An eventful week is slowly coming to an end, with next week set to cause waves in the markets. In the coming week, on the monetary front, we highlight the release of the Riksbank’s May monetary policy meeting minutes on Wednesday. As for financial releases, we make a start on Monday with the release of the Czech Republic’s CPI rates for April. On Tuesday, we get Japan’s Corporate Goods Prices rate, Germany’s final HICP rate both for April, followed by the UK’s ILO Unemployment rate, Average weekly earnings and employment change figure for March and the HMRC Payrolls figure for April, later on we get the Eurozone’s current economic sentiment figure, Germany’s ZEW economic sentiment and current conditions figures all for May and ending off is the US PPI Machine manufacturing figure for April. On Wednesday, we get Japan’s Machinery orders rate for March and Chain store sales rate for April, Sweden’s CPI rate and France’s final HICP rate for April, followed by the Eurozone’s Preliminary GDP rates for Q1 and Industrial production rate for March, the US CPI rates for April, followed by the US retail sales rate for April and ending off the day is Canada’s Manufacturing sales rate for March. On Thursday we get Japan’s GDP rates for Q1, Australia’s Employment data for April, Norway’s GDP rate for Q1, the US weekly initial jobless claims figure, the US Philly Fed Business index for April and the US Industrial production rate for April. Lastly on Friday, we note China’s retail sales and urban investment rates, and the Eurozone’s final HICP rate, all for the month of April.

USD – CPI readings to move the greenback

The USD is about to end the week relatively unchanged against its counterparts, after a relatively quiet week in terms of financial releases. We note that the USD may have gained some momentum on the heel of Fed policymakers who may have influenced the currency’s direction with their comments during the week. In particular, Minneapolis Fed President Kashkari who stated that “the bar for a rate hike is quite high but it’s not infinite”, implying that the bank may soon be faced with a decision as to whether or not to hike interest rates. The possibility of a rate hike by the Fed, may provide support for the greenback. Yet, it should be noted that despite not being a voting member this year, Minneapolis Fed President Kashkari is still considered to be influential in the Fed’s decisions. On the flip side, Richmond Fed President Barkin, New York Fed President Williams and Boston Fed President Collins, implied that the current

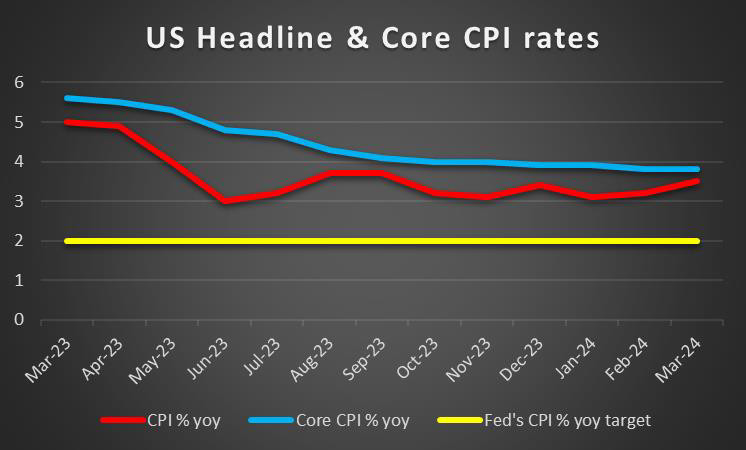

monetary policy is restrictive, thus contradicting the possibility of a rate hike by the Fed. Overall, with the narrative of rate cuts having been replaced with the rhetoric of maintaining interest rates higher for longer, it appears that market participants have perceived this shift as a “relatively hawkish” indication by Fed policymakers, thus potentially aiding the dollar. On a macroeconomic level, we note the Preliminary University of Michigan consumer sentiment is set to be released later on today and could potentially weigh on the dollar. Specifically, the preliminary consumer confidence figure for May is expected to decrease from 77.2 to 76.3, implying that consumer confidence in the US economy might be decreasing. On the contrary the Atlanta Fed GDPNow preliminary rate for Q2 which was released this Wednesday came in higher than expected at 4.2% versus the expected rate of 3.3%, thus implying that the US economic expansion not only grew but also accelerated, which supported the dollar following it’s release, which may overshadow the expected reduction in consumer confidence in the US economy. Next week, we would highlight the release of the US CPI rates for April, as a gauge of inflationary pressures in the US economy, where a higher-than-expected reading could support the dollar, as it may encourage the Fed to maintain its restrictive monetary policy stance and vice versa.

GBP – BoE keep’s rates steady

The pound is about to end the week unchanged against the USD,whilst gaining ground against the JPY and losing against the EUR. On a fundamental level, we note that following the loss of a seat in the House of Commons, for the Tories, a new poll released by YouGov shows the Labour Party leading the polls in a general election at 44% compared to the Conservatives at 18%, which could weigh on the pound, as political uncertainty could arise. On a monetary level, a rift appears to be emerging between BoE policymakers, as following the bank’s interest rate decision on Thursday, the number of policymakers who voted for a cut was 2 instead of the anticipated 1. As such, despite the bank maintaining interest rates at their current levels as it was widely expected, the divergence in the number of allocated votes appears to be weighing on the pound. In the bank’s accompanying statement, the BoE stated that “CPI inflation is expected to return to close to the 2% target, but to increase slightly in the second half of this year, to around 2 ½ %”. Therefore, it could be inferred that inflation is nearing the bank’s 2% inflation target and that it may be appropriate to begin easing the bank’s restrictive monetary policy stance. Furthermore, this stance appears to be in play following BoE Governor Bailey’s press conference following the bank’s decision in which he stated that a “June bank rate cut is not ruled out or planned”, implying that the bank may be preparing to cut interest rates earlier than

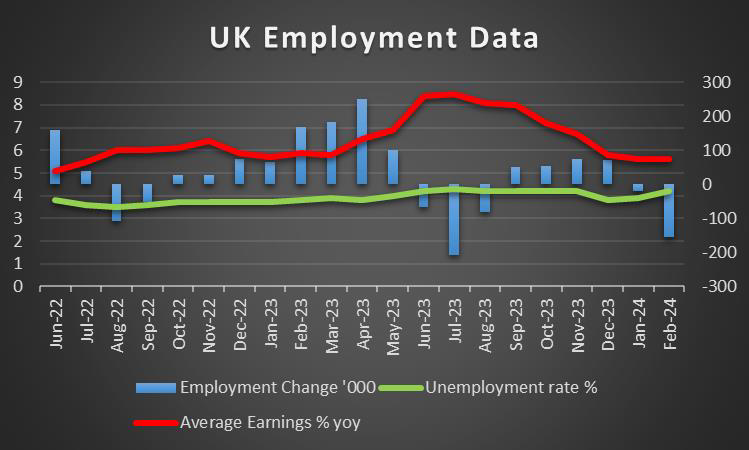

expected, which may weigh on the pound. On a macroeconomic level, we note the release of the preliminary GDP rate for Q1 earlier on today. Despite the preliminary GDP rates coming in higher than expected, managing to escape negative territory, implying the UK economy escaped the technical recession it was in. Hence, some optimism for the UK economy appears to have emerged, which may alleviate some of the downward pressures faced by the pound this week. For next week, we highlight the UK’s employment data for March and April, in which should both releases imply a resilient UK labour market, it could provide support for the pound, despite being readings for two different months. On the flip side, an implication of a loosening labour market could weigh on the pound, as pressure on the BoE to cut interest rates earlier than expected may increase.

JPY – Japan’s support for JPY shortlived?

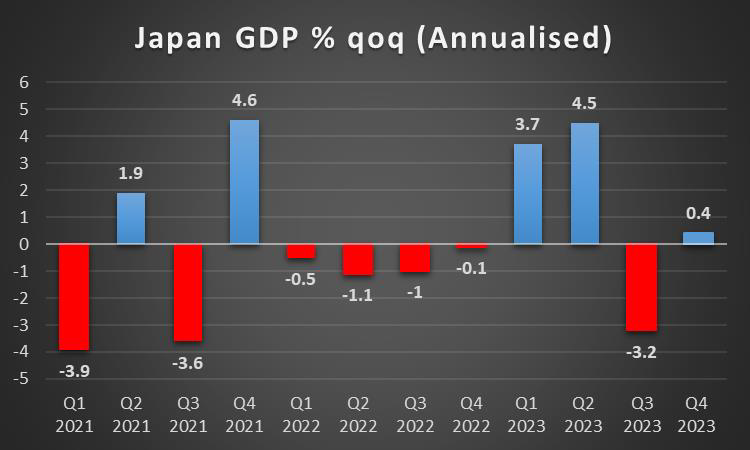

JPY is about to end the week weaker against the USD, the GBP and the EUR, in a sign of wider weakness. The weakening of the JPY may be stemming from market participants, doubting the oral warnings about another Government intervention in support of the JPY. Furthermore, it could be extrapolated from the JPY’s weakness that market participants may not be convinced that the BOJ’s current monetary policy rate is restrictive enough. As such with USD/JPY aiming for the 160 ceiling upon which the Government intervened last week, we would not be surprised to see another intervention by the Government should the Yen continue to weaken. Moreover, the USD/JPY’s rise could also be attributed to a strengthening dollar, yet that alone may not account for the Yen’s widespread weakening against other major currencies. On the flip side, according to the WSJ, BOJ Governor Ueda on Wednesday stated that he is open to the idea of early interest-rate increases if inflation rises at a faster pace than the bank’s projections, which may provide support for the Yen. However, market participants may want to see an actual commitment by the BOJ in terms of monetary policy decisions rather than hypothetical scenarios, in order to be convinced. Hence for now, we would not be surprised to see the Yen to continue to weaken, with some Government interventions along the way until the bank’s next monetary policy meeting. On a macroeconomic level, we would like to note Japan’s GDP rate for Q1 which is due out next Thursday. Should the GDP rate come in higher than the previous quarter’s reading, hence implying an expansion in the Japanese economy at a faster pace, it could provide some leeway for the BOJ to accelerate their monetary policy normalization by potentially increasing interest rates at a greater pace than what is expected, thus potentially providing support for the JPY.

EUR – Eurozone Preliminary GDP rate next week

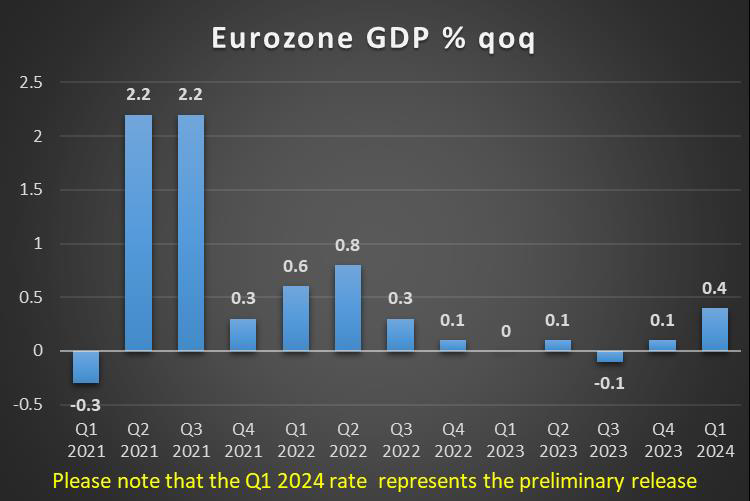

The EUR is about to end the week in the greens against the USD, the pound and JPY, in a sign of wider strength. On a fundamental level, we note the meeting between France’s President Macron and China’s President Xi Jinping who earlier on this week broke protocol according to France24, by taking a trip to the Pyrenees trip for a chance for a one-on-one meeting. Overall an improvement of the Sino-EU trading relationships could support the common currency and vice versa. On a monetary level, we note the comments made by ECB member Nagel on Tuesday who according to Reuters stated that the ECB cannot be lenient with structural inflationary forces, implying that the ECB may need to adopt a more restrictive monetary policy stance. Thus, should more policymakers re-iterate the need for a continuation in the bank’s restrictive monetary policy stance to continue further than the market’s expectations of a June rate cut with two or maybe three rate cuts by the end of the year, it could support the EUR. On a macroeconomic level, we note that some positive indication for the Eurozone appear to have emerged in terms on financial releases, earlier on this week. In particular, the Eurozone’s composite PMI figure for April came in better than expected, in addition to France’s services and composite PMI figures for April having also exceeded expectations, appear to have sent a positive image about the Eurozone’s economy. A view also highlighted by the Eurozone’s Sentix consumer sentiment figure for May which despite being a month ahead, shows an improved sentiment by consumers for the Eurozone’s economic outlook. However, the economic powerhouse of Europe which is Germany appears to be contradicting that view. Specifically, Germany’s factory orders rate for March failed to reach expectations of an increase of 0.4% and came in lower at -0.4% implying a further reduction in demand for manufactured goods, which could dampen the aforementioned view. Nonetheless, traders may now be eyeing the Eurozone’s preliminary GDP rates for Q1 next week. Should the preliminary GDP rates come in lower than the prior reading, hence implying a potential slowdown in economic growth it could weigh on the EUR and vice versa.

AUD – RBA remains on hold

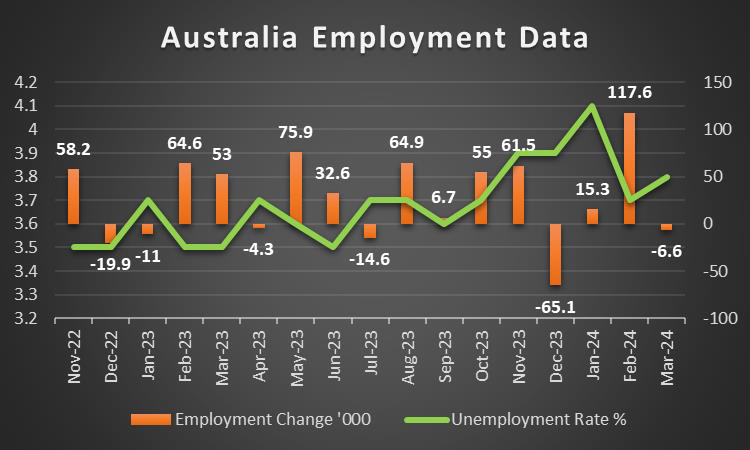

The Aussie is about to end the week relatively unchanged against the USD. On a fundamental level, we note that the Aussie as a commodity currency seems to be more sensitive to the overall market sentiment. Hence a possible more risk-oriented approach by the market could provide some support for the AUD and vice versa. Also, we note the sensitivity of the Aussie to developments in the Chinese economy, given the close Sino-Australian economic ties. Hence, China’s better-than-expected trade data for April appears to have provided support for the Aussie, as China’s import growth rate, accelerated to 8.4% versus the prior rate of -1.9%, which may imply more exports of Australian raw materials to China. On a fundamental level, we note the geopolitical tensions surrounding China. The US Government seems to be preparing to impose tariffs on China and media report that it may happen as soon as next week. The new tariffs are expected to focus on industries including electric vehicles, batteries and solar cells, with existing levies largely being maintained. Overall the tensions in the US-Sino relationships on a trading level, may turn the market sentiment more cautious thus weighing on riskier assets such as commodity currencies and especially the Aussie. On a monetary level, we highlight the release of RBA’s interest rate decision on Tuesday in which the bank remained on hold, as it was widely expected. The bank in its accompanying statement also highlighted that the outlook remains uncertain and stressed that returning inflation to target is the highest priority. As for forward guidance, RBA stated that “The path of interest rates that will best ensure that inflation returns to target in a reasonable timeframe remains uncertain and the Board is not ruling anything in or out, and remain data dependent”. Despite the tone of the accompanying statement being rather hawkish the Aussie seems to have lost ground at the release as the market seems to have been expecting more. Furthermore, RBA Governor Bullock appears to have tweaked the bank’s hawkishness, as she stated that “rates are at the right level to get inflation back to target” which may imply easing monetary policy and thus may have weighed on the Aussie. On a macroeconomic level, we note the release of the retail trade growth rate for Q1 which came in lower than expected, implying a reduction of the demand side of the Australian economy. However, we should note that the RBA’s interest rate decision and the retail trade growth rate were released before China’s trade data and thus appear to have been overshadowed by the aforementioned increase in the imports rate. The next hurdle for Aussie traders may be the release of Australia’s Employment data for April next Thursday. Should the data imply a resilient labour market, it could provide some leeway for the RBA to maintain its restrictive monetary policy, which may support the AUD and vice versa.

CAD – April Employment data due out today

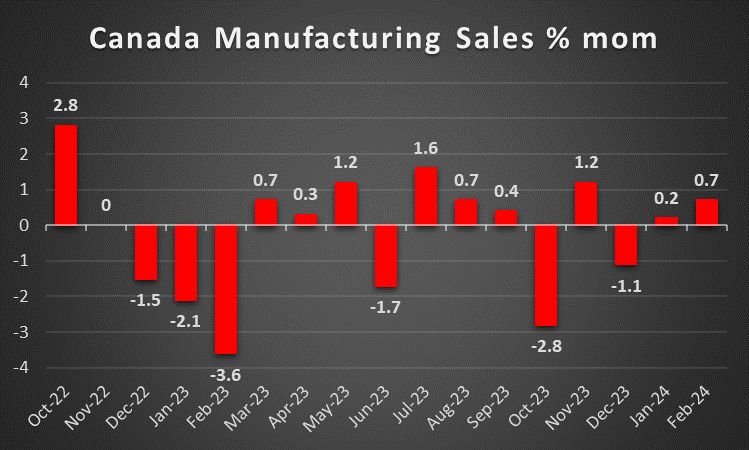

The CAD is about to end the week at the same levels it began, against the USD. On a macroeconomic level, we note the improvement of Canada’s Ivey PMI figure for April, implying an increase in manufacturing activity which appears to have provided some short-lived support for the Loonie. We note that the time of this report, Canada’s employment data for April has yet to be released. Thus, should the data imply a continuance of the slack in the Canadian employment market as reported for March, it could weigh on the CAD substantially. At a monetary level, we note the comments made by BoC Governor Macklem who during his testimony to Canada’s financial committee stated that the Government’s spending has not been helpful in easing inflationary pressures in the economy. As such, should the Canadian Government increase spending, it could indirectly impact the bank’s monetary policy approach and may tilt the narrative towards the hawkish side which may provide support for the Loonie. On a more fundamental level, we note that a possible improvement of the market sentiment could provide some support for the Loonie, given also its status as a commodity currency. Also, we note the sensitivity of the Loonie to oil prices, given Canada’s status as a major oil-producing economy. Oil prices for the week seem to have risen slightly yet did not escape their downward trajectory. Should they continue to improve in the coming week we may see some support for the Loonie building up.

General Comment

In a more general note, we expect the USD to reacquire some of its initiative in the FX market as the gravity and frequency of US financial releases seem to be increasing. Overall though we have to note that volatility may ease somewhat should there be no surprises, as we have a rather busy calendar next week. As for US equities, we note that US stock markets are about to end the week in the greens for a third week in a row, in a sign of a more risk oriented market sentiment. A number of high-profile companies released their earnings reports, yet in the coming week, we note that the release of the earnings reports of Alibaba (#BABA), HomeDepot (#HD), Cisco Systems (#CSCO), JD Inc (#JD), Baidu(#BIDU) and Walmart (#WMT) could catch the market’s eye. On the fundamentals of US stock markets should Fed policymakers continue to stress the possibility of the Fed maintaining rates high for longer, the market sentiment could turn more cautious thus weighing on US stock markets. Furthermore, we note that gold’s price is rising despite the relative inactivity of the USD, underscoring the absence of the negative correlation of the USD with the precious metal in the past few days. Hence we turn our attention to the decline of US bond yields the past few days, which may have made them unappealing for investors and thus may have provided some support for the precious metal’s price.

Si vous avez des questions d'ordre général ou des commentaires concernant cet article, veuillez envoyer un email directement à notre équipe de recherche à l'adresse research_team@ironfx.com

Avertissement :

Ces informations ne doivent pas être considérées comme un conseil ou une recommandation d'investissement, mais uniquement comme une communication marketing. IronFX n'est pas responsable des données ou informations fournies par des tiers référencés, ou en lien hypertexte, dans cette communication.