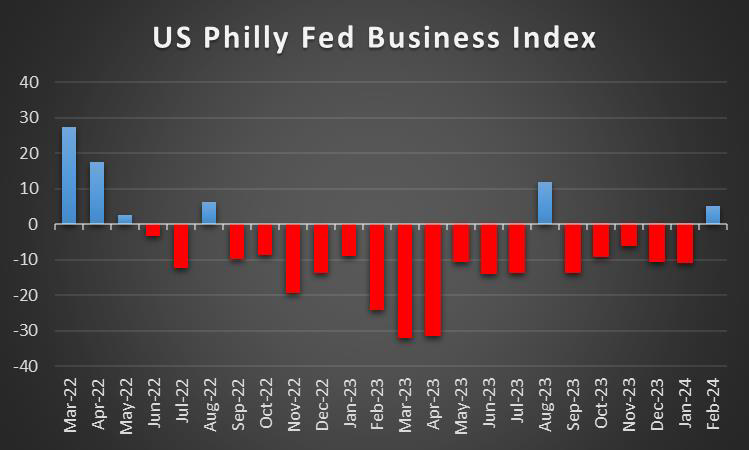

The coming week is to be busy, so let’s have a deeper look. On the monetary front, in the coming week, we have a central bank bonanza and we highlight the release of the Feds’ interest rate decision on Wednesday, yet also BoJ’s, RBA’s and BoE’s interest rate decisions on Tuesday and Thursday. Furthermore, we note the interest rate decisions of China’s PBOC and the Czech Republic’s CNB on Wednesday and on Thursday we get from Switzerland SNB’s, Norway’s Norgesbank and Turkey’s CBT interest rate decisions. We also note that on Wednesday we get BoC’s March meeting minutes and on Friday RBA’s Financial Stability Review. As for financial releases, on Monday we get Japan’s machinery orders for January, China’s industrial output for February, Norway’s GDP rate for January, the Eurozone’s final HICP Rate for February and Canada’s Producer prices for February as well. On Tuesday we get Germany’s ZEW indicators for March and Canada’s CPI rates for February. On Wednesday we get UK’s CPI and PPI rates for February, Eurozone’s preliminary consumer confidence for March and later on we get New Zealand’s GDP rate for Q4. On Thursday we highlight the release of the preliminary PMI figures of Australia, Japan, France, Germany, the Eurozone as a whole, the UK and the S&P US preliminary PMI figures for March. Also on Thursday, we note the release of Japan’s trade data for February, Australia’s employment data for the same month, the US weekly initial jobless claims figure, March’s Philly Fed Business index and later on New Zealand’s trade data for February. On Friday we get Japan’s CPI rates for February, UK’s CPI rates for the same month, Germany’s Ifo indicators for March and Canada’s retail sales for January.

USD – Fed’s interest rate decision to shake the dollar

The USD seems about to halt last week’s drop against its counterparts and rise. On a macroeconomic level, we note that the release of the US CPI rates for February may have taken the markets by surprise as the headline rate unexpectedly ticked up, while the core rate slowed down less than expected, both on a year-on-year level. The release highlighted the persistence of inflationary pressures in the US economy for the past month and may harden the stance of the Fed to maintain high rates for longer. We also note that the market’s expectations for the Fed’s stance have altered, as the market before the release was expecting the bank to deliver four rate cuts, starting from June onwards, yet currently, only three rate cuts are expected. Hence we highlight the Fed’s interest rate decision next Wednesday. The bank is widely expected to remain on hold with Fed Fund Futures (FFF) implying a probability of 99% for such a scenario to materialise. Yet the main element that could shake the markets could be the tone of the accompanying statement and Fed Chairman Powell’s press conference half an hour later. Should the bank’s tone more or less verify the market’s expectations for its rate-cutting path, we may see the USD slipping while should the bank signal that it intends to keep rates higher for longer we may see the USD gaining. Also, we highlight the release of the new dot plot which is to showcase Fed policymaker’s expectations for where the interest rates may land for the year and the following two. Should Fed policymakers indicate that they expect rates to remain higher than the market expectations for the year, implying less interest rate cuts we may see the USD getting some support. We also note the release of the Fed’s projections for inflation and growth which could shape the market’s expectations for the US economic outlook.

GBP – BoE to remain on hold

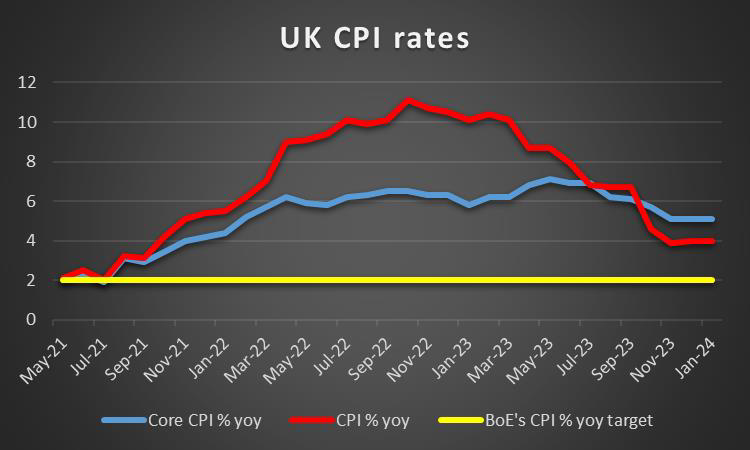

The pound is about to end the week lower against the USD and the EUR yet gains against the JPY. On a macroeconomic level, we note the deterioration of the UK employment data for January, with the employment figure dropping into the negatives and the unemployment rate ticked up. Yet the release of the GDP rates tended to provide some comfort for pound traders, given that on a month-on-month basis, the UK economy seems to have returned to positive readings for January. The next big piece of the puzzle is to be the release of the CPI rates for February on Wednesday and should rates slow down it may add pressure on the BoE to start cutting rates earlier. For the time being, the bank is expected by the market to start cutting rates in August and deliver two rate cuts in total for the year. Hence we expect pound traders’ interest next week, to peak at the release of BoE’s interest rate decision on Thursday. BoE is widely expected to remain on hold at 5.25% and GBP OIS currently imply a probability of 98% for such a scenario to materialise. Market participants are expected to keep a close eye on the accompanying statement and we expect the bank to maintain a rather hawkish tone, given that the CPI rate is still above the bank’s target and seems to have difficulties easing further, which in turn may support the pound. Any easing of the bank’s hawkishness on the other hand could substantially weigh on the pound as it would contradict the market’s expectations. We also note the vote count of the decision and any deviation from the prior vote count, could signal a shift in the balance of power within the bank, possibly affecting the pound’s direction.

JPY – To hike or not to hike

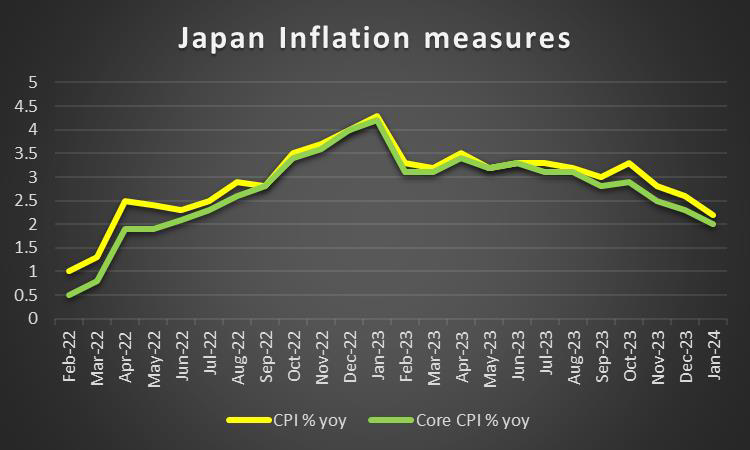

JPY is about to end the week lower against the USD, the EUR and the pound in a sign of a wider weakness. The main issue tantalising JPY traders is currently the intentions of BoJ. Hence we highlight BoJ’s interest rate decision on Tuesday’s Asian session. Currently, market expectations for the bank are almost evenly split with JPY OIS implying that the bank may remain on hold at -0.10% by 58.38%, with the rest implying that a 10 basis points rate hike is also possible. So there is a relative uncertainty for the rate decision itself. It should be noted that headline CPI rates are slowing down both on a headline and core level, with the headline rate reaching the bank’s target of 2%. The easing of inflationary pressures would be advising a possible delay of any rate hikes. Yet on the other hand, we note that Japanese workers seem to have secured a big pay rise, actually the biggest in decades, which was considered as a key prerequisite from BoJ before hiking its interest rates. Should the bank remain on hold we may see JPY slipping as part of the market will be disappointed, while a possible hike would be unexpected by the market and could cause the JPY to rise asymmetrically. At this point, we have to note that market prices in a rate hike in the bank’s next meeting in April, another rate hike due in September and a third in December. Should the bank remain on hold though we expect the market to shift its attention toward the accompanying statement and if the bank starts preparing the markets for rate hikes to come, we may see JPY gaining some ground. Yet should the bank maintain its dovishness we may see JPY weakening substantially.

EUR – Preliminary March PMI figures to move the EUR

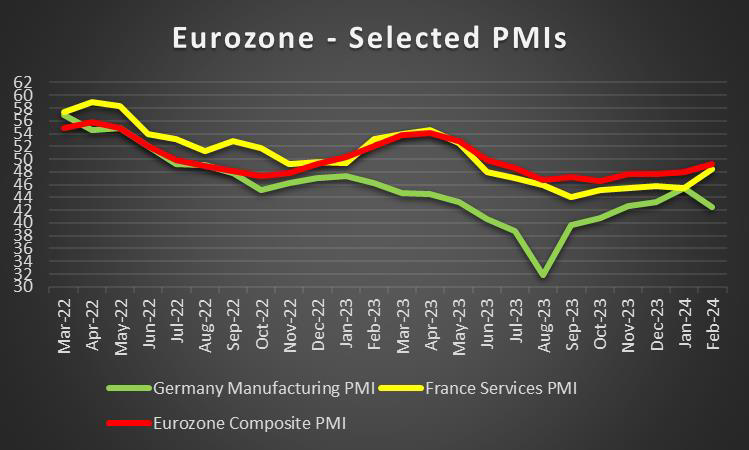

The common currency seems about to end the week relatively unchanged against the greenback, yet comes out stronger against the pound and the Yen. On a macroeconomic level, we note that the easing of inflationary pressures for February in the two largest economies of the Eurozone, France and Germany was confirmed. Furthermore, we note the wide contraction of the Eurozone’s industrial production for February in a sign of shrinking economic activity. The release elevates the interest of the markets regarding the preliminary PMI figures of March due out on Thursday. We tend to focus on Germany’s manufacturing sector, the economic powerhouse of the Eurozone which has suffered a continuous and deepening contraction of economic activity transforming it into the problem child of the area. On the other hand, the Eurozone as a whole, seems to be slowly recovering, more than making up for the contraction of economic activity in Germany’s factories. Should the release indicate further improvement in economic activity in the area, we may see the common currency getting some support. On the monetary front, we note that the market expects the bank to start cutting rates in June and deliver three rate cuts in total within the year. Dovish signals seem to be escaping the ECB as policymakers seem to push for rate cuts. In the dovish side of the ECB’s monetary policy spectrum, we highlight Greece’s Stournaras’ comments on the need for the bank to cut rates twice before its summer break. On a more moderated view ECB chief economist Lane seems to also recognise the need for a rate cut, yet at the same time also highlights that the bank must take its time before cutting rates. Should the ECB policymakers’ calls for a delay in the start of rate-cutting multiply, contradicting market expectations, we may see EUR getting some support.

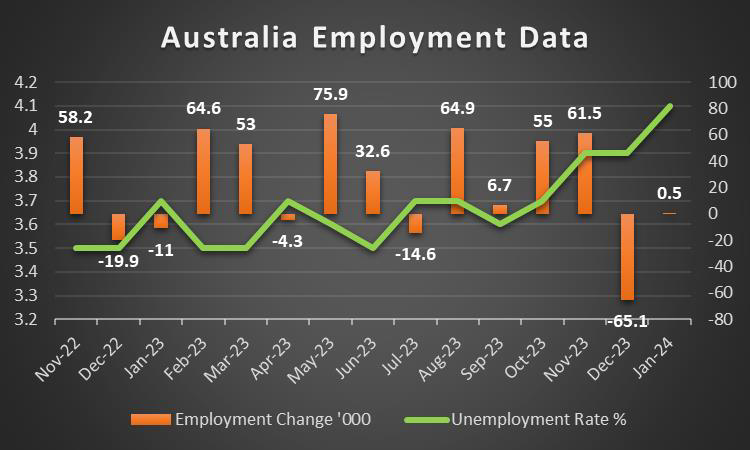

AUD – RBA’s interest rate decision in focus

The Aussie is about to end the week relatively lower against the USD. On a macroeconomic level, we note the improvement of business conditions in Australia for February which was yet accompanied by slightly less optimism. In the coming week, we note the release of Australia’s employment data for February on Thursday. Should the readings show further easing in the Australian employment market, we may see the release weighing on the AUD. On a more fundamental level, we note the sensitivity of AUD to developments in China, given the close Sino-Australian economic ties. Early on Monday, we get China’s industrial production growth rate for February and a possible slowdown could weaken the Aussie as it could imply fewer exports of raw materials from Australia to China. On the monetary front, we highlight RBA’s interest rate decision on Tuesday’s Asian session. The bank is widely expected to remain on hold as AUD OIS implies a probability of 93.78% for such a scenario to materialise. Hence market attention is expected to shift to the release of the accompanying statement. It should be noted that the bank in its last interest decision, stated that “a further increase in interest rates cannot be ruled out”. The statement was deemed as hawkish and tended to provide some support for the Aussie. The market currently expects the bank to start cutting rates in August and deliver another rate cut in December. Yet should the bank actually maintain the hawkish tone of the prior decision, implying in contrast to market expectations, that another rate hike is possible, it could provide substantial support for the Aussie. Any failure of the bank to sound hawkish enough could weigh on AUD.

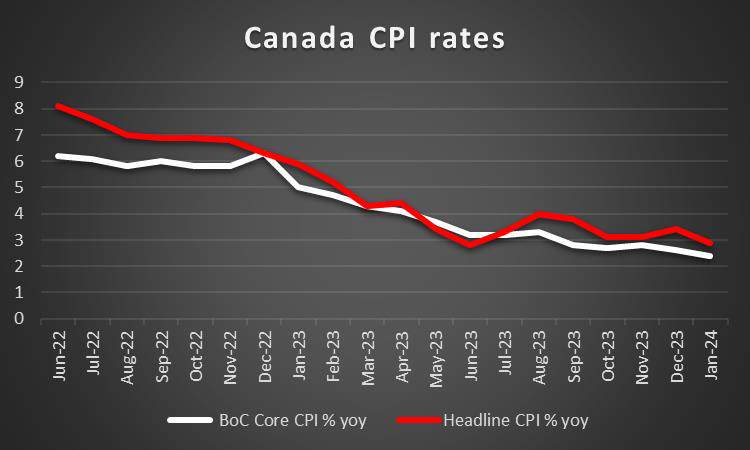

CAD – CPI rates in focus

The Loonie is about to end the week lower against the USD. On a macroeconomic level, we note the acceleration of the manufacturing sales for January, as the rate showed growth once again. Next week, we highlight the release of Canada’s CPI rates for February. Should inflationary pressures in the Canadian economy slow down, we may see more pressure building up on BoC to start easing its monetary policy and thus could weigh on the Loonie. On a monetary level, we note the market’s expectations currently, for the bank to start cutting rates in July and deliver two maybe three rate cuts in the year. Also please bear in mind the hawkish predisposition of the bank in its last interest rate decision. On the other hand, inflation is already within the bank’s 1-3% inflation target zone and pressure on the bank to start cutting rates may be increasing. On a fundamental level, we note the positive correlation of oil prices with the Loonie. The rise of oil prices over the past week may have prevented the CAD from weakening materially against the USD. Should we see a continuance of the strengthening of oil prices, we may see the CAD gaining ground. Also given the perceived riskier nature of the CAD, should market sentiment improve over the coming week, it could prove to be another factor supporting the Loonie.

General Comment

As a general comment, we expect the USD to maintain some of the initiative in the FX market against other currencies. Yet given that the calendar of the coming week is full of high-impact financial releases and events stemming from other countries, we may see the influence of the USD receding somewhat. In the US equities markets, we note the bullish sentiment, yet there seems to be some hesitancy on behalf of the bulls. It’s characteristic that Dow Jones and Nasdaq, despite being in the greens for the week, seem unable to reach new record highs. In contrast, the S&P 500, which as an index has a broader base and seems to continue its upward motion keeping the hope alive. On a company level, we highlight the troubles of Boeing (#BA) in production quality control being ongoing, which continue to weigh on the company’s share price. The only reason the company has not faced the risk of bankruptcy yet might be the lack of substantial alternatives, given that Airbus, which is Boeing’s main rival, is working at full production capacity, while its order books are also pretty full. Overall the tendency for the time being is for Airbus to get support while on the flip side, Boeing’s share price sinks. We also maintain our worries for Tesla (#TSLA) as the negative headlines continue to multiply. It’s characteristic that Wells Fargo downgraded the share’s outlook and highlighted the potential for Tesla’s stock to fall as much as 23% as it is characterized as a ‘Growth company with no growth’. In the gold market, we highlight the drop in gold’s price for the week after three consecutive weeks of gains and

hitting new record high levels. Given the negative correlation of the USD with gold’s price the rise of the USD against its counterparts may have been the main factor behind the drop of gold’s price along with the rise of US yields. Overall should the USD continue to rise in the coming week, we may see bearish tendencies of gold’s price intensifying and vice versa.

If you have any general queries or comments relating to this article please send an email directly to our Research team at research_team@ironfx.com

Disclaimer:

This information is not considered as investment advice or an investment recommendation, but instead a marketing communication. IronFX is not responsible for any data or information provided by third parties referenced, or hyperlinked, in this communication.