With the week nearing its end, we note that Canada’s Employment data for August have yet to be released. On a monetary level, we highlight the ECB’s interest rate decision on Thursday. In regards to financial releases, we make a start on Monday with Norway’s and the Czech Republic’s CPI rates for August and on Tuesday, we begin with the UK’s Employment data, followed by Norway’s GDP rate for July and finish the day with Germany’s ZEW indicators for September. On Wednesday we make a start with Japan’s corporate goods price rate for August, followed by the UK’s Preliminary GDP and Manufacturing Output rates both for the month of July. Later on, we note the Eurozone’s industrial production rate for July and we highlight the release of the US CPI data for August. On a Thursday, we begin with Japan’s Machinery orders rate for July, followed by Australia’s Employment data and Sweden’s CPI rate for August, the US weekly initial jobless claims figure, PPI rates and Retail sales rates both for the month of August. Finally on Friday, we note China’s industrial output rate for August, followed by Canada’s Manufacturing sales rate for July, the US Industrial production rate for August and the Preliminary University of Michigan Sentiment figures for September.

USD – US Economy to gear up for another rate hike?

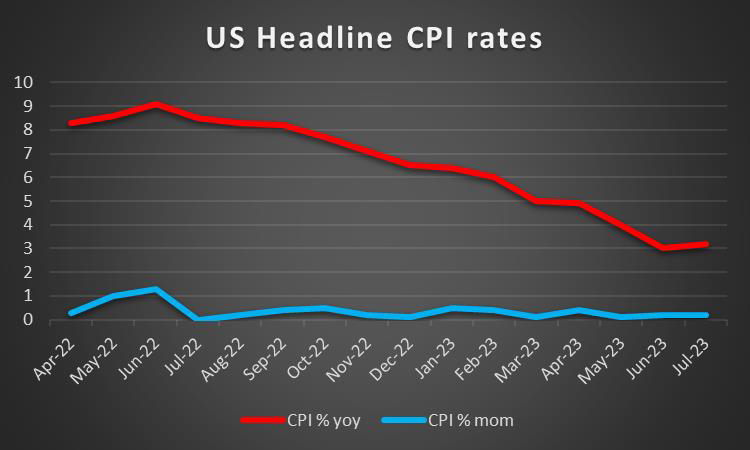

The USD is about to end the week in the greens, marking its 8th consecutive winning streak as the dollar’s ascent appears to be unstoppable. On a fundamental level, we highlight that the Pentagon announced on Wednesday a new security package for Ukraine, including the controversial armour-piercing munitions, which could draw some condemnation from China. Should there be further indications towards increased tensions between the two nations, the market sentiment may decline causing the USD some safe haven inflows. On a monetary level, we highlight the speeches by Cleveland Fed President Mester and Fed Governor Waller who stated that “a couple of months continuing along this trajectory before I say we’re done” raising interest rates”, which could be interpreted that the bank may be willing to continue on its aggressive rate hiking cycle in order to combat inflationary pressures. However, it could also imply that the bank may be nearing its terminal rate as other Fed policymakers have signalled, which may be in line with market expectations of the bank’s interest rate hiking cycle to peak and as such could weaken the green, in anticipation that the end is in sight. On a macroeconomic level, we highlight the US Employment data which came in last Friday, which showed an increase in the Non-Farm Payrolls figure, yet the Unemployment rate rose and hourly earnings fgrowth rate slowed down, potentially indicating a loosening of the US labour market in the long run. Furthermore, the Fed’s beige book that was released on Thursday was indicative of a reduction in activity and implied that hiring growth peaked during the summer, further supporting our aforementioned theory. However, the negative sentiment appears to have been mitigated following the ISM Manufacturing and Non-Manufacturing PMI figures which were better than expected, despite the former still implying a contraction of economic activity, indicating stronger than expected manufacturing and non-manufacturing sectors, which may be seen as a resilient US economy. In conclusion, the better-than-expected ISM PMI figures both for Non-Manufacturing and Manufacturing seem to be behind the dollar’s ascent, which could have opened the door to the Fed should it decide to continue its rate hiking cycle. Lastly, looking at next week we note the release of the US CPI rates for August as the next big test for the greenback but also note the weekly Initial jobless claims figure, Final PPI ,retail sale rates and the US Industrial production rate all for the month August in addition to the preliminary University of Michigan Sentiment figure for September.

GBP – Has the BOE reached its terminal rate?

The pound seems about to end the week weaker against the USD, EUR and remains rather stable against the JPY.. On a fundamental level, we note that the Birmingham city council has declared bankruptcy, which could have a fundamental impact of the pound should more councils declare “financial distress”, in the event that the Government is forced to re-allocate funds to “save” the council(s). On a monetary level, we highlight the speech by BoE Governor Bailey who stated “we are much nearer now to the top of the cycle. And I’m not therefore saying we’re at the top of the cycle because we’ve got a meeting to come”, implying that the bank may be reaching its terminal rate, and as such as was mentioned last week an easing of BoE’s hawkishness in the coming week may weigh on the pound as the case for the bank’s for future rate hikes, appears to have weakened. On a macroeconomic level, we note the UK Halifax house prices rate for August, which came in lower than expected, implying a reduction in demand for housing in the UK, which could be attributed to the burden placed on consumers due to the currently high-interest rates, which may have discouraged new first home buyers. Lastly, we note the increase of major financial releases next week and as such, we may see the pound being more influenced by data once again.

JPY – Japan’s revised GDP rate for Q2 indicates a weaker than expected economy

JPY is about to end the week relatively unchanged against the EUR and GBP and weaker than the dollar.On a fundamental level, we note that according to various media sources, the Japanese Prime Minister is due to re-shuffle his cabinet next week in an apparent attempt to drum up support for the incumbent Government before a possible snap election. On a monetary level, we note the speech from BOJ policymaker Nakagawa whose comments, appear to have been perceived as dovish, as Nakagawa stated that “we’re not at a stage where we can judge that Japan has achieved our price target in a stable, sustainable fashion”, implying that the bank may remain on its ultra-loose monetary policy course, which in turn could weigh on the JPY. On a macroeconomic level, we note Japan’s revised GDP rate for Q2 which came in lower than expected during today’s early Asian session, implying that the bank’s current monetary policy appears not to be having a positive impact on the country’s economy to the degree expected and as such could weaken the case for a tightening of the monetary policy. Therefore, in conclusion we may see the JPY weakening as we head into next week, unless BoJ and/or the Japanese government come to the Yen’s rescue or the Japanese currency gains some safe haven inflows.

EUR – Deceleration of growth in the Union following the Preliminary GDP rates for Q2

EUR is about to end the week in the reds against the USD yet slightly stronger against the pound and the JPY. On a fundamental level, we highlight the statement made by the ECB Executive board member Frank Elderson who stated that “The tragedy is upon us and it has started to unfold” when referring to the effects of climate change. Should the ECB decide to aggressively push its climate change agenda, it could impact the manufacturing capabilities of the Eurozone at a time when the bloc needs to project strong manufacturing capabilities. On the monetary front, we note the speech by ECB President Lagarde in which she avoided providing an indication about whether or not the ECB will raise or hold interest rates in their Monetary policy meeting next Thursday. Furthermore, ECB Nagel stated on Tuesday that “It would be wrong to speculate that an interest-rate peak will soon be followed by cuts,”, implying that the bank may maintain its current level of high interest rates for a prolonged period of time. Should the bank decide to remain on hold as is widely anticipated by market analysts, it could weaken the EUR, as it may signal that the bank has reached its terminal rate, yet the bank may opt for a 25-basis point hike based on comments made by ECB President Lagarde last week and ECB Holzman’ who supported the case for further rate hikes. On a macroeconomic level, the downward revision of Eurozone’s GDP rates for Q2 was indicative of a reduction in economic activity as an average of the euro-area. The lower-than-expected Preliminary GDP rates for Q2 may be a sign that the current monetary policy is at sufficiently restrictive levels. However, the better-than-expected exports and imports rates for July for Germany, could indicate that if inflation is left ‘unattended’ it could re-surface, which could risk the undoing of the ECB’s work so far. We also note that Germany’s ZEW Economic sentiment figure for August is due out next Tuesday.

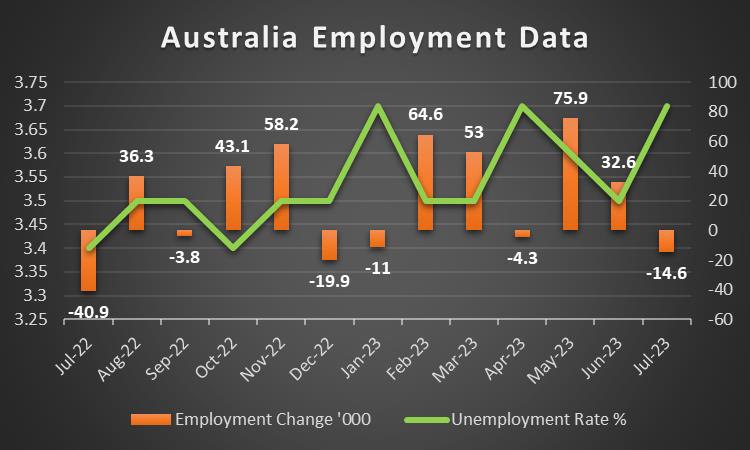

AUD – RBA remains on pause

AUD is about to end the week weaker than the USD. On a fundamental level, we note that LNG workers at the Chevron plants are reported to have begun partial strikes, intensifying supply chain fears for LNG in Europe. On a deeper fundamental level, we highlight the substantial effort by China to recover its economy, which may be bearing some fruit following the better than expected imports rate for August, which may support the Aussie given their heavy dependence on China to import their goods. On a monetary level, we note the comments made by outgoing Governor Lowe, who stated if “ inflation became sticky, would require tighter monetary policy”, implying that the bank following his absence, may still need to raise rates if needed. However, during this week’s interest rate decision, the bank remained on hold, which appears to have disappointed traders, as the Aussie appears to have retreated to lower ground following the announcement. We also note that beginning September 18th, the new Governor will be the current Deputy Governor Bullock who is set to inherit a bank that has been criticized for stifling growth. On a macroeconomic level, we note Australia’s real GDP rate for Q2 which was released on Wednesday, which came in better than what market analysts had expected. In particular, the GDP rate on a quarter on quarter level, came in at 0.4%, identical to that of Q1, yet on a year on year level it came in slightly lower at 2.1% but still managed to beat market expectations of 1.8%. Therefore, the better than expected GDP rates could potentially indicate that the Australian economy is more resilient than what market analysts give it credit for. However, the better than expected GDP rates seem to have managed to temporarily stop the ‘bleeding’, before the Aussie continued its downwards trajectory. As such, market participants may be looking forward to Australia’s employment data on Thursday, which we anticipate that may come in slightly higher than last month’s data, thus potentially providing support for the Aussie. Yet should it disappoint traders and come in lower than expected, it could potentially weigh on the AUD.

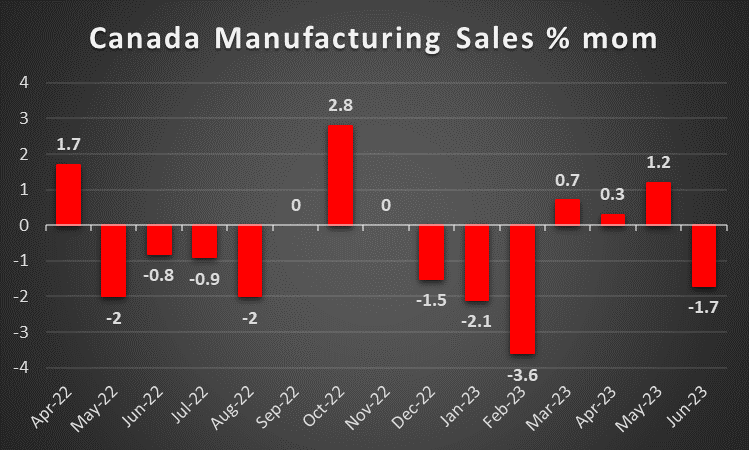

CAD – BoC remains on hold

The Loonie is on track to finish for an 8th week in a row lower than the greenback. On a fundamental level, we note that the evacuees that were ordered to leave their homes due to wildfires are now being told that they can return to their homes. On another fundamental note, CAD traders on the other hand may keep a close eye on oil prices which following the surprise announcement by Saudi Arabia and Russia that they would be extending their oil cuts up until the end of the year, saw oil prices print yearly highs, nearing the $90 per barrel figure. On the other hand, market worries for the demand outlook of the commodity, given China’s slow recovery may weaken oil prices. Should oil prices continue to rise we may see the CAD benefiting, given that Canada is a major oil-producing economy. On a monetary level, we note that the Bank of Canada remained on hold during their interest rate decision on Wednesday, as was widely anticipated by market analysts. However, the bank stated that they are “prepared to increase the policy interest rate further if needed”, implying that the door for future rate hikes is still open, should it be required and as such could provide support for the Loonie should inflationary pressures persist. On a macroeconomic level, we note that Canada’s GDP rates for Q2 came in lower than expected, implying that the Canadian economy may not be able to sustain the currently high-interest levels for much longer, with the possibility for the economy to enter a recession slightly increasing. We also note that at the time of this report, the Canadian employment data has yet to be released and should it come in better than expected, we might see some strength by the Loonie, as it could aid to the narrative stated by the bank yesterday. On the other hand, should it come in lower than expected we may see the Loonie further ceding ground to the USD. Lastly, we note Canada’s manufacturing sales rate for July, which is due to be released on Friday, which we anticipate to improve slightly, which may support the Loonie. However, should it come in lower than expected, it could further weaken the dollar.

General Comment

In the coming week, we expect volatility in the FX market to continue to increase given the high volume of financial releases that are due out. We also note that in the equities markets, Arm LTD is widely anticipated to launch its IPO next week, on the 14th of September and has been widely touted as the biggest IPO of the year. As for gold’s price, we note that it appears to have ended its two week winning streak and is on track to end the week lower. On a more fundamental level, we highlight that the G20 summit is due to take place over the weekend, with its starting date on Saturday. During the meeting, it may be interesting to see if the US is going to be able to advance its relationships with emerging economies, given the absence of Russian President Putin and Chinese leader Xi. In the sidelines India may officially announce its intentions to be renamed as Bharat, following the widespread reporting of the current President Droupadi Murmu , sending G20 invites in which she is being referred to as the “President of Bharat”. Lastly, we note that the tensions between the US and China seem to be affecting industry giants such as Apple, following the announcement by China that it was restricting the use of iPhones by Government officials and was planning to widen the iPhone ban, leading to the stock dropping like a rock during Thursday’s trading session. Overall though the issue may have wider consequences if considered that China Huawei was able to launch its new mobile phone with a new microchip. Voices in the US Congress are calling the Biden administration for harder measures against China. Should the tensions in the US-Sino relationships escalate further, we may see a more cautious sentiment settling in the markets which may have a more adverse effect on riskier assets such as equities and commodity currencies, AUD and NZD.

اگر در مورد این مقاله سوال یا نظر ی کلی دارید، لطفاً ایمیل خود را مستقیماً به تیم تحقیقاتی ما بفرستیدresearch_team@ironfx.com

سلب مسئولیت:

این اطلاعات به عنوان مشاوره سرمایه گذاری یا توصیه سرمایه گذاری در نظر گرفته نمی شود ، بلکه در عوض یک ارتباط بازاریابی است. IronFX هیچ گونه مسئولیتی در قبال داده ها یا اطلاعاتی که توسط اشخاص ثالث در این ارتباطات ارجاع و یا پیوند داده شده اند ندارد.