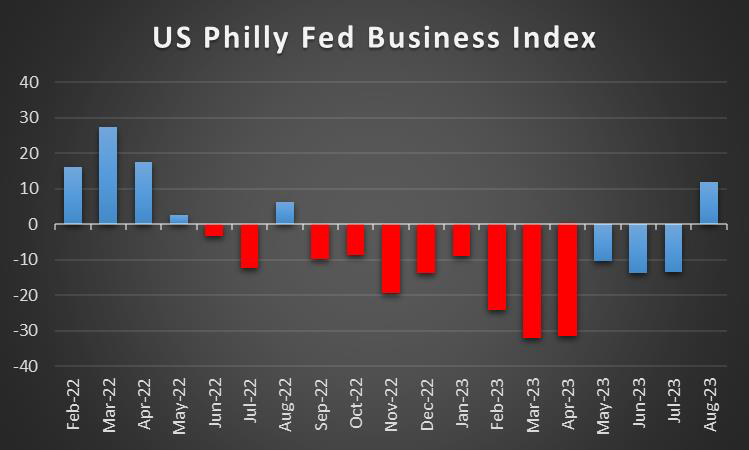

With the week nearing its end, we note that the US Preliminary University of Michigan consumer sentiment has yet to be released. On a monetary level, we highlight the RBA’s September meeting minutes on Tuesday, the BoC’s September meeting deliberations and the FED’s interest rate decision on Wednesday, the SNB’s, Riksbank’s, Norgesbank’s , BOE’s and from Turkey CBT’s interest rate decisions which are all due on Thursday and lastly the BOJ’s interest rate decision on Friday. In regard to financial releases, we make a start on Tuesday with the Eurozone’s final HICP rate and Canada’s CPI rates both for the month of August. On Wednesday we make a start with Japan’s trade data, followed the UK’s CPI data both for the month of August. On Thursday, we note New Zealand’s GDP rate for Q2, France’s overall business climate figure for September, the US weekly initial jobless claims figure, the US Philly FED business index for September and the Eurozone’s Preliminary consumer confidence figure for September. Lastly on Friday, we begin with Australia’s preliminary Judo Bank manufacturing PMI figure for September, Japan’s CPI rates for August and preliminary JiBunBK manufacturing PMI figure for September, followed by the UK’s retail sales rate for August, France’s, Germany’s, the Eurozone’s, UK’s and the US preliminary S&P PMI figures for September as well as UK’s CBI trends figure also for the month of September and lastly Canada’s retail sales rate for July.

USD – FED’s interest rate decision due next week

The USD is about to end the week in the greens against its counterparts for a ninth consecutive week. On a fundamental level, we highlight that the House of Representatives has opened a formal impeachment inquiry into President Joe Biden. Should there be further escalations between the Republican and Democratic party, we may see a political standoff before the Government’s funding expires on the 30th of September and as such any delays which may increase the risk of a government shutdown and in turn could weigh on the dollar. On a monetary level, we highlight that we are currently in the Fed’s blackout period, as their next monetary policy meeting is due to occur next Wednesday. Therefore, we turn our attention to one of the last Fed members who spoke last Friday just before the Fed’s blackout period, which was New York Fed President Williams. Fed President William’s stated when referring to the current impacts of monetary policy, that “It’s pretty clear we’re restrictive” but it’s “still an open question as we go forward”, implying that the banks current rate of monetary policy is sufficient to combat inflation, yet there may be a degree of uncertainty as to whether they still need to raise rates further. As such, the vagueness in New York Fed President William’s answers do not necessarily lean on the dovish nor the hawkish side and as such, does not necessarily offer any support to either the bulls or bears, which may have incurred a state of limbo in the FX market. Nonetheless, we note expectations from market analysts that the bank will remain on hold yet we also see increased chances for the scenario that the bank may hike rates by 25 basis points. On a macroeconomic level, we highlight the US CPI rates which came out on Wednesday, that were indicative of persistent inflationary pressures. The higher-than-expected CPI print could be considered as an elevation of the inflationary pressures which the US economy is facing and as such could potentially, support the case for further rate hikes in order to combat inflation. Yet, the majority of market participants are anticipating the Fed to remain on hold and characteristically FFF imply a 97% probability for such a scenario to materialise. Even should the bank remain on hold a possible hawkish accompanying statement or a hawkish tone in Fed Chairman Powell’s press conference could provide some support for the USD. On the other hand should the bank remain on hold and signal that it has reached its terminal rate, we may see the USD losing ground. In conclusion, with the markets now anticipating the Fed’s interest rate decision next week, we believe that the other financial releases stemming from the US such as the weekly Initial jobless claims figure, Philly Fed business manufacturing index figure and the preliminary S&P manufacturing PMI figure, may likely be overshadowed by the Fed’s interest rate decision.

GBP – BOE’s interest rate decision due next week

The pound seems about to end the week weaker against the USD and relatively unchanged agsint the EUR and JPY. On a fundamental level, we note that POLITICO reported that an alleged Chinese spy met with a UK government minister to discuss amendments on a key legislation piece relating to China. Although the meeting may be immaterial, the political backlash could potentially pressure the Government to respond with a tougher stance against China, thus potentially straining the UK-China relationship which could weaken the pound, should the UK ‘lose’ more trading partners. On a monetary level, we highlight the speech by BoE member Mann who stated “In my view, holding rates constant at the current level risks enabling further inflation persistence, which will have to be unwound eventually with a worse trade-off,”, strongly implying that the bank may need to continue raising interest rates, in their next monetary policy meeting which is due next week. This is also widely expected by market participants to result in a 25 basis point hike and as such could provide support for the pound, a view with which we agree, as the current levels of inflation are still far away from the bank’s 2% target. On a macroeconomic level, we note the UK GDP rates, which came in lower than expected at -0.5% compared to the expected rate of -0.2%, implying a contraction in the UK economy, which could be attributed to the burden placed on a pound, as the UK’s economic situation continues to deteriorate. Lastly, we note the financial releases stemming from the UK next week, with the UK’s CPI rates, retail sales rate for August, the UK’s preliminary manufacturing PMI figures, and CBI trend orders figure, both for the month of September.

JPY – BOJ interest rate decision due next week

JPY is about to end the week relatively weaker against the dollar, yet remain unchanged against the EUR and GBP. On a fundamental level, we note the Japanese Prime Minister has re-shuffled his cabinet with some new appointees appearing to notion that Japan is intent on strengthening relations with Taiwan, which could provoke China thus generating instability in the region which may support JPY, as it may experience safe haven inflows. On a monetary level, we note the speech from BOJ Governor Ueda who according to Reuters stated, “If we judge that Japan can achieve its inflation target even after ending negative rates, we’ll do so,” implying that the bank may ready to gradually phase out its ultra loose monetary policy. However, despite the Governor’s comments, he did also mention that the bank has a long way to go and that the banks inflation target is not in sight, thus even though many news outlets are running with stories implying an immediate shift in BOJ policy, we believe that it is not the case at this point time and may occur during next year. Therefore, despite the JPY gaining upon the comments of the Governor, we anticipate that a clearer picture may be painted in the bank’s interest rate decision which is due to take place next Friday, where it is widely anticipated that the bank will remain on hold. However, should there be any indication of a switch from the bank’s current monetary policy in the accompanying statement or press conference, we may see support for the JPY, and should there be an indication of the bank’s commitment to its ultra-loose monetary policy, we may see the JPY slipping. On the other hand, should the Governor hint at a phasing out of the bank’s ultra-lose monetary policy in the near future, we may see the JPY gaining against its counterparts, yet this is an unlikely scenario. On a macroeconomic level, JPY traders may be interested in Japan’s trade balance data which is due next Wednesday and Japan’s CPI rates for August which are due on Friday. We anticipate that based on the comments made by the Governor, Japan’s CPI rates may come in higher than expected, which may support the JPY. On the other hand, should the CPI rates come in lower than expected, we may see the JPY weakening against its counterparts.

EUR – ECB hikes by 25 basis points

EUR is about to end the week in the reds against the USD yet relatively unchanged against the pound and the JPY. On a fundamental level, we note the statements made by the EU Commission President Ursula Von Der Leyen who stated that China was providing huge subsidies to its EV makers, which could spark retaliatory measures by China and given their status as a major EU trading partner, any tit-for-tat measures could weigh on the EUR. On the monetary front, we note that the ECB hiked rates by 25 basis points as part of the market expected, yet practically implied that it has reached its terminal rate. In the accompanying statement the bank stated that “Based on its current assessment, the Governing Council considers that the key ECB interest rates have reached levels that, maintained for a sufficiently long duration, will make a substantial contribution to the timely return of inflation to the target”. Later on, in her press conference ECB President Lagarde stated that there was a solid majority in favour of the hike yet at the same time answering a question, stated that based on the current assessment the bank is to maintain the current level of interest rates and is to maintain a data-dependent approach. We may see the shift of stance of the bank and the lowering of its expectations for the economy to grow, weighing on the common currency. On a macroeconomic level, the lower-than-expected Germany’s ZEW Economic sentiment figure for August was indicative of a continued deterioration in expectations of Germany’s economy. Should Germany’s economy continue taking a turn for the worst, it could heavily weigh on the common currency, as Germany is the largest economy in the Eurozone and as such, a weaker German economy could lead to a weaker common currency. We plan to closely watch the release of September’s preliminary PMI figures, especially for Germany’s manufacturing sector and adverse data may enhance market worries and push EUR lower.

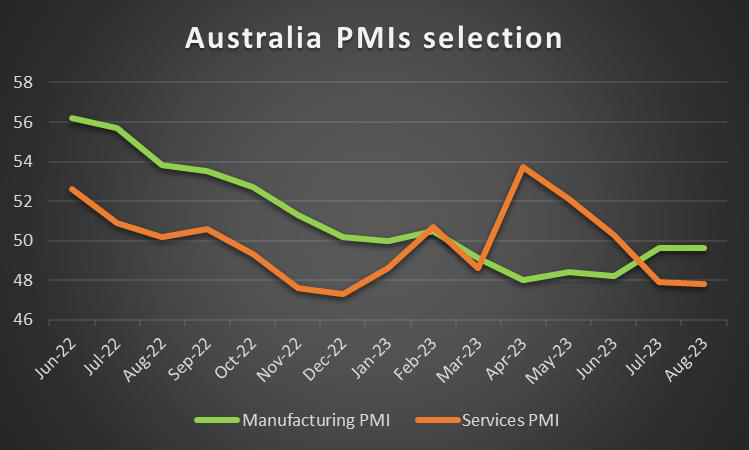

AUD – RBA’s September monetary policy meeting minutes are due out next week

AUD is about to end the week higher than the USD. On a fundamental level, we note that LNG workers at the Chevron plants are reported be escalating their industrial action, with the possibility of 24-hour strikes occurring, which could further intensify supply chain fears for LNG in Europe. On another fundamental note, we continue to monitor China’s behemoth attempts at boosting economic growth, and should there be an indication of an improvement, it could also support the AUD, given that China is a major importer of Australian goods. On a monetary level, we note that the RBA’s September meeting minutes are due to be released next Tuesday, following the bank’s decision to remain on pause during their last meeting. Should the meeting minutes indicate that the bank is unwilling to hike interest rates in the future, thus implying that they may have reached their terminal rate, we may see the Aussie weakening against the dollar. However, on the other hand, should the meeting minutes indicate a willingness by even some members to maintain interest rates at current levels, or even continue in their aggressive rate hiking cycle, we may see the Aussie gaining support. Yet in our opinion, we anticipate that due to the changing of the guard at the RBA, the September minute meetings may be more subdued in terms of a general consensus being reached to remain on pause, with a slight possibility of a hike, thus potentially weighing on the Aussie. On a macroeconomic level, we note Australia’s employment data which was released on Thursday, we correctly anticipated in last week’s report that it would come in higher, and appears to have provided support for the Aussie, as the data was indicative of a resilient labor market. As such should next week’s preliminary Judo bank manufacturing PMI figure come in higher than expected, we may see the Aussie further gaining as it could provide support for the RBA should they decide to hike. Yet, in the event that the manufacturing PMI figures come in lower than expected, we may see the Aussie weakening as it could be indicative of a slowdown in manufacturing activity, thus painting a slightly worrying picture for the economy.

CAD – Is Canada’s ruling party losing its popularity?

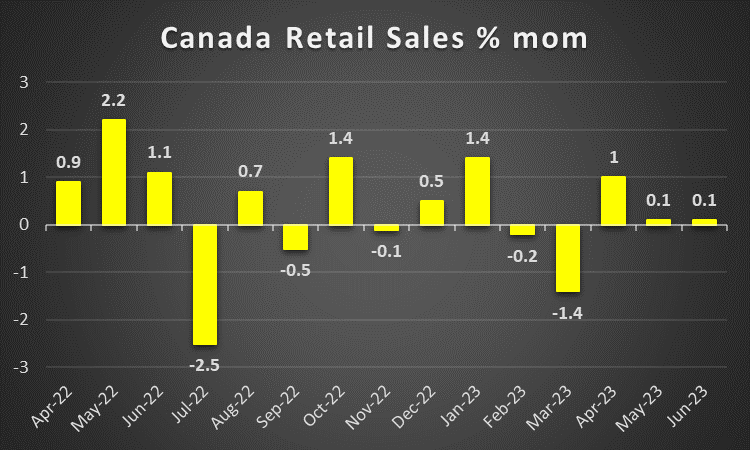

The Loonie is on track to finish higher than greenback, ending an eight-week losing streak. On a fundamental level, we note that the country’s ruling Liberal party under current Prime Minister Trudeau, are trailing behind their Conservative opponents based on recent polling. In the event that the country’s current ruling coalition collapses before 2025, we may see the political uncertainty weighing on the Loonie, yet at this point in time this scenario is considered unlikely. On another fundamental note, CAD traders may be keeping a close eye on oil prices which are about to end higher than last week and as such could support the Loonie if they continue their upward trajectory, given Canada’s status as a major oil producing nation. On a monetary level, we note that the Bank of Canada is due to release its September monetary policy deliberations on Wednesday. In the event that the deliberations are indicative of a willingness by bank officials to continue on a rate hiking cycle in the future, we may see the Loonie gaining against the dollar. On the other hand, should the deliberations indicate a general sense of unwillingness to raise interest rates in the future, we may see the Loonie weakening, as it may suggest that the bank has reached its terminal rate. In our opinion, we believe that the deliberations will indicate that a discussion for a rate hike took place, yet the bank officials might prefer to keep interest rates at their current levels for a prolonged period of time, in order to properly assess their impact on the economy. On a macroeconomic level, we note that Canada’s manufacturing sales rate for July has yet to be released but is anticipated by market analysts to come in higher than the prior reading, thus potentially providing support for the Loonie. Lastly, Loonie traders may be interested in next week’s financial releases, starting on Tuesday with the BoC’s CPI rates for August and then on Friday with Canada’s retail sales rate for July.

General Comment

In the coming week, we expect volatility in the FX market to continue to increase given the high volume of monetary policy decisions that are due out next week. We also note that in the equities markets, Arm LTD went public yesterday with substantial success while US stockmarkets seem about to end the week higher due to the improved market sentiment. As for gold’s price, we note that it appears to be continuing its downward movement for a second week in a row. On a more fundamental level, we note that the tensions between the EU and China seem increasing, following the announcement by the EU Commission that China has been allegedly heavily subsidizing its domestic EV market, which may promote unfair competition in the EV market, as EU car manufacturers struggle to compete with their Chinese counterparts lower prices. It’s characteristic that in the US Congress, members are reported calling the Biden administration for harder measures against China and the overall issue could have a wider adverse effect on the market sentiment should tensions escalate.

Se tiver alguma dúvida ou comentários sobre este artigo, solicitamos que envie um email diretamente para a nossa equipa de Research através do research_team@ironfx.com

Isenção de responsabilidade:

Esta informação não é considerada como aconselhamento ou recomendação ao investimento, mas apenas como comunicação de marketing. O IronFX não é responsável por quaisquer dados ou pela informação fornecida por terceiros aqui mencionados, ou com links diretos, nesta comunicação.