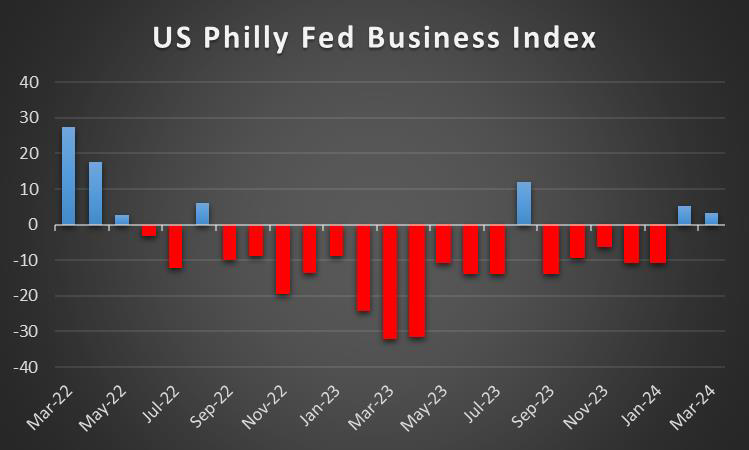

As the week draws to a close let’s have a look at what’s scheduled next week. On the monetary front, we note the release of the speech by BoE Governor Bailey on Tuesday and the release of the Fed’s beige book on Wednesday. As for financial releases, we get on Monday Japan’s Machinery orders rate for February and Chain store sales rate for March, followed by Turkey’s Unemployment rate and the Eurozone’s Industrial rate both for the month of March. Later on, we get the US NY Fed Manufacturing figure for April and the US Retail sales rate for March. On Tuesday, we make a start with China’s industrial output rate for March, China’s GDP rate for Q1, the UK’s Unemployment data for February, Germany’s ZEW figures for April, Canada’s Housing starts figure and CPI rates followed by the US Industrial production rate, all for the month of March. On Wednesday we begin with New Zealand’s CPI rate for Q1, followed by Japan’s Tankan Non-Manufacturing and Manufacturing figures for April, followed by Japan’s trade balance for March. Later on in the day, we get the UK’s CPI rates and the Eurozone’s final HICP rate all for the month of March. On Thursday we start with Australia’s Employment data for March, the US weekly initial jobless claims figure, the US Philly Fed Business index figure for April and the US existing home sales figure for March. On Friday, we note Japan’s CPI rates for March, Germany’s producer prices rate and UK retail sales rate both for the month of March.

USD – US CPI rates unexpectedly tick up

After a roller coaster ride the greenback is about to end the week substantially stronger than its counterparts. The USD proved to be the main market mover in the FX market and the factor causing the greenback to change direction, appears to have been the release of the US CPI rates for March. On Monday we saw the greenback weakening, despite the US Employment report coming in hotter than expected for a third month in a row. Yet the highlight of the week may have been the release of the US CPI rates for Mach. In particular, the Core CPI rate came in higher than expected at 3.8% implying persistent inflationary pressures in the US economy. Yet the greatest shock in our opinion, was the headline CPI rate which accelerated to 3.5%, implying that not only is inflation persistent in the US economy,but it is also intensifying. The risks of inflationary pressures remaining entrenched in the US economy, may add pressure on the Fed to adopt a hawkish stance appears to be increasing. Moreover, the US Employment data for March which was released last Friday came in better than expected, implying a resilient labour market and in particular the Non-Farm Payrolls figure which vastly exceeded expectations by coming in at 303k versus the expected 212k. Therefore with the prospects of the US economy remaining resilient despite the restrictive financial environment, the dollar appears to have more than recovered its losses since last Wednesday. On the monetary front, we note the comments of Chicago Fed President Goolsbee, who stated following the release of the CPI rates that “we need to be humble about how easy it is to get there”, when reffering to the Fed’s progress in combating inflation. Hence, Chicago Fed President Goolsbee’s comments could be perceived as slightly hawkish, as he appears to be implying that interest rates may need to stay at the current levels for a longer period of time. Furthermore, this sentiment appears to have been seen as well in the bank’s March meeting minutes, released on Wednesday in which policymakers stated their concerns about “uneven” progress in combating inflationary pressures in the US economy. Moreover, it was stated that “the bank did not deem that it would be appropriate to reduce the target range until they had “gained greater confidence that inflation was moving sustainably toward 2 per cent”, implying that interest rates may stay at their current levels for a prolonged period of time. Overall, we anticipate the dollar to maintain its bullish momentum in the upcoming week following the hawkish innuendos on a monetary level and the resilient inflation data as seen earlier on this week.

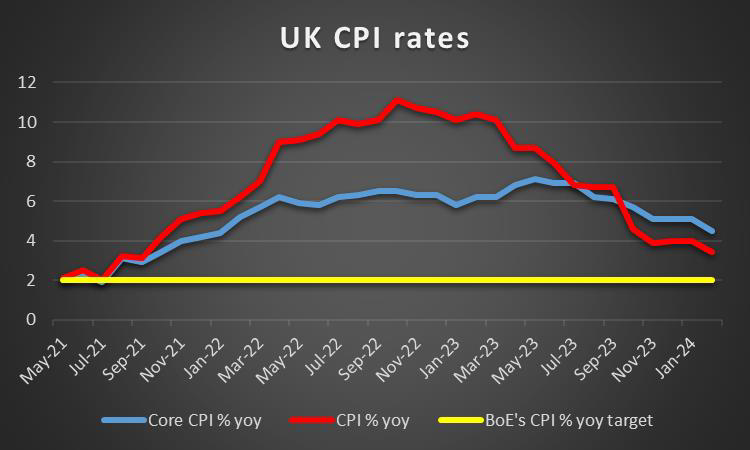

GBP – UK’s CPI rates to move the pound

The pound is about to end the week relatively weaker against the USD yet stronger against the EUR and unchanged against the JPY. On a fundamental level, we note the report by AllianzTrade which estimates that the additional costs on importing animal and plant products into Dover set to go into effect on the 30th of April, could hike costs to businesses by 10% in its first year. The increased costs could add to inflationary pressures in the UK economy. On a macroeconomic level, we note a relatively quiet week in terms of financial releases stemming from the UK. Yet pound traders may be interested in next week’s releases, and in particular the UK’s Employment data for February on Tuesday and the CPI rates for March on Wednesday. Should the financial releases imply that the UK economy remains resilient and that the risk of inflationary pressures remain elavated, then we may see the pound strengthening as pressure may mount on the BoE to keep interest rates high for longer. Whereas any other scenario could weigh on the pound. On a monetary level, the current market expectations are for the bank to cut interest rates twice this year, with the first being in August, thus should the CPI rates come in higher than expected, we may see market expectations shifting to a potential rate cut even later on this year which could support the pound. A view which appears to be supported by BoE policymaker Greene, who stated in the FT on Thursday that interest rate cuts “should still be a way off” and that “the markets are moving rate cut bets in the wrong direction”. The policymaker’s comments could be perceived as hawkish in nature, as the policymaker implies that monetary policy may need to remain restrictive for a prolonged period of time, which in turn could provide support for the pound. Thus should more policymakers opt to join the “hawks”, it could further support the pound. Lastly, we would like to note the release of the UK’s retail sales rate for March next Friday, but we anticipate that its release may be of lesser importance when compared to the release of the UK’s CPI rates earlier on in the week.

JPY – Government intervention?

JPY is about to end the week in the reds against the dollar, yet relatively unchanged against the GBP and stronger against the EUR. On a macroeconomic level, we note that no major financial releases emerged from Japan during this week with the exception of Japan’s Current account figure for February which was released on Monday. The figure came in higher than last month’s figure by coming in at 2.644T versus 0.438T implying that Japan’s trade surplus has increased which could be seen as bullish for the JPY. However, the figure failed to meet market expectations of 3.112T and thus despite improving, it seems to have fallen slightly short of the target set by economists, thus potentially weighing on the JPY. On the monetary front, we note the speech by BOJ Governor Ueda on Tuesday who according to Reuters, stated that “the central bank must consider whittling down stimulus further if inflation continues to accelerate”. The comments could be perceived, as a vote of confidence for the Japanese economic outlook, with the Governor stating that solid pay hikes will likely boost household income and consumption which could drive inflationary forces higher in the future. The underlying risk of inflation accelerating in the months to come could aid current market expectations for another rate hike by the BOJ in the June meeting and could end up boosting the probabilities for further hikes down the line. On the other hand, the bank’s ambition for increased consumption by Japanese households, appears to be debatable, as the most recent financial release of Japan’s household confidence figure for March, came in lower than expected. Moreover, Japan’s economy watchers’ current index figure for March came in at 49.8, implying a slightly pessimistic view from the consumer side of the Japanese economy, which could hinder BOJ Governor Ueda’s hopes of increased consumption in the economy. On a more fundamental level, we note that given that JPY remains near quite low levels against the USD, the possibility that the Japanese government may proceed with a market intervention operation to the Yen’s defence, is still present.

EUR – ECB remains on hold

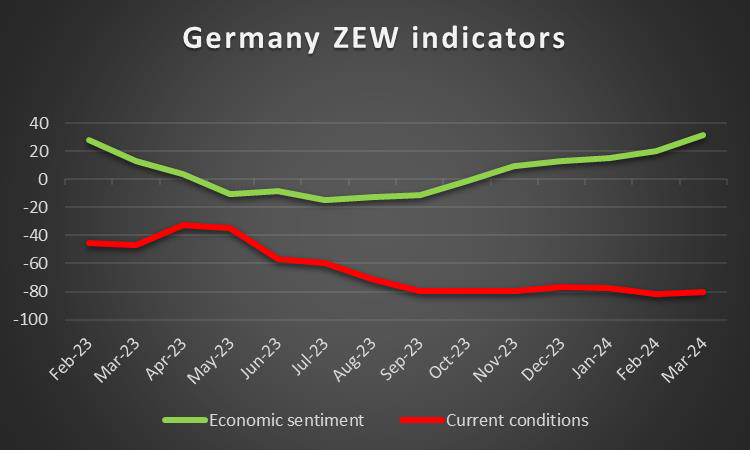

The common currency is about to end the week in the reds against the USD, JPY and GBP in a sign of general weakness. The ECB during their monetary policy meeting on Thursday remained on hold as was widely expected, yet the initial market reaction appears to have been slightly dovish, as some dovish signals appear to have emerged from the bank’s accompanying statement. In particular, we highlight the section in which the bank stated that “If the Governing Council’s updated assessment of the inflation outlook…were to further increase its confidence that inflation is converging to the target in a sustained manner, it would be appropriate to reduce the current level of monetary policy restriction”. Implying that the bank may be preparing to cut interest rates, yet is unwilling to pre-commit to a “particular rate path”. The aforementioned comments were re-stated by ECB President Lagarde during her press conference, following the bank’s decision. Overall, the accompanying statement and press conference, could be described as relatively neutral in their tone, yet appear to have struck a dovish tone with market participants. Should the ECB’s current monetary policy stance continue to feed through into the economy by reducing inflationary pressures, we would not be surprised to see the first rate cut by the ECB in their June meeting. Yet, we would push back against the notion made by ECB Stournaras’s comments of the ECB cutting twice before August, as being unrealistic. On the macro-economic front, we note a relatively quiet week in the Eurozone, yet interest in the EUR may pick up in the upcoming week. In particular, the release of Germany’s ZEW figures may be of interest to EUR traders, as they may provide insight to the consumer’s perspective of one of Europe’s largest economies. Therefore, should the sentiment appear to be pessimistic, it could weigh on the EUR and vice versa.

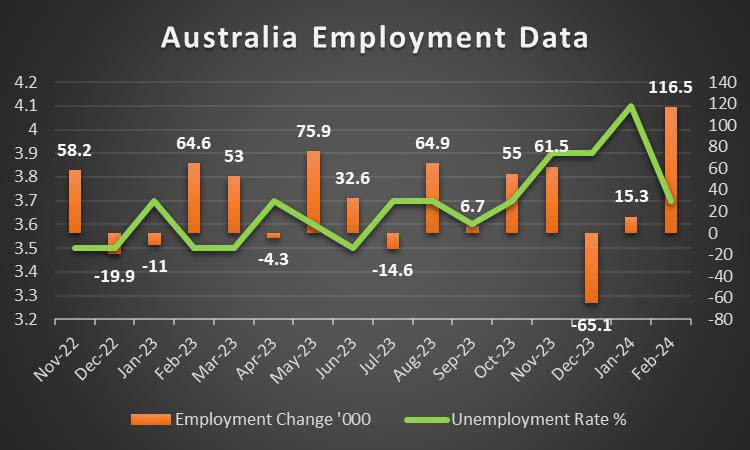

AUD – Fundamentals continue to lead the Aussie

AUD is about to end the week lower against the USD. On a fundamental level, we note the statement by Chinese President Xi on Wednesday who stated that nobody can stop the “family reunion” with Taiwan. In our view, this “family reunion” may not be as peaceful as President Xi would like, and thus should the military aggresion by China against increasing in the upcoming week, it could fundamentally weigh on the AUD as well. Furthermore we note the close Sino Australian economic ties and any improvement in the Chinese macroeconomic outlook could provide some support for the Aussie as well as it would imply more exports of raw materials from Australia to China. Hence we highlight the release of China’s CPI and PPI rates both for March which showcased a decrease of consumption in the economy and a reduction in demand for manufacturing goods, implying a decrease in economic activity . Next week we may see AUD traders keeping a close eye on the release of China’s GDP rate for Q1 and Australia’s Employment data for March on Thursday. A resilient labour market in Australia, could lead to increase consumer spending in the economy and thus, potentially aiding inflationary pressures. In such a scenario, it could increase pressure on the RBA to maintain a hawkish tone, which could aid the Aussie. Moreover, should China’s GDP rate come in lower than expected, implying that the economic situation in China is deteriorating, it could fuel speculation for a future reduction in demand for Australian raw materials, and thus may weigh on the Aussie. On the flip side, a better than expected Chinese GDP rate for Q1, could boost optimism about China’s recovery prosectes and thus a potential increase in demand for raw materials from Australia, which in turn could provide support for the AUD.

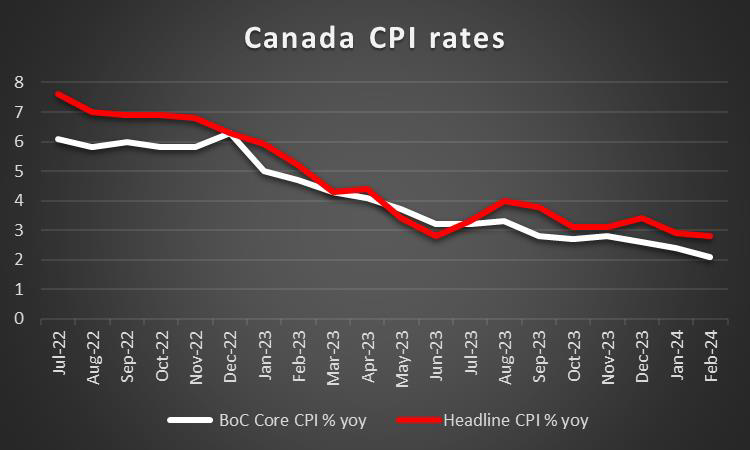

CAD – Canada’s CPI rates eyed

The CAD is about to end the week relatively significantly lower against the USD. On a fundamental level, we may see Loonie traders keeping a close eye over the course of oil prices given the positive correlation of oil with CAD, as Canada is a major oil-producing economy. Oil prices moved slightly lower during the week as supply side worries regarding the international oil market, appear to have eased slightly. Yet, the risks of a retaliation from Iran against Israel remain elevated and as such, may be supporting oil prices. In our opinion, we would not be surprised if a proxy attack on Israel occurs within the next week, which in turn could increase volatility in the region and could boost oil prices from a supply-side perspective. On a macroeconomic perspective we note Canada’s employment data for March which was released last Friday, which came in lower than expected and prompted the comment by the BoC in its accompanying statement that “A broad range of indicators suggest that labour market conditions continue to ease”. On the monetary front the bank remained on hold as was widely expected, keeping interest rates at 5.00%. We also note the market’s expectations for the bank to start cutting rates in its June meeting have remained, as the bank also stated when referring to inflation that “the Council will be looking for evidence that this downward momentum is sustained”, which could imply that the door for a June rate cut remains open, which appears to have weighed on the Loonie. Furthermore, BoC Governor Tiff Macklem seems to have confirmed this possibility during the press conference, following the bank’s decision in which he stated that “an interest rate cut in June is possible”. Therefore, should Canada’s CPI rate for March which is due to be released next week, verify the bank’s expectations of easing inflationary pressures in the Canadian economy, it could further weigh on the Loonie.

General Comment

Overall we expect that volatility in the FX market is to be maintained given that we have a high number of high-impact financial releases. We also expect that the USD may cede its driver’s seat in the FX market to its counterparts, who may have more high-impact financial releases. As for US stock markets, we note that US stock markets seem to be sending some mixed signals this week. We also note that equities may start generating more interest, as the earnings season kicks off later on today with major banks such as City Group (#C), JPMorgan (#JPM) and Wells Fargo (#WFC) releasing their earnings reports. As for gold, we note that the precious metal continues printing new record high levels, with its most recent ATH figure standing at $2363 per troy ounce, and is about to end in the greens for a third week in a row. We expect the divergence between the USD with gold’s price to be maintained in the upcoming week, yet also the path of US yields could influence the precious metal’s direction as could safe haven flows.

If you have any general queries or comments relating to this article please send an email directly to our Research team at research_team@ironfx.com

Disclaimer:

This information is not considered as investment advice or an investment recommendation, but instead a marketing communication. IronFX is not responsible for any data or information provided by third parties referenced, or hyperlinked, in this communication.