The markets are in full swing with worries for a possible escalation of the Israeli conflict easing somewhat, yet still be present. On the monetary front, we note that a number of high ranked policymakers, from various central banks are scheduled to make statements throughout the week and may sway the market’s mood. As for financial releases we note the release on Monday of Japan’s corporate goods prices for October. On Tuesday, we get UK’s employment data for September, Sweden’s CPI rates for October, the Eurozone’s revised GDP rate for Q3, Germany’s ZEW indicators for November and we highlight the US CPI rates for October. On Wednesday we make a start with Japan’s revised GDP rate for Q3, China’s industrial output rate for October, UK’s CPI rates for the same month, Eurozone’s industrial output for September, the US PPI rates and retail sales, both for October and Canada’s September manufacturing sales for October. On Thursday we note the release of Japan’s trade data and Australia’s employment data, both for October, the weekly US initial jobless claims figure, the US November Philly Fed Index and October’s industrial production. On Friday we get UK’s retail sales, Eurozone’s final HICP rates and Canada’s producer prices, all being for October.

USD – October’s US CPI rates in sight

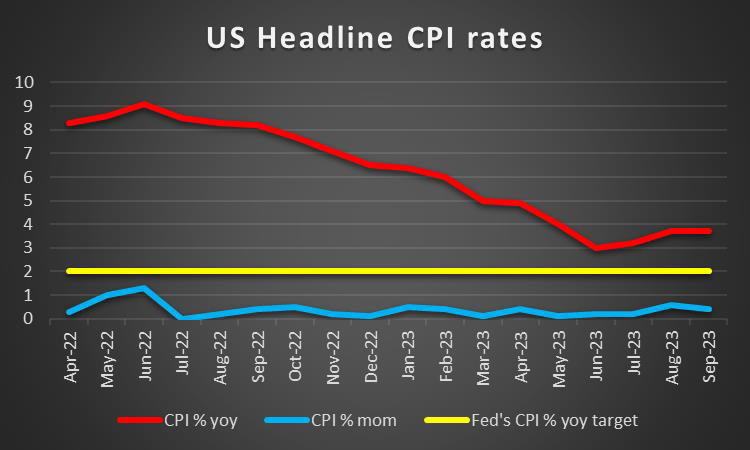

The USD seems about to end the week in the greens, regaining some of last week’s losses. On the monetary front we note that Fed Chairman Powell along with other Fed policymakers expressed some uncertainty on whether the Fed’s tightening is enough to combat inflationary pressures in the US economy. The statements come one week after the bank decided to pause its rate hiking path and were perceived as leaning on the hawkish side by the market. Nevertheless, we note that the market’s expectations that the bank has reached its terminal rate and may proceed with a rate cut in early summer next year seem to remain present, yet any further hawkish comments may contradict them and provide support for the USD. On a political level, we note that the possibility of a US government shutdown looms and in the next week we may see discussions for the issue arising and affecting the USD. On a deeper fundamental level, market worries for a slowdown of the US economy tend to persist to some degree. On a macro-economic level, we note that October’s US employment report showed some cracks in the US employment market. The US economy added 150,000 jobs in October, shy of the estimated 180,000, the unemployment rate ticked up to 3.9% from 3.8%, and wage growth slowed. The release tended to solidify the market’s expectations for the Fed to remain on hold and understandably weakened the USD. The next big test for the greenback is expected to be the release of the US CPI rates for

the same month and a possible failure of the rates to slow down may enhance hawkish tendencies within the Fed and thus support the USD.

GBP – Recession worries afloat

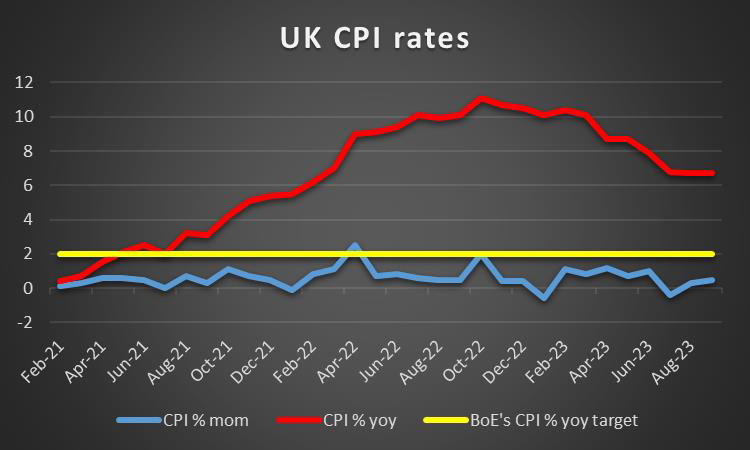

The pound is about to end the week lower than the USD, higher than JPY and EUR. On a fundamental level we still see the cost of living crisis as possibly the main issue for the UK economy, albeit market worries for a possible recession tend to also remain. Such worrιes tended to ease though, by the release of the GDP rates for Q3 which showed that the UK economy avoided a contraction. It should be noted that on a monetary level, the cumulative tightening of BoE’s monetary policy so far, has had a negative effect on growth as was expected. Furthermore the consecutive rate hikes seem to have eased inflationary pressures yet the CPI rate remains still very high and a far cry from BoE’s 2% target, which in turn tends to place more pressure on the BoE to act. For the time being we note that the market’s expectations are for BoE to remain on hold and proceed with a rate cut in Q3 24, underscoring that the bank may have reached its terminal rate. We note that BoE’s chief economist Huw Pill stated that it was essential that rates remain at their current level, which seemed like a hawkish shift. Any statements from BoE officials setting the prementioned market expectations into doubt by sounding more hawkish may provide some support for the GBP in the coming week. Nevertheless, inflationary pressures are still present and hence we highlight the release of the UK CPI rates for October on Wednesday and should rates not slow down further we may see the pressure on BoE intensifying.

JPY – Exit from ultra-loose monetary policy settings?

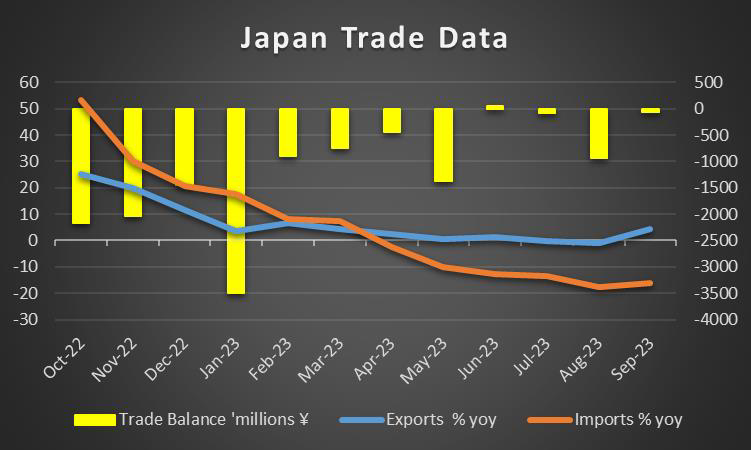

JPY is about to end another week lower against the USD, EUR and GBP in a sign of broader weakness. We still view BoJ’s ultra-loose monetary policy as the main factor behind JPY’s weakening. It should be noted that despite the bank signaling that the rise of wages is a prerequisite for an exit for the current settings, BoJ Governor Ueda stated according to Reuters “But in terms of how long we maintain our massive monetary easing … real wages don’t necessarily have to turn positive before that decision is made,”. Yet even that was not able to reverse the market sentiment and the market now requires more concrete steps on behalf of the bank. On a more fundamental level, we note that the Japanese currency may have also slipped due to an improved market sentiment and may have experienced some safe haven outflows, yet that seems to be of a secondary significance right now. Nevertheless, should the market sentiment improve in the coming week, possibly due also easing of market worries for the Israeli conflict, we may see it weighing on the JPY. Yet we remain worried for the weakening of the JPY as despite getting some respite after the release of the US employment report for October that allowed JPY to gain some points against the USD, USD/JPY has restarted its upward movement and is in a zone that may cause Japan to intervene in the market to JPY’s support. On a macroeconomic level we still are worried about the growth of the Japanese economy, given also its strong manufacturing orientation and hence highlight the release of the revised GDP rate for Q3 next Wednesday and a possible slowdown or even a contraction of the growth rate may intensify such worries and weigh on the JPY.

EUR – Fundamentals to lead the way

The common currency seems to have remained relatively unchanged against the USD, implying some resilience, given that it strengthened against the JPY and GBP. On a monetary level we maintain the view that ECB is to maintain its current interest rate level, for a prolonged period, practically something that is also anticipated from the market. We note that the bank seems convinced that the current level of rates could bring inflation back down to its 2% yoy target yet it was characteristic how Germany’s BuBa president and ECB policymaker Nagel, warned that the bank must remain vigilant as inflation may surprise the markets. Any talks for a possible rate cut were dismissed as being premature by the BuBa President in another sign of rates are to remain unchanged. We expect that ECB’s stance, given the surrounding circumstances at the time, to provide some support for the common currency. In the coming week, we expect the release of Eurozone’s final HICP rate for October to confirm the markable slowdown reported in the preliminary release, implying that ECB’s cumulative monetary policy tightening is working. Yet worries are surrounding economic activity and the revised GDP rate for Q3, is expected to verify the contraction of Eurozone’s economy on a quarterly level, which would be a sign that Eurozone’s economy is struggling and could intensify EUR trader’s worries for the economic outlook of the Zone.

AUD – RBA’s dovish hike

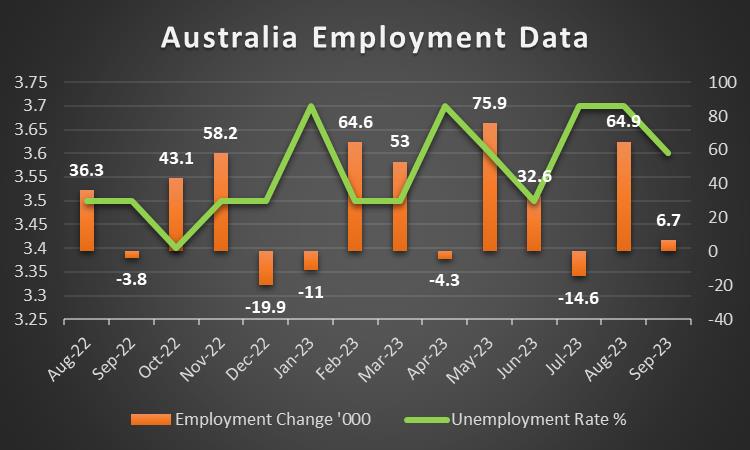

AUD is about to end the week lower against the USD and RBA’s dovish hike may have been key in AUD’s weakening. RBA in its interest rate decision decided to hike rates by 25 basis points yet in Governor Bullock’s statement refrained from locking in further rate hikes. The Governor in her statement recognised that inflation is still too high and that it remains persistent, possibly with slower easing than initially expected, yet also stated that the bank practically remains data dependent, thus weakening AUD. The bank failed to commit to another rate hike, with an easing of the hawkish tone characterising the banks’ prior decision, hence we tend to view the bank’s stance as weighing on the Aussie on a monetary level for the time being. On a fundamental level, we tend to have some worries for China’s data released last week as despite an acceleration of the import growth rate, which would imply more exports of Australian raw materials to China, the trade surplus narrowed substantially and the export growth rate slowed down. Further more, China show deflationary rates for October both on a consumer as well as on a producer level in an another sign of the headwinds faced by the Chinese economy in its efforts to recover. Further such signs for the Chinese economy could weigh on the Aussie given the close Sino-Australian economic ties. Hence in the coming week we highlight the release of China’s industrial output and urban investment growth rates, as well as Australia’s employment data, all being for October.

CAD – Financial data and oil prices may dictate CAD’s direction

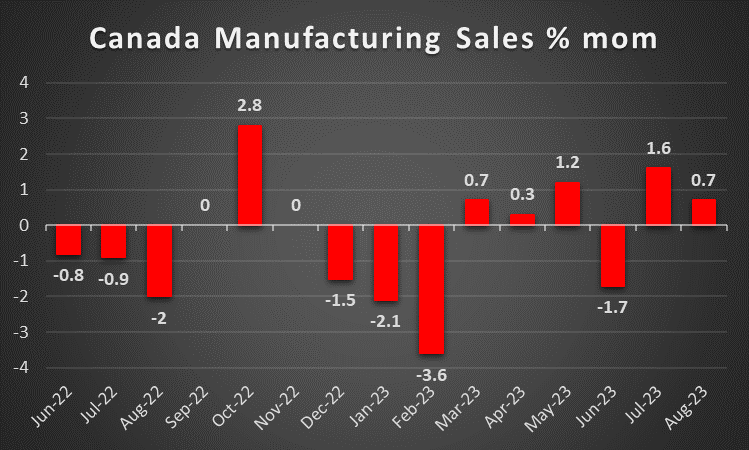

The Loonie ended the week lower against the USD and the drop of oil prices for the week may have been a key factor behind it. It should be noted that oil prices were driven lower as the US oil market seems to have presented a slack with US oil inventories rising, there were expensive worries for the demand side of the commodity especially from China, given its problems in growing its economy and market worries for the Israeli conflict seem to have eased given the intensification of calls for a ceasefire and humanitarian aid to Gaza. We expect that should oil prices continue to fall we may see the CAD slipping further, given that Canada is a major oil-producing country. On a deeper fundamental level, we note that the CAD failed to gain from the market sentiment and view that a more risk oriented approach by the market may support the commodity currency. On a monetary level, we note that the release of Bank of Canada’s Summary of Governing Council deliberations showed a split within the bank on whether another or more rate hikes would be required, yet failed to provide substantial support for the CAD. The market expects the bank to remain on hold until the early summer of next year and then proceed with a rate cut and should there be no signs of an intentions for another rate hike, we expect the bank’s stance to weigh on the CAD on a monetary level in the coming week. On a macroeconomic level, we note that September’s trade data were quite favourable as the trade surplus widened considerably implying growth of the Canadian economy from its international trading transactions, yet the wide contraction of the building permits growth rate also for September, tended to create some worries. In the coming week we have a number of medium impact financial releases which could affect the CAD’s direction.

General Comment

In the coming week we expect that the release of the US CPI rates may allow the USD to gain on attention. Yet financial releases are spread throughout from various countries and may allow other currencies to come under the spotlight at certain points during the week. As for US stockmarkets we may see a shift in the market’s attention as we get the earnings reports of a number of retail companies. We note that on Tuesday we get the earnings report of Home Depot (#HD), on Wednesday JD.Com (#JD) and on Thursday it’s the turn of Ali Baba (#BABA) and Walmart (#WMT). Yet the releases are not only to show the health of the companies mentioned, but given the fact that the companies are in the retail sector, the releases may provide a picture of the demand side of the US economy. Overall though, should the market sentiment be positive, we may see some support for US stockmarkets. As for precious metals, we note that the bearish tendencies for gold’s price intensified, partially possibly also due to the strengthening of the USD. Overall we note that the negative corelation of the USD to gold’s price seems to have reemerged, yet is still not as strong. We have to note though that gold’s price dropped despite US yields also dropping, which should provide some support for the gold’s price. Furthermore, the precious metal may have also experienced some safe haven outflows given the easing of market worries for the Israeli conflict.

If you have any general queries or comments relating to this article please send an email directly to our Research team at research_team@ironfx.com

Disclaimer:

This information is not considered as investment advice or an investment recommendation, but instead a marketing communication. IronFX is not responsible for any data or information provided by third parties referenced, or hyperlinked, in this communication.