With the week nearing its end, we note that the US Core PCE rates have yet to be released and no deal at this point in time has been reached to avoid a US Government shutdown, which could occur on Sunday. On a monetary level, we note that the BOJ is due to release its summary of opinions of its September monetary policy meeting on Monday, in addition to the Riksbank which is also due to release its September monetary policy meeting minutes on Monday, as well. In regard to financial releases, we make a start on Monday with Australia’s final Judo bank manufacturing PMI figure for September, Japan’s Tankan big manufacturing index figure for Q3, Germany’s HCOB Manufacturing PMI figure for September, the UK’s final manufacturing PMI figure, Canada’s manufacturing PMI, the US S&P Final manufacturing PMI figure and the US ISM Manufacturing PMI figure all for the month of September. On Tuesday, we note Australia’s building approvals rate for August, Switzerland’s CPI rates for September and the US JOLTS Job openings figure for August. On Wednesday, we make a start with France’s Services PMI figure for September, the Eurozone’s Final composite PMI figure, the UK’s Final composite figure, the US ADP National Employment figure and the US final composite PMI figure all for the month of September, followed by the US factory orders rate for August and the US ISM Non-Manufacturing PMI figure for September. On Thursday, we note Australia’s trade balance figure, Germany’s export rate which are both for the month of August, followed by the UK’s composite PMI figure for September, the US weekly initial jobless claims figure and Canada’s trade balance figure for August. Finally, on Friday we note Germany’s industrial orders rate for August followed by the UK’s Halifax house prices rate for September, the US Non-Farm Payrolls figure, the Unemployment rate , Average hourly earnings and Canada’s Employment data all for the month of September.

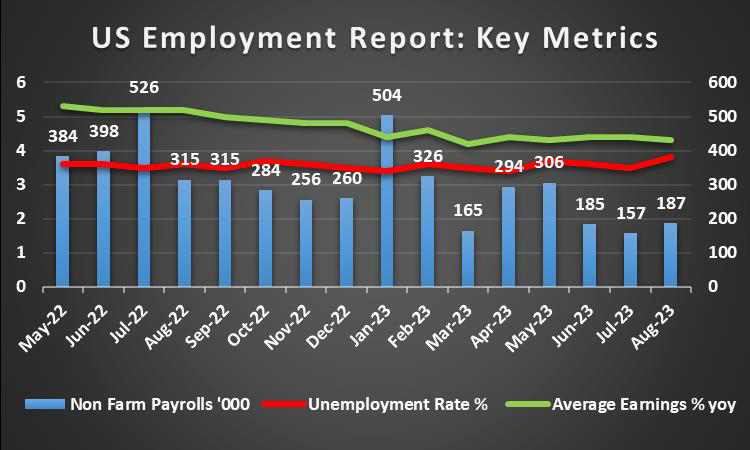

USD – US Employment data in focus

The USD is about to end the week stronger against the EUR,and the JPY but relatively unchanged against the pound. On a fundamental level, we highlight that the US Government is facing the very real possibility of shutting down and at this point in time no deal has been reached to avoid a government shutdown which has been touted to be as early as October 1st which is this Sunday. On a monetary level, we highlight that Minneapolis Fed President Kashkari stated on Thursday that “we might not be as restrictive as we think” , implying that the bank may have to raise rates higher. Furthermore, Chicago Fed President Goolsbee on Thursday, hinted that he may be willing to consider another rate hike if there is a lack of progress on the price side. Therefore, supporting the theory that the Fed may need to raise rates at least one more time before the end of the year

and as such, we may see the greenback gaining against its counterparts. On a macroeconomic level, we highlight that the US weekly initial jobless claims figure came in lower than expected, hinting at a resilient labour market in the US economy. Furthermore, the increase in the US core durable goods orders rate, which was released on Wednesday, may have indicated a resilient consumer market, which in combination with the weekly initial jobless claim figure may have supported the dollar. However, other financial releases such as the real consumer spending rate for Q2 came in at 0.8% which was significantly lower than last quarters rate of 4.2% , in addition, the pending home sales rate for August came in at -7.1% compared to the previous month’s rate of 0.5%. The two aforementioned financial releases, tend to paint a different picture for the US economy, implying that the consumer base of the US, may not be able to withstand further rate hikes, which could weigh on the dollar. Therefore, we turn our attention to the Core PCE rates for August which are due to be released later on Today, which is the Fed’s favourite tool for measuring inflationary pressures. In conclusion, we note the greenback’s strengthening at the end of the week, yet traders may be awaiting the US PMI figures and the US Employment data which may provide greater insight into the resilience of the US economy.

GBP – GDP rates for Q2 indicate a resilient UK economy

The pound seems to be ending the week lower against the EUR, slightly stronger than the JPY and relatively unchanged against the dollar. On a fundamental level, we note Prime Minister Sunak on Wednesday announceed a reversal on his climate change policy, by announcing that the ban on the sale of oil and liquid petroleum gas will be pushed back to 2035. On a monetary level, we highlight that BoE is set to create a pernament lending facility for non-bank financial insitutions such as , insurers and pension funds during times of stress according to a report by FT. The creation of a pernament lending fascility is aimed at stabilizing the financial system as a whole according to bank officials, yet we tend beg the question, as to how the UK Government will prevent the potential exploitation of this system by “bad actors”. In our opinion, the creation of a pernament lending fascility, despite its good intentions, may be abused and exploited by these “bad actors” and as such from a more long term view, it may generate issues for the UK economy and Government. On the other hand, it could increase stability and generate increased consumer confidence in the UK eocnomyover the long run. On a macroeconomic level, we note the GDP rates for Q2 which came in earlier today, implied that the UK economy grew, at a greater degree than what was previous anticipated, as the rate came in at 0.6% versus the expactation of 0.4%, which may support the pound. In conclusion, the pernament lending fascility could either support or weigh on the pound depending on the checks and balances imposed, whilst the GDP rate on the other hand appears to be providing a positive sign for the UK economy. The better than expected GDP rate may have aided to the pounds rise, whilst the effects of the proposed pernament lending fascility have yet to be seen. Lastly, traders may be looking at the UK’s PMI figures which are due to be released next week in order to gauge how the economy has faired, in light of the persistent inflationary pressures and high interest rate levels imposed by the BOE.

JPY – CPI rates send mixed signals

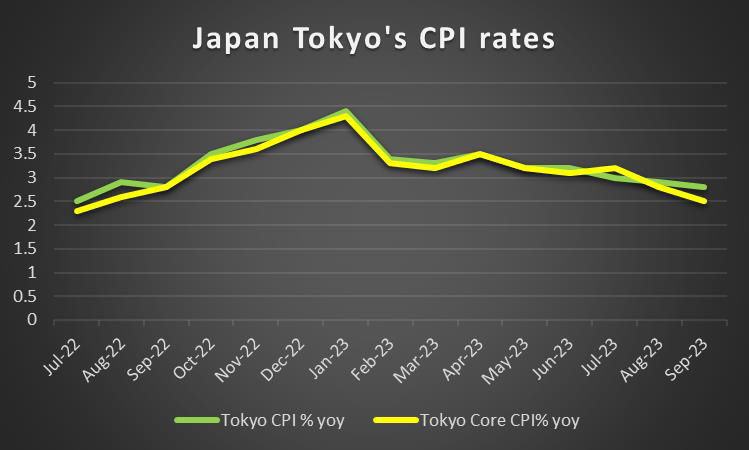

The JPY is about to end the week weaker against the dollar, and the pound but relatively unchanged against the EUR. On a fundamental level, we note that according to Bloomberg, US and Japanese officials are warning that a group of China linked hackers are targeting companies based in the US and Japan, despite no malicious activity at this time, should major financial companies in Japan be compromised, we may see the JPY weakening, as the stability of the Japanese financial industry could be brought into question. On a monetary level, we note BOJ Governor Ueda, stated on Monday that the bank’s “basic stance is that we must patiently maintain monetary easing”, implying that the bank may not be abandoning its ultra loose monetary policy anytime soon. Furthermore, the BOJ’s July meeting minutes hinted that the bank may continue with its ultra loose monetary policy, with the banks members anticipating that the Japanese economy is on track to recover moderately for the time being and as such could potentially weaken the JPY.On a macroeconomic level, the BOJ’s Core CPI rates which was released earlier on this week, indicated an increase in inflationary pressures in the Japanese economy, potentially aiding to the banks objective to reach its 2% inflation target. Yet, the Tokyo Core CPI rates contradict that view, as they were indicative of easing inflationary pressures in the economy after coming in lower than expected. The lower-than-expected rates could hinder the bank’s objective of reaching its 2% inflation target. In conclusion, despite the JPY seemingly being poised to further weaken, we must note that, the last time the JPY dropped to such levels, we saw a government intervention in order to safeguard the JPY and as such, in our opinion, may happen again. Thus, should such a move occur, we may see the JPY gaining against its counterparts. On the other hand, should we see no government intervention we may see the JPY weakening. Lastly Yen traders may be interest in the release of the bank’s summary of opinions for its September meeting, which are due to be released on Monday.

EUR – Eurozone’s PMI figures in focus

The EUR is about to end the week in the reds against the USD the pound and the JPY. On a fundamental level, we note the escalating tensions between the EU and China, with the EU announcing a probe into the subsidies received by EV companies exporting to Europe. The probe is meant to prevent unfair competition which may be experienced by Chinese EV makers who export their cars to the EU who are the accused receivers of such subsidies. On the monetary front, we note the speech by ECB Holzmann who stated yesterday that “It is unclear whether we’re at peak rates yet” implying that the bank may have not reached its terminal rate , yet ECB President Lagarde who stated earlier on in the week that “ rates have reached levels that, maintained for a sufficiently long duration, will make a substantial contribution to the timely return of inflation to our target”. Despite the contradicting views, they both appear to agree that the interest rates may remain at current levels for a prolonged period of time, which could support the EUR in the long run.On a macroeconomic level, a different story emerged, with Germany’s and France’s Preliminary CPI rates for September. The CPI rates for France and Germany came in lower than expected, hinting at easing inflationary pressures in Europe’s largest economies. As such, the lower-than-expected CPI rates, could weaken the case for future rate hikes , which could weigh on the EUR. Lastly, traders may be looking forward to next week’s PMI figures for the Eurozone, Germany and France in order to gauge the impact of the current interest rates on the Euro area. In the event that PMI figures come in higher than expected, we may see the EUR gaining support as it may indicate persistent inflationary pressures in the economy and vice versa.

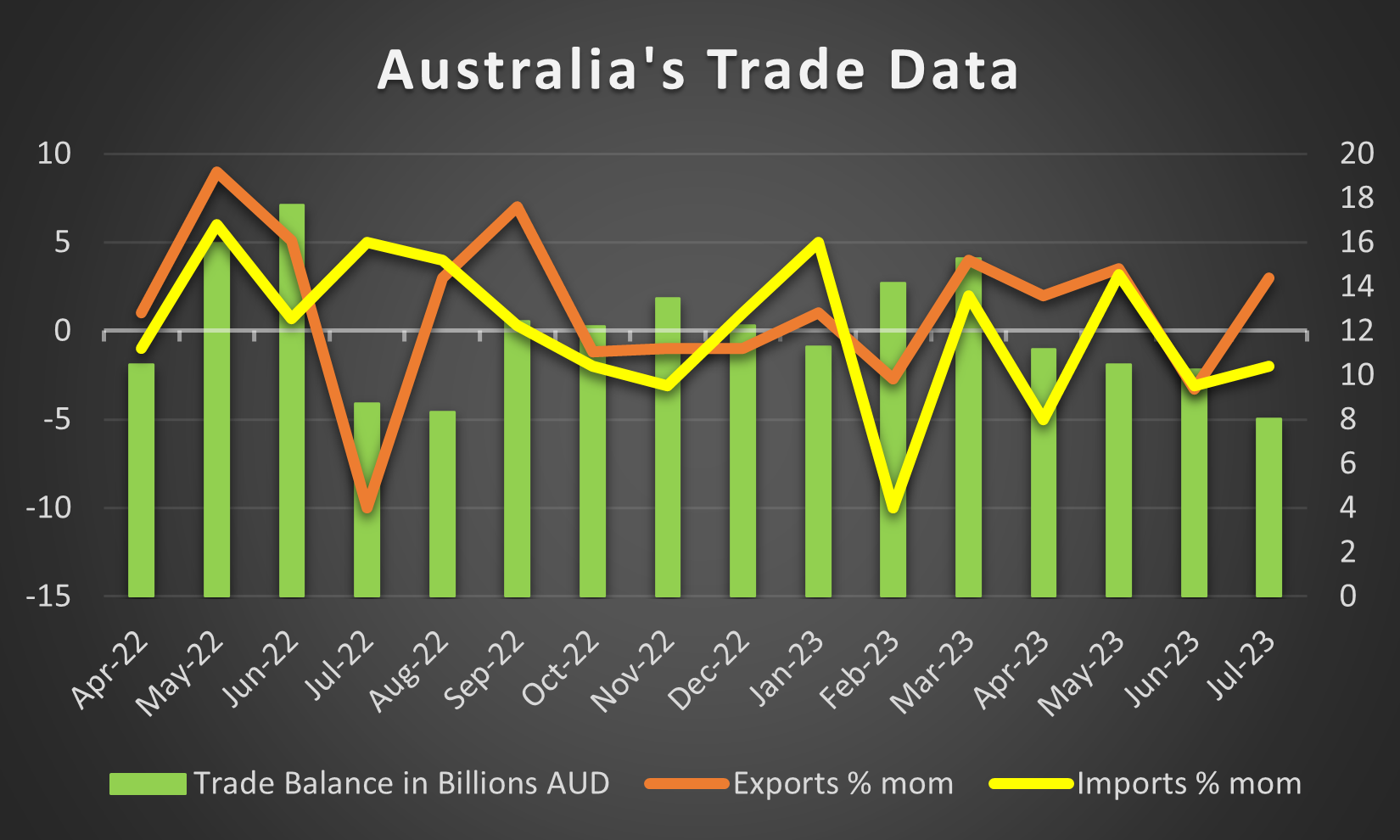

AUD – RBA interest rate decision in sight

AUD is about to end the week stronger than the USD. On a fundamental level, we highlight the agreement reached between France and Australia on the creation of stable supply chains for critical raw materials, further enhancing the co-operation between the bloc and Australia. In the long term, the increased co-operation could boost the Aussie, as it may reduce its dependence on China for its exports, therefore being less exposed to volatility stemming from China. On another fundamental issue, China’s embattled property developer Evergrande, is facing serious questions about its future, following report that the company’s CEO was under police surveillance. Should China’s property market woes continue and spill over into the nation’s manufacturing activity, we may see a weakening in the Aussie, due to the country’s overreliance on China for its exports. On a monetary level, we note that the RBA’s interest rate decision is due next week, with market participants widely expecting the bank to remain on hold with AUD OIS currently implying a 90.87% probability for such a scenario to materialize. We tend to agree with the general market consensus that the bank may remain on hold during their meeting next Tuesday as the risks posed by China are still elevated in our opinion. Therefore, we may see the Aussie weakening. On the other hand, should the RBA take the markets by surprise and hike, we may see the Aussie gaining support. On a macroeconomic level, we note a relatively quiet week for Australia in terms of financial releases once again. Yet, we note Australia’s preliminary retail sales rate for August, came in lower than expected at 0.2%, implying that the Australian consumer may have less disposable income, or is less willing to spend. In the event that economic activity declines, we may see the Aussie weakening. Looking at next week, we highlight the Judo Bank manufacturing PMI figure for September and Australia’s trade balance figure for August, which may be of interest to market participants.

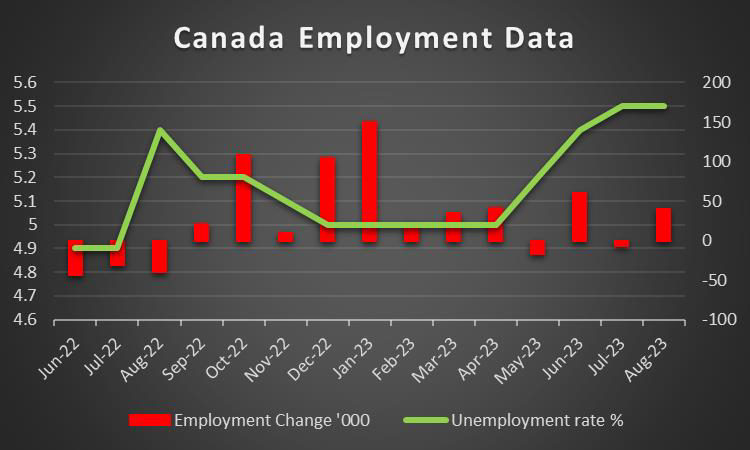

CAD – Canada’s Employment data due out next week

The Loonie is on track to finish the week relatively stronger against the greenback. On a fundamental level, we note that after Prime Minister Trudeau’s accusation of India of being involved in the assassination of a Canadian Sikh activist, on Canadian soil, it appears that tensions are escalating, with media outlets reporting on Thursday evening, that Indian hackers took down the website of Canada’s army. On another fundamental note, CAD traders may be keeping a close eye on oil prices which are moving closer and closer to the $100 bpd touted by market analysts as being a potential target for the commodity. Yet at the time of this report, it appears that oil’s ascent may have been temporarily halted. Nonetheless, should oil prices regain their upwards momentum we may see some support for the Looney, given Canada’s status as a major oil-producing nation. On a monetary level, we note the Canadian senate has proposed Bill S-275, which proposes the establishment of a monetary policy committee consisting of independent members who would be responsible for setting interest rates. In addition, the proposed bill would mandate the bank to publish a cost-benefit analysis of its interest rate adjustment on a yearly basis. The proposal is anticipated to fail to pass yet underscores the rising tensions about the BoC’s interest rate policy and any hindering to the current status quo, could in our opinion weaken the Loonie, as market volatility could be translated to the FX markets . On a macroeconomic level, we note that Canada’s preliminary GDP rates for July have yet to be released at the time of this report. However, market participants are anticipating that the GDP rate will come in higher than the previous month, as such should that be the case, we may see the Loonie gaining against the dollar, whilst should it come in lower than expected, we may see the Loonie weakening. In our opinion however, based on the rise of oil prices in the past few weeks, we anticipate that the GDP rates may come in higher than expected, potentially providing support for the Loonie. Lastly, traders may be interested in the financial releases stemming from Canada next week, with the manufacturing PMI figures for September, Canada’s trade balance figure and on Friday the Canadian employment data.

General Comment

In the coming week, we expect higher volatility in the FX market due to the higher number of PMI figures which are expected to be released during next week. We also note that in the US equities markets, all three major indexes appear to be continuing their downwards trajectory as the week nears its end, possibly also due to the uncertainty created by a possible US government shutdown. As for gold’s price, we note that it appears to be ending the week below the key psychological figure of $1900, yet with the possibility of a US government shutdown, it could potential edge higher. Furthermore, we note that Oil’s price appears to be losing some momentum after aiming for the $100 dollar per barrel figure, which has been touted as a potential target by market analysts. Lastly, the higher-than-expected reduction in US oil inventories during the week, combined the OPEC+ production cuts being extended until the end of the year, appear to be forming a long-term view, of elevated oil prices. In addition, the US Strategic Petroleum reserve is near all-time lows, with the current inventories nearing levels last seen in 1983, which could hinder the ability of the US government to influence oil prices by increasing the supply of oil in the market. Therefore, potentially ceding control to OPEC+ and its members.

اگر در مورد این مقاله سوال یا نظر ی کلی دارید، لطفاً ایمیل خود را مستقیماً به تیم تحقیقاتی ما بفرستیدresearch_team@ironfx.com

سلب مسئولیت:

این اطلاعات به عنوان مشاوره سرمایه گذاری یا توصیه سرمایه گذاری در نظر گرفته نمی شود ، بلکه در عوض یک ارتباط بازاریابی است. IronFX هیچ گونه مسئولیتی در قبال داده ها یا اطلاعاتی که توسط اشخاص ثالث در این ارتباطات ارجاع و یا پیوند داده شده اند ندارد.