hints at another rate hike in the future

The USD is about to end the week stronger against the EUR, the pound and the JPY. On a fundamental level, we highlight that the escalations within the Republican party appear to be reaching a boiling point, as some Republicans are for a bill that would cause another government shutdown. Please note that we near the cut-off date, the 30th of September, therefore should no deal be reached in time, we may see the dollar gaining some safe-haven inflows as we near the end of next week. On a monetary level, we highlight that the Fed remained on hold during the monetary policy meeting on Wednesday, as was widely expected by market participants. Interestingly, Fed Chair Powell in the post-meeting conference, stated “We want to see convincing evidence really that we have reached the appropriate level, and we’re seeing progress and we welcome that. But, you know, we need to see more progress before we’ll be willing to reach that conclusion”, implying that the Fed may still have another rate hike in the bag, thus may provide support for the greenback over the long term.

On a macroeconomic level, we highlight the US PMI figures are expected to come in higher than their previous recorded figure and should that be the case, we may see further support for the greenback, as it may provide the Fed with the justification and support to continue in their rate hiking cycle, as it may be indicative of a resilient economy despite the high-interest rate levels. However, the potential risk of the US Government shutdown, could have a macroeconomic effect, as it would result in government programs and social security payments potentially being paused, in addition to the risk of the government defaulting on its debt, could have negative consequences and may send the US economy into a recession.

Lastly, as the week nears its end, we note for next week the US consumer confidence figure for September, the Final GDP rate for Q2, the weekly initial jobless claims figure, the consumption rate for August, the University of Michigan Final sentiment figure and the Fed’s favourite tool for measuring inflation, which is the Core PCE rates for August. In conclusion, we note the greenback’s strengthening at the end of the week, yet traders may await next week’s Core PCE rates, as a potential signal to inflationary pressures in the US economy. In our opinion, for the bank to remain on hold we anticipate the rate to come in as expected or slightly lower.

GBP – The BOE remains on hold

The pound seems about to end the week lower against the USD, EUR and JPY in a sign of broader weakness for the pound. On a fundamental level, we note multiple news agencies are reporting that a UK firm sold thousands of unverified jet engine parts, which in itself may have no effect on the pound, yet in our opinion, it further diminishes the UK’s credibility on a global stage and as such, we may see the financial world further shunning the UK. On a monetary level, we highlight that BoE, remained on hold at 5.25%, a possibility that was priced in at the start of the week at a rate of 20% and suddenly became 50% after a surprise slowdown of the UK’s CPI rates in August. Interestingly, the members who voted for a pause were 5, compared to the 4 who opted for a rate hike.

The lack of unanimity could be a precursor to internal conflicts within the BOE, as it appears that they are no longer unified in their decision-making process and as such, we may see heightened volatility in the pound, which may weigh on the pound in the long run. Yet, we beg the question, with inflation still at 6.7%, does the bank believe that the current interest rate is sufficient to combat inflation, considering that average hourly earnings have been increasing and unemployment is still at record low levels? In our opinion, the bank may have to continue hiking in the future and the longer it takes to combat inflationary pressures, the greater the risk of inflationary pressures becoming engrained in the UK economy.

Yet the slowdown presented in August’s CPI rates may be indicative that the current level of interest rates may be having an impact on easing inflation. In conclusion, our hypothesis that the bank may have to increase interest rates in the future is based on the still above BoE’s target inflation levels in the UK economy and that a single month of easing inflationary pressures does not signal that the battle is over. Yet, we acknowledge that the UK economy is in a peculiar state, with firms shunning from London such as Arm LTD, but also the EU carbon border adjustment mechanism, which enters a transitional phase on the 1st of October 2023, in which the UK exporters who are exporting to the EU will pay a carbon emission tax and provide the EU with the necessary data, further increasing costs for UK producers.

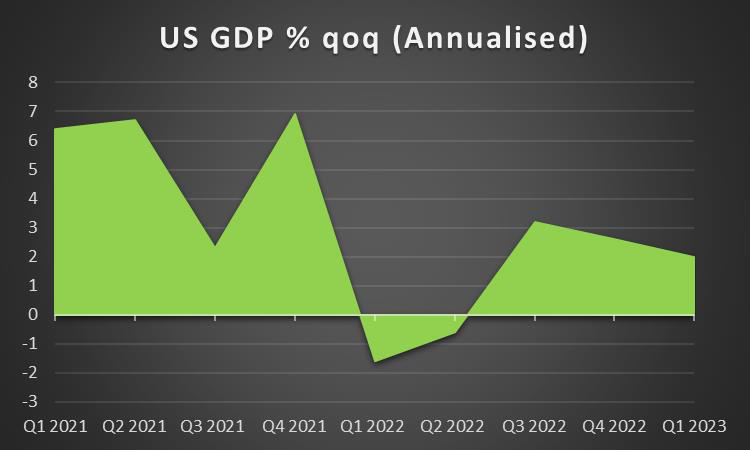

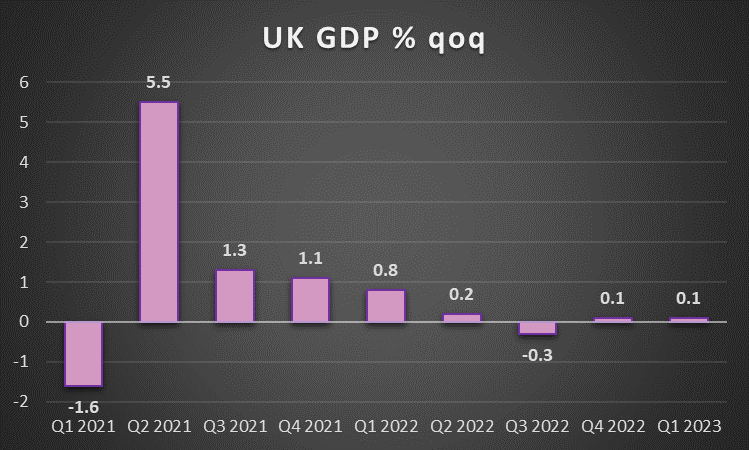

In conclusion, traders may be looking at the UK’s GDP rate for Q2 which is due to be released next week, in order to gain a better view of the UK’s economy.

JPY – BOJ remains on hold as expected

JPY is about to end the week relatively weaker against the dollar, yet relatively unchanged against the EUR and stronger than the GBP. On a fundamental level, we note that according to Al Jazeera, the Japanese Government has asked from China to remove a buoy in Japan’s EEZ, although this may not have a material impact on the JPY, it may signify a further deterioration in Japan’s relationship with China, which appears to have escalated over the past few months. Should there be further escalation in the in the tensions in the Sino-Japanese relationships, we may see safe haven inflows for the Yen. On a monetary level, we note the BOJ remained on hold during their monetary policy meeting, as was widely expected by market participants.

It should be noted that JPY traders earlier today were in a selling mode for JPY as BoJ’s interest rate decision failed to provide any indications for a change in the bank’s ultra-loose monetary policy settings disproving any analysts hoping for a shift. Hence, we expect monetary policy outlook differentials to continue to weigh on JPY.

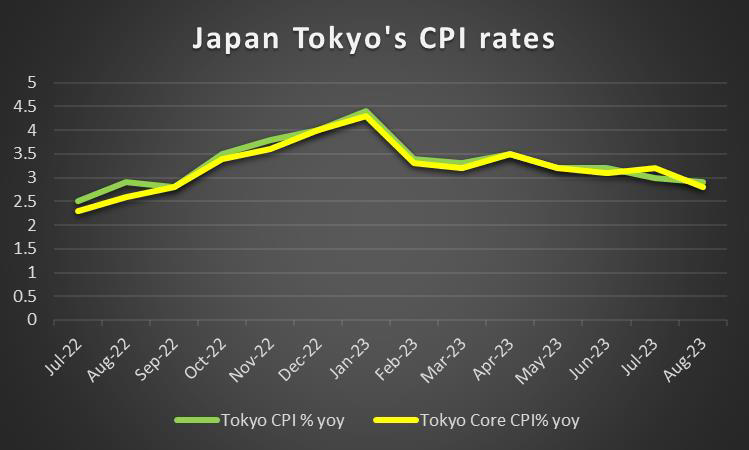

We have to note at this point that the Japanese Yen has reached very low levels against the USD and a market intervention by the Japanese government is possible. Japan’s Finance Minister Suzuki was reported saying by Reuters that he would “not rule out any options on currencies as the dollar broke above 148 yen to the dollar, warning against yen sell-offs that would hurt trade-reliant Japan”. Yet on a macroeconomic level, inflationary pressures in the Japanese economy do not seem to have slowed down substantially since February as Japan’s CPI rates for August tended to show.

Furthermore, it should be noted that the trade deficit widened in August, implying that the Japanese economy suffered even more outflows from its international trading activities and even worse Japan’s preliminary manufacturing PMI figure implied that the crucial sector suffered an even wider contraction of economic activity in the current month.

EUR – Eurozone’s HICP rates in focus

EUR is about to end the week in the reds against the USD yet stronger against the pound and the JPY. On a fundamental level, we note the escalating tensions between Poland and Ukraine over Poland’s ban on Ukrainian grain, with Ukraine filing a WTO lawsuit against Poland amongst other nations. The escalating tensions between Ukraine and EU members may lead to internal conflict in the EU, which could result in instability in the bloc and as such may weigh on the common currency in the long run.

On the monetary front, we note that ECB Kazimir, stated on Monday that “It is, therefore, premature to place market bets on when the first interest rate cuts will occur”, hinting that even if the bank may have reached its terminal rate, in his opinion the current interest rates will remain at current levels for a prolonged period of time. In addition, ECB Kazimir according to Reuters stated that “I cannot rule out the possibility of further rate increases today” implying that further rate hikes may still be feasible.

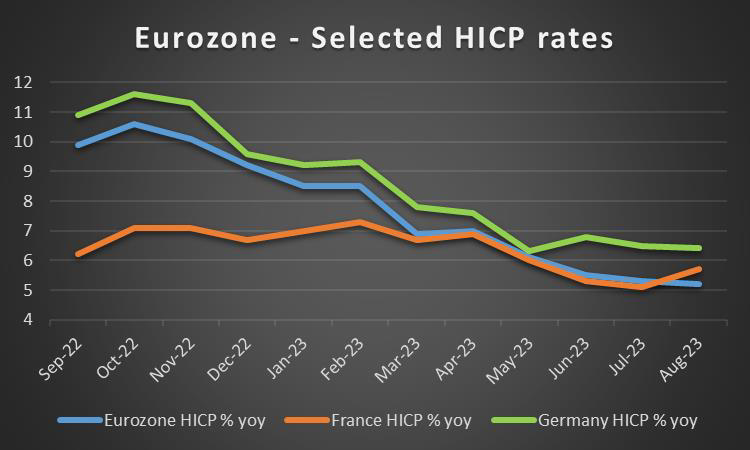

However, given that ECB Kazimir was a vocal advocate for further rate hikes, his apparent softening tone may be a further indication to the bears that the ECB may have reached its terminal rate, which could weigh on the EUR. On a macroeconomic level, the lower-than-expected Eurozone’s HICP rate on a yoy basis for August, was indicative of easing inflationary pressures on the Eurozone, perhaps implying that the current interest rate levels are sufficiently restrictive in combating inflation. In addition, the fact that despite the mixed signals about France and Germany the September preliminary PMI figures are still deep in a contractionary mode for the Eurozone in September thus supporting the case for the ECB to remain on hold with its interest rates, as further hikes may be weighing down on the economy.

However, France’s HICP rate came in as expected at 1.1% and the Zone’s HICP rate is still far higher than the ECB’s target, which may cast some doubt on the long-term feasibility of the ECB’s ambitions to remain on hold. Thus, we plan to closely watch the release of Germany’s IFO business climate and GFK consumer sentiment figures, given the characterisation of Germany as the patient of Europe, in addition to the Eurozone’s economic sentiment figure and the Preliminary HICP rates for Germany, France and the Eurozone in order to properly gauge if inflationary pressures in the Eurozone have eased. Should they come in higher than expected, we may see the EUR strengthening as the case for further hikes may be supported, whereas a lower-than-expected rate may ease calls for future hikes, thus weighing on the EUR.

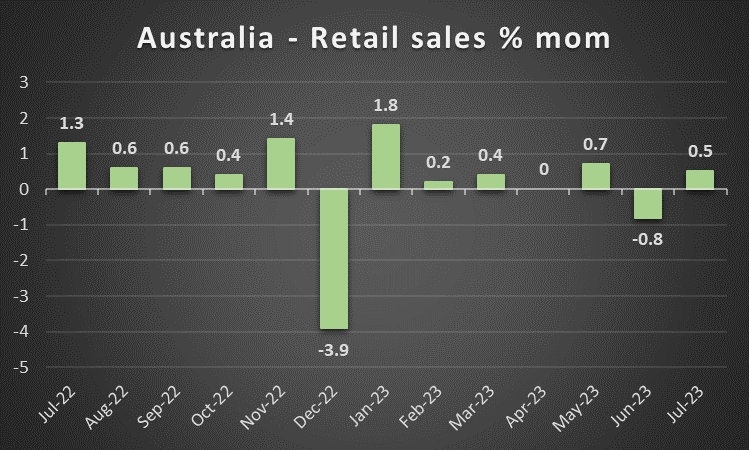

AUD – RBA’s September monetary policy meeting minutes

proposal, thus alleviating concerns for about roughly 7% of the global LNG market. On another fundamental issue, China’s better-than-expected industrial production rates were indicative of a strengthening manufacturing sector, thus should the economic conditions further improve it could also support the AUD, given that China is a major importer of Australian goods. On a monetary level, we note that the RBA September meeting minutes stated that “the case to keep the cash rate target unchanged at this meeting was the stronger one”, implying that the bank’s pause may have not been unanimous and that the case for a 25-basis point hike was made ”based on the expectation that inflation will remain above the Bank’s target” when referring to inflation.

Surprisingly, the market showed little to no reaction, implying that they believe that the bank’s rate hiking cycle is over. The minutes came in as we had predicted in last week’s report “due to the changing of the guard at the RBA, the September minute meetings may be more subdued in terms of a general consensus being reached to remain on pause, with a slight possibility of a hike”, which now appears to have weighed on the Aussie. On a macroeconomic level, we note a relatively quiet week for Australia in terms of financial releases with the exception of the Judo Bank Preliminary PMI figures for September, which came in lower than expected for the manufacturing sector, hinting at the possible negative consequences of higher rates. We tend to suspect that underlying fundamental issues still persist in the Chinese economy and as such from a more macro-perspective, we may see the Aussie weakening.

CAD – CPI August acceleration pressure BoC

Minister Trudeau recently accused India of being involved in the assassination of a Canadian Sikh activist, on Canadian soil. The accusation appears to have taken a dramatic turn for the worst with India expelling one of Canada’s top diplomats in the country, ramping up tensions between the two nations. The escalating tensions may not impact the Loonie, but are rare occurrences in which a democratic nation accuses another of murdering one of its citizens on its own soil. On another fundamental note, CAD traders may be keeping a close eye on oil prices which are about to end unchanged since last week, which could weigh on the Loonie as they tend to imply a temporary peak.

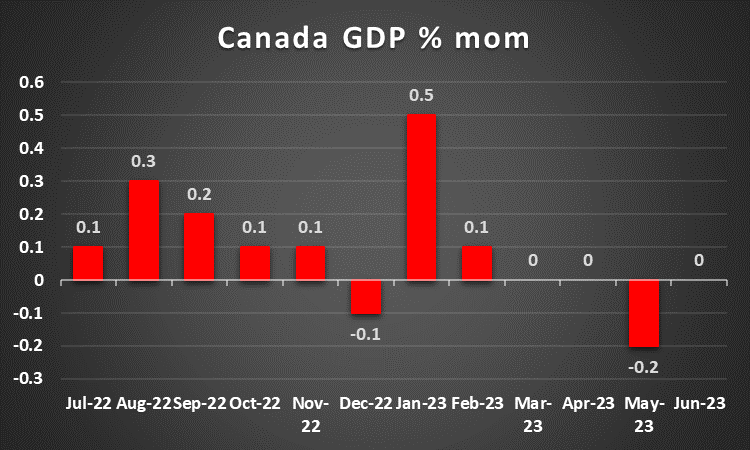

Should oil prices regain their upward momentum we may see some support for the Looney, given Canada’s status as a major oil-producing nation. On a monetary level, we note the BOC’s September monetary policy deliberations on Wednesday, which we correctly anticipated in last week’s weekly report that bank officials might prefer to keep interest rates at their current levels for a prolonged period of time, in order to properly assess their impact on the economy. As a result, we may see some support for the Loonie next week in the event that the GDP rates for July come in higher than expected, as it may indicate that the anticipation of slowing demand by the BOC may have not materialized and as such may warrant further rate hikes.

However, should the GDP rate come in lower than expected, we may see the Loonie weakening as it may enforce the bank’s view that the current interest rates are in restrictive levels and are slowing demand, thus reducing the need for further rate hikes, which could weigh on the Loonie. On a macroeconomic level, we note that Canada’s BoC’s CPI rates for August came in higher than expected, implying persistent inflationary pressures in the Canadian economy. Therefore, in our view, we anticipate that the bank may hike in its next meeting as it refers to the point made by BoC officials that they are concerned about the lack of progress in slowing core inflation, and as such may warrant future rate hikes.

Lastly, we note that Canada’s retail sales rate for July have yet to be released and that Loonie traders may be interested in next week’s business barometer figure for September and the GDP rate for July.

General Comment

In the coming week, we expect lower volatility in the FX market as the high volume of monetary policy decisions is to be reduced. We also note that in the equities markets, all three major indexes appear to be moving lower for the week, possibly also due to the uncertainty created by a possible US government shutdown. As for gold’s price, we note that it appears to ending the week slightly higher than last week, yet following the strengthening of the dollar, it is still possible that it may end the week in the reds. We note also the rise of US yields, which may have clipped any possible wider gains for gold’s price.

On a more fundamental level, we note that Saudi Crown Prince Mohammed bin Salman, in his first interview with an American TV channel since 2019, indicated that the US, Israel and Saudi Arabia were making progress in talks in regard to normalizing relations, however, the issue of Palestine still remains a key point for the Crown Prince, having stated that “The Palestinian issue is very important. We need to solve that part”.

The apparent improvement between US-Saudi relations which were perceived to have slightly soured due to OPEC’s oil production cuts, appear to be improving and should they continue on this trajectory we may see some good faith actions from Saudi toward the US, which may be in the form of easing on their oil production cuts in an attempt to garner some good faith from the US for future negotiations.

اگر در مورد این مقاله سوال یا نظر ی کلی دارید، لطفاً ایمیل خود را مستقیماً به تیم تحقیقاتی ما بفرستیدresearch_team@ironfx.com

سلب مسئولیت:

این اطلاعات به عنوان مشاوره سرمایه گذاری یا توصیه سرمایه گذاری در نظر گرفته نمی شود ، بلکه در عوض یک ارتباط بازاریابی است. IronFX هیچ گونه مسئولیتی در قبال داده ها یا اطلاعاتی که توسط اشخاص ثالث در این ارتباطات ارجاع و یا پیوند داده شده اند ندارد.