With a chorus of hawkish central banks coming to an end we open a window at what next week has in store for the markets. In regards to monetary policy we note from Sweden Riksbank’s interest rate decision on Thursday and the release of BoJ’s summary of opinions for the June meeting on Tuesday, while ECB is to hold its annual forum at Sinta, Portugal, with key speakers including ECB President Lagarde, BoE Governor Bailey and Fed Chair Powell. As for financial releases we make a start with Germany’s Ifo indicators for June and UK’s CBI distributive trades indicator for the same month. On Tuesday, we get from the UK the nationwide house prices for June, the US durable goods orders for May, Canada’s CPI rates for May and the US consumer confidence indicator for June. On Wednesday we note the release of Germany’s forward looking GfK consumer sentiment indicator for July, while on Thursday we note the release of Australia’s retail sales growth rate for May, Eurozone’s economic sentiment for June, the US weekly initial jobless claims figure and highlight Germany’s preliminary HICP rate for June and the US final GDP rate for Q1. Finally, in a packed Friday we note the release from Japan of Tokyo’s CPI rates for June and preliminary industrial output for May, from China we get the NBS Manufacturing PMI figure for June, UK’s GDP rate for Q1, France’s and the Eurozone preliminary HICP rate for June, Switzerland’s KOF indicator for the same month, the US the consumption rate and the core PCE price index both for May, Canada’s GDP rate for April and we end the end with the final University of Michigan consumer sentiment for June from the US.

USD – Fed’s hawkishness maintained

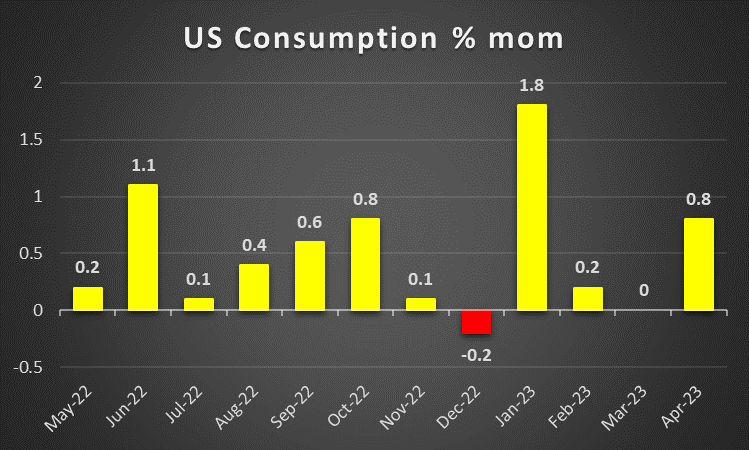

The USD seems about to end the week on the front foot against its counterparts ending a losing streak of three weeks. We must note that the greenback gained retreated favoured also by the Fed’s hawkishness. It was characteristic that Fed Chairman Powell in his testimony before Congress on Wednesday more or less confirmed that more rate hikes lay ahead and stated that “Inflation pressures continue to run high, and the process of getting inflation back down to 2% has a long way to go,”. Furthermore, he reiterated that all FOMC policymakers expect that “it will be appropriate to raise interest rates somewhat further by the end of the year”, contradicting market expectations for rate cuts any time soon at the same time. The Fed Chairman cited the US employment market as being still tight despite some signs of easing. Overall the Fed Chairman maintain a clear hawkish tone in his testimony, yet at the same time did not add something new. Should the bank’s hawkishness be maintained or even elevate to higher levels in the coming week, we may see the USD getting some support. On a more fundamental level, we note the conflicting messages sent on a political level. Despite the initial positive signals coming from US Foreign Secretary Blinken’s visit to China that tensions between the two countries may start thawing or at least may not escalate further, US President Biden calling China’s leader Xi as a “dictator” is not expected to go down well with the Chinese. Further escalations of tensions in the US-Sino relationships may intensify market worries and thus provide support for the USD. Even more worrying may be the market’s intensifying expectations for a possible global economic slowdown, which in turn may feed the greenback safe haven inflows. On a macroeconomic level our worries for the outlook of the US tend to remain despite the rise of the number of House starts for May and thus we highlight the release of the final GDP rate for Q1 on Wednesday, on the inflationary front Mays’ Core PCE price index and on the demand side of the US economy, May’s Consumption rate.

GBP – BoE hikes rates

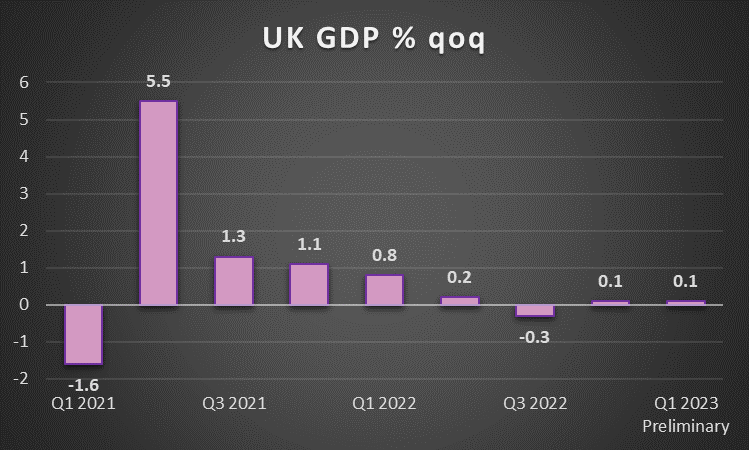

The pound is about to end the week lower against the USD, higher against the JPY yet remains relatively unchanged against the EUR. On a monetary policy level, BoE took the markets by surprise hiking the interest rate by 50 basis points and raising it to 5.00%. In its accompanying statement, the bank cited “ indications of persistent inflationary pressures in the economy” and “the tightness of labor market conditions”. The market maintains the view of more rate hikes to come with the peak being set at 6.25% in 2024. Overall we expect the bank to maintain its hawkish stance and the market’s expectations for more rate hikes to come to be maintained, which in turn may continue to provide support for the pound. On a macroeconomic level, the size of the hike was suspected by the markets and is understandable given that for May the headline CPI rate remained unchanged on a year-on-year level and the core CPI rate even accelerated, showcasing the persistent inflationary pressures in the UK economy. Yet on the other hand, further monetary policy tightening by the BoE may weigh on the economic outlook of the UK and slow down if not even cause a contraction of economic activity and growth. The situation was displayed by the deeper drop of UK’s preliminary manufacturing PMI figure for June, showing an even wider contraction of economic activity in the sector. On the other hand, the services sector seems to be still holding on despite a slowdown of expansion of economic activity in June.

JPY – CPI rates continue to ease

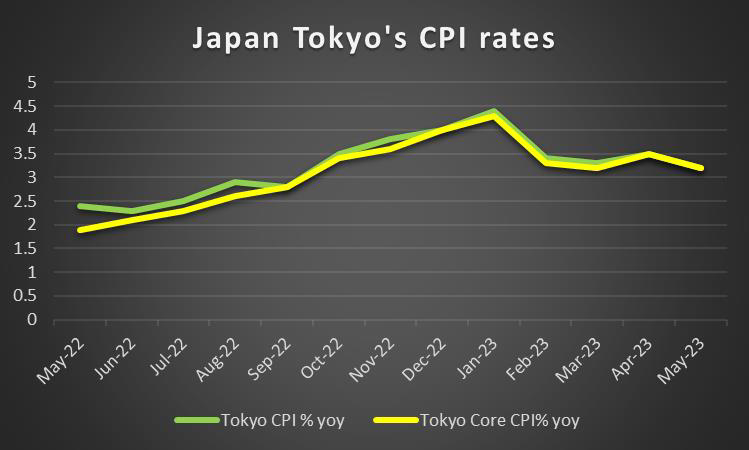

JPY seems to be edging lower against the USD, EUR and GBP in a sign of wider weakness. On a fiscal level, we note Japan Finance Minister Suzuki’s comments that FX stability is important and that FX moves are closely watched. Despite this could constitute a slight market intervention with statements, we see the risk for a substantial market intervention currently as low. On a deeper fundamental level, we continue to highlight JPY’s second nature as a safe haven and note that should we see a risk off market sentiment arising we may see the Japanese getting some support and vice versa. On a monetary level, we note that BoJ is expected to continue to be dovish despite April’s meeting minutes showing that BoJ debated the possible risk of hiking interest rates too late. It’s characteristic that BoJ board member Noguchi stated that wages must keep rising in order for the bank’s inflation target of 2% to be reached. Yet at the same time implied that the ultra-loose monetary policy settings must remain in place to support the Japanese economy and that no operational tweaks to the bank’s yield curve control were required for the time being. BoJ seems to be justified on a macroeconomic level, given the further slowdown of the country’s CPI rates for May. The slow-down may ease further the pressure on the bank to alter its dovish stance and thus could weaken the JPY in the coming week.

EUR – Contraction of economic activity weighing

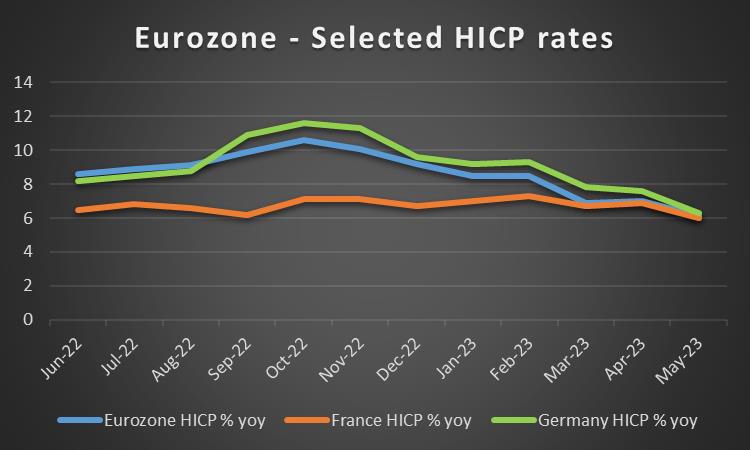

The common currency is about to end the week weaker against the USD yet is gaining ground against the JPY and GBP. On a monetary level, ECB’s hawkishness seems to have been maintained over the past week, an element that may have provided some support for the common currency. ECB Vice President De Guindo’s statements that the slowdown of underlying prices at a core level is still not as pronounced as expected. Such a viewing of inflationary pressures in the Eurozone may force the bank to maintain its hawkish stance thus providing some support for the EUR at the current stage. Hence we highlight the preliminary release of June’s HICP rates for Germany, France and the Eurozone as a whole and should the rates slow down further we may see them weighing on the common currency as they may ease the pressure on the bank eases. It should be noted though that on a producers level inflation contracted even further in May which tended to underscore the possibility of further easing of inflationary pressures at a consumer level for the area. The tightening of the bank’s monetary policy does not come without a cost, as economic activity in the manufacturing sector with a special focus being on Germany, possibly the spearhead of the area’s exports, contracting once again intensifying our worries for the economic outlook of the area.

AUD – The Aussie breaks its three-week winning streak

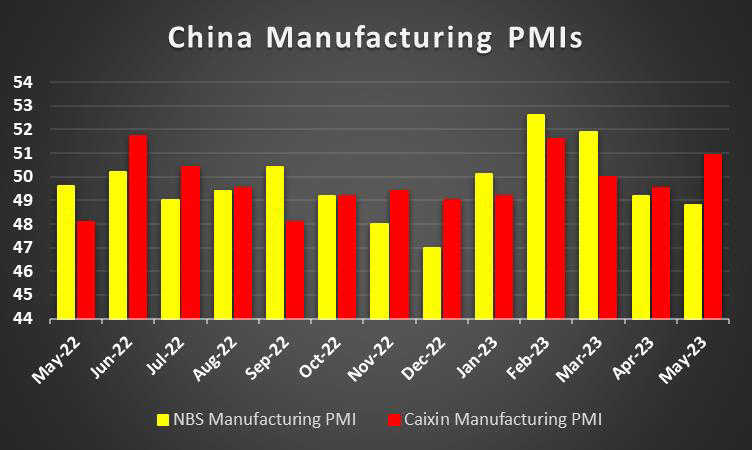

AUD’s three-week winning streak against the USD was abruptly interrupted as the Aussie lost considerable ground. On a monetary level, the release of the June meeting minutes of RBA tended to provide some grounds for the retreat of the Aussie, as the document revealed that the decision for a rate hike was “finely balanced”, thus implying that RBA policymakers were in the limbo on whether to hike rates or not. The release tended to ease our expectations for further rate hikes by the bank. It should be noted though that RBA Deputy Governor Bullock stated that higher rates are the only way for the bank to curb inflationary pressures in the Australian economy, a statement that tended to imply that more rate hikes may be in the pipeline. At this point, we must note again the political pressure exercised on RBA Governor Lowe, as he is up for reappointment. Australian Finance Minister Chalmers seems to prefer, according to local media, Deputy Governor Bullock as his replacement for the time being. On a more fundamental level and given the close Sino-Australian ties, our worries for the headwinds faced by the Chinese economy trying to recover, tend to be maintained. We note that the Central Bank of the People’s Republic of China cut lending rates in an effort to boost activity in the Chinese economy, yet the cuts delivered may not be sufficient to revive it. We expect the release of China’s June NBS manufacturing PMI figure to show whether economic activity in the Chinese giant continues to contract and if so may weaken the Aussie further.

CAD – Canada’s CPI rates in focus

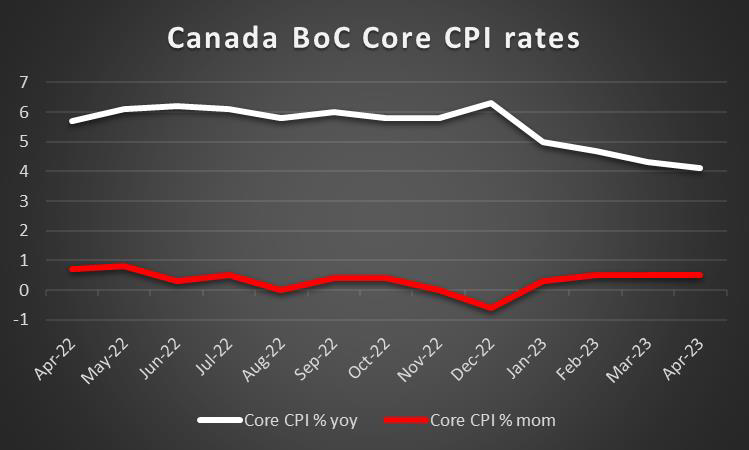

The CAD seems about to end the week in the reds against the USD but just barely. On a monetary level, we note that BoC in its June deliberations was convinced by the “surprisingly resilient consumer spending” that its monetary policy was not sufficiently restrictive and required another rate hike. The bank’s view was reaffirmed on a macroeconomic level, by the acceleration of the retail sales growth rate for April. We would also add to that, the relatively tight Canadian employment market despite the drop of the employment change figure, and the widening of the trade surplus for April, tended to provide some justification for the rate hike. For the time being the market seems to expect another rate hike in the bank’s July meeting and on a monetary level that may provide some support for the CAD. For the time being, we note the release of Canada’s CPI rates next week and a possible acceleration of the rates could provide additional support for the CAD as it may sharpen the bank’s hawkishness, while a possible slowdown could weaken the CAD as it may ease the pressure on BoC. On a more fundamental level, the Loonie is expected to continue to be moved by the market sentiment as a commodity currency and a more risk-on approach of the market could possibly support the CAD. Furthermore, CAD traders should keep a close eye over the course of oil prices given that Canada is a major oil-producing economy. WTI prices seem about to end the week in the reds. Possibly clipping the Loonie’s gains and should the drop be extended into the coming week as well we may see the CAD suffering some losses.

General Comment

In the coming week, we expect volatility to ease somewhat, given that the number of high-impact financial releases is reduced. We also expect that the USD may relent more of the initiative to other currencies allowing for other currencies to shine under the spotlight and thus create an even more balanced blend of trading opportunities in the FX market. As an epilogue, we would like to make a comment on the interest rate decisions released yesterday besides BoE. The Swiss National Bank delivered a 25 basis points rate hike that tended to pass rather unnoticed as it may have been expected by the markets. Norges Bank on the other hand, took the markets by surprise and delivered a 50 basis points rate hike and stated in its forward guidance that more rate hikes lay ahead. The bank’s intentions could continue to provide support to the Norwegian Krona on a monetary level. Finally the big disappointment for exotic currency pairs on Thursday may have been served by the Turkish Central Bank. The bank given the change of leadership was expected to perform a pivot from its previous dovish stance and hike rates considerably, signaling a return to orthodox economic policies. Some analysts even considered that the bank could raise the one-week repo to 21%. Any case, the bank seems to have failed to meet the market’s hawkish expectations as it raised the one week repo rate to 15% from prior 8.5%. The decision may have intensified the market’s doubts about the sincerity of Erdogan’s intentions and thus allowed for the Lira to enter a freefall, with USD/TRY reaching a new record high at 24.5. The decision is understandable in the sense that the bank may not have wanted to raise interest rates too quickly yet it failed to communicate its intentions early on. We expect that the weakening of the TRY may be maintained on Monday unless we see some dramatic moves by the Turkish Government.

Si vous avez des questions d'ordre général ou des commentaires concernant cet article, veuillez envoyer un email directement à notre équipe de recherche à l'adresse research_team@ironfx.com

Avertissement :

Ces informations ne doivent pas être considérées comme un conseil ou une recommandation d'investissement, mais uniquement comme une communication marketing. IronFX n'est pas responsable des données ou informations fournies par des tiers référencés, ou en lien hypertexte, dans cette communication.