As the week comes to an end, we have a look at what next week has in store for the market. On the monetary front we note on Monday the speech of Fed Chairman Powell. As for financial releases we get on Monday Japan’s preliminary industrial output for August, China’s NBS and Caixin manufacturing PMI figures for September, UK’s final GDP rates for Q2 and Nationwide house prices for September, Switzerland’s September KOF indicator and Germany’s preliminary HICP rates for September. On Tuesday, we get Japan’s Tankan indexes for Q3, Australia’s retail sales and building approvals for August, the Czech Republic’s revised GDP rates for Q2, Eurozone’s preliminary HICP rate for September, Canada’s manufacturing PMI figure for September and from the US the ISM manufacturing PMI figure for September and August’s JOLTS job openings. On Wednesday, we get from the US, September’s ADP national employment figure while oil traders may be more interested in OPEC+’s ministerial panel. On Thursday we get Australia’s August trade data, Switzerland’s and Turkey’s CPI rates both being for September and from the US the ISM non-manufacturing PMI figure for the same month. On Friday we get the US employment report for September with its NFP figure.

USD – Inflation data today

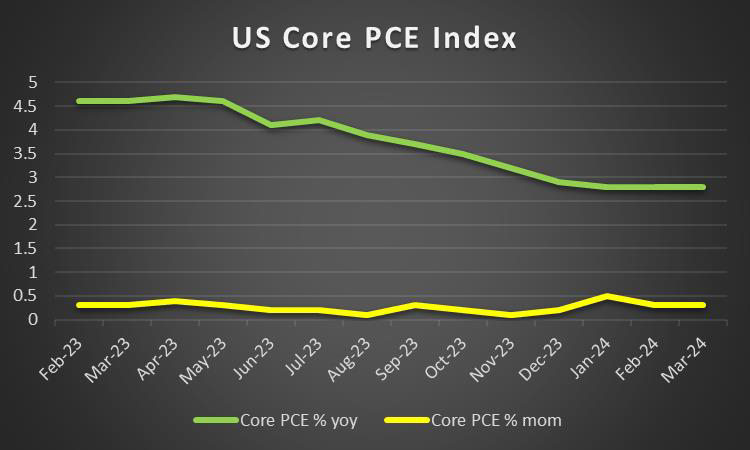

On a fundamental level, we would like to note the Vice Presidential debate, which is set to occur on the 1st of October, which may be crucial for both campaigns as former President Trump according to a NYT poll appears to have gained a lead in the swing state of Arizona against Vice President Harris. On a monetary level, we would like to note Chicago Fed President Goolsbee’s comments that he sees “many more” rate cuts ahead, which may imply further rate cuts down the road by the Fed. Yet, some divisions between Fed policymakers are evident, as Fed Governor Bowman who dissented on the rate vote, stated her concerns about inflation and the risk of a premature declaration of victory. As such from a macro-economic perspective the release of the PCE rates today may take on an even greater importance, where should the PCE rates showcase easing inflationary pressures in the US economy it may amplify calls for the Fed to continue on their rate-cutting cycle and vice versa. In addition, next week’s employment data appears to be the main focus of the Fed’s dual mandate as attention shifts away from inflation and is re-directed to the Fed’s other mandate of maximum employment.

GBP – BoE Bailey’s comments

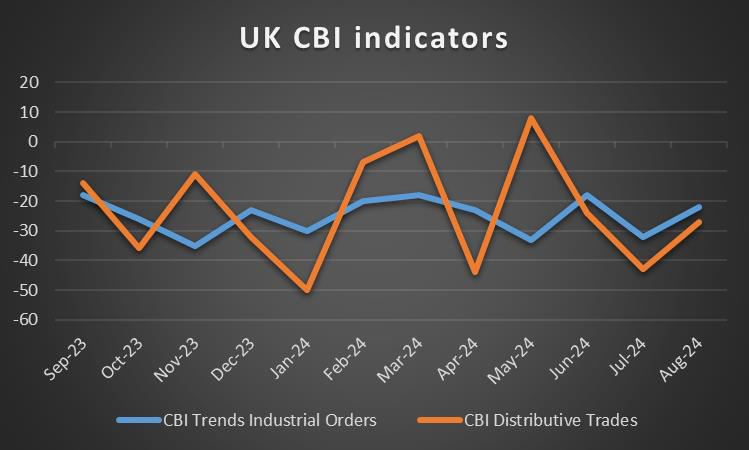

On a monetary level for the pound, we would highlight BoE Governor Bailey’s comments earlier on this week. The Bank of England Governor, stated earlier on this week in an interview that “very big shocks” would be required for interest rates to fall back to near zero, whilst re-iterating his view that the bank’s monetary policy easing cycle would be gradual. In turn, BoE Governor Bailey’s comments may have dimmed prospects of an aggressive rate-cutting cycle by the bank, which in turn appears to have aided the pound. On a macroeconomic level, the financial releases coming out from the UK this week appear to be a source of concern, with the preliminary figures for the UK’s Manufacturing and Services PMI figures coming in lower than last month’s readings and lower than the expected figures. The lower-than-expected PMI figures may imply that the UK manufacturing and services sector of the economy are expanding at a slower pace and thus may raise concerns about the resiliency of the UK economy. For next week, pound traders may be interested in the UK’s final GDP rate for Q2, which may provide greater insight into the healthiness of the UK economy.

JPY – BOJ minutes showcase some hesitancy

On a political level, former Defence Minister Ishida has won the ruling party’s race to be the next leader. Given that the ruling party has all but ruled Japan since the post-war era, it is almost a certainty that he will be the country’s next Prime Minister next Tuesday, where he is expected to be voted into office. On a monetary level, the BOJ’s July meeting minutes were released yesterday and provided useful insight into the inner thinking of BOJ policymakers. In particular, we would like to point out the comment made by a member that “the Bank should therefore

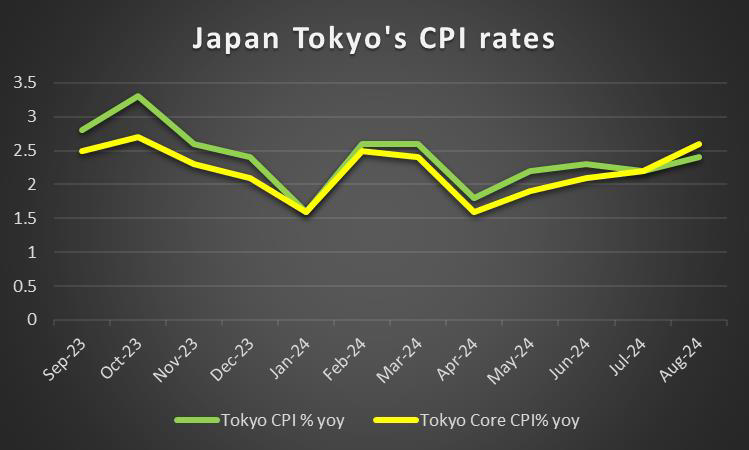

avoid a situation where market expectations for future policy interest rate hikes increase excessively”, which may imply that the bank may adopt a more cautious approach and decide on a meeting-by-meeting basis as to whether the financial conditions warrant a rate hike. Moreover, BOJ Governor Ueda on Thursday, implied that the bank was in no rush to raise interest rates, further supporting our aforementioned hypothesis and thus may have contributed to the Yen’s weakening against the dollar this week. Overall, the apparent dovish remarks by BOJ policymakers in regards to the pace upon which the bank should continue hiking rates, appear to have weighed on the JPY against the greenback over the past week. On a macroeconomic level, the BOJ’s Core CPI rate for September came in as expected at 1.8%, implying that the bank’s target of achieving its inflation target in a sustainable manner appears to be in sight.

EUR – Is the Eurozone in trouble?

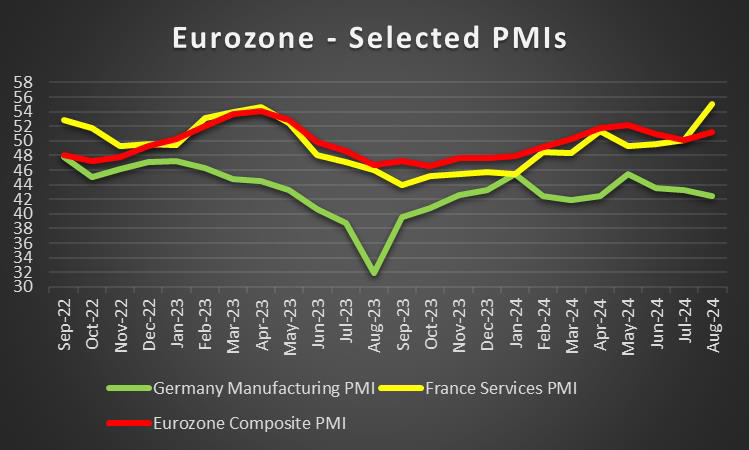

Starting on a macroeconomic note for the Eurozone, France’s, Germany’s and the Eurozone as a whole, released their preliminary services and manufacturing PMI figures for September this Monday. Across the board, the PMI figures came in lower than expected implying a weakening in Europe’s largest economies and in particular, Germany’s manufacturing PMI figure appears to be moving further into contraction territory as well as France’s services PMI figure which also dropped into contraction territory. The PMI figures may paint a dire picture for the Eurozone’s economy and thus may place a greater degree of pressure on the ECB to continue or embark on a more aggressive monetary policy easing stance. As such, should ECB policymakers adopt a more dovish tone, i.e implying further rate cuts down the line, it may weigh on the common currency. On the flip side, should ECB policymakers refrain from committing to future rate cuts, it may intensify market worries about the health of the Eurozone and thus may aid the common currency initially, yet should recession worries arise it could eventually weigh on the EUR. Therefore, with the risks being this high, we would not be surprised to see attention being shifted to next week’s release of the Eurozone’s preliminary HICP rates for September. Should the HICP rate fail to showcase easing inflationary pressures in the zone, it may aggravate concerns about a potential recession and vice versa.

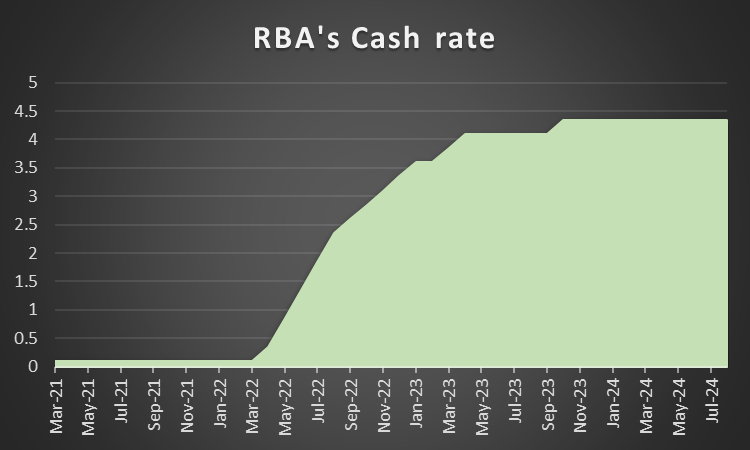

AUD – RBA remains on hold

On a monetary level, the RBA remained on hold at 4.35% as was widely expected by market participants. As such attention may have turned to the bank’s accompanying statement following the interest rate decision in which it was stated according to Reuters that “while headline inflation will decline for a time, underlying inflation is more indicative of inflation momentum, and it remains too high”. Essentially, it appears that RBA policymakers remain vigilant about the risks of inflation remaining entrenched in the Australian economy and that the bank may need to keep interest rates at sufficiently restrictive levels. Furthermore, RBA Governor Bullock stated that “the message clearly from the board is that in the near term, it does not see interest rate cuts”. In turn, the messaging from RBA policymakers may have aided the Aussie, as the bank appears to be poised to keep interest rates at restrictive levels for a prolonged period of time. However, from a macroeconomic perspective, the monthly CPI indicator for August came in as expected at 2.70% which is lower than the prior rate of 3.50% and thus may imply easing inflationary pressures. Overall, should the inflation readings showcase easing inflationary pressures in the Australian economy, it may increase pressure on the RBA to adopt a more dovish tone which in turn may weigh on the AUD. However, should inflation fail to drop to levels deemed appropriate by the RBA, the bank’s stance may remain steadfast and thus could aid the Aussie.

CAD – Trudeau survives vote of no confidence

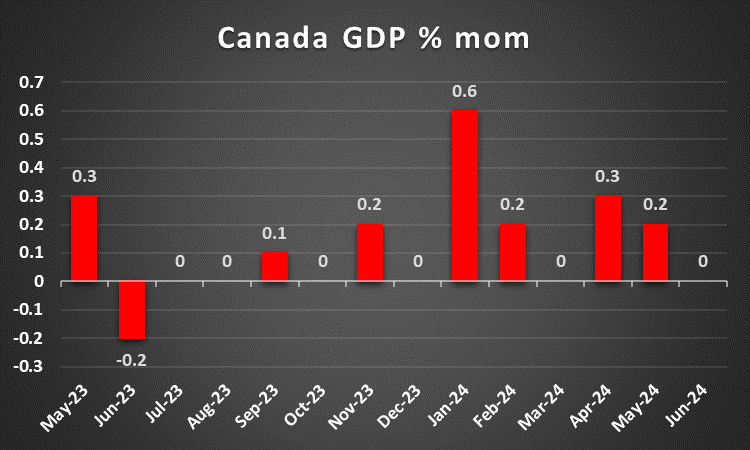

On a political level, Canadian Prime Minister Justin Trudeau managed to survive the vote of no confidence brought by the conservative opposition party earlier on this week. The recent tensions on a political level may impact the Canadian dollar in the event that an early election is called, yet that does not appear to be the case at this point in time. On a monetary level, BoC Governor Tiff Macklem stated on Tuesday that the progress made by the bank in bringing inflation down to the bank’s 2% inflation target, may make it reasonable to expect more rate cuts. In turn, the comments made by the BoC Governor may be interpreted as dovish in nature, as the bank may continue on their monetary policy easing path and thus may weigh on the CAD. On a macroeconomic level, Loonie traders may be looking forward to Canada’s manufacturing PMI figure for September next Tuesday. Should the PMI figure exit contraction territory and enter expansionary territory it may imply that the Canadian economy is improving and thus could aid the CAD and vice versa. On a fundamental level, given Canada’s status as an oil exporting nation, the recent report by Reuters that Saudi Arabia will give up its oil price target and will raise oil output could weigh on the Canadian dollar.

General Comment

As a closing, we note for the FX market that we expect the USD to regain some of the initiative to other currencies, given that the frequency and gravity of US financial releases are set to increase in the coming week. As for US stock markets, we note the optimism characterizing market participants in the past few days, with all three major US stock market indexes namely Dow Jones, S&P 500 and Nasdaq preparing to end the week in the greens. On a fundamental level, the recent escalation between Israel and Hezbollah appears to be dominating the media airwaves, as the possibility of a regional war has drastically increased since last week. Thus, with geopolitical tensions in the region mounting, we would not be surprised to see inflows into the precious metal given its status as a safe haven asset.

이 기사와 관련된 일반적인 질문이나 의견이 있으시면 저희 연구팀으로 직접 이메일을 보내주십시오 research_team@ironfx.com

면책 조항:

본 자료는 투자 권유가 아니며 정보 전달의 목적이므로 참조만 하시기 바랍니다. IronFX는 본 자료 내에서 제 3자가 이용하거나 링크를 연결한 데이터 또는 정보에 대해 책임이 없습니다.