After a busy interest rate decision week, we take a look into what next week has in store for the markets. On the monetary front, we highlight the release of RBA’s interest rate decision on Tuesday, yet also BOE’s and CNB’s interest rate decisions on Thursday which are expected to gather interest among traders. But it’s expected to be an exciting week also due to the release of a number of high-impact financial data. On Monday we make an early start with Japan’s Preliminary Industrial production rate for June, China’s NBS Manufacturing PMI figure, Eurozone’s Preliminary HICP rate, both for July and lastly the Eurozone’s Preliminary GDP rate for Q2. On Tuesday we note the release of Australia’s building approvals rate for June, China’s Caixin Manufacturing PMI figure for July, Germany’s Final Manufacturing PMI figure and the US ISM Manufacturing PMI figure both for July. On a quiet Wednesday we note New Zealand’s employment data for Q2. On Thursday, we note Australia’s Trade Balance figure for June, Switzerland’s and Turkey’s CPI rates for July, the US weekly initial jobless claims figure, the US Factory orders rate for June and the US ISM Non-Manufacturing PMI figure for July . On Friday we make a start with Germany’s Industrial orders rate for June and highlight the US and Canada’s Employment data both for the month of July.

USD – Fed hikes rates and keeps door open for more

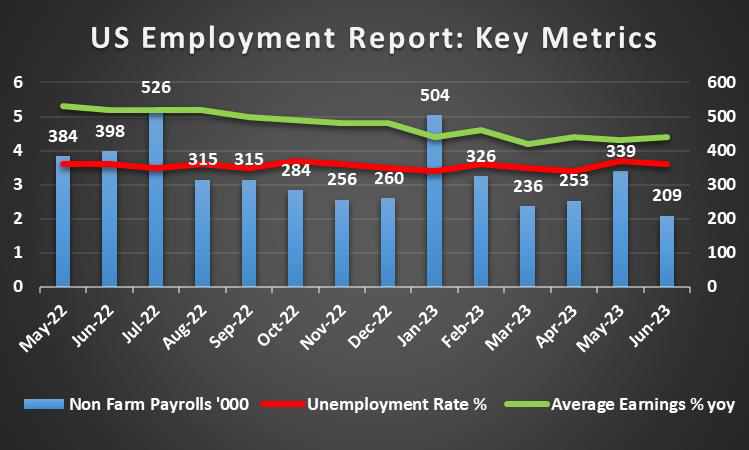

The USD seems to continue to remain in the greens for a second week in a row against its counterparts. On a macroeconomic level, we note the continued albeit narrowed contraction of economic activity in the US manufacturing sector as per the US Preliminary S&P Manufacturing PMI figure in July. Our worries tended to intensify, for the sector yet the release of the US Preliminary GDP rate for Q2, came in better than expected with the actual rate accelerating to 2.4%, despite expectations for a slowdown to 1.8%. Furthermore, the initial jobless claims figure came in at 221k compared to the expected 235k and may have been indicative of a continued tight labour market in the US. The releases tended to highlight the resilience and prospects of the US economy. Therefore, we anticipate that next week’s release of the US Employment Report for July may shed some light on the tightness of the US labour market and should the rates and figures show a tight US employment market we may see the greenback gaining. On a monetary level, we note that the Fed hiked interest rates, as was widely expected by 25 basis points, with Fed Chair Powell leaving the door “open” for a potential September rate hike. In addition, we believe that based on the accompanying statement , the bank would now appear to be more data oriented, with its predisposition for rate hikes, now been shunned aside in favour of a more data oriented approach. In conclusion, despite the better than expected GDP growth rate for Q2, we anticipate that the bank will favour a more cautious approach and remain on hold in its next meeting, in order to allow for the bank to assess the impact of the continued high-interest rates on the economy.

GBP – BoE’s interest rate decision in the crosshair

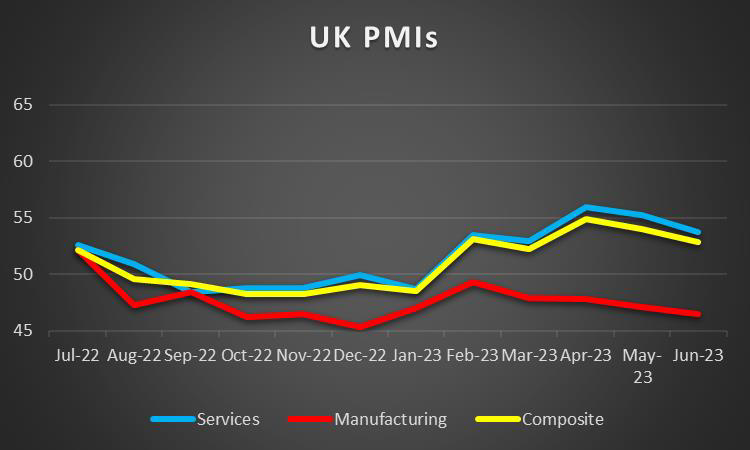

The pound seems about to end the week lower against the USD,and the JPY yet is gaining aginst the GBP. On a fundamental level, we highlight a report by the BBC that the Junior doctors in the UK have announced a strike action plan in August and that strikes in the nation’s airports and railway’s appear to be continuing, with a strike action set for the 29th of July for the biggest rail union and staff at Gatwick are anticipated to vote on a pay deal, where should it be rejected, they will walk out for four days from the 4th of August to the 8th of August. Yet we should note the majority of strikes have been managed to be prevented, as staff at other airports accepted a new pay deal. Overall the unrest does not seem to bode well for pound traders. On a macroeconomic level, the strengthening of the pound seems odd after the continued deterioration in the UK’s Preliminary PMI figures for June. The continued deterioration of economic activity in the UK should have driven the pound to lower ground, yet it could be that the lack of other financial releases have allowed the pound to capitalize on its counterparts’ weakness. Furthermore, the lack of financial releases next week, could allow the pound’s direction to be dictated by other pairs and as such could be vulnerable to volatile price swings. On the monetary front, we highlight the BoE’s interest rate decision which is due next Thursday, with GBP OIS currently implying 72% probability for the bank to hike rates by 25 basis points whilst the remainder anticipate a 50 basis point hike. Therefore, we attribute the pounds rise against its counterparts, to market expectations that the BoE will continue its aggressive rate hiking path, thus allowing the pound to gain. Furthermore, with Meghan Green’s first official meeting as an MPC member, we highlight her perceived hawkish comments made to the press, thus we anticipate that there may be more support for a 50 basis point hike than what market analysts currently anticipate. Should the bank actually maintain a hawkish tone that may justify the market’s expectations for more rate hikes to come and support the sterling.

JPY – BoJ making its YCC more flexible

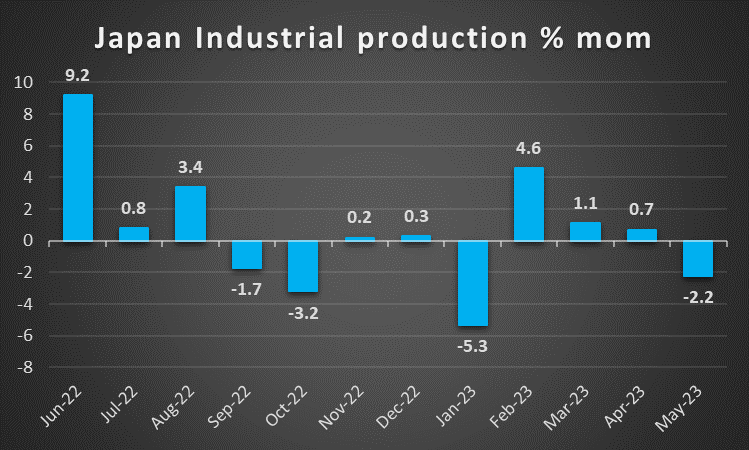

JPY seems about to end the week higher against the USD, the EUR and the pound, in a sign of general strengthening. On a macroeconomic level, we note the higher-than-expected CPI rates for Japan that where released earlier today, were indicative of persistent inflationary pressures in the Japanese economy, as inflation pressures across developed economies appear to be easing, the story in Japan appears to be different. The higher than expected rates tended to provide some additional support to JPY in Friday’s Asian session. In addition, traders may be looking to Monday’s Preliminary Industrial production rate for June, which is anticipated to shed some light into the country’s industrial dynamic as global demand appears to be slowing down. A possible slowdown of the preliminary industrial output growth rate could be in line with the continued contraction of economic activity in the manufacturing sector as indicated by July’s preliminary PMI figures. On a monetary level, BoJ remained on hold as was expected and actually did tweak its Yield Curve Control (YCC) policy, yet not exactly the way the market expected. The bank actually announced that it will continue purchasing Japanese Government Bonds (JGB) yet show a wider flexibility in its tolerance regarding their yield. The ultimate band is widened to 1% from the prior 0.5% yet the bank stated that it may also purchase JGBs without waiting for yields to reach a full 1%. In any case, the decision despite BoJ’s dovish narrative, was perceived as some sort of tightening and provided support for JPY. There seem to be expectations for the tightening to continue in the coming meetings, yet we would express our doubts for such a scenario. Nevertheless, we note the statements made by IMF Economist Gourinchas, who advised the Japanese economy to prepare itself for potential interest rate hikes, adding pressure for a shift in the bank’s stance on its ultra-loose monetary policy settings by the end of the year.

EUR – ECB hikes yet hesitates for more

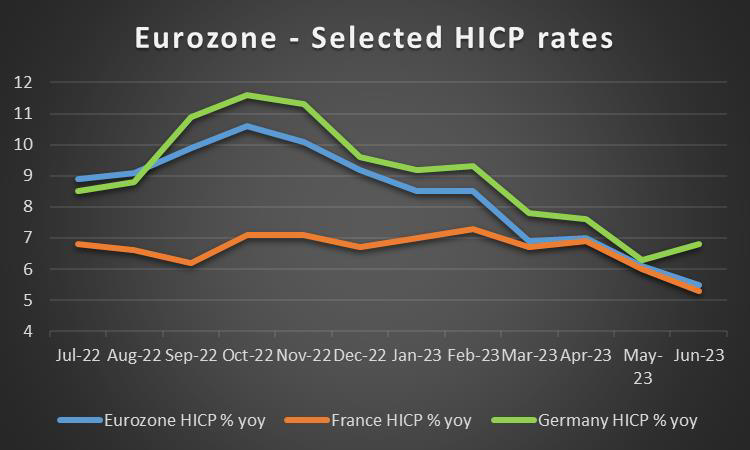

The common currency ends the week lower against the USD, GBP and JPY in a sign of wider weakness for the common currency in the week. On a fundamental level, we note that the raging wildfires in Greece appear to be continuing and the overall rather extreme climate conditions in Europe may weigh on the common currency. On macroeconomic level, the Preliminary PMI figures for July for France, Germany and the Eurozone as a whole, could be described as a bloodbath. The Preliminary PMI figures where indicative of a continued deep contraction, spiking fears of a recession in the largest economies of the Eurozone, which in turn weigh heavily on the euro. Should these fears continue to be validated by future financial releases, we may see the common currency, losing ground to its counterparts, as it becomes more evident that a recession is inevitable in the Eurozone. Furthermore, traders may be looking at the Eurozone’s Preliminary HICP rate for July and Preliminary GDP rate for Q2, for more clues as to how the Eurozone as a whole is faring with the high levels of interest rates. On the monetary front, we highlight the ECB’s interest rate decision yesterday, where the bank hiked by 25 basis points as was expected. The key take away however, was ECB President Lagarde’s press conference, where when asked by a Bloomberg reporter about the remaining ground that needed to be covered with interest rates, the ECB President replied with “At this point, I don’t think so” , hinting that the bank may be reaching its terminal rate faster that what was previously anticipated, as such with the end in sight, we may see the common currency further seceding ground to its counterparts. In our view, the current financial releases stemming from the Eurozone, could be indicative of the high interest rates, having a meaningful impact on the war against inflation and as such should the ECB continue down it’s current path , we may see a deep recession being induced by the bank.

AUD – RBA interest rate decision in the spotlight

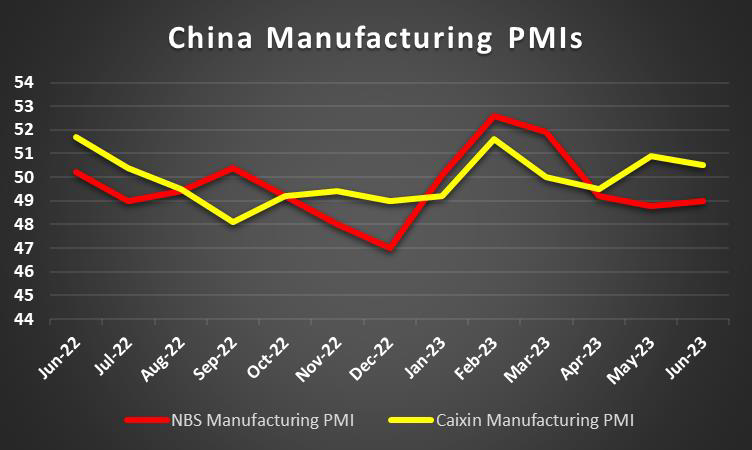

AUD is about to end the week lower against the USD for the second week in a row. On a macroeconomic level, we note that Australia’s CPI rates for Q2 came in lower than expected, hinting that inflationary pressures on the Australian economy, appear to be easing. In addition, the continued fears surrounding China’s economy appear to be weighing heavily on the Aussie, as their overreliance on China for their exports appears to be taking a turn for the worst. Therefore, despite positive developments for the Aussie, their reliance on China as their main trading partner for their exports, could potentially see the Australian economy being dragged down by the Chinese economic deterioration. Furthermore, we note that the lower than expected PPI rates for Q2 released earlier today and contraction of retail sales for July continue to validate our hypothesis that the Australian inflationary pressures continue to slow down. As such, Aussie traders may be looking at next week’s China’s Caixin and NBS manufacturing PMI figures for July, in order to gauge long term demand for their exports, in addition to Australia’s trade balance figure for June which may shed light on the perceived demand for Australian exports. On a monetary level, despite RBA members stating in their last meeting that the “Members agreed that some further tightening of monetary policy may be required to bring inflation back to target within a reasonable timeframe, but that this depended on how the economy and inflation evolve” , it would appear that the aforementioned macroeconomic events, could potentially weigh on the RBA’s interest rate decision which is due next Tuesday, with AUD OIS currently implying a 76% probability for the bank to remain on hold. We anticipate, that this will be the case next week, as it will be the last meeting of the current RBA Governor Lowe, who is set to be replaced by Deputy Reserve Bank governor Bullock in mid-September. Therefore, we may see a pause in order to prevent “rocking the boat” before his departure. However, in the event that the bank takes the market by surprise and hikes, say for example in a pre-emptive strike before the switch of leadership, we would anticipate the Aussie to gain in the short term, yet on the long term it could potentially stifle growth in an already fragile economy, thus weakening the Aussie over a greater time period.

CAD – July’s employment data in focus

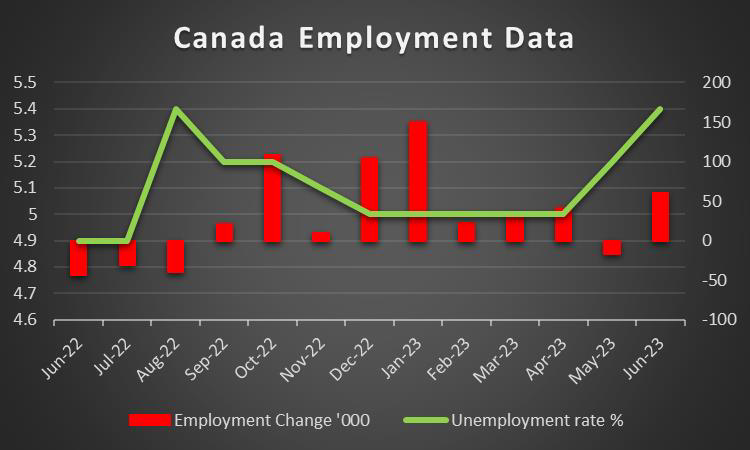

The Loonie tended to remain relatively stable against the USD in the past week, in a continuation of past week’s movement. On a monetary level, the Loonie seems to remain supported as BoC in its Summary of Governing Council deliberations before the July meeting discussed delaying to hike rates, yet ultimately did so by 25 basis points in order to ensure progress is being made in curbing inflationary pressures in the Canadian economy. For the time being, we note that the market still expects another rate hike by the bank after a pause in the September meeting. Such expectations are expected to be enhanced should inflation fail to slow down considerably over the next months. On a more fundamental level, we note that the rise of oil prices seems to maintain support for the Loonie, given that Canada is a major oil-producing economy. We note that as long as the market expects increased demand from China and given the expected low production levels of OPEC+ members, we may see oil prices continuing to rise slowly but steadily. On a macroeconomic level, we note that Canada’s business barometer remained relatively unchanged in a possible sign of uncertainty about the economic outlook and note that May’s GDP rate is still to be released. In the coming week we highlight the release of Canada’s July employment data and despite expecting a correction lower of the employment change figure after the stellar 59.9k for June, should the data show that the Canadian employment market remains tight we may see the Loonie getting some support.

General Comment

As conclusion, we expect volatility to be maintained in the coming week as high impact financial releases are expected to keep reeling in as are monetary policy events. The USD may share of the initiative in the FX market with other currencies, thus allowing for a more balanced blend of trading opportunities. US stockmarkets are still expected to be influenced by the earnings season, given that a number of high profile companies are to release their earnings reports. In the coming week, we note the release of the earnings

reports, on Tuesday of Uber (#Uber), Pfizer (#PFE), AIG (#AIG) and Starbucks (#SBUX), on Wednesday of Paypal (#PYPL) and on Thursday we highlight Amazon (#AMZN), Apple (#AAPL), Airbnb (#Airbnb) among a slew of earnings releases during the week. For the time being we note the improvement of the market sentiment which allowed all three main US stock market indexes, namely the Dow Jones, Nasdaq and S&P 500 to rise further. The improved market sentiment seems also to be related to the easing of the Fed’s hawkish stance, as market worries for a possible overtightening of the Fed’s monetary policy seemed to ease. We expect the market positive market sentiment to be maintained yet that remains to be seen. As for gold’s price, we note that the rise of the USD seems to have weighed on the precious metal’s price. We expect the negative correlation of the USD with gold’s price to be maintained in the coming week with the US yields also playing a substantial role given that US Bonds tend to be a competing trading instrument to gold. Should the USD gain further, Gold’s price may continue to drop and vice versa.

이 기사와 관련된 일반적인 질문이나 의견이 있으시면 저희 연구팀으로 직접 이메일을 보내주십시오 research_team@ironfx.com

면책 조항:

본 자료는 투자 권유가 아니며 정보 전달의 목적이므로 참조만 하시기 바랍니다. IronFX는 본 자료 내에서 제 3자가 이용하거나 링크를 연결한 데이터 또는 정보에 대해 책임이 없습니다.