US stock markets tumbled yesterday as traders returned from their holidays ahead of the release of the US employment report for August on Friday. Market worries for growth not only in China but the US as well tended to intensify, while NVIDIA fell more than 9% dragging US stockmarkets lower as a whole and souring the market mood even further. In the European markets we note that Volkswagen’s considerations to close down factories in Germany for the first time caused a public outcry. We are also to have a look at APPLE’s “It’s Glowtime” event and for a rounder view conclude the report with a technical analysis of Dow Jones’ daily chart.

US August employment data

We highlight on Friday, the release of the US employment report for August, which is expected to have ripple effects beyond the FX market also on US stockmarkets. Forecasts are for the non-farm payrolls figure to rise and reach 160k if compared to July’s 114k. The unemployment rate is expected to tick down to 4.2% if compared to 4.3% in July and the average earnings growth rate to accelerate slightly reaching 3.7%yoy if compared to last month’s 3.6% yoy. Should the actual rates and figures meet their respective forecasts, we may see the data aligning towards pointing a tightening US employment market. A possible tightening of the US employment market could also allow the Fed to ease its dovish intentions to procced with extensive rate cuts in the coming months. In turn we note that currently the market expects the bank to lower interest rates by 1% by Christmas. Such expectations imply a double rate cut by the bank, possibly in the November meeting. Should the Fed be encouraged by a tighter US employment market to cut rates to a lesser extent, we may see the market being forced to reposition itself, in turn weighing on US stock markets. On the flip side should the rates and figures show that July’s slack in the US employment market remained or has even widened in August, we may see

US stock markets getting substantial support. Please note that Fed Chairman Powell in his speech at the Jackson Hole Economic Symposium, mentioned the shift in the bank’s attention from curbing inflationary pressures to the weakening US labour market, which in turn could enhance the impact of the release.

NVIDIA

Maybe the most characteristic bearish move yesterday was the drop of NVIDIA’s share price. It should be noted that the company got a subpoena from the US Department of Justice as part of an antitrust probe, regarding the company’s practices. The subpoena is an issue by itself as US officials worry that NVIDIA, is hardening its stance in regards of switching from its chips to competitors and tends to punish any client who does not use exclusively its chips. Should the probe deepen further or even create negative repercussions for the chip maker, we may see an adverse effect on NVIDIA’s share price. Yet we see the drop of NVIDIA’s share price as an expression of the doubts and second thoughts of market participants for the prospects of Artificial Intelligence in general and NVIDIA specifically.

Volkswagen to close plants in Germany?

The revelation that Volkswagen is considering closing plants in Germany for the first time in its 83 year history, caused a public outcry for the company. Analysts mention the possibility that VW may close down factories in Dresden and Osnabrück. The company is facing intense competition, especially in China where BYD’s electric vehicles seem to dominate the market. Efforts are concentrated in cutting jobs, an issue which is expected to find intense headwinds from the strong union IG Metall. It should be noted that the company had agreed to a job-shielding agreement in 1994, which spans until 2029. It should be noted that the issue tends also to have a political aspect at a regional and national level. Should we see market worries for the outlook of the company intensifying, we may see it having a bearish effect on its share price, yet the issue could also have wider bearish implications for German stock markets.

APPLE’s event

The selloff in US equities markets has also affected Apple’s (#AAPL) share price yesterday. Please note that the company is to have the 2024 Apple “It’s Glowtime” event on the 9th of September, when the company is expected to debut the first generative AI iPhone. In the event we expect an enhancement of Apple Intelligence and Siri, possibly available across the new iPhone line. Also higher definition is expected while focus may also be placed on longer lasting batteries. Also we would not be surprised to see updated versions of hardware such as iPods yet tend to expect new Macs at a later stage. Overall, shall we see the event exciting tech experts and consumers we may see a bullish effect on Apple’s share price and vice versa.

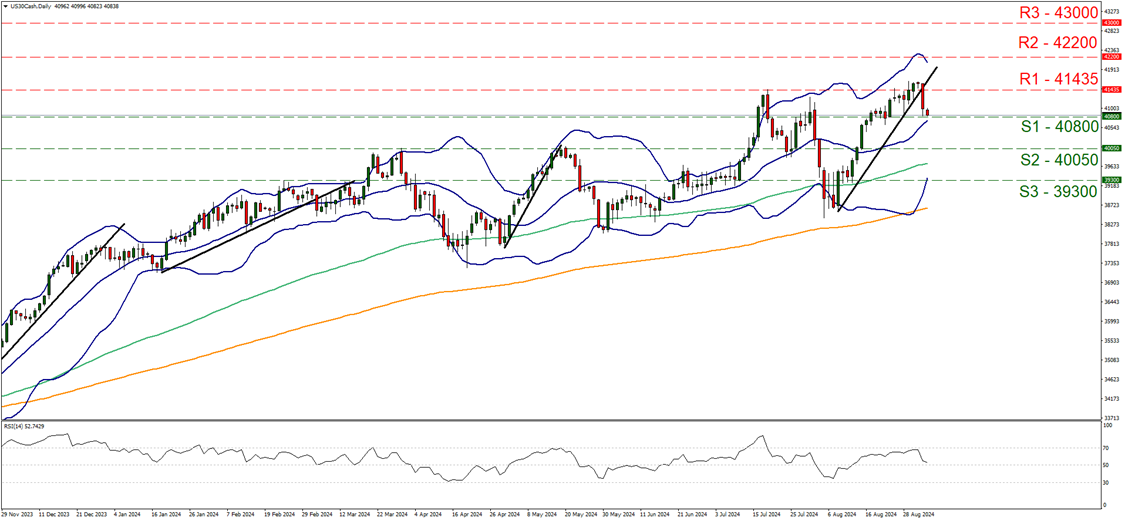

TECHNISCHE ANALYSE

US 30 Cash Daily Chart

- Support: 40800 (S1), 40050 (S2), 39300 (S3)

- Resistance: 41435 (R1), 42200 (R2), 43000 (R3)

Dow Jones tumbled yesterday breaking the 41435 (R1) support line, now turned to resistance and continued lower testing the 40800 (S1) support level. Given that the downward motion of the index, clearly broke the upward trendline guiding it since the 8th of August, we switch our bullish outlook in favour of a sideways motion bias initially. Also the RSI indicator dropped from the highs of almost 70 to just above the reading of 50 implying that the bullish sentiment of the market eased if not has faded away. Yet the drop of the RSI also implies that a bearish sentiment has yet to be build up. For a bearish outlook we would require index’s price action to break clearly the 40800 (S1) support line and start aiming for the 40050 (S2) support base. Even lower we note the 39300 (S3) support barrier. Should the bulls regain control over the index, we may see it breaking the 41435 (R1) resistance line and set as the next possible target for the bulls the 42200 (R2) resistance level.

If you have any general queries or comments relating to this article please send an email directly to our Research team at research_team@ironfx.com

Disclaimer:

This information is not considered as investment advice or an investment recommendation, but instead a marketing communication. IronFX is not responsible for any data or information provided by third parties referenced, or hyperlinked, in this communication.