It’s been a shaky week in the midst of the holiday period and we are to open a window in what the next week has in store for the markets. On the monetary front, we note the release of RBA’s meeting minutes on Tuesday and we highlight the release of New Zealand’s RBNZ interest rate decision on Wednesday’s Asian session while in the American session we note the release of the Fed’s meeting minutes. Yet we also note on Thursday the interest rate decisions from Turkey of CBRT and from Norway of Norgesbank. As for financial releases we make an early start on Mondays’ Asian session with the release of Japan’s GDP rates for Q2 and China’s industrial output for July. On Tuesday we make a start with the UK employment data for June followed by Germanys’ ZEW indicators for August and in the American session we get Canada’s inflation metrics for July and the US industrial production growth rate for the same month. On Wednesday’s Asian session, we get Japan’s machinery orders for June and trade data for July, while in the European session we get UK’s inflation metrics for July, Eurozone’s second estimate of the GDP rate for Q2 and in the American session we get the US retail sales for July. On Thursday’s Asian session we highlight the release of Australia’s employment data for July while in the European session, we get Norway’s GDP rate for Q2, Eurozone’s final HICP rate for July and in the American session we get from the US the weekly initial jobless claims figure and the Philly fed Business index for August. On Friday we get New Zealand’s trade data for July, Japan’s CPI rates for July, UK’s retail sales for July and Canada’s retail sales for June.

USD– Fed’s meeting minutes in focus

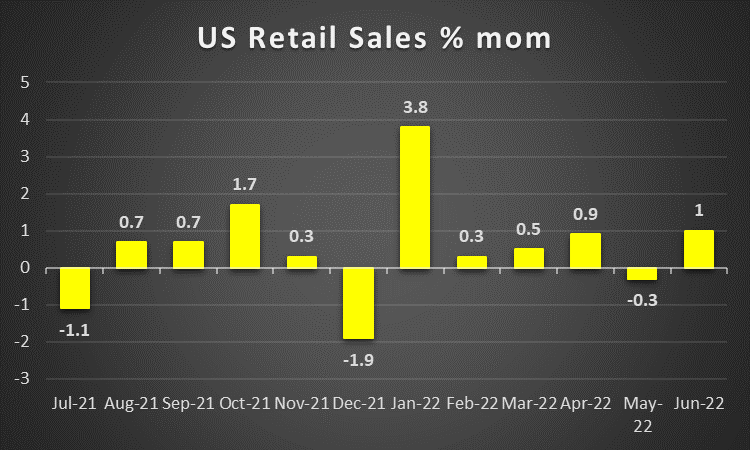

The USD is about to end the week weaker against its counterparts. The main driving force behind the weakening of the USD was the release of the US CPI rates for July on Wednesday. The annual inflation rate in the US slowed more than expected, with July’s reading of 8.5% yoy being below the 8.7% yoy market forecasts and marking the peak and the slowdown, from the 42-year high rate of June which was reported at 9.1% yoy. Compared to the previous month, the mom CPI slowed to stagnation levels being also lower than the forecasted rate of 0.2% mom. Should the prices indeed have reached their peak in June, then investors expect the Fed to take it’s foot off the pedal when it comes to the pace as well as the magnitude of the upcoming rate hikes. Since the readings were both coolerthan-expected, the market rushed to reappraise the probabilities of the Fed’s future monetary policy. On Wednesday prior to the release of July’s CPI rates, we noted that the FFF assigned a 70% probability for a 75-basis points rate hike for September’s meeting. After the event, the probabilities tilted marginally in favour of a 50-basis points basis points rate hike reflecting the market’s sentiment shift towards the new data and the expectations for a slowdown of the Fed’s aggressive stance. Following the releases Minneapolis Fed President Kashkari stated that the Fed is “far, far away from declaring victory” on inflation, despite welcoming the positive news that inflation may have started to cool down. Other Fed officials have said they want to see months of evidence that prices are cooling, especially in the core inflation metric. Hence we would not jump so quickly to the conclusion that the Fed is to ease its rate hiking path, just yet. Please note that another round of monthly CPI and jobs reports, for August, is to be released before the Fed’s next policy meeting on 21st of September. Thus we highlight the release of the Fed’s meeting minutes on Wednesday and we expect the document to be scrutinised by market participants in search for clues regarding the bank’s intentions. Should the tone of the document be tilted towards the hawkish side we may see the USD getting some support and vice versa. As for financial releases we make a start on Monday with the NY Fed Manufacturing for August, on Tuesday we get the number of housing starts and building permits for July, on Wednesday we get the US retail sales for July and on Thursday we get the weekly initial jobless claims figure, the Philly Fed Business index and the number of existing home sales for July.

GBP – CPI rates and employment data to move the pound

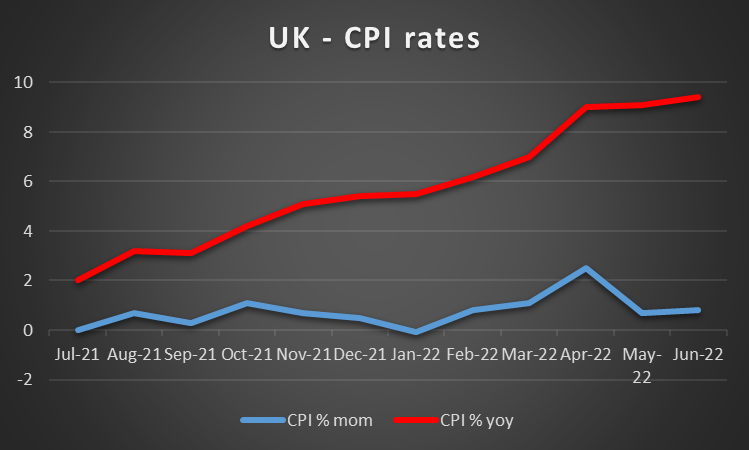

The pound is about to end the week stronger against the USD, yet not the EUR and JPY, implying that the rise of cable was more related to the weakness of the greenback rather than the strengthening of the sterling. On a fundamental level the race for the leadership of the Tories and the seat of the UK Prime Minister is on and headlines are appearing for Rishi Sunak and Liz Truss, with many political promises possibly affecting fiscal policy in the future, but for the time being seemed to have little if any effect on the market. Among promises for tax cuts from Truss and subsidies for energy from Sunak, Truss’s idea for BoE seems to be heavily debated. From weakening regulator’s powers to altering the bank’s mandate, all could be spelling bad news for the pound. It’s no surprise that BoE Governor Bailey defended the importance if the independence if the central bank and the powers of the regulatory arm of the bank. On the other hand BoE’s Governor also warned that interest rate hikes are to continue despite an extended recession in the UK economy, in order to prevent inflationary pressures becoming embedded in the UK economy. Also BoE’s chief economist Huw Pill stated that Britain will only feel the full impact of higher interest rates in late 2023 and that it is unlikely to be any return of quantitative easing for at least a few years, according to Reuters. The statement more or less reaffirmed the bank’s intentions to continue on its rate hiking path to curb inflationary pressures, while at the same time contradicts the idea that the bank will ease its monetary policy next year in order to fight a recession in the UK economy. As for financial releases we note the decline of the GDP rates for Q2 and June in negative territory, yet there was little reaction on the sterling. In the coming week though, we also get a number of financial releases that could interest pound traders. We make a start on Tuesday with the release of the UK employment data, while on Wednesday we highlight the release of UK’s CPI and PPI rates for July. Finally on Friday we get the retail sales growth rate for July.

JPY – GDP rates and other financial data eyed

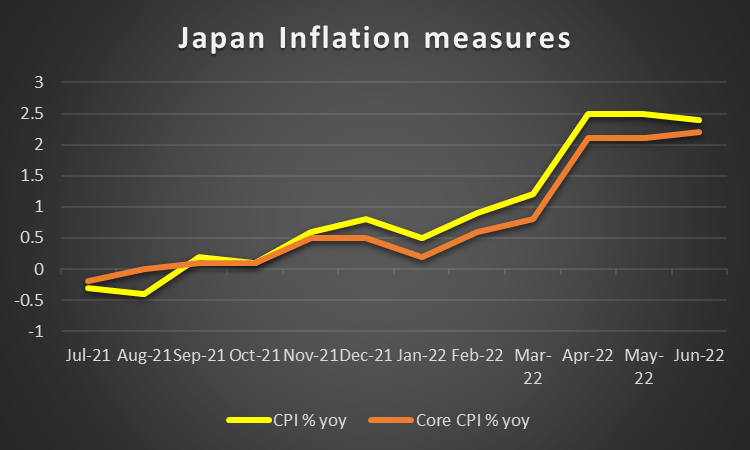

JPY is about to end the week stronger against the USD, but also GBP and EUR in α wider sign of strenghtening for the JPY. On a fundamental level we have to highlight the dual nature of JPY as a safe haven and a national currency. Hence any frictions in the interantional scene could create inflows for the Japanese currency. On a political level, the reshuffling of the Japanese Cabinet by Prime Minister Kishida cannot pass unnoticed. Public anger is being reported against the government of ties with the Unification Church, which has been characterised as a cult by critics. It should be noted that approval ratings of the Japanese Prime Minister Kishida are currently at very low levels over the issue. It’s no surprise that PM Kishida stated that the Church had no sway over the government’s policies and reshuffled the cabinet in an effort to ease any public reactions. It should be noted that according to Reuters the assasination of former Prime Minister Abe was linked to the issue. Overall though the direction of the Government’s policies seems to remain unchanged given that Finance minister Suzuki, remains in his post. The issue seems to be harmless yet for Japanese politics is serious and given that the stakes are high, it should be kept under watch, at least initially on a fundamental level. On a monetary level we expect the ultra loose monetary policy stance of BoJ to remain unchanged. Overall the policy stance is expected to remain the same until Governor Kuroda’s retirement next year, but even then, local media report that PM Kishida seems to be leaning towards the idea of the next BoJ Governor also being a dove. JPY traders though are to have a busy schedule ahead for the coming week. We make a start on Monday with the preliminary GDP rates for Q2 and should the rates remain in the negatives, that could imply that the Japanese economy has entered a technical recession. On Wednesday, we would also like to note the release of Japan’s machinery orders for June as well as the trade data for July. Finally on Friday we highlight the release of Japan’s CPI rates for July and a possible acceleration could provide some support for the JPY as it could increase the pressure on BoJ to tweak it’s dovish policy.

EUR – Scorching temperatures

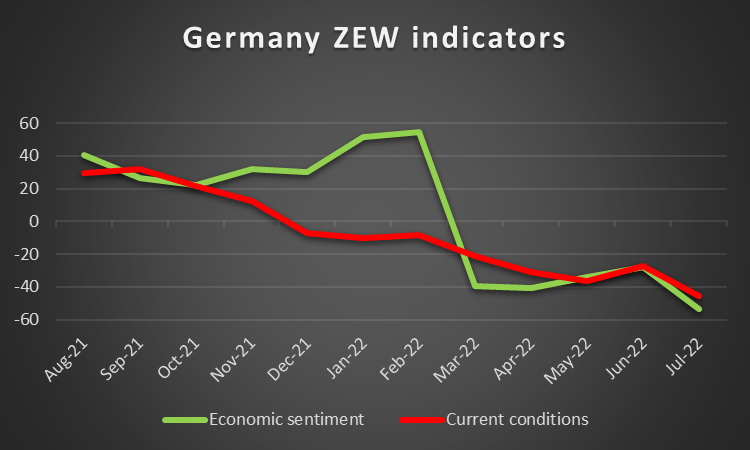

The common currency is about to end the week higher against the USD as well as against the pound but not JPY. There are scorching high temperatures in Europe and energy consumption seems to be running high as well. It’s characteristic that France and the UK have issued extreme hot weather alerts. It’s also characteristic that the Rhine River is reported to have low levels of water, actually so low, that some parts are about to, or have been closed for transportation. The river is considered a vital shipping route for Germany’s manufacturing sector and a possible halt of transport through the watery corridor could slow down the German economy, which is considered the economic powerhouse of the area. At the same time, energy consumption seems to be on the rise as the need to cool homes and offices grows. It’s reported that power prices in France and Germany have reached record levels as demand for natural gas got a boost. The situation seems to be dire and the stage seems to be set for an even more difficult winter ahead, given the dwindling natural gas inventories of the area. The possibility of energy rationing is being actively considered by European states and it’s characteristic of the situation. Yet environmental issues seem to have more diverse implications for the continent. Energy stations may have to work at low levels in order to prevent them from overheating, while the risk of fires in forests is rising substantially. On a monetary level, we expect the ECB to maintain its stance regarding its policies, especially in order to avoid fragmentation of the debt costs of member states. We also note that the slowdown of the US CPI rates for July in the US may have an effect also on the balance of power within the ECB, as supporters of faster rate hikes may argue that the Fed, given its wider rate hikes, is more effective in curbing inflationary pressures than the ECB. On the other hand, one could argue that each economy has its own characteristics and the Fed’s policies are not to be simply blindly followed. As for financial releases in the coming week, we have a rather light calendar for EUR traders, yet we would still like to note the release of Germany’s ZEW indicators for August on Tuesday and on Wednesday Eurozone’s second estimate of the GDP rate for Q2. Finally on Thursday we get Eurozone’s final HICP rate for July

AUD – Employment and Chinese data in focus

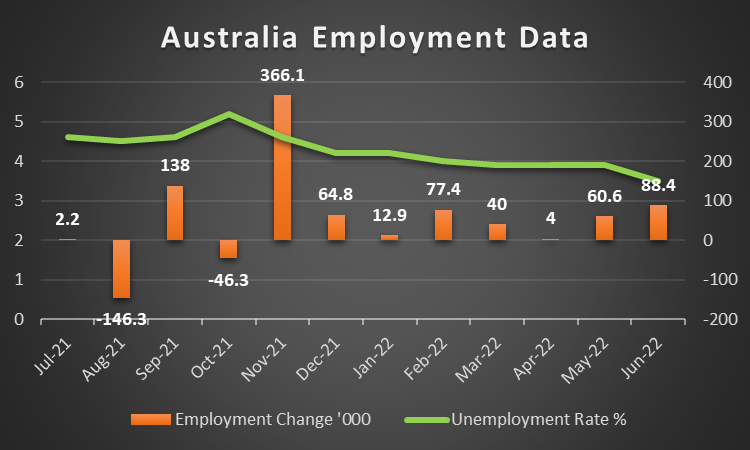

AUD is about to end maybe one of the best weeks it had since February, against the USD. On a fundamental level , we note that the improved market sentiment seems to be providing support for the commodity currency, which is considered a riskier asset. On the other hand though, the escalation of the tensions in the US-Sino relationships are still an issue for the Aussie. We maintain our fundamental worries for the possibility of China proceeding with military action on the island of Taiwan. It’s characteristic that Taiwan’s foreign minister Wu warned earlier today in a press conference that “China has used the drills … to prepare for the invasion of Taiwan” according to Reuters and urged “international support to safeguard peace and stability across the Taiwan Strait”. It should be noted that the Taiwan straits are of the busiest shipping routes worldwide and tensions could halt trading activities. We highlight the possible adverse risks for the Chinese economy of the matter, but also the closely linked Australian economy, as well as the outlook for global economy as a whole, given its severity. On the monetary level we note the release of RBA’s latest meeting minutes on Tuesday, which could provide a deeper insight for the bank’s intentions. It should be noted that a degree of uncertainty was inserted in the latest decision, which tended to weaken the Aussie. As for financial releases we note from Australia the release of July’s employment data. Should the rates and figures show that the Australian employment market seems to remain tight we may see the Aussie getting some support as it would encourage RBA to proceed with more and faster rate hikes. From China, we note on Mondays’ Asian session the release of July’s industrial output and retail sales. Should the growth rate be on the rise that could provide some support for the Aussie as it would imply a faster expansion of economic activity in the Chinese industrial sector and a rather robust internal market demand, which in turn could imply more exports of Australian raw materials to China.

CAD- CPI rates in the epicenter

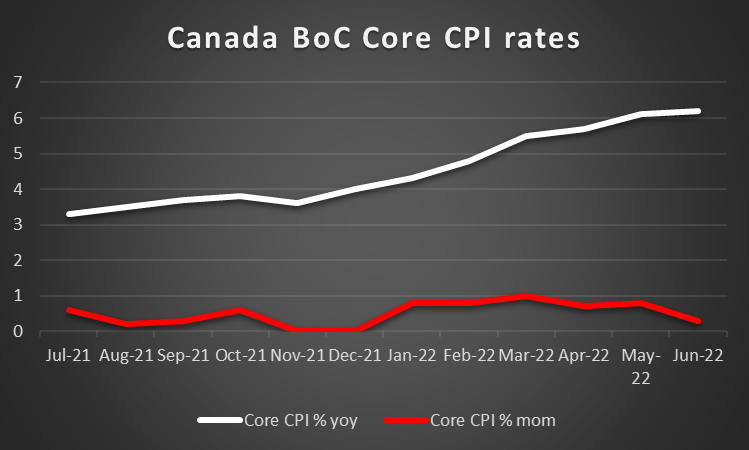

The Loonie is about to end the week stronger against the greenback recovering all the losses of the week before and then some. On a fundamental level, we note the influence that oil prices may have on the commodity currency’s price action. It should be noted that WTI prices seem to be on the rise for the past few days which may have contributed to the strengthening of the CAD as well. Overall oil’s price seems to have conflicting fundamentals as on the one hand, oil inventories in the US are on the rise yet, also a high demand for gasoline is being reported. On the monetary front we tend to maintain the expectation for BoC to remain tilted to the hawkish side, given the high inflationary pressures in the Canadian economy. Please note though that Canada’s inverted yield curve rings the bells of alarm, that the bank may be proceeding too fast with rate hikes and risks throwing the Canadian economy into a recession. For the time being it seems that the market’s expectationsfor the Bank to proceed with a 75 basis points rate hike are cooling down, yet that also depends on developments on the inflationary front. Hence in the coming week we highlight the release of Canada’s CPI rates for July. Please note that the headline rate accelerated further in June, reaching a 39 year high at 8.1% yoy, adding more pressure on BoC to hike rates at a fast pace. Should the rates slowdown though, implying that inflationary pressures have peaked and are correcting lower, we may see the CAD losing some ground as that would allow BoC to ease its hiking approach somewhat. On the other hand, should the rates accelerate further, we may see the pressure on BoC intensifying. Last but not least, we would also like to note the release of Canada’s retail sales for June on Friday.

General Comment

As a closing comment we expect the greenback to relent some of its advantage over other currencies in the determination of the FX market’s direction, given that the number of high impact financial releases stemming from the US is lessening, yet still the release of the Fed’s meeting minutes could generate some substantial interest among traders. On the other hand, other currencies could also come under the spotlight once again in certain moments during the week. At this point we would like to highlight the release of the interest rate decisions from the central banks of New Zealand, Turkey and Norway which could stir the waters of their respective currencies. Once again we note that we are entering the holiday period and we may see thin trading conditions being reflected at some points in the markets. As for US stockmarkets, given that the earnings season is slowly coming to an end, as most high profile companies have released their earningsreports, we expect traders’ interest to return to normal levels. Last but not least, we must note that gold’s price was on the rise, for a fourth consecutive week, as the precious metal benefited from the weakening of the greenback. Yet we expected actually gold’s reaction to be wider so, despite the directional part being as expected the quantitative part of gold’s ascent tended to disappoint us. We expect the negative correlation with the USD to be maintained in the coming week and could define gold’s direction.

If you have any general queries or comments relating to this article please send an email directly to our Research team at research_team@ironfx.com

Disclaimer:

This information is not considered as investment advice or an investment recommendation, but instead a marketing communication. IronFX is not responsible for any data or information provided by third parties referenced, or hyperlinked, in this communication.