The bullish tendencies of S&P 500, Nasdaq and Dow Jones seem to remain present despite some mixed signals being send over the past week. In this report, we are to discuss primarily the fundamentals surrounding US stockmarkets but also the upcoming earnings releases and finish off the report with a technical analysis of S&P 500’s daily chart.

Financial data released and what lies ahead

Before we have a look at what lies ahead in regards to financial releases, we note the easing of inflationary pressures in the US economy during June as the CPI rates tended to slow down for the past month. It’s characteristic that the headline rate slowed down beyond market expectations reaching 3.0%yoy if compared to May’s 3.3%yoy, while prices even contracted on a month-on-month level. On a core level, inflation ticked down enhancing the signal of easing inflationary pressures in the US economy. The release was somewhat contradicted by the acceleration of the PPI rates for the same month somewhat, yet we expect that should there be further signs that inflationary pressures are on the retreat in the US economy we may see US stockmarkets getting some support. Furthermore we note that the demand side of the US economy seems to be resilient as the retail sales growth rates for June came in better than expected, with the core rate even accelerating on a month on month level. Further signs of strong demand in the US economy could add more support for US stockmarkets. Today we note the release of the US industrial production for June and tomorrow July’s Philly Fed Business index. Should the indicators’ readings come in better than expected implying also some resilience for the production side of the US economy we may see US stockmarkets being supported.

The Fed’s stance

The easing of inflationary pressures in June, in conjunction with a cooling of the US employment market for the same period, intensified the market’s current expectations for the Fed to start cutting rates in September and deliver another two rate cuts within the year, one on November and one in December. The intensification of the market’s expectations tends to add more pressure on the Fed to ease its hawkishness, something that may have been implied by Fed Chairman Powell last week. We expect that should more Fed policymakers ease their hawkishness and maintain a more dovish outlook for the Fed’s intentions, we may see US stockmarkets getting additional support. We tend to view the Fed’s monetary policy stance as the key factor behind the direction of US stockmarkets along with the markets’ excitement for the possibilities offered by AI.

The assassination attempt on Trump

On a deeper fundamental level, Saturday’s assassination attempt on former President Trump, may had enhanced uncertainty somewhat, yet that effect calmed down quickly. On the flip side the unsuccessful attempt, seems to have caused a rally around the flag effect for Trump supporters and thus enhanced the possibility for him to get elected. Should market expectations enhance for such a scenario we may see riskier assets such as US stockmarkets getting some support as in parallel, the market’s expectations for the Republicans to return to the White House and deliver tax cuts, could strengthen the optimism of the market.

Worries for China

Our worries for the recovery of the Chinese economy tended to intensify after Monday’s Asian session, as a number of Chinese data released, were alarming. The GDP rate for Q2, and the retail sales for June slowed down beyond market expectations but also the urban investment and the industrial output growth rates decelerated, while house prices contracted deeper, all being for June. Calls for supportive measures by the People’s Bank of China have intensified. Should market’s worries for the difficulties faced by the Chinese economy intensify, we may see some cautiousness settling in among investors that could have adverse effects on US stockmarkets.

Earnings season releases

As for earnings we note the release of the relevant report for Netflix tomorrow, yet the heavy point of earnings releases is expected to be next Tuesday when we get the earnings reports of Microsoft (MSFT), Alphabet A (GOOG), Tesla (TSLA), Visa A (V), Louis Vuitton ADR (LVMUY), Coca-Cola (KO), General Electric (GE), Philip Morris (PM) and General Motors (GM) among others. We expect attention to be set primarily on the big Tech companies Microsoft and Alphabet which could also be setting the tone for US stockmarkets, given the AI frenzy dominating the markets.

기술적 분석

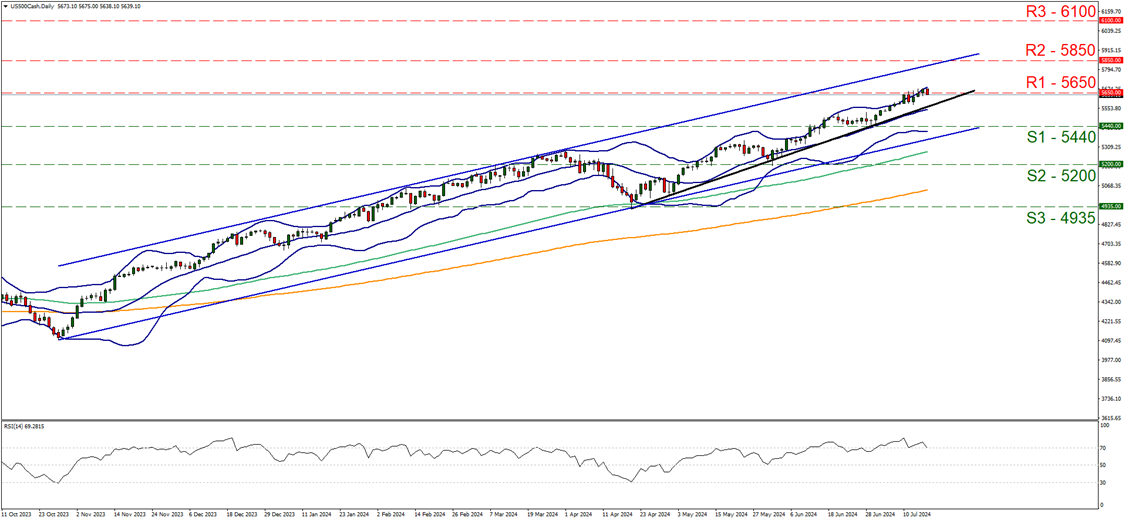

US500 Cash Daily Chart

- Support: 5440 (S1), 5200 (S2), 4935 (S3)

- Resistance: 5650 (R1), 5850 (R2), 6100 (R3)

S&P 500 timidly broke the 5650 (R1) resistance line yesterday reaching new all time highs, yet corrected lower during today’s Asian and early European session. Despite the correction lower we tend to maintain our bullish outlook for the index as long as the upward trendline guiding the index since the 19th of April remains intact. Furthermore we note that the 20, 100 and 200 moving averages are all pointing upwards underscoring the bullish direction of the index. Also the RSI indicator is currently running along the reading of 70, implying a strong bullish sentiment among market participants for the index which could push it even higher if maintained. Yet at the same time the RSI indicator may be implying that the index is at overbought levels and may be ripe for a correction lower. Similar signals are being also send by the fact that price action is flirting with the upper Bollinger band, which could slow down the bulls or even cause a correction lower. Should the bulls maintain control over the index we may see it breaking the 5650 (R1) resistance line, clearly thus entering unchartered waters once again and set as the next possible target for the bulls the 5850 (R2) resistance level. Should the bears take over, we may see the index initially breaking the prementioned upward trendline, in a first signal that the upward motion of the index has been interrupted, break the 5440 (S1) support line which was used by the index as a platform to jump higher on the 25th of June and set its sights on the 5200 (S2) support base, a level that held its ground against the downward pressure of the index’s price action on the 31st of May.

이 기사와 관련된 일반적인 질문이나 의견이 있으시면 저희 연구팀으로 직접 이메일을 보내주십시오 research_team@ironfx.com

면책 조항:

본 자료는 투자 권유가 아니며 정보 전달의 목적이므로 참조만 하시기 바랍니다. IronFX는 본 자료 내에서 제 3자가 이용하거나 링크를 연결한 데이터 또는 정보에 대해 책임이 없습니다.