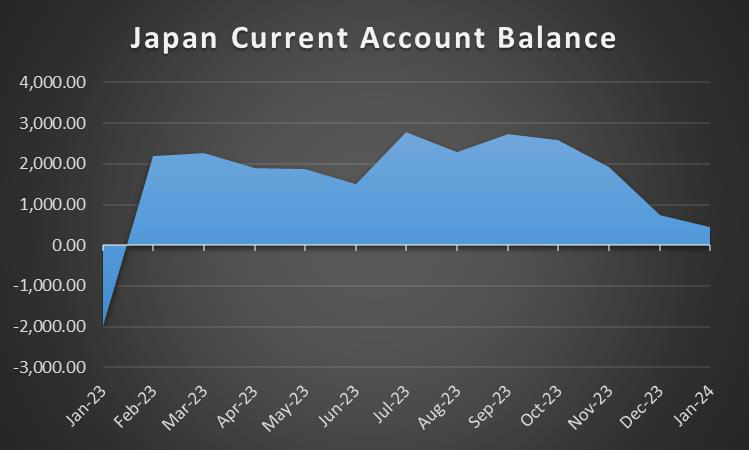

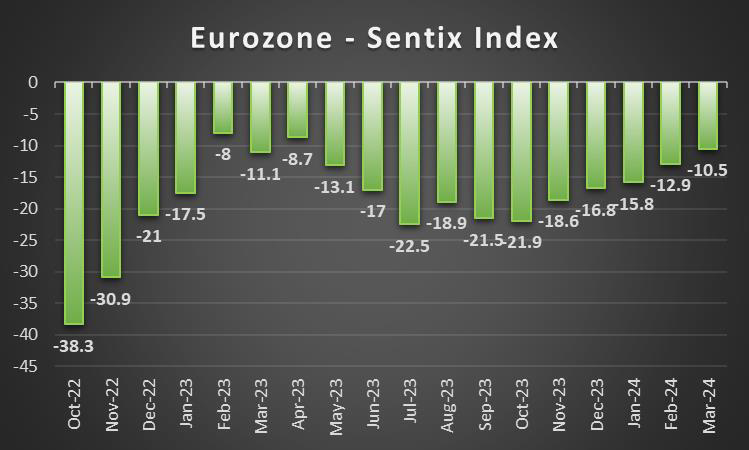

As the week draws to a close let’s have a look at what’s scheduled next week. On the monetary front, we note the release of the interest rate decisions of New Zealand’s RBNZ and Canada’s BoC interest rate decision on Wednesday and we highlight ECB’s interest rate decision on Thursday. Also please note that on Wednesday the Fed is scheduled to release the minutes of the March meeting, while SNB Chairman Jordan and BoJ Governor Ueda are to make statements on Monday and Wednesday respectively and could sway the market’s mood. As for financial releases, we get on Monday Japan’s current account balance for February, Germany’s industrial output for the same month and Eurozone’s Sentix index for April. On Tuesday we get Australia’s business conditions and confidence for March. On Wednesday we get Japan’s corporate goods prices for March, Sweden’s GDP rate for February, we note Norway’s and the Czech Republic’s CPI rates for March and we highlight the release of the US CPI rates also for March. On Thursday we get China’s inflation metrics for March, Norway’s GDP rates for February and from the US we get the weekly initial jobless claims figure and the PPI rates for March. Finally on Friday, we get China’s trade data for March, Germany’s and France’s final HICP rate for March, UK’s GDP and manufacturing output rates for February, Sweden’s CPI rates for March and the US preliminary University of Michigan consumer sentiment for April.

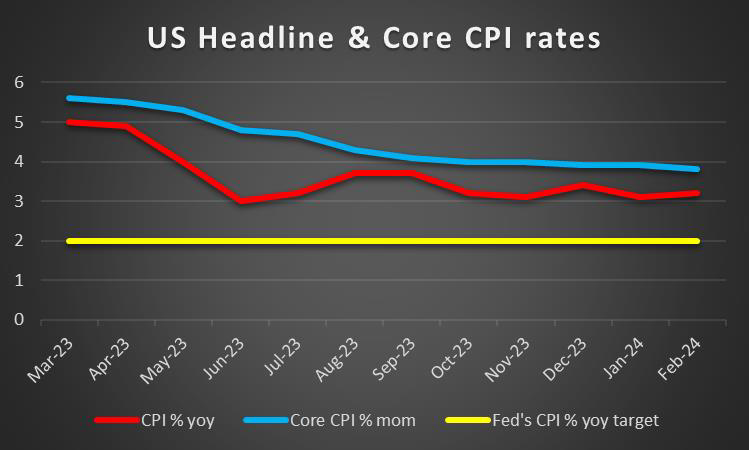

USD – US CPI rates for March to catch the market’s attention

After a roller coaster ride the greenback is about to end the week slightly weaker than its counterparts, yet the US employment report for March is still to be released and could alter that picture. The USD proved to be the main market mover in the FX market and the factors causing the greenback to change direction, were primarily two, the Fed’s intentions and financial data releases and we expect a continuance of that pattern in the coming week, as we get high impact releases on both fronts. But first things first, let’s have a look at what moved the dollar in the past few days. On Monday we saw the greenback getting some support as a better-than-expected reading for the ISM manufacturing PMI figure for March was released showing an expansion of economic activity for the sector for the first time since October 2022. On the flip side, the greenback lost ground on Wednesday as the ISM non-manufacturing PMI figure for March unexpectedly dropped implying a slower expansion of economic activity. In the coming week, we highlight the release of the US CPI rates for March. Should the rates slow down, we may see the USD slipping a bit, on the flip side, a failure of the rates to slow down or even a possible acceleration of the rates may provide asymmetric support for the USD as it could highlight the resilience of inflationary pressures in the USD economy and may force the Fed to maintain a tougher stance against the market’s expectations for three rate cuts starting in June. On the monetary front, we note the comments of various Fed policymakers over the week displaying some hesitation on behalf of Fed policymakers to start cutting rates. It’s characteristic that Fed Chairman Powell expressed his optimism for inflation to slow down, yet Fed policymakers need to see more evidence of easing inflationary pressures before cutting rates. On a monetary level, a number of Fed policymakers are scheduled to make statements throughout the week and could affect the market’s approach. We intend to focus also on the release of the Fed’s March meeting minutes on Wednesday and should the document showcase the bank’s hesitations to cut rates, we may see the USD getting some support.

GBP – UK’s GDP rates to move the pound

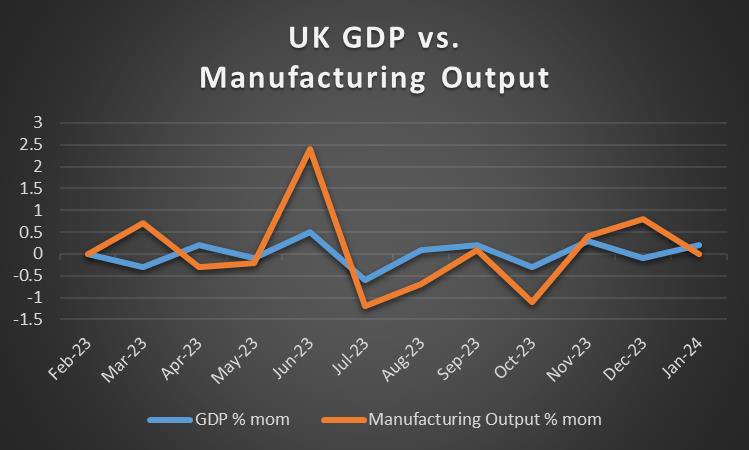

The pound is about to end the week relatively unchanged against the USD and the JPY but is losing ground against the EUR. On a macroeconomic level, we note the contraction of housing prices for March, while on a deeper fundamental level, we note that the number of mortgage approvals in the UK, beat expectations in Febraury which may provide some comfort regarding the outlook of the UK real estate sector. As foreconomic activity, the Manufacturing PMI figure for March was revised upwards showing an expansion of economic activity for the sector for the first time since July 2022. In the crucial services sector though, the slower expansion of economic activity for the same month was verified. In the coming week, we highlight for pound traders the release of the GDP and manufacturing output growth rate for February on Friday. A possible acceleration of the rates would imply growth for the UK economy and could provide some support for the sterling. On a monetary level, we note the market’s expectations for BoE to start cutting rates from the June meeting onwards and deliver three rate cuts in total before the year ends. For the time being, we may see BoE policymakers pushing back against market expectations, which could provide some support for the sterling. It’s characteristic how BoE interest rate setter Haskel warned last week that rate cuts are still a way off. Overall we tend to view the scenario of a rate cut in June as quite possible yet there is a high uncertainty for it. Also the bank expressed its intention to overhaul the way it produces and communicates its outlook for the economy according to the Financial Times.

JPY – BoJ’s intentions are key for JPY’s direction

JPY despite some slight bearish tendencies against the USD and the pound remained relatively stable during the week, while is losing ground against the EUR. On a macroeconomic level, we note that the Q1 Tankan index for big manufacturers dropped yet less than expected, while the sister indicator for non-manufacturers rose more than expected, both providing some improvement in Japan’s economic outlook. Also, we note an improvement in the demand side of the Japanese economy as the All household spending for February accelerated escaping the negative area and showing growth again on a month-on-month level. On the monetary front, we note market expectations for the bank to continue hiking rates and deliver another three 10 basis points rate hikes until the end of the year. On the other hand, BoJ policymakers are signaling some hesitance towards further monetary policy normalisation or at least seem to take their time and that may weaken the JPY on a monetary level. It’s characteristic that ex-BoJ official Watanabe expects the bank to raise interest rates again in October at the earliest. Furthermore, we also note that BoJ lowered its expectations for the economic recovery of most regions yet at the same time still seems confident that wage rises are widening to other regions of Japan. Such a scenario may imply a feeding of inflationary pressures in the Japanese economy and enable the bank to proceed with more rate hikes. On a more fundamental level, we note that given that JPY remains near quite low levels against the USD, the possibility that the Japanese government may proceed with a market intervention operation to the Yen’s defence, is still present. Also, the recent escalation of tensions in various geopolitical issues such as the war on Gaza could generate safe haven inflows for the Japanese currency.

EUR – ECB’s interest rate decision to rock the EUR

The common currency broke a three-week losing streak and is about to end the week in the greens against the USD, while it also is scoring gains against the pound and the Yen in a sign of a wider strength. In the coming week, we highlight the release of ECB’s interest rate decision on Thursday as the main event for EUR traders. The bank is widely expected to remain on hold keeping the deposit rate at 4.00% and the refinancing rate at 4.50%. Currently, EUR OIS imply a probability of 90% for such a scenario to materialise while they also imply that the market may expect the bank to start cutting rates in the June meeting and deliver four rate cuts in total for the year. We expect the bank to remain on hold in line with market expectations, and if actually so, we may see market attention turning the release of the accompanying statement and ECB President Lagarde’s press conference. Should the bank opt to start preparing the markets for a possible rate cut in its June meeting, keeping a rather dovish tone, we may see the market’s expectations for rate cuts being enhanced and thus such a scenario may weaken the EUR. On the flip side, should the bank maintain a strong, confident, hawkish tone, or push back against market expectations for rate cuts in the June meeting, we may see the market repositioning itself and thus the EUR getting some support. It should be noted that March’s preliminary HICP rates for the Eurozone slowed down beyond market expectations, both on a headline and a core rate level. Characteristically the headline rate was at 2.4% yoy nearing substantially the ECB’s target of 2% yoy, which may allow the bank to start preparing for a rate cut. Otherwise, the ECB may opt to wait until the HICP rates are at or below its target to start cutting rates.

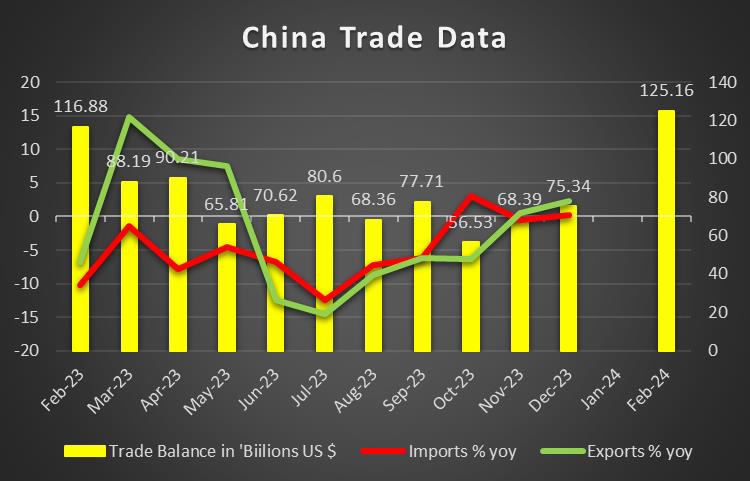

AUD – Fundamentals to lead the Aussie

AUD is about to end the week higher against the USD. On a monetary level, we note the release of RBA’s March meeting minutes last Tuesday. The document showed that the Bank’s policymakers did not consider the possibility of a rate hike, which tends to underscore the easing of worries about the path of inflationary pressures in the Australian economy. Characteristically, the document stated that “ Members observed that inflation had continued to moderate over prior months, broadly as expected”. The market seems to expect the bank to cut rates in September and stop for the year. Overall we expect the Aussie to be under pressure on a monetary policy level. On a fundamental level, we note the close Sino Australian economic ties and any improvement in the Chinese macroeconomic outlook could provide some support for the Aussie as well as it would imply more exports of raw materials from Australia to China. Hence we highlight the release of China’s manufacturing PMI figures for March. Both the Caixin and NBS manufacturing PMI figures, aligned in rising above 50, and thus showcased an increase of economic activity in the crucial manufacturing sector. Next week we may see AUD traders keeping a close eye on the release of China’s March trade data. Furthermore and on a deeper fundamental level, we note that Aussie as a commodity currency is considered of riskier nature and thus should the market sentiment turn more risk oriented, we may see AUD getting some support. Please note that the number of high impact financial releases stemming from Australia the coming week are to be few, thus we expect fundamentals to lead the Aussie.

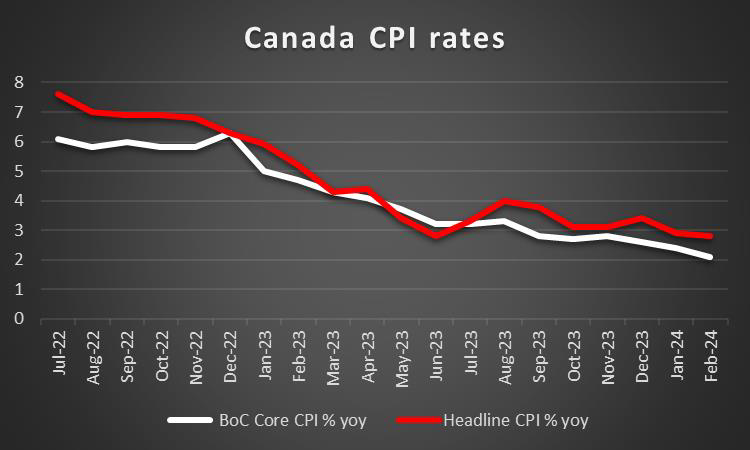

CAD – BoC’s interest rate decision eyed

The CAD is about to end the week relatively unchanged against the USD, yet Canada’s employment data for March are still to be released and could alter the Loonie’s direction. On a fundamental level, we may see Loonie traders keeping a close eye over the course of oil prices give the positive corelation of oil with CAD, as Canada is a major oil producing economy. Oil prices moved decisively higher during the week, with the latest push upwards being caused by the market worries about the supply side of the international oil market. Tensions in the Middle East, with war on Gaza and an escalation in the tensions of the Iranian-Israeli relationship being on the rise, tended to fuel market worries and thus allowed oil prices to climb higher. We expect that should oil prices continue to be on the rise, we may see them providing also support for the CAD. Yet the main event in the coming week for CAD traders may prove to be the release of BoC’s interest rate decision on Wednesday. The bank is expected to remain on hold, keeping interest rates at 5.00% and currently CAD OIS imply a probability of 83% for such a scenario to materialise. We also note the market’s expectations for the bank to start cutting rates in its June meeting and deliver a total of three 25 basis points rate cuts until the end of the year. The market’s expectations are understandable in the sense that the CPI rates entered the bank’s 1%-3% target zone both on a headline as well as on a core level. Hence, should the tone of the bank’s accompanying statement be characterised by the prospect of an easing of its monetary policy, we may see the Loonie weakening as it would reaffirm the market’s expectations. On the contrary, should the accompanying statement imply a continuance of the tight monetary policy we may see the CAD getting some support as the market may have to reposition itself.

General Comment

Overall we expect that volatility in the FX market is to be maintained given that we have a high number of high impact financial releases. We also expect that the USD may remain in the driver’s seat in the FX market as the frequency and gravity of US high impact financial and monetary releases is to be maintained as well. As for US stockmarkets, we note that US stock markets are about to end the week in the reds, after Thursday’s sell-off, yet the week is still not over. Some consolidation was expected on a technical level, given that all three major US stockmarket indexes, namely the Dow Jones, S&P 500 and Nasdaq, were trading near record high levels. Main factors behind US stockmarket movement, seem to be also fundamental with the Fed’s intentions being on traders’ minds. Any signal for a possible prolongment of the relatively tight financial conditions in the US economy could weigh on US stockmarkets and vice versa. Yet we also note that equities may start generating more interest in the coming week, as the earnings season kicks off on Friday with major banks such as City Group (#C), JPMorgan (#JPM) and Wells Fargo (#WFC) releasing their earnings reports. As for gold, we note that after hitting new record high levels at $2305 per ounce, has retreated lower, yet is still about to end the week in the greens. We expect the negative corelation of the USD with gold’s price to be one of the main drivers of gold’s price in the coming week, yet also the path of US yields could influence the precious metal’s direction as could safe haven flows.

اگر در مورد این مقاله سوال یا نظر ی کلی دارید، لطفاً ایمیل خود را مستقیماً به تیم تحقیقاتی ما بفرستیدresearch_team@ironfx.com

سلب مسئولیت:

این اطلاعات به عنوان مشاوره سرمایه گذاری یا توصیه سرمایه گذاری در نظر گرفته نمی شود ، بلکه در عوض یک ارتباط بازاریابی است. IronFX هیچ گونه مسئولیتی در قبال داده ها یا اطلاعاتی که توسط اشخاص ثالث در این ارتباطات ارجاع و یا پیوند داده شده اند ندارد.