The week is slowly drawing to a close as we open a window at what next week has in store for the markets. On the monetary front, we note the BoC’s interest rate decision on Wednesday and the ECB’s interest rate decision on Thursday. As for financial releases, on Monday we get Australia’s Judo bank final manufacturing PMI figure, China’s Caixin Manufacturing final PMI figure, Turkey’s CPI rates, Germany’s HCOB Manufacturing PMI, the UK’s, Canada’s , the US’s Final S&P Manufacturing PMI figure in addition to the US ISM Manufacturing PMI figure, all for the month of May. On Tuesday, we get Switzerland’s CPI rates for May, followed by the US Factory orders rate for April and JOLTS Job openings figure for April. On Wednesday, we get Australia’s GDP rates for Q1, China’s Caixin Services PMI figure, France’s HCOB Services PMI figure and the Eurozone’s HCOB Final composite PMI figure and the US ADP Non Farm Employment figure all for the month of May and ending of the day is the US ISM Non-Manufacturing PMI figure for May. On Thursday, we get Germany’s industrial orders rate, the Czech Republic’s and Canada’s trade balance figures both for April and Canada’s Ivey PMI figure for May. On a busy Friday, we get China’s trade balance figure for May, followed by Germany’s industrial production rate for April, the UK’s Halifax House prices rate for May, the Eurozone’s revised GDP rates for Q1, the US Non-Farm Payrolls figure and Employment data for May and Canada’s Unemployment rate also for May.

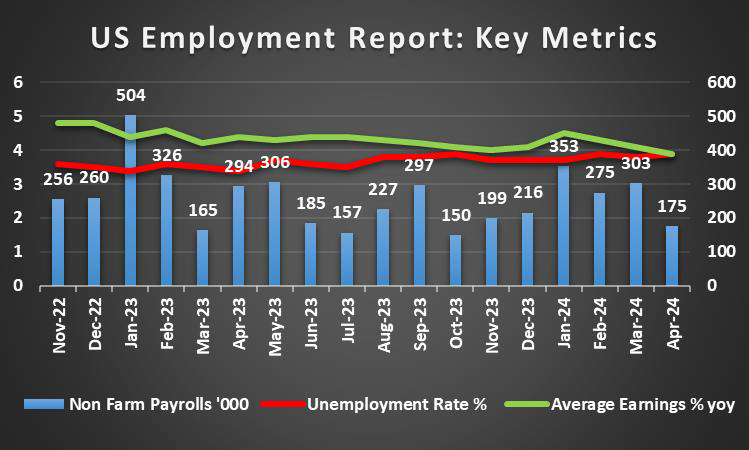

USD – US Employment data due out next week

The USD is about to end the week slightly lower against its counterparts. On a macroeconomic level, the USD gained on Tuesday, following the release of the US consumer confidence figure for the month of May, which exceeded expectations and thus provided support for the dollar, as confidence in the US economy from the consumer’s side increased. However, following the release of the US 2nd GDP revision of the growth rate for Q1, the dollar seems to have returned the majority of the gains it had made since Tuesday. In particular, the rate for Q1, came in lower than expected at 1.3%, implying a weaker-than-anticipated US economy, which in turn seems to have weighed on the dollar. Although, it should be said that this week’s most important economic indicator, has yet to be released, which is the Core PCE rates for April. The rates are the Fed’s favourite tool for measuring inflationary pressures. Should the rates imply a persistent or even an acceleration of inflation in the US economy, it could force the Fed’s hand to maintain current interest rates thus supporting the dollar and vice versa. For next, week the US is expected to release it’s Manufacturing PMI figures, yet most crucial will be the US Employment data on Friday, as a gauge of the labour market. A tight labour market may increase pressure on the Fed to maintain current interest rate levels, which in turn may support the dollar and vice versa.On a monetary level, the Fed’s beige book which was released on Wednesday, tended to highlight that “economic activity continued to expand from early April to mid-May”, which may feed inflationary pressures in the US economy. Furthermore, Minneapolis Fed President Kashkari stated earlier on this week that he wants to see “many more months” of positive inflation data. The aforementioned comment seems to be in line with our statement last week, that “should we see Fed policymakers re-iterating the bank’s message that there is still some way to go before any rate cuts, we may see the greenback gaining further”. However, he did also state that he does not see more than two rate cuts by the Fed this year, which seems to be in line with the current market expectations and thus, despite his relatively hawkish comments, his statement could be perceived as relatively neutral, given his tendency to lean towards the “hawkish” side of the spectrum.

GBP – Debate week incoming

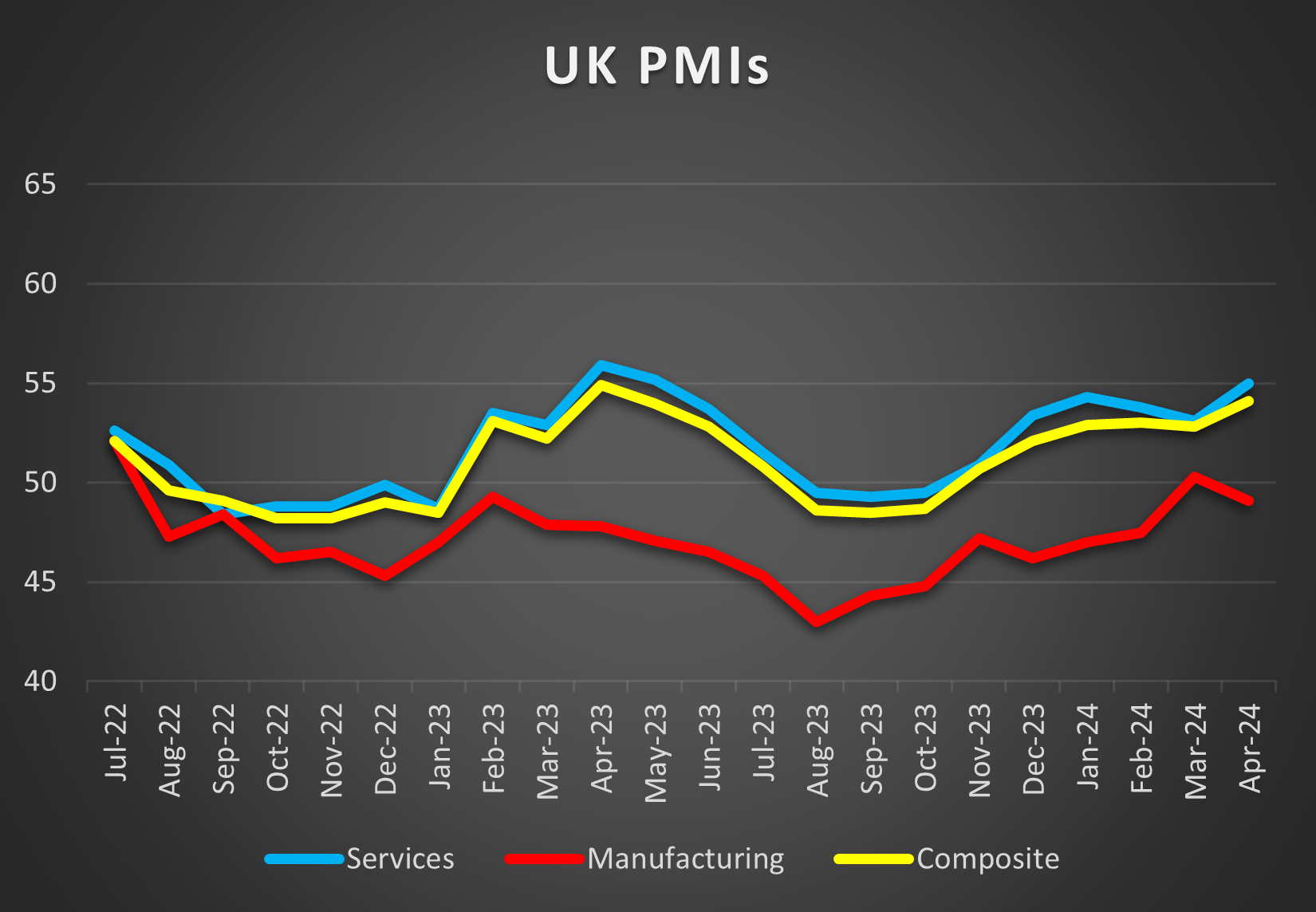

The pound is about to end the week lower against the USD and the EUR, but remained relatively unchanged against the JPY. On a political level, we note that after the starting gun was fired for a UK general election, the first debate between the two front runners which are UK Prime Minister Sunak and Keir Starmer the Leader of the Labour party, will be taking place on the 4th of June. Moreover, we would like to note that the British Parliament has now officially been dissolved, as campaigning has officially commenced. On a macroeconomic level, we note that this week has been relatively quiet from the UK in terms of financial releases with nothing of importance to note. As such traders may look forward to next week, where we are set to receive the UK’s manufacturing PMI figure for May. Should the figure come in lower than the previous reading of 51.3, implying a reduction in manufacturing activity in the UK, it could dampen the nation’s economic outlook and thus may weigh on the pound. On the other hand, a figure higher than 51.3, could provide support for the pound. On a monetary level, we emphasize that according to Bloomberg, the BoE has cancelled its public speaking engagements as a result of the snap elections and thus, the attention of the market may influenced at a greater degree from financial releases. Moreover, the recent comments made by UK Prime Minister Sunak that a vote for his conservative party at the general election, would be a vote for interest rate cuts, may cast doubt over the bank’s future impartiality and thus could also increase volatility. To be clear however, we do not anticipate the BoE to abandon its neutrality, yet the comments made by the UK Prime Minister, are dragging the BoE into the political spotlight.

JPY – Fundamentals to lead the way

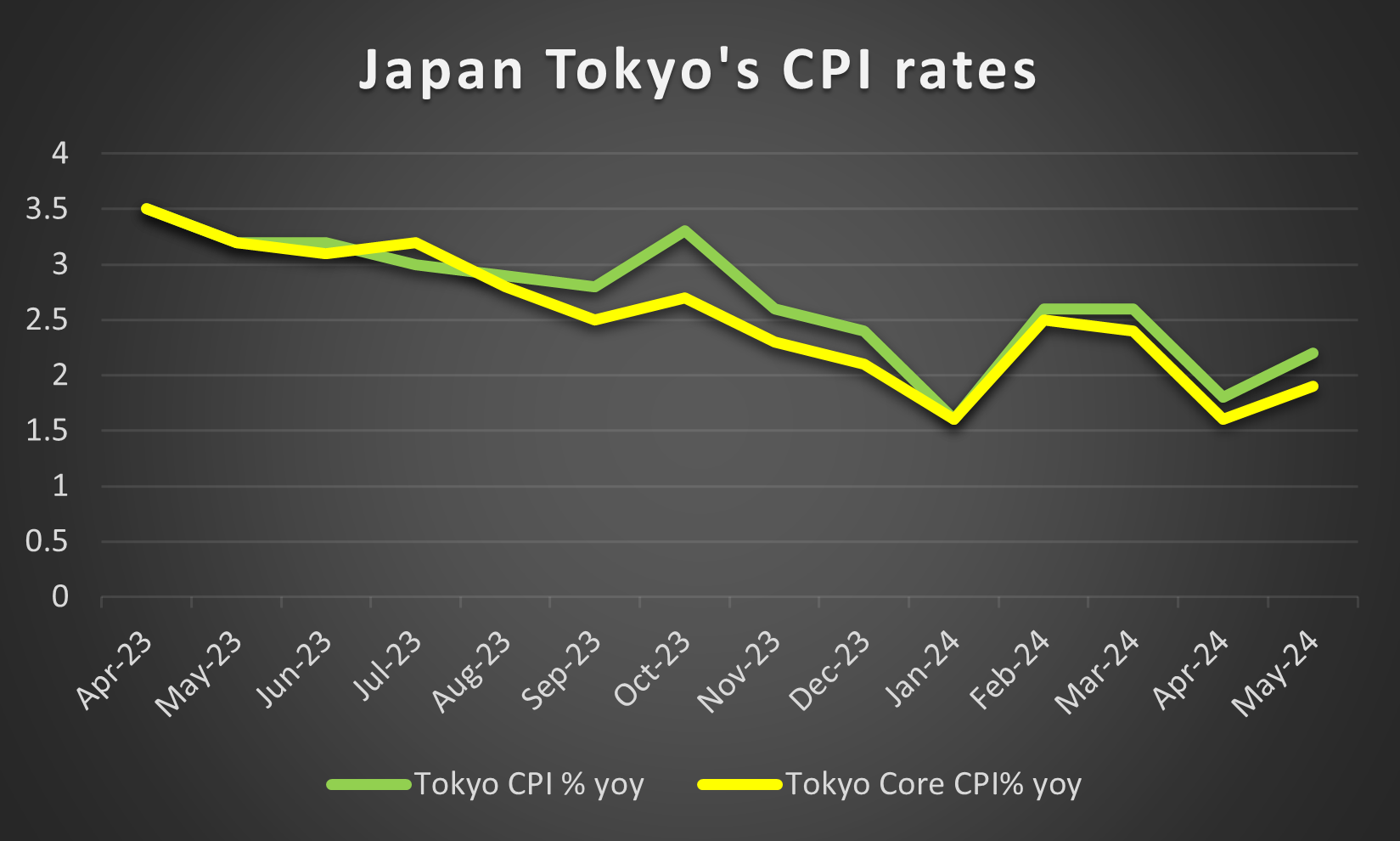

The JPY is about to end the week lower than the USD and the EUR but remained relatively uncanged against the Pound . Japan’s macroeconomic outlook continuesto darken, as the preliminary industrial production rate for April contracted by -0.1% earlier. The much lower-than-expected rate which highlighted the contraction in production activity, may be worrying for the Japanese economy, which has a heavy industrial orientation. On another note, the BOJ’s Core CPI rates came in lower than expected at 1.8%, which implied that the bank may not need to increase it’s interest rates further in order to combat inflationary pressures in the Japanese economy. The release, may hinder the BOJ’s ambitions to continue on its monetary policy normalisation by possibly continuing on their rate hiking path. Therefore the release weighed on the Yen, with the JPY falling to its weakest level against the GBP in almost 16 years. Moreover, in today’s Asian session, the release of the Tokyo Core CPI rates tended to re-affirm our aforementioned theory, which may have aided to the Yen’s recent weakening.For next week we note no major financial releases stemming from Japan, which in turn may result in the Yen’s direction being dictated by other stronger currencies. On a fundamental level, let’s not forget that another market intervention by Japan to the Yen’s rescue, is always possible should JPY slip even lower.

EUR – ECB Interest rate decision due out next week

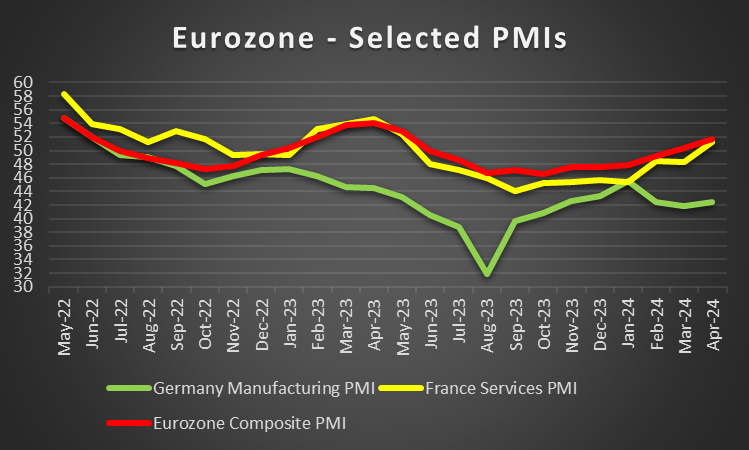

The common currency is about to end the week relatively unchanged against the USD but higher than the GBP and the Yen. On a political level, the elections for the new EU Parliament are set to occur next week between the 6th and 9th of June, which tends to provide some uncertainty for the path of the area ahead on a political level, as far-right parties are expected to make significant gains, which could upend the traditional power balance. On a monetary policy level, we note that the ECB’s interest rate decision is set to take place next Thursday, with EUR OIS currently implying a 92% probability for the bank to reduce the refinancing rate and deposit rate by 25 basis points to 4.25% and 3.75% respectively. As such our attention now turns to the bank’s accompanying statement, where should it be inferred that the bank may continue on an interest rate reduction path for the remainder of the year, it could weigh on the EUR. However,s should signs of hesitation emerge from ECB policymakers in regards to more rate cuts later on this year, it could provide support for the EUR. Yet for now it is our belief that the ECB may cut interest rates next week, but may opt-in its accompanying statement to keep the door open for maintaining interest rates higher for a little bit longer.On a macroeconomic level, we note the release of the preliminary HICP rates for May from, Germany, France and the Eurozone as a whole, which indicated an acceleration of inflationary pressures on a year-on-year level . In particular Germany’s preliminary HICP rate on a year-on-year level came in at 2.8%, which was higher than the anticipated rate of 2.7%. The higher-than-expected rate, could cast some doubt on the narrative that inflationary pressures are easing in the Euro area,and thus pressure may increase on the ECB to maintain interest rates at their current levels for a prolonged period of time, which in turn could provide support for the EUR in the upcoming week. For next week, EUR traders may be looking forward to the release of the Eurozone’s revised GDP rate for Q1. Should the revised GDP rates come in higher than the prior rate of 0.3% on a qoq basis and 0.4% on a year-on-year basis, thus implying that the Eurozone’s economy remains resilient, in spite of the tight financial conditions. It could further increase pressure on the ECB to keep rates steady, in order to avoid a resurgence in inflationary pressures in the Euro area, which in turn could support the EUR.

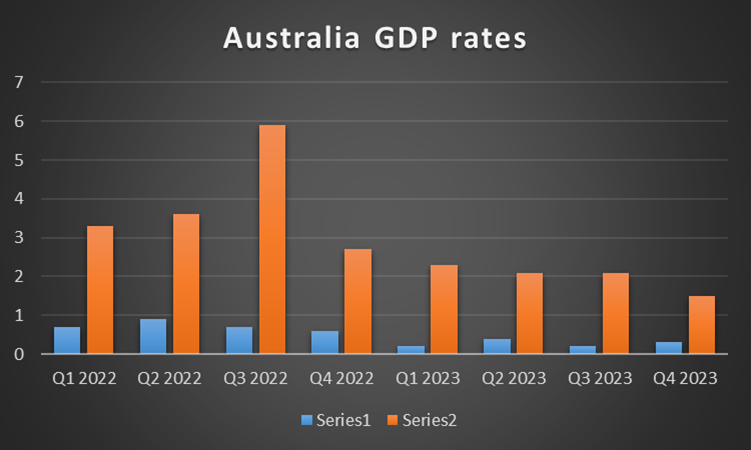

AUD – CPI rates next week

AUD is about to end the week stronger than the USD. On a fundamental level, we highlight the close socio-economic ties between Australia and China, thus should US[1]Sino relationships deteriorate we may see the Aussie taking a hit as well. In particular, we are referring to the war games which China began last Thursday around the island of Taiwan and were concluded two days later. On another fundamental note, we note the release of China’s NBS Manufacturing PMI figure for May, which came in lower than expected, showcasing a contraction in manufacturing activity, which could also imply that demand for raw materials from Australia may decrease, having the potential to weigh on the Aussie. On a macroeconomic level, we note the release of Australia’s CPI rate for April which came in higher than expected at 3.60% versus 3.40%, implying an acceleration of inflationary pressures in the Australian economy. The stubbornness of inflation in the Australian economy could further support RBA’s case for the continuance of a tight, or even tighter financial environment in Australia, and thus could support the AUD. However, not all was peachy for the Australian economy as the preliminary retail sales rate for April on a month on month level came in lower than expected at 0.1% implying that consumer spending increased but not to the expected rate, despite it coming in at 0.1%, it was still higher than the prior rate of -0.4%. For next week would would like to note Australia’s GDP rate for Q1. Where should it be indicated that the Australian economy expanded at a greater rate than what was expected, it could support the Aussie and vice versa.

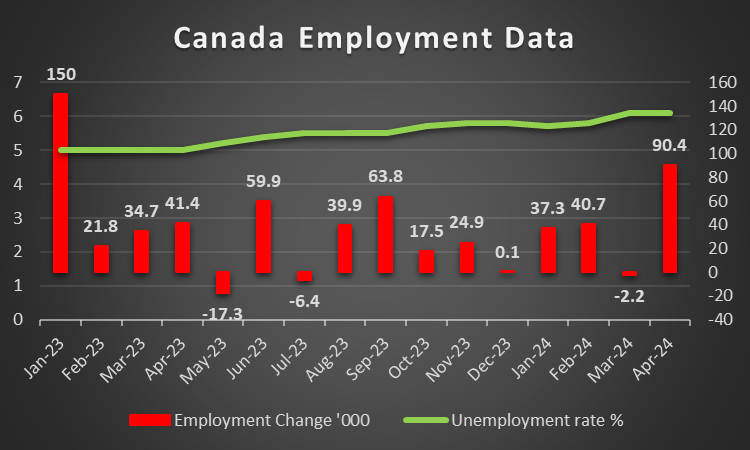

CAD – Employment data next week

The CAD is about to end the week stronger against the USD. It was a rather easy-going week for Loonie traders, although we should point out that Canada’s GDP rates for Q1 have yet to be released and thus may influence the Loonie before this week comes to an end. On a fundamental level, we note that oil prices seem to have moved higher since the beginning of the week, which may have provided some support for the Loonie, given Canada’s status as a major oil-producing economy. Thus should oil prices continue on their ascent, we may see the Loonie also getting some support in the coming week. On another note, the OPEC+ meeting is set to occur on Sunday and thus any decisions made could impact the global oil markets and thus by association the Loonie.On a macroeconomic level, we note the release of Canada’s Employment data for May next week, where should the rates imply a resilient labour market, we may see the Loonie gaining and vice versa. Moreover, we would also like to note the release of Canada’s trade balance for April, where should a trade surplus emerge, it could support the Loonie, whereas a trade deficit could weaken the CAD. However, the highlight of the week for Loonie traders is set to be the BoC’s interest rate decision on Thursday, with CAD OIS currently implying 59.34% probability for the bank to cut interest rates by 25 basis points, with the rest being attributed to a hold. Should the bank cut interest rates, it could weigh on the Loonie. However, should the bank decide to maintain its current interest rate levels it may instead provide support for the CAD.

General Comment

As closure and in a more general note, we expect in the FX market the USD to increase its influence over other currencies. In turn that may allow for a more influential dollar to overshadow financial releases stemming from other countries, by taking the spotlight. It’s characteristic that all three major US stock market indexes appear to have retreated from their recently formed new all time highs. Also, we note that the negative correlation of the USD with gold’s price being once again present this week, given the strengthening of the USD and the decline of the precious metal’s price. We expect the negative correlation of the two trading instruments to be maintained and should the USD move higher, we may see gold’s price weakening further. On another note, OPEC+’s meeting on Sunday is expected to roll over their current voluntary oil production cuts, which could weigh on oil prices. However, any deviation such as reducing their oil production levels even further, could support global oil prices.

If you have any general queries or comments relating to this article please send an email directly to our Research team at research_team@ironfx.com

Disclaimer:

This information is not considered as investment advice or an investment recommendation, but instead a marketing communication. IronFX is not responsible for any data or information provided by third parties referenced, or hyperlinked, in this communication.