We tend to note some degree of hesitation for US stock market bulls, as there were some mixed signals interfering with the clearcut bullish run of past weeks. In this report, we are to take a different approach than usual and focus mostly on major fundamental issues that surround the US stock markets and end the report with a technical analysis of a US stock market index for a more rounded view.

Fitch downgrading the US economy

On a fundamental level, we note the fresh downgrading of the US economy by Fitch. The credit rating agency stripped the US from its perfect AAA rating and downgraded it to AA+. The main reason cited for the decision was the expectation of a difficult fiscal expansion ahead as the US Government, due to the high US debt and debt ceiling rules after the agreement reached with Congress raised some degree of uncertainty. The US Government strongly disagreed with the rating agency’s decision and stated that the decision to downgrade the US “defies reality to downgrade the United States at a moment when President Biden has delivered the strongest recovery of any major economy in the world,“. It should be noted that Fitch is the second credit rating agency downgrading the US after Standard & Poor’s for the same reason. For the time being we do not concur with the downgrading given that we saw the preliminary US GDP rate accelerating for Q2, beyond market expectations implying a resilience of the US economy, while at the same time inflationary pressures seem to be easing, allowing the Fed to end its rate hiking cycle or at least is near the terminal rate. The news may sour the market sentiment, as uncertainty rises and weaken US stock markets, yet for the time being we expect the overall effect to be temporary if it’s being expressed at all.

The Fed’s interest rate decision and data

US stock markets did not seem to have been affected substantially by the Fed’s interest rate decision last week. The Fed delivered the expected 25 basis points rate hike yet provided little new for market participants. In its accompanying statement, in our opinion, the bank seems to have removed its predisposition for more rate hikes and is more data-dependent. It’s as if the bank accepts that it has reached the end of its rate hiking cycle yet at the same time keeps the door open for another rate hike in the September meeting if necessary. The release overall was viewed as leaning towards the dovish side and tended to provide some slight support for US stock markets. It should be noted that on the other hand, the release of the US Core PCE price index for June, improved the market sentiment as the rates slowed down beyond market expectations implying that inflationary pressures continued to be on the retreat in June a scenario that if combined with the stronger than expected preliminary GDP rate for Q2, enhance market’s expectations that the US economy will be able to avoid a recession. The data tended to provide some support for US stock markets as the pressure on the Fed to continue hiking rates seemed to have eased further which provides additional support to the idea that the recovery of the US economy may be faster than initially expected. We highlight as the next major risk event for US stock markets the release of July’s US employment report with its NFP figure on Friday and should data show that the US employment market remains considerably tight, we may see US stock markets retreating.

Earnings reports

But in addition to the above stock traders have to navigate through earnings reports which are being released. We make a start with Starbucks which tended to disappoint traders given that despite the expansion in China and improved and better-than-expected EPS figure, revenue was slightly lower than expected. On the other hand, both Merck and Pfizer delivered better-than-expected figures both on an EPS and revenue level, implying a healthy pharma sector. Up until our next equities report we note the possible release of Novavax (#NVAX), Apple (#AAPL), Amazon (#AMZN), GoPro (#GPRO), DropBox (#DBX), TNDM, Airbnb (#ABNB), Booking (#BKNG), LYFT (#LYFT) and Walt Disney Company (#DIS), among others. Hence there is expected to be an increased focus on the US tech sector as well as traveling.

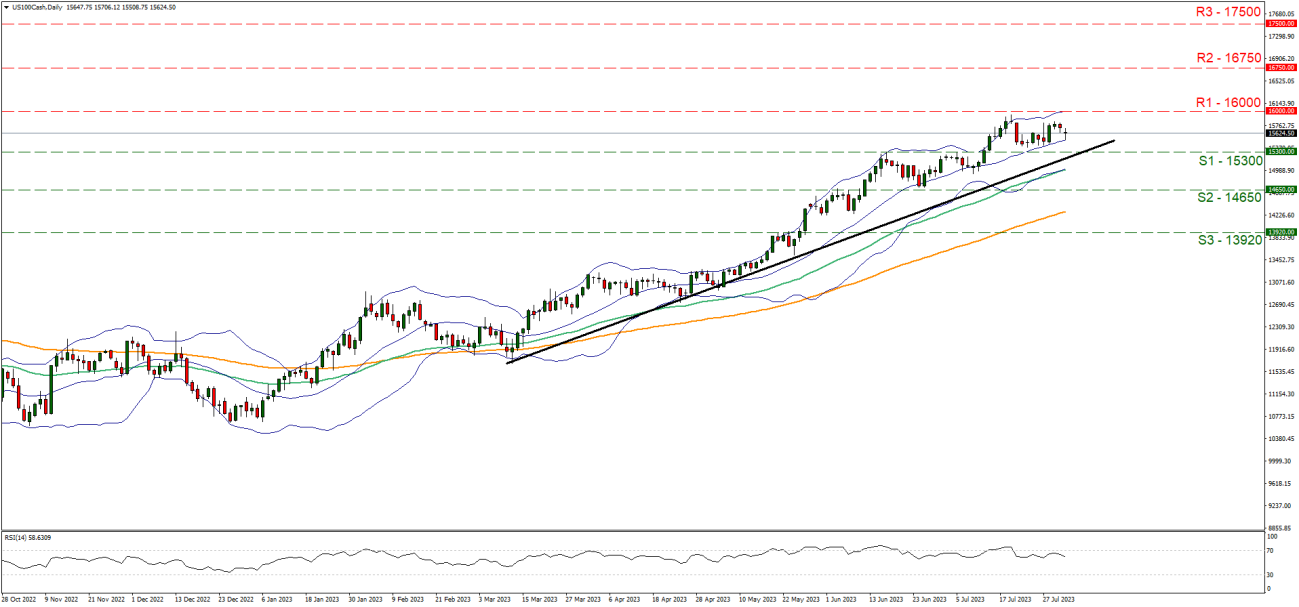

تجزیه و تحلیل فنی

#US 100 (Nasdaq) Daily Chart

Support: 15300 (S1), 14650 (S2), 13920 (S3)

Resistance: 16000 (R1), 16750 (R2), 17500 (R3)

Nasdaq (US100) seems to have stabilised somewhat over the past week, remaining in a rangebound movement between the 16000 (R1) resistance line and the 15300 (S1) support line. We tend to maintain an expectation that the sideways motion is to be maintained in the coming week given also that the RSI indicator is slowly dropping, aiming for the reading of 50, implying that the influence of the bulls in the market sentiment is fading away. Yet on the other hand the upward trendline incepted since the 13th of March, and given an intensifying bullish movement at some point, for the time being remains intact. Also please note that the 20 (Blue line, median of Bollinger bands), the 50 (Green line) and the 100 (Orange line) moving averages, all are pointing upwards, supporting the notion of a continuation of the upward movement. Hence any bullish tendencies of the index’s price action should not take us by surprise. Should the bulls actually regain control over the index we may see the index breaking the 16000 (R1) resistance line, with the next possible target for the bulls being the all-time high level of 16750 (R2) resistance barrier. Should the bears take over, we may see the index dropping, breaking the upward trendline prementioned, signaling an interruption of the upward movement, breaking the 15300 (S1) support line and aiming if not breaking the 14650 (S2) support base.

اگر در مورد این مقاله سوال یا نظر ی کلی دارید، لطفاً ایمیل خود را مستقیماً به تیم تحقیقاتی ما بفرستیدresearch_team@ironfx.com

سلب مسئولیت:

این اطلاعات به عنوان مشاوره سرمایه گذاری یا توصیه سرمایه گذاری در نظر گرفته نمی شود ، بلکه در عوض یک ارتباط بازاریابی است. IronFX هیچ گونه مسئولیتی در قبال داده ها یا اطلاعاتی که توسط اشخاص ثالث در این ارتباطات ارجاع و یا پیوند داده شده اند ندارد.