We are nearing the end of the week and have a look at next week’s calendar. On Monday we get Germany’s Ifo indicators for November. On Tuesday we get UK’s CBI distributive trades for November, the US PPI rates for September and the US consumer confidence for November. On Wednesday, we get Australia’s CPI rates for October, from New Zealand, RBNZ’s interest rate decision, Norway’s GDP rates for Q3, and from the US we may get the PCE rates for October, the durable goods orders for October, the 2nd estimate if Q3’s GDP rate and the weekly initial jobless claims figure. On Thursday we get Australia’s capital expenditure for Q3, Germany’s GfK for December and Euro Zone’s economic sentiment for November. On Friday we get Japan’s Tokyo CPI rates for November and preliminary industrial output for October, Sweden’s final GDP Rate for Q3, France’s and Germany’s preliminary HICP rate for November, from Switzerland the GDP rate for Q3 and the KOF indicator for November and from Canada, Q3’s GDP rate.

USD – US PCE and GDP rates in focus

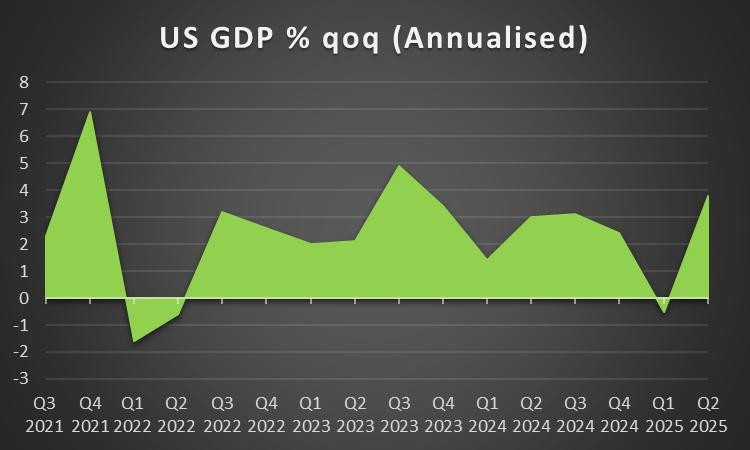

Our comment for the USD starts with monetary policy as the market expectations for the Fed’s intentions seem to be a key if not the key driver behind the greenback’s direction. The release of the Fed’s October meeting minutes highlighted the bank’s hesitation for further easing of its monetary policy. Signals from Fed policymakers, seem mixed, yet in the big picture a shift is detected towards the bank remaining on hold in December. It’s no wonder that the market’s expectations as implied by Fed Fund Futures are 75.6% for the bank to remain hold. Should we see the market’s expectations for the bank to remain on hold be enhanced in the coming week, we may see the USD getting additional support. On a macroeconomic level, we note that the release of the US employment data for September sent out mixed signals as the NFP figure came in higher than expected while at the same time the unemployment rate ticked up. We note that the release failed to alter materially the market’s expectations for the Fed intentions. In the coming week, we highlight the release of the US PCE rates for October and a possible acceleration of the rates could imply a resilience of inflationary pressures in the US economy providing possibly some support for the USD. Also we highlight the release of the second estimate of the US GDP rate for Q3 and a possible slowdown of the rate could further enhance the already existing market worries for the US economic outlook, thus possibly weighing on the greenback. On a fundamental level, we note that the unpredictive US President Trump could at any given shake the markets.

Analyst’s opinion (USD)

“We note the Fed’s intentions as a key driver behind the direction of the USD and expect it to continue driving the greenback in the coming week as well. A possible enhancement of the market’s expectations for the Fed to remain on hold could provide aid for the USD. On a macro level, a possible release of the US PCE rates for October and the second estimate of the US GDP rate for Q3 could stir interest among traders.”

GBP – Autumn budget to move the pound

The main event for the GBP in the past week may have been the release of the UK CPI Rates for October. The rates slowed down as was expected and the headline rate reached 3.6% while the core rate reached 3.4%. We note the slight easing of inflationary pressures for UK economy, yet at the same time note that the CPI Rates are still at too high levels and further easing is required. On a macro level, the calendar for pound traders is rather empty of high impact financial releases from the UK, thus we may see the pound seeking direction from fundamentals. On a monetary level we note the market’s expectations for the BoE to cut rates in its December meeting, which may weigh on the sterling somewhat, yet that’s still a way off, so the influence on the markets unless it alters materially may be low. In the coming week on a fundamental level, we may see UK Chancellor of the EX Chequer Reeves’ Autumn budget playing a dominant role in the direction of the pound. The budget is to be released by Reeves on Wednesday the 26th. The big issue is how the UK Finance minister is trying to fill the expected deficit, while at the same time perform a balancing act by promoting growth in the UK economy. We may see the UK finance minister raising taxes on high personal income and possibly also capital gains and inheritance, given also the UK government’s leftish orientation. At the same time, we may see the some reforms promoting possibly some deregulation, to loosen the reins on the UK economy. Should the event be perceived as promoting an expansionary fiscal policy for the UK economy, we may see the pound getting some support, while on the flip side, should the UK Government be perceived as overtaxing which in turn may weigh on the UK economic outlook we may see the event weighing on the pound.

Analyst’s opinion (GBP)

“In the coming week, in regards to the pound and given the rather empty calendar, we intend to focus on the release of UK finance minister Reeves’ Autumn budget. The event is expected to play a dominant role for the pound’s direction and should it be perceived as overtaxing the UK economy it could weigh on the pound. On the flip side should the expansionary fiscal policy be underscored the pound may get some support.”

JPY – Market intervention possible

The main characteristic of JPY over the past week was its substantial weakening against the USD. On a macro level, we note the slight slowing of the CPI rates for October, yet at the same time we still consider their level as sufficient for the BoJ to continue supporting its plans for a possible tightening of its monetary policy. For the time being we note that JPY OIS imply that the market expects the bank to remain on hold in the December meeting and marginally expects the bank to proceed with a rate hike in the January meeting. It’s characteristic of the bank’s hawkish intentions that BoJ Board Member Koeda signalled the possibility of a rate hike even in the December meeting. Please note that on Thursday BoJ board member Noguchi is to make a speech and should he signal that the bank may tighten its monetary policy we may see JPY getting some support. On the other hand we highlight the political pressures exercised by Japanese Government on BoJ to take it slow with any tightening of its monetary policy, which tend to weigh on JPY. We have to note that JPY has reached very low levels against the USD and both BoJ and the Japanese Government are monitoring the situation with a great sense of urgency. The continuous weakening of JPY tends to enhance the possibility of a market intervention to its rescue, yet at the same time we note that even a possible market intervention may prove to be a temporary relief for the Yen. On the other hand a possible tightening of BoJ’s monetary policy could act as a more lasting deterrent for JPY sellers.

Analyst’s opinion (JPY)

“We highlight the continuous weakening of JPY against the USD over the past few days. It should be noted that the situation is being closely monitored by BoJ and the Japanese Government with a great sense of urgency and we add that as long as the JPY continues to weaken the possibility of a market intervention to its rescue increases.”

EUR – Germany’s and France’s preliminary November HICP rates

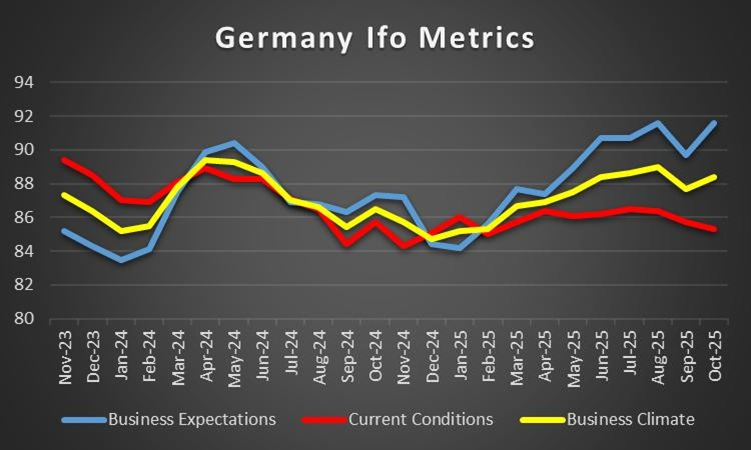

The UER is about to end the week in the reds against the USD and on a macro-economic level we note that the preliminary PMI figures for November sent out mixed signals and our worries tend to continue to revolve around Germany’s manufacturing sector. Given the macroeconomic worries for growth in the Euro Zone, we note the release of the revised Q3 GDP rates for Germany and France, yet the highlight may prove to be the release of the preliminary HICP rates for November of Germany and France. Should we see the rates accelerate we may see the market’s expectations for the ECB’s intentions shifting. For the time being the EUR OIS imply that the market expects the bank to remain on hold until the end of the coming year. On a more positive note the EU Commission announced that it expects growth to accelerate, yet military spending increases debt. Also on a fundamental level, we note that the war in Ukraine continues to be a destabilising factor for EU’s east flank. The recent incidents with a sabotage of a train line alleged from Russia and a breaking of the Romanian airspace by a drone, as well as the recent comment by Germany’s defence minister Boris Pistorius, that this may have been the last peaceful summer, are indicative of existing and intensifying uncertainty. The uncertainty tends to weigh on the macroeconomic outlook thus also on the single currency. The latest US peace plan seems to have been failed to gain traction, yet it’s a positive that the US is still active in finding a solution. Should we see market worries about the issue intensifying, we may see the EUR losing further ground.

Analyst’s opinion (EUR)

“On a macroeconomic level we note the release of Germany’s and France’s preliminary HICP rates for November as the highlight of the week. On a monetary level the markets’ expectations for the ECB to remain on hold throughout 2026 tend to be supportive for the EUR. Yet on a fundamental level, the war in Ukraine tends to create uncertainty and tends to weigh on the single currency.”

AUD – Australia’s October CPI rates could shake the Aussie

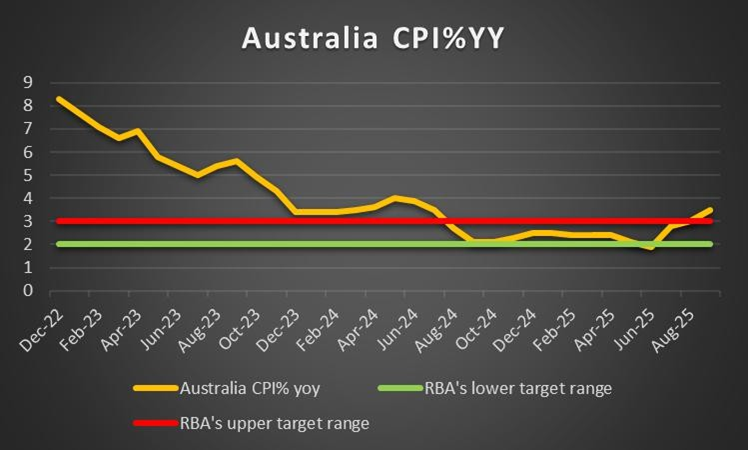

The Aussie seems about to end the week deep in the reds against the USD. On a fundamental level, the intensification of the risk averse market approach tended to weigh on the Aussie which is considered as a riskier asset in the FX market, given its commodity nature. Should we see in the coming week, an easing of the market cautiousness we may see the Aussie gaining some ground. In the coming week, on a macro economic level, we note the release of the October CPI rates as the highlight for the week. Should the rates accelerate implying a resilience of inflationary pressures in the Australian economy, we may see the Aussie getting some ground as it could entail a hardening of RBA’s stance. For the time being AUD OIS imply that the market does not seem to price in the bank to cut rates until the end of the coming year. Such expectations tend to provide some support for the Aussie. Last but not least, we note the close economic ties of Australia with China, hence should we see tensions in the US-Sino relationship reemerging, we may see the Aussie retreating.

Analyst’s opinion (AUD)

“The Aussie seems about to end the week deep in the reds against the USD as the market’s cautiousness tended to weigh on the commodity currency. In the coming week we highlight the release of Australia’s CPI rates for October and a possible acceleration could provide support for AUD.”

CAD – Canada’s Annualised GDP rate for Q3, possibly the main event for the Loonie

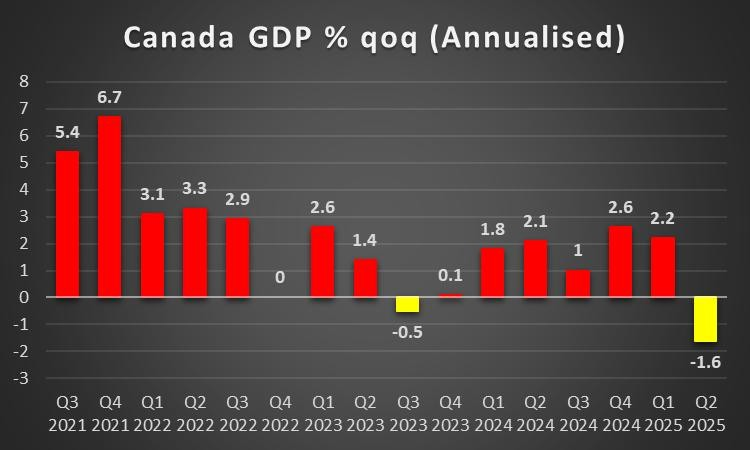

Also the Loonie seems about to end the week in the reds against the USD, with the cautious market sentiment weighing on the commodity currency. It should be noted that the drop of oil prices may have weighed on the Loonie as well given Canada’s status as a major oil producer. Market worries for a possible oversupply of the international oil market tend to drive oil prices lower and should they drop further, we may see the CAD suffering further. Also on a fundamental level, the voting of Canada PM Carney’s first budget, in the Canadian Parliament, even with a narrow majority, is considered as a positive for the CAD. On a monetary level, we note that BoC seems to remain firm on not easing its monetary policy. Currently CAD OIS imply that the market expects the bank to remain on hold until the end of next year. Overall such expectations tend to be supportive for the Loonie. It should be noted that the bank is expected to remain on hold despite Canada’s CPI rates slowing down in a signal of easing inflationary pressures in the Canadian economy. In the coming week, we shift our attention on growth and highlight the release of Canada’s GDP rates for Q3. The rate is currently in the negatives, and should it remain below zero, we may see market worries for a recession in the Canadian economy, intensifying and possibly weighing on the Loonie.

Analyst’s opinion (CAD)

“We tend to view the market’s expectations for BoC to remain on hold as supportive for the CAD, while the market’s cautiousness tends to be weighing. We expect the highlight of the coming week for Loonie traders, to be the release of Canada’s GDP rate for Q3. Should the rates accelerate and manage to escape the negatives, we may see the CAD getting some support, on the contrary, we may see the Loonie losing ground.”

General Comment

In the big picture, we expect the USD to maintain the initiative over other currencies, yet ease its grip on the FX market. Volatility may ease somewhat as we leave the release of the US employment data and the Fed’s meeting minutes behind us. Hence we may see a more balanced trading mix emerging in the FX market. We express our worries for the US stock markets given the sell-off of the past week. Main market worries seem to be focusing on the possibility of overvaluations for AI companies and the market expectations for financial conditions in the US economy to remain relatively tight. Should market worries intensify, we may see US stock markets losing further ground. On the other hand, we note that gold’s price seems to have stabilised somewhat as the market may still be maintaining a wait-and-see position.

이 기사와 관련된 일반적인 질문이나 의견이 있으시면 저희 연구팀으로 직접 이메일을 보내주십시오 research_team@ironfx.com

면책 조항:

본 자료는 투자 권유가 아니며 정보 전달의 목적이므로 참조만 하시기 바랍니다. IronFX는 본 자료 내에서 제 3자가 이용하거나 링크를 연결한 데이터 또는 정보에 대해 책임이 없습니다.