The week is about to reach its end and we take a pip look at what is next week’s calendar. On the monetary front we note on Tuesday the release of the RBA’s June meeting minutes and the speeches by Fed Chair Powell and ECB President Lagarde. On Wednesday we get the Fed’s June meeting minutes.As for financial releases, on Monday we get Japan’s Tankan Big Mfg and Non-Mfg index figures for Q2, followed by China’s Caixin manufacturing PMI figure for June, Germany’s preliminary HICP rate for June and the US ISM Manufacturing PMI figure for June as well. On Tuesday we get the Eurozone’s preliminary HICP rate for June, followed by Canada’s manufacturing PMI figure for June as well and ending off the day is the US JOLTS Job openings figure for May. On Wednesday, we get Australia’s building approvals figure and Retail sales rate both for the month of May , followed by Turkey’s CPI rate for June, the Eurozone’s final composite PMI figure, the UK final services PMI and the US ADP employment figure all for the month of June, followed by the US weekly initial jobless claims figure, Canada’s trade balance figure and the US factory orders rate both for May and ending off the day is the US ISM Non Manufacturing PMI figure for June. On Thursday, we get Germany’s industrial orders rate for May, and Switzerland’s CPI rate for June. On Friday, we get Japan’s household spending rate and Germany’s Industrial order rate both for May. Furthermore, we get the UK’s Halifax house prices figure for June, Sweden’s GDO rate for May, the US Employment data for June and Canada’s employment data for June as well.

USD – US Employment data next week

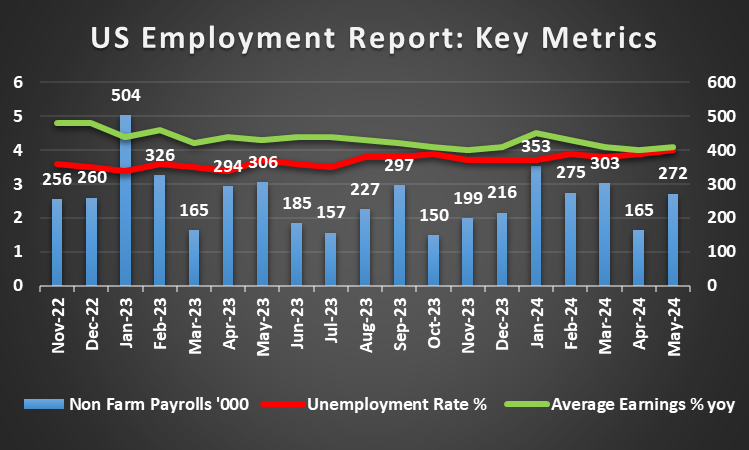

The USD seems to be about to end the week relatively unchanged against its counterparts. On a fundamental level, we note that the greenback could enjoy some safe haven inflows in the coming week as tensions appear to be rising in the Middle East, as Israel and Hezbollah move closer towards a full-out war with one another. On a monetary policy level, we note that Fed policymakers seem to be amplifying the rhetoric for patience regarding any rate cuts, with some being also open to the possibility of another rate hike.In particular, Fed Governor Bowman stated earlier on this week that she was open to raising interest rates if the progress in battling inflationary pressures does not improve. As such, should the Fed’s June meeting minutes which are set to be released next week, also showcase a desire by policymakers to maintain interest rates for a prolonged period of time, we may see the dollar strengthening. On a macroeconomic level, the US core durable goods orders came in lower than expected, implying that US businesses are less willing to invest in the economy. However, the highlight of the week which is the US Core PCE rate for May which is the Fed’s favourite tool for measuring inflationary pressures in the US economy, has not yet been released. Should the Core and headline PCE rates slow down we may see the USD weakening as it would imply an easing of inflationary pressures in the US economy and could enhance market expectations for the Fed to proceed with two rate cuts in the year. As for financial releases, the highlight of next week is set to be the US Employment data for June, which is expected to showcase a loosening labour market when looking at the Non-Farm Payrolls figure which is expected to decrease to 180k from 272k. Yet the unemployment rate which is expected to remain at 4% may cast some doubt on the aforementioned scenario. Nonetheless, should the US Employment showcase a loosening labour market, it could weigh on the dollar and vice versa.

GBP – UK General Election next week

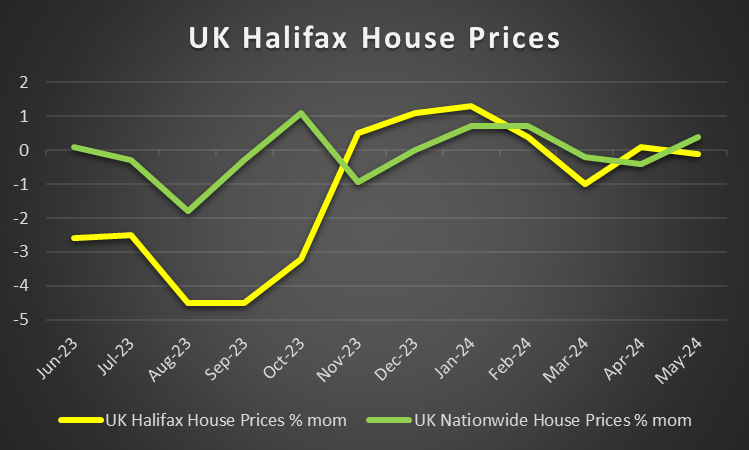

GBP seems about end the week in the greens against the USD and JPY but lower than the EUR. On a fundamental level, the UK’s general election is next to take place next week on the 4th of July, with Labour enjoying a comfortable lead against the Conservatives. On a monetary level, we note a relatively quiet week from BoE officials. Overall, we do not anticipate any significant remarks from BoE officials before the general elections in order to maintain their impartiality. On a macroeconomic level, we note that the pound may cede some control over its direction, as the financial releases stemming from the UK may be overshadowed from releases arising from the US. Nonetheless, for next week pound traders may be interested in the release of the UK’s final services PMI figure for June and the UK’s Halifax house prices rate for June as well. Should the final service PMI figure come in better than expected implying that the services sector of the UK economy has continued to expand, it could potentially provide support for the pound. On the flip side, should it come in lower than expected it could weigh on the pound.

JPY – JPY Intervention on the horizon?

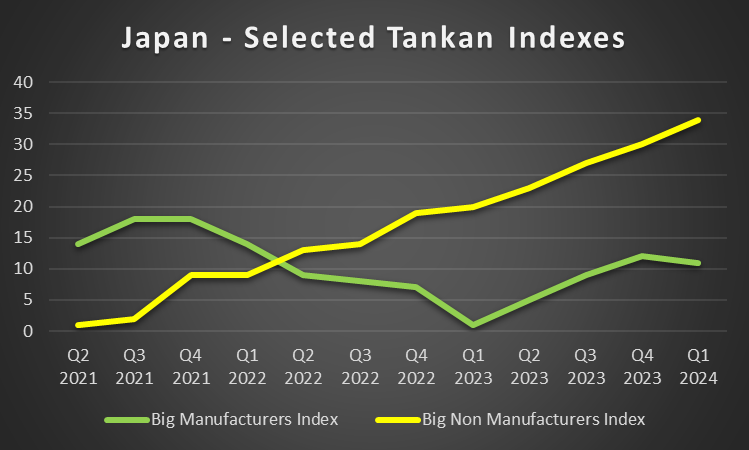

JPY seems about to end the week in the reds against the EUR and USD but stronger than the GBP. We make a start for JPY by noting that on a fundamental basis, the Yen could gain safe haven inflows should tensions in the region escalate between Manilla and Beijing who saw a physical confrontation earlier on this week between personnel from both nations. For the time being though the main factor behind JPY’s direction could be BoJ’s monetary policy. In particular, the bank’s summary of opinions at their June monetary policy meeting stated that “If the outlook for economic activity and prices presented in the April Outlook Report will be realized and underlying inflation will increase, the Bank will raise the policy interest rate and adjust the degree of monetary accommodation.” The comments could be regarded as hawkish in nature, with policymakers clearly stating a willingness to raise interest rates higher, which in turn may aid the JPY. On a macroeconomic level, we would like to highlight the release of the BOJ’s Core CPI rate for June which came in higher than expected at 2.1% versus the expected rate of 1.9%. Yet despite the higherthan-expected rate, the Yen only gained temporarily. On another note, it should be noted that JPY’s continued weakening over the past week has led it to exceed levels at which the last market intervention measures were taken to support the Yen. Hence as JPY continues to slip, the chances of market intervention are increasing. On a macroeconomic level, we note the release of Japan’s Tankan Big manufacturing and non-manufacturing index figures for Q2. Should they come in higher than expected they could support the JPY, whereas any figure lower than what is currently anticipated by economists may weigh on the JPY.

EUR – France’s parliamentary elections on Sunday

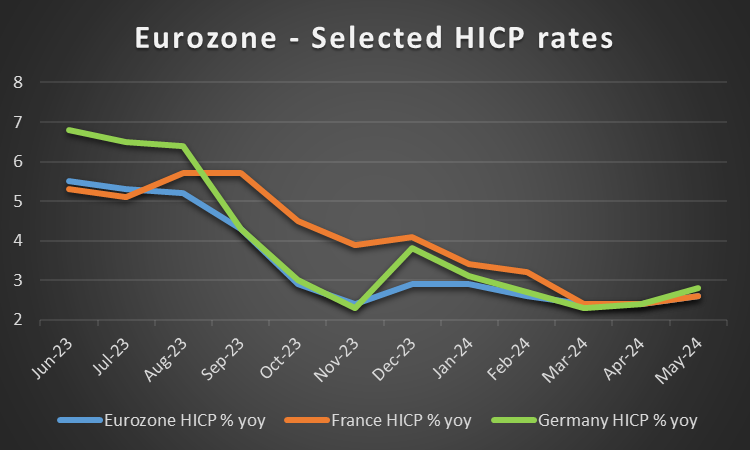

The EUR is about to end the week higher against the USD, the GBP and JPY. On a fundamental level, we note that the result of the EU Parliament elections seems to be intensifying centrifuge forces within the EU. The first round of the elections are set to take place this Sunday, with the euro-sceptic parties set to make tremendous gains. In particular, a recent survey, by France 24 has Marine Le Pen’s party ‘RN’ at over 35%, with the leftist coalition trailing at 29% and Macron’s party at third place with around 20% . Overall, the uncertainty characterising the overall European political outlook may weigh on the common currency next week. Besides the uncertainty of the EU political outlook, on a fundamental level we also highlight the escalating trading war between the EU and China. It should be noted that the EU has announced that it will be imposing tariffs on Chinese EVs. Should the trade war escalate, we may see the common currency slipping. On a monetary policy level, we note the remarks by ECB policymaker Kazimir who stated that “we can expect one more rate cut this year”. The comment could be interpreted as slightly dovish in nature, as it implies that the bank may cut rates again by the end of the year. However, the current market’s expectations are for the ECB to cut rates in the September and the December meetings. As such the implications of only one rate cut, could instead be perceived as relatively hawkish in nature, which could aid the EUR. Overall though the path for ECB’s rates remains on its downwards trajectory and that may be enhancing the bearish sentiment somewhat. On a macroeconomic level, we note the release of Germany’s Ifo figures for June which came in lower than expected. The lower than expected figures may imply a deterioration in the confidence in the German economy, which despite their bearish implications, failed to have any impact on the EUR. Nonetheless, for next week we would like to note Germany’s preliminary HICP rate and the Zone’s preliminary HICP rate both for the month of June, in addition to Germany’s industrial output rate for May.

AUD – May’s CPI rate showcases an acceleration in inflationary pressures

AUD is about to end for a third week in a row, in the greens against the USD. On a fundamental level, it should be noted that AUD as a commodity currency is particularly sensitive to the market’s mood. Should we see the market turning more cautious, AUD may lose ground and vice versa. Also on a fundamental level, we note that the Aussie could suffer some losses should tensions in the US-Sino relationships escalate further, given that China is the main trading partner of Australia. On a monetary level, we note the comments made by RBA Assistant Gover Kent who emphasized that the bank’s monetary policy remains restrictive. Yet, did also state that the extent to which they remain restrictive remains “unclear”. As such, the comments could be interpreted as the RBA keeping interest rates higher for longer, should the bank fail to see further progress on inflationary pressures. Therefore, should further RBA policymakers adopt a more hawkish tone, we may see the Aussie gaining. In the coming week, we highlight the release of Australia’s RBA June meeting minutes, in which should it showcase a willingness by RBA policymakers to maintain interest rates higher for longer, or having entertained the thought of a rate hike in the future, we may see the Aussie gaining. Moreover, in terms of financial releases, we would like to note Australia’s retail sales rate as a gauge of the resilience of the Australian consumer. Should the rate for May come in lower than the prior rate of 0.1% or even enter negative territory, implying consumer spending has decreased, it could weigh on the AUD and vice versa. Lastly, given Australia’s close economic ties with China, we would like to note the release of China’s Caixin manufacturing PMI, which should it imply an expansion in manufacturing activity in China, it could also imply that demand for Australia’s raw materials may also increase. Such a scenario may provide support for the AUD and vice versa.

CAD – Loonie traders focus on the release of May’s CPI rates

The CAD is about to end the week relatively unchanged against the USD. On a fundamental level, we note that the Loonie as a commodity currency is considered to be of riskier nature and thus more sensitive to the market sentiment. Should the market sentiment turn more risk oriented we may see the CAD getting some support and vice versa. The CAD is especially sensitive to the path of oil prices, given that Canada is a major oil producing economy. It should be noted that oil prices currently seem to have been the on the rise in the past week, as tensions in the Middle East continue to increase. For the time being, should oil prices continue on their ascent, we may see the CAD gaining as well, given the market’s perception for a positive correlation of the CAD with oil prices. On a monetary policy level, we note the comments made by BoC Governor Tiff Macklem earlier on this week, in which he stated that “there is room for the Canadian economy to grow and add more jobs even as inflation continues to move closer to the target”, implying that the Canadian economy is on track for a soft landing scenario. Nonetheless, the comments may be regarded as slightly dovish in nature, which could weigh on the Loonie.On a macroeconomic level, we highlight the release of Canada’s employment data for June next week. Should the employment data showcase a resilient labour market we may see the Loonie gaining and vice versa. Yet, with BoC Governor Tiff Macklems recent comments, even if the labour market showcases resiliency it may not significantly impact the bank’s monetary policy.

General Comment

As a closing comment, we expect volatility in the coming week to increase significantly, and the USD to regain the initiative and regain its dominance in the FX market, as the gravity and frequency of US financial data tends to increase. As for US stock markets, we note that the NASDAQ ,S&P 500 and Dow Jones 30 appear to be on track to end the week in the greens. Yet the Dow Jones still maintains its relatively sideways motion. We tend to highlight the risk that the market may have gotten ahead of itself and fundamentals may not be able to sustain the rally, especially given that the Fed is hesitant to start cutting rates. As for gold, we note that the negative correlation of gold prices to the USD seems to have resumed. It should be noted despite the initial rise of US yields earlier on in the week, the gains appear to have been erased at the time of this report and thus may have not predominantly influenced gold’s price.

If you have any general queries or comments relating to this article please send an email directly to our Research team at research_team@ironfx.com

Disclaimer:

This information is not considered as investment advice or an investment recommendation, but instead a marketing communication. IronFX is not responsible for any data or information provided by third parties referenced, or hyperlinked, in this communication.