With the week nearing its end, we note that the BRICS summit is due to be hosted in South Africa next Tuesday, with the leaders of the group anticipated to discuss the creation of a common currency backed by a basket of commodities and/or gold. On the monetary front, we note Turkey’s interest rate decision on Thursday. As for financial releases, we make a start on Monday with Germany’s producers prices rate for July and the UK’s House Price rate from Rightmove for August. On Tuesday we note Norway’s GDP rates for Q2. On Wednesday, we note Japan’s JibunBK Preliminary PMI figure, France’s ,Germany’s and the Eurozone’s Preliminary manufacturing PMI figures for August, followed by the UK’s preliminary manufacturing and services PMI figures for August, followed by Canada’s Retail sales rate for June, the US S&P preliminary PMI figures for August and the Eurozones preliminary Consumer Confidence figure for August. On Thursday we make a start with France’s manufacturing business climate figure for August, the UK’s CBI distributive trades figure for August, the US durable goods rate for July and the US weekly initial jobless claims figure. On Friday we note Japan’s Tokyo CPI rate for August, Germany’s preliminary GDP rates for Q2, Sweden’s Unemployment rate for July, Germany’s IFO figures for August and the US University of Michigan Final figure for August.

USD – US Treasury Yields reach 15-Year highs

The USD continued its upward trajectory against its counterparts for its 5th week in a row. On a fundamental level, we highlight that following Moody’s credit rating agency, downgrading a number of mid-sized banks last Monday, a Fitch credit rating analyst according to CNBC claimed that the nay be forced to downgrade a number of US banks which may include JPMorgan, potentially causing some concern over the “health” of the US banking industry. On a monetary level, we highlight the release of the FOMC July meeting minutes, indicated that “most participants continued to see significant upside risks to inflation, which could require further tightening of monetary policy”, implying that the bank may continue its in rate hiking path. Yet two officials favoured leaving rates unchanged, potentially hinting at some signs of dissent in the FOMC. Furthermore statements made by Minneapolis Fed President Kashkari on Wednesday hinted that more rate hikes may be required, yet in our opinion we believe that some dovish chords were struck during his statements as he stated that “We can take a little bit more time to get some data before we decide whether we need to do more”, potentially indicative of a softening stance , which may be translated in favour of a pause in the FOMC’s next meeting. On a macroeconomic level, we highlight Tuesday’s Retail sales rates for July in addition to the Philadelphia Fed Manufacturing figure for August which appeared to be indicative of a resilient US economy despite the high interest rates. Furthermore, the US Treasury Yields have reached 15-Year highs during the week, which may be indicative of market expectations of prolonged high interest rate levels. Lastly, we highlight the release of the US S&P Preliminary Manufacturing PMI figure for August next Tuesday and the US durable goods rate for July next Thursday.

GBP – Is the UK economy in trouble?

The pound seems about to end the week higher against the USD and the JPY but lower than the EUR. On a fundamental level, we note the deciscion by PM Rishi Sunak who stated that the Government is commited to increasing the state pensions despite the current rate of Inflation. On a monetary level, BoE Pill stated during a BoE event yesterday that “monetary policy is now in restrictive territory”, reffering to the slides predented during the August Monetary Policy Report. BoE’s pill could be intepreted that the BoE may proceed with a less aggressive approach as “that monetary tightening, that policy is working”, potentially indicating that the BoE may be concerned about overhiking and “strangling” the economy. On a macroeconomic level, the UK’s CPI rates on Wednesday came in higher than expected, implying persistent inflationay pressures. However, that may be of concern given that the Unemployment rate came in higher than expected on Tuesday combined with the lower than expected Retail sales rate released earlier today, paint a dire picture for the UK economy. As with high inflationary pressures and increasing unemployment , with a potential reduction in economic growth ,we return to last weeks moral question where the BoE, may have to consider forcing the UK economy to potentially enter a recession in order to curb inflation or try to tackle inflation over a prolonged period of time, yet such a scenario may keep economic growth at anemic levels. Lastly, we highlight next week’s Housing prices rate which is due on Monday and the UK’s Preliminary PMI figures on Wednesday.

JPY – Japan’s GDP rate indicate a strong economy

JPY is about to end the week lower against the USD the pound but stronger against the EUR. On a fundamental level, we note the Trilateral Summit between the US, Japan and South Korea which is taken place today in the United States at Camp David, the presidential retreat. The summit could potentially draw the ire of China, thus potentially escalating tension. In the Asian-Pacific region. On a monetary level, we note the statements made by BoJ’s Suzuki that the bank will respond appropriately to excessive moves in the FX market, prompting market analysts to consider the possibility of the Japanese Government intervening in the FX market should the exchange rates as he stated that “The government is closely monitoring market developments with a high sense of urgency”. On a macroeconomic level, we highlight the the country’s Preliminary GDP rates come in better than expected for both on a yoy level and on a qoq level, implying that the Japanese economy remains resilient. Aiding to the positive news was Japan’s Core CPI print which was released earlier today, which seemed to imply that inflationary pressures appear to be easing on the Japanese economy. Lastly, we should note that Japan’s preliminary JibunBK Manufacturing PMI figure is due to be released next Monday and Japan’s Tokyo CPI rate for August is expected to be released next Friday.

EUR – ECB versus Italy

EUR is about to end the week in the reds against JPY, but higher against the dollar and the pound. On a fundamental level, we highlight that according to the Financial Times, billionaire George Soros’s foundation, Open Society Foundations will be scaling back its activity in Europe and will be focusing on other parts of the world. On the monetary front, we note the decision of the Italian Government to impose a 40% windfall tax on banks which rattled markets upon its announcements, has apparently caused friction with Brussels, as according to a Bloomberg report, the ECB is preparing to file a complaint for not being informed in advance of the decision. In the the event that divisions over monetary policy are intensified between members of the bloc, we may see a weakening of the ECB’s decision making in the long run, with a potential less unified approach on combating inflation. On a macroeconomic level, we note the Eurozone’s CPI rates that came in as expected, hinting at easing inflationary pressures in the Euro area in addition to the Eurozone’s revised GDP rate for Q2 which was in line with expectations, coming in at 0.6%. Interestingly the Eurozone’s Industrial production rate on a mom and yoy basis came in higher than expected, which may be considered slightly optimistic for the eurozone. Lastly, we highlight Germany’s producers prices rate due on Monday, the Eurozone’s , Germany’s and France’s Preliminary Manufacturing PMI figures and the Eurozone’s Preliminary consumer confidence figure all on Tuesday. France’s manufacturing business climate figure on Thursday, Germany’s GDP rates for Q2 and IFO figures on Friday.

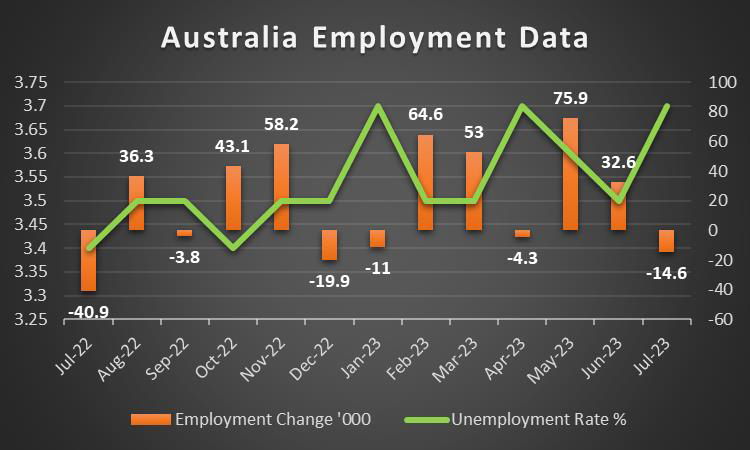

AUD – RBA minutes indicate a credible path to the inflation target

AUD is about to end for a 5th week in a row lower against the USD. On a fundamental level, we note that last week’s fears regarding Australian LNG producers appear to be in fully swing, as workers begin voting to determine if they will go in strike. In the event that LNG workers decide to go on strike it possibly disrupt 10% of the world’s liquified natural gas supply. On a monetary level, we note the RBA’s August meeting minutes which stated that there is a “credible path back to the inflation target with the cash rate staying at its present level”, implying that the bank may be willing to remain on pause in its next meeting, in order to gather data on the restrictiveness of their current monetary policy. On a macroeconomic level, we note the Australia’s wage price index rate for Q2 coming in lower than expected, combined with the country’s employment data indicating a loosened labour market, seem to be weighing on the Aussie. Furthermore China’s worsening trade data, in particular, the reduction in imports by approximately 12.4% could be considered a very worrying sign for the Australian economy in the long run, which is predominantly dependent on Chinese demand for their exports, as such should the economic situation deteriorate in China, deteriorating economic activity with their industrial production rate come in lower than expected, seem to be painting a dire picture for Australia who is predominantly dependent on China for its exports. Lastly, we turn our attention to next week’s financial releases with no major financial releases of interest for Australia, thus the pair may be dictated by financial releases stemming from the US.

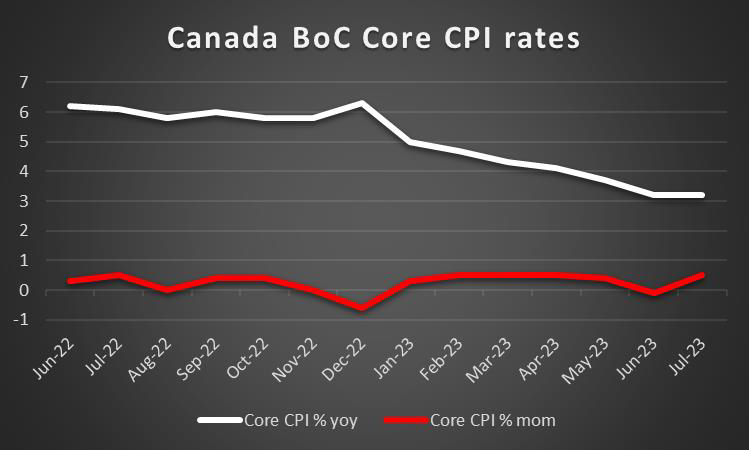

CAD – Canada’s CPI implies persistent inflationary pressures

The Loonie appears to be ending for a 5th week in a row in the reds against the dollar. On a fundamental level, we note the wildfires in Yellowknife, with Reuters reporting that all 20,000 residents are evacuating. On a monetary level, we note major press releases by bank officials, despite recent financial releases and as such the pair might have ceded control to financial releases stemming from Canada or could be driven by the direction of its counterparts. On a macroeconomic level, we note that Canada’s Core CPI comes in higher than expected, implying that inflationary pressures still persist in the Canadian economy and as such, could lead to future implications on the economy. Moreover, given Canada’s status as a major oil producer, the reduction in the price of oil could weigh on the Loonie, as over the past few days the liquid gold has moved in a downwards trajectory given heightened worries regarding China’s economic recovery. Therefore, if there are worries about China’s recovery, given their status as the worlds largest oil importer, Canada could be indirectly affected through lower oil prices. Lastly, we note the lack of financial releases regarding Canada next week, excepted the Retail sales rate for June which is expected to be released on Wednesday.

General Comment

In the coming week we expect volatility in the FX market to increase given the high volume of financial releases which are due next. We also note that the earnings season in the US appears to be slowing down, as most high-profile companies have already released their earnings reports. Nonetheless, we would note BestBuy(#BestBuy) and Baidu (#BIDU) on Tuesday, NVIDIA (#NVIDIA) on Wednesday and Opera (#Opera) on Thursday are expected to release their earnings. As for gold’s price, we note its continued decline over the week as the USD remained elevated with some US yields reaching 15-year highs. As a reminder the BRICS summit is due next Tuesday. On a more fundamental level, we highlight that tensions between China and it’s western counterparts, appears to be heating up. In addition the current situation in China is deeply troubling. In our opinion, the removal of the youth unemployment figure by the Chinese Government may be indicative of a much worse economic situation that what is already being presented.

اگر در مورد این مقاله سوال یا نظر ی کلی دارید، لطفاً ایمیل خود را مستقیماً به تیم تحقیقاتی ما بفرستیدresearch_team@ironfx.com

سلب مسئولیت:

این اطلاعات به عنوان مشاوره سرمایه گذاری یا توصیه سرمایه گذاری در نظر گرفته نمی شود ، بلکه در عوض یک ارتباط بازاریابی است. IronFX هیچ گونه مسئولیتی در قبال داده ها یا اطلاعاتی که توسط اشخاص ثالث در این ارتباطات ارجاع و یا پیوند داده شده اند ندارد.