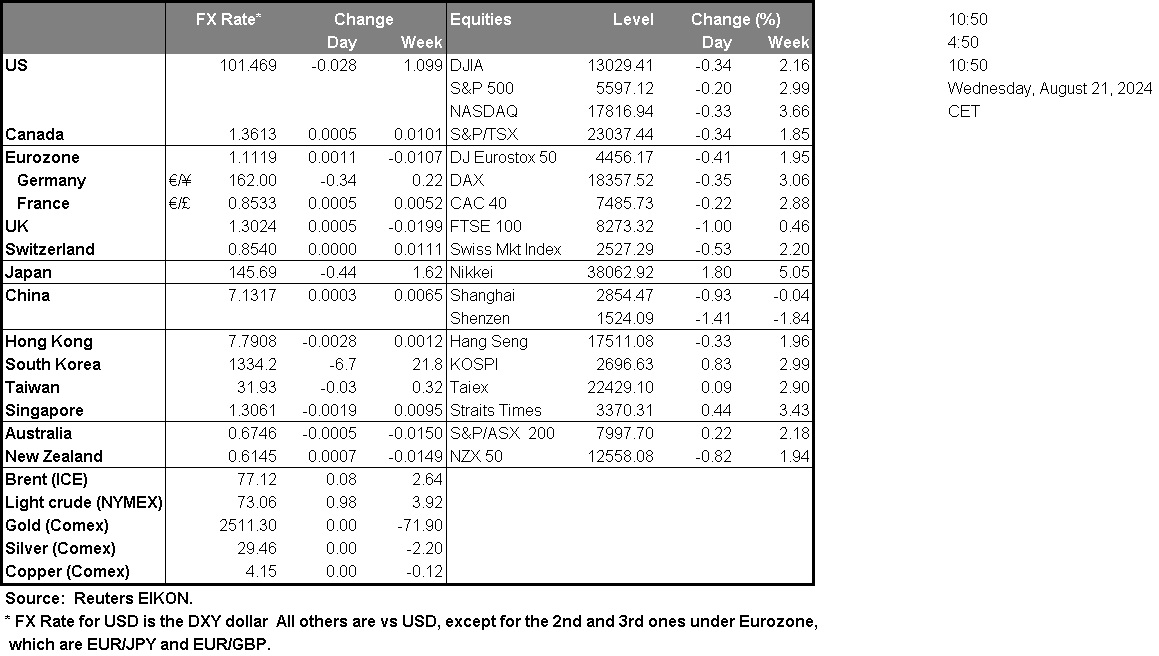

The USD continued to weaken against its counterparts yesterday, as the market’s expectations for the Fed remain heavily tilted to the dovish side. The markets currently expect the Fed to start cutting rates in its next meeting in September and continue to deliver another rate cut in the November meeting and a double rate cut in the December meeting according currently, to Fed Fund Futures. Despite the market’s expectations may be over fetched its dovish orientation is very clear. Hence, we highlight today the release of the Fed’s July meeting minutes. Should the document be characterised by a sufficiently dovish tone thus verifying the market’s expectations it could weigh on the USD and provide support for US stock markets and gold. Any comments of Fed policymakers, implying a less dovish path on behalf of the bank could force the market to reposition itself providing support for the USD and adding selling pressure on US stock markets and gold.

As for US stockmarkets on a technical level, we note that the Dow Jones edged lower yesterday, with the bulls practically taking a break just above the 40800 (S1) support line. We tend to maintain a bullish outlook for the index as long as the upward trendline guiding the index since the 8th of August remains intact. Also please note that the RSI indicator remains between the reading of 50 and 70, implying the presence of a bullish market sentiment for Dow Jones. Should the bulls maintain control over the index, we may see it taking aim of the 41435 (R1) resistance line. Should the bears take over, we may see the index breaking the prementioned upward trendline, signaling an interruption of the upward movement, the 40800 (S1) support line clearly and take aim of the 40050 (S2) support level.

In the FX market, we turn our attention towards JPY which tended to benefit from USD’s weakness over the past few days. Tomorrow, we get the preliminary PMI figures for August and attention is being placed on the figure for Japan’s manufacturing sector. A possible improvement of indicator’s reading, would imply an improvement of economic activity for the crucial sector and could support the Yen. Yet during tomorrow’s Asian session, we also get some data related to the demand side of the Japanese economy, and an acceleration of the chain retail sales growth rate for July could provide some support for the JPY. Yet financial data may not be the main driver of JPY’s direction, hence we highlight BoJ’s stance. Yen traders’ attention is expected to turn towards the Japanese Parliament’s session on Friday, at which BoJ Governor Ueda is scheduled to testify about the July rate hike. BoJ’s Governor is to justify the decision to hike rates for a second time this year at the bank’s July meeting and we expect Mr. Ueda to maintain the view of persistent inflationary pressures in the Japanese economy which could allow for more rate hikes to come, thus supporting the Yen.

USD/JPY continued to fall for a third day in a row yesterday breaking the 146.00 (R1) support line, now turned to support. We tend to maintain a bearish outlook for the pair as long as the downward trendline, incepted since the 16th of August, remains intact. Also we note that the RSI indicator despite a slight correction higher during today’s Asian session remains just above the reading of 30, implying that the bearish sentiment of the market for the pair is maintained. Should the bears take over, we may see the pair aiming for the 143.40 (S1) support line. Should the bulls take over, we may see the pair breaking the prementioned downward trendline and continue to break the 146.00 (R1) resistance line and aim for the 148.90 (R2) resistance base.

Other highlights for the day

Today we get in the American session, from Canada the July producer prices and the release of the EIA crude oil inventories figure. During tomorrow’s Asian session, we get Australia’s preliminary August PMI figures.

US30 Cash Daily Chart

- Support: 40800 (S1), 40050 (S2), 39300 (S3)

- Resistance: 41435 (R1), 42200 (R2), 43000 (R3)

USD/JPY Daily Chart

- Support: 143.40 (S1), 140.35 (S2), 137.25 (S3)

- Resistance: 146.00 (R1), 148.90 (R2), 151.90 (R3)

If you have any general queries or comments relating to this article please send an email directly to our Research team at research_team@ironfx.com

Disclaimer:

This information is not considered as investment advice or an investment recommendation, but instead a marketing communication. IronFX is not responsible for any data or information provided by third parties referenced, or hyperlinked, in this communication.