The Israeli conflict continues to tantalize the markets and the worries for a possible escalation seem to intensify. It should be noted that a massive land invasion of Israeli forces in Gaza could cause reactions from Araba countries in the entire Mid-East region. Already reports are surfacing that Israel’s Defence Forces have received the green light from the Israeli Government, while the width and timing of such an operation is still to be seen. On the monetary front, we highlight the release of BoC’s and ECB’s interest rate decisions on Wednesday and Thursday respectively, while also noting from Turkey, CBT’s interest rate decision on Thursday. As for financial releases, we note on Monday the release of the Eurozone’s preliminary consumer confidence for October. On Tuesday we get the preliminary PMI figures of Australia, Japan, France, Germany, the Eurozone, the UK and the US while we also note the release of Germany’s November GfK consumer confidence and UK’s employment data for August. On Wednesday we note the release of Australia’s CPI rates for Q3 and Germany’s Ifo indicators for October. On Thursday we highlight the release from the US of the preliminary GDP rate for Q3, but also note September durable goods orders and the weekly initial jobless claims figure. On Friday we note the release of Japan’s CPI rates for October and from the US the consumption rate for September, the core PCE price index for the same month and October’s final University of Michigan Consumer Sentiment.

USD – The spotlight on the GDP advance rate

The USD seems to remain unchanged, maybe even edging a bit lower for the week against its counterparts. On a fundamental level, we note that the GOP still has difficulties in electing a speaker for the House of Representatives. We note that Jim Jordan’s bid as a speaker of the House was not successful as these lines are written, as he faces steep opposition from far-right Republicans. As mentioned in our last report the issue highlights the rift between the factions within the Republican Party. On a monetary level, we note that the market seems to solidify its view that the bank has reached its terminal rate, yet the high-interest environment seems to be maintained for a prolonged period. We would like to note though the worries of some Fed policymakers that inflationary pressures are still at high levels. Characteristically Fed Chairman Powell despite not actually committing to any form of action noted that inflation is still too high and that Fed policymakers are united in the effort to bring inflation back to the bank’s 2% target. Nevertheless, the Fed Chairman acknowledged the progress made so far. On a macroeconomic level, we note that the stronger-than-expected retail sales rate for September tends to highlight a robust demand side for the US

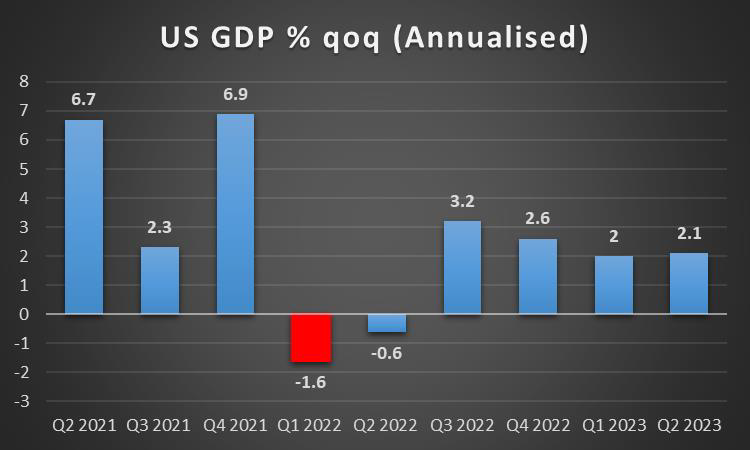

economy while the US labour market seems to remain rather tight. Both of the aforementioned may continue feeding inflationary pressures in the US economy, or at least not allow inflation to come down at a faster pace and thus may harden the Fed’s hawkish stance. In the coming week, we highlight the release of the preliminary US GDP rate for Q3 and a possible acceleration could support the USD as it would signal that the US economy despite the problems and the tight financial environment remains resilient. Also, it may signal that the scenario of a soft landing of the US economy, expected by the Fed may still be possible. Furthermore, such a scenario may also allow the Fed to maintain its hawkish stance for an even longer period.

GBP – Second part of UK’s Employment data to be released

The pound seems about to end the week a bit lower against the USD, substantially lower against the EUR and is gaining slightly against the JPY. On a fundamental level, we note that the cost of living may still be the main issue troubling society. We also note that UK government advisers stated that UK infrastructure needs more investment and further signs of fiscal openings may support the pound. Overall, we highlight the dilemma BoE faces, to hike or not in its next meeting, as on the one hand, inflationary pressures remain persistent in the UK economy, while on the other hand, the economy seems to be slowing. BoE’s chief economist Hugh Pill was reported stating that there is still work to be done, which underlined the need for a tighter monetary policy. Yet the market seems to maintain the view that the bank is to remain on hold in its next meeting as GBPOIS implies a probability of 85.59% for such a scenario to materialize. Furthermore, the market seems to expect the bank to remain on hold throughout the year. Yet the issue gained further traction as on a macroeconomic level the CPI rates for September practically did not slow down on a year-on-year level, while on a month-on-month level, even accelerated. It should be noted that the average earnings growth rate for August, slowed down yet remained above 8% yoy which may imply that the UK employment market may still feed inflationary pressures in the UK economy. In the coming week, we note the release of the second part of August’s employment data and should the data show that the UK employment market remains tight we may see the GBP getting some support. Furthermore, we note the release of the preliminary PMI figures for October with the heavy point being placed on the Services sector. The indicator’s reading is below the reading of 50, implying a contraction of economic activity in the critical services sector of the UK economy and a possible drop of economic activity in the sector would underline the problems faced in the UK’s economic recovery.

JPY – Remaining dangerously weak

JPY seems about to end the week lower against the USD, EUR and GBP in a sign of broader weakness. On a fundamental level, we note that the Japanese currency seems not able to attract safe haven inflows from the Mid-East tensions, or at least such inflows may be countered by a continuing weakening of JPY. On a deeper fundamental level, we note that Japanese PM Kishida has sent a ritual offering to the controversial Yasukuni Shrine, a move that may underscore the possibility of further tensions with China. Also on a political level, we note that the approval ratings of the Japanese Government, after the reshuffling of the Cabinet, seem to sink to levels not reached since he assumed office in October 2021. Any possibility of destabilisation of the Japanese Government may weigh on the JPY as it would enhance uncertainty, yet on the flip side it may also provide some safe haven inflows for JPY. On a monetary level, we note expectations in various media reports for BoJ to raise its inflation forecasts for the current and next year. The bank is expected in its next meeting to raise inflation forecasts for March 2024 to 3.0% if compared to July’s projection for the same period of 2.5%. Such a change about where inflation may land may provide difficulties to the bank’s dovish stance and hence we may see the banks’ rhetoric starting to shift. It should be noted that BoJ’s ultra-loose monetary policy settings may have been the main factor behind the weakening of the Japanese currency since the start of the year. Should we see an actual shift in the tone characterizing BoJ officials’ statements, we may see JPY gaining some traction. On a macro level though we note the slowdown of Japan’s CPI rates for September that do not justify such a shift just yet.

EUR – ECB and October’s preliminary PMIs eyed

The common currency is about to end the week slightly higher against the USD, the pound and JPY in a sign of broader strength. On a fundamental level, we note the divide in European society across borders in regard to the Israeli conflict, yet that is not expected to have a major effect on the markets. On the contrary, there are developments in the energy sector as Germany was reported conceding to French demands to keep the subsidies for atomic energy. In the big picture, the EU energy ministers seem to have reached an interim compromise regarding the reforming of the Union’s electricity market, a development that could provide

some easing of the energy crisis and some support for the common currency. On a monetary level, we note the ECB’s interest rate decision next week. The bank is widely expected to remain on hold keeping the refinancing rate at 4.5% and it’s characteristic that EUR OIS imply currently a possibility of 99% for such a scenario to materialize, practically implying that the interest rate part of the decision is an open and shut case. The next element to keep an eye out for, would be the accompanying statement and ECB President Lagarde’s press conference later. The bank is expected to reassure the markets that conditions have not materially changed possibly even mentioning that inflation is slowing and the cumulative effect of the rate hikes performed is sufficient to bring inflation back to target, a development that may weaken the EUR. On the other hand, the possibility of stressing that rates are to remain at high levels for a prolonged period could provide some support for the common currency. On a macroeconomic level, we note that the slowdown of the Eurozone’s HICP rate for September was verified and now we turn our attention towards economic activity. Thus in the coming week, we note the release of the preliminary PMI figures for October and should the indicators show readings substantially below 50, implying another contraction of economic activity, especially for Germany’s manufacturing sector as is expected, we may see the EUR slipping.

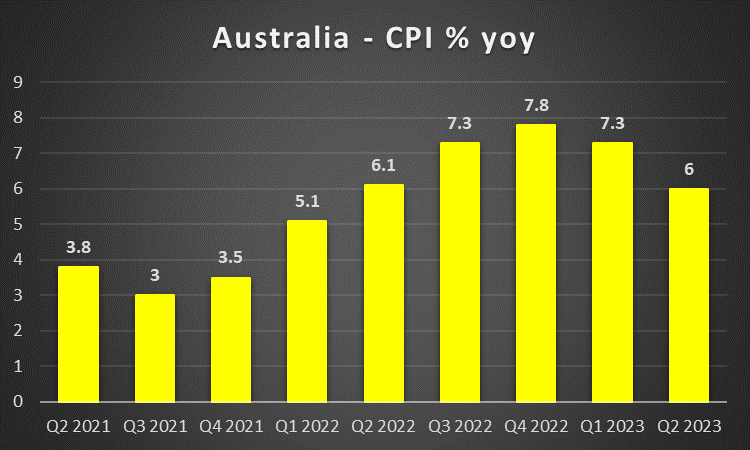

AUD – CPI rates in sight

AUD is about to end the week relatively unchanged against the USD. On a fundamental level we note the developments in China’s economy given the close Sino-Australian economic ties and the amount of raw materials exported from Australia to China. Chinese data took the markets by surprise as the GDP rate for Q3, industrial production and retail sales growth rates for September did not slow down as far as expected. Yet we note that embattled property developer Country Garden, is at risk of defaulting on its entire offshore debt, following the company missing its payment deadline on Tuesday. The failure to repay its $15 million coupon, following a 30-day grace period, appears to be reflecting China’s deteriorating property sector, following the collapse of Evergrande. The issue highlights the headwinds placed by the construction sector to the recovery of the Chinese economy and a loss of confidence in its outlook could weigh on the market sentiment and thus on AUD. On a monetary level, we note the market’s expectations for the bank to remain on hold in its next two meetings, yet to hike rates in February. It should be noted that RBA Governor Bullock had expressed her concerns about the possible inflationary effect that the Israeli conflict may have on Australia’s economy and should we see RBA policymakers adopting in general a more hawkish view we may see the Aussie getting some support as market’s expectations for another rate hike in December may be enhanced. Yet such market expectations could also be affected by the release of the CPI rates for Q3 due out on Wednesday. Should the rates accelerate we may see AUD getting some support as it would highlight the need for more rate hikes. A possible substantial slowdown of the CPI rates could weaken the Aussie yet the overall effect in case of a slowdown may also be linked to its width.

CAD – BoC’s interest rate decision in focus

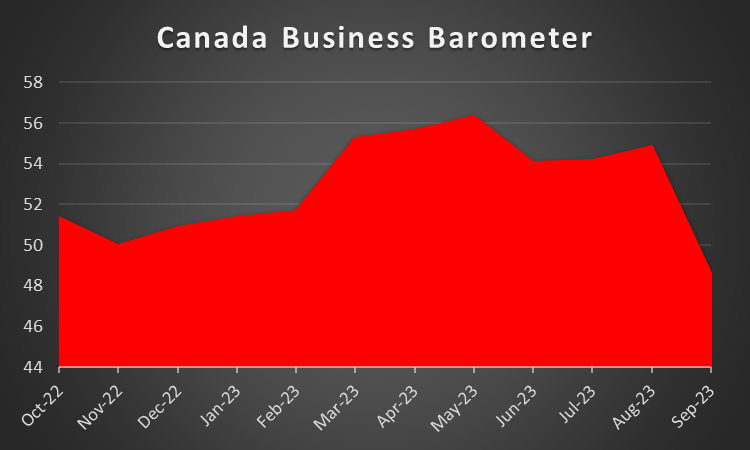

CAD is about to end the week lower against the USD. It should be noted that the CAD weakened despite oil prices gaining over the week. It should be noted that oil prices edged lower despite signals that the US oil market tightened recently, while the bullish effect of the Israeli conflict seems to remain present and may intensify should the conflict escalate. Yet Venezuela seems to have reached an understanding with the US and is ready to boost the supply side of the international oil market thus weighing on its price possibly. On the other hand, the refilling of the US Strategic Petroleum Reserve (SPR) may boost oil prices. Should oil prices continue to rise, we may see a bullish effect on CAD. Also, we note that the CAD as a commodity currency may be regarded as a riskier asset and thus be more sensitive to the market sentiment. Should we see the market sentiment turning more cautious the CAD may lose some ground and vice versa. Yet also on a macroeconomic level, we note the slowdown of the CPI rates both on a core and a headline level for September, easing the pressure on BoC for further tightening. The bank is to release its next interest rate decision on Wednesday and is expected to remain on hold at 5.0%. CAD OIS imply a probability of 84% for such a scenario to materialise, with the rest implying that a 25 basis points rate hike is also possible. CAD OIS also seem to imply that the market expects the bank to remain on hold, until early spring next year and proceed then with a 25 basis points rate hike. Hence we may see attention shifting towards the accompanying statement. Should the document maintain elements of uncertainty and hesitation about the bank’s rate hiking path it may contrast the market’s expectations for a possible rate hike in Q1 24 and thus deliver a bearish effect on CAD. On the flip side, should the bank sound hawkish we may see the Loonie getting some support.

General Comment

We expect in the coming week the USD to regain some of the initiative in the FX market over other currencies, given that the frequency and gravity of US financial releases seem to increase. Nevertheless, we maintain the view that at some moments certain currencies may get out of the shadow of the greenback. Furthermore, we maintain the view that market attention may continue to be shifted towards US stock markets given the high-profile companies releasing their earnings reports in the coming week. Hence for the coming week, we note the earnings reports of 3M(#MMM), GOOGLE (#GOOG), General Electric (#GE), General Motors (#GM), Coca-Cola (#KO), Visa (#V), Microsoft (#MSFT) on Tuesday, Boeing (#BA), EBAY (#EBAY) , IBM(#IBM), APPLE (#AAPL), META (#FB) on Wednesday, Mastercard (#MA), Amazon (#AMZN), Intel Corp. (#INTC) on Thursday and Exxon Mobil (#XOM) on Friday. We expect market attention to focus on the US tech sector given the mega-cap tech companies due to release their earnings reports. As for gold, it seems to have been maintaining its upward trajectory, albeit at a slower pace than the last week. Nevertheless, the precious metal seems to enjoy an asymmetrically high safe haven inflow if compared to the weakening of the USD, due to the Israeli conflict. It should be noted that gold’s price got a substantial boost despite US yields rising to levels not seen in years, with the 10-year yield almost reaching 5%, a level not seen since 2007. The fact that even with yields that high, the US bond market seems to continue not to attract investors tends to paint a pretty grim picture for the US economy.

Se tiver alguma dúvida ou comentários sobre este artigo, solicitamos que envie um email diretamente para a nossa equipa de Research através do research_team@ironfx.com

Isenção de responsabilidade:

Esta informação não é considerada como aconselhamento ou recomendação ao investimento, mas apenas como comunicação de marketing. O IronFX não é responsável por quaisquer dados ou pela informação fornecida por terceiros aqui mencionados, ou com links diretos, nesta comunicação.