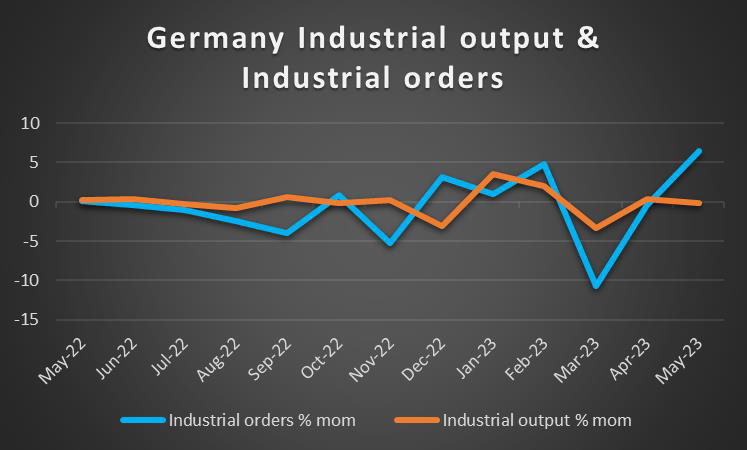

With the week nearing its end, we note that the US employment report for July is still to be released as these lines are written and could alter the big picture of the market. In the coming week, we expect volatility to ease a bit, yet there are still highlights that could keep traders interested. On the monetary front, we note that a number of policymakers from various central banks are scheduled to make statements and could swing the market’s opinion and we single out the release from Japan of BoJ’s summary of opinions for its July meeting during Monday’s Asian session. As for financial releases, we make a start with the release of Germany’s industrial output for June and the UK’s Halifax House prices for July. On Tuesday we get from Japan the current account balance for June, China’s trade data for July, Germany’s final HICP rate for July and Canada’s trade data for June. On Wednesday we note the release of China’s inflation metrics, while on Thursday we get Japan’s corporate goods prices, Norway’s and the Czech Republic’s CPI Rates yet the main release is expected to be the US CPI rates, all being for July. On Friday we note the release of the UK GDP rates, France’s final HICP rates and from the US we get the preliminary University of Michigan consumer sentiment for August.

USD – US CPI rates at the forefront

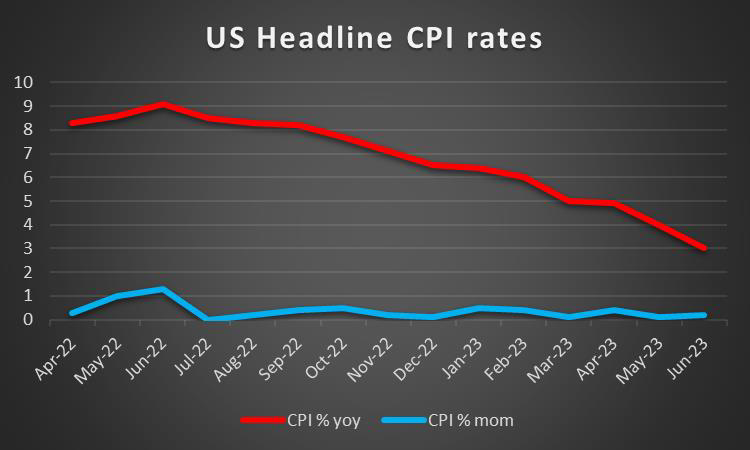

The USD continued its upward trajectory against its counterparts for a third week in a row, yet we note that the US employment report for July is still to be released and could alter USD’s direction. On a fundamental level, we highlight the downgrading of the US by the Fitch credit rating agency. The credit rating agency stripped the US from its perfect AAA rating and downgraded it to AA+. The main reason cited for the decision was the expectation of a difficult fiscal expansion ahead as the US Government, due to the high US debt and debt ceiling rules after the agreement reached with Congress were raising some degree of uncertainty. The US Government strongly disagreed with the rating agency’s decision and stated that the decision to downgrade the US “defies reality to downgrade the United States at a moment when President Biden has delivered the strongest recovery of any major economy in the world,“. It should be noted that Fitch is the second credit rating agency downgrading the US after Standard & Poor’s back in 2011. The news tended to raise US Bond yields and cause the USD to wobble, yet for the time being, we expect the overall effect to be temporary. It was characteristic that recent US financial data and a number of economists citing the downgrade as out of place tended to out-trump Fitch’s decision allowing for market confidence in the recovery of the US economy to remain present. On a monetary level, the market seems to maintain the view that the Fed has reached its terminal rate and the rate hiking cycle has come to an end. On a macroeconomic level, we highlight the release of the US CPI rates for July which in conjunction with the US employment report for July is to provide additional insight to the Fed’s next possible moves. Should CPI rates show that inflation eased further in July, we may see market expectations for the Fed to remain on hold intensifying and thus weakening the USD and vice versa.

GBP – GDP rates at the end of the week

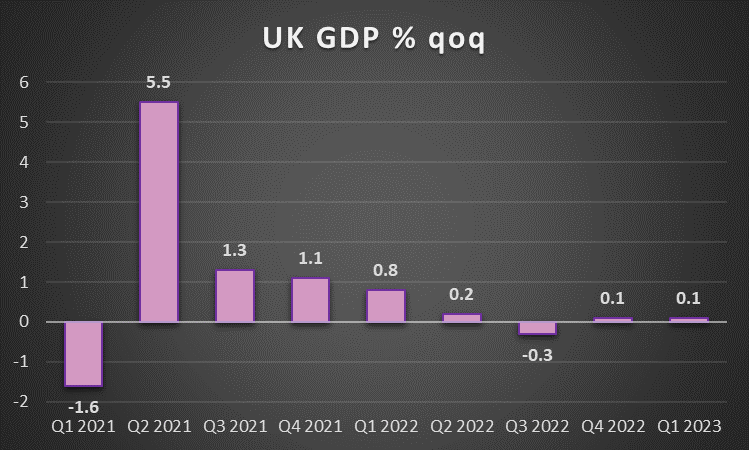

The pound seems about to end the week lower against the USD and the EUR and tends to remain stable against the JPY. It’s characteristic of GBP’s weakening that even the 25 basis points rate, delivered by BoE was not able to reverse the pound’s direction. The decision was partially priced in, yet it was indicative of the market’s hawkish predisposition before the release that the market seemed to also partially expect that the bank could hike rates not by 25 but by 50 basis points. In its accompanying statement, the bank stated that its monetary policy is already at restrictive levels, yet the “MPC will ensure that Bank Rate is sufficiently restrictive for sufficiently long to return inflation to the 2% target sustainably in the medium term, in line with its remit”. The statement may not have satisfied the market’s hawkish expectations and definitely given that the bank itself expects inflation to fall to 5% by the end of the year, which is substantially above the bank’s 2% target, a wider rate hike may have been required in our opinion. On a macro-economic level, we note the contraction of the nationwide house prices for July, while the slower expansion of economic activity for the crucial services sector in July was confirmed, both being a minus for the GBP. In the coming week, we note the release of the UK GDP rate for Q2 and a possible slowdown of growth or even a contraction could have an adverse effect on the pound. Yet we note that with GDP rates being at anemic levels for Q1, it’s a matter of time before the UK economy starts contracting, given the tight monetary policy of the BoE.

JPY – BOJ’s summary of opinions eyed

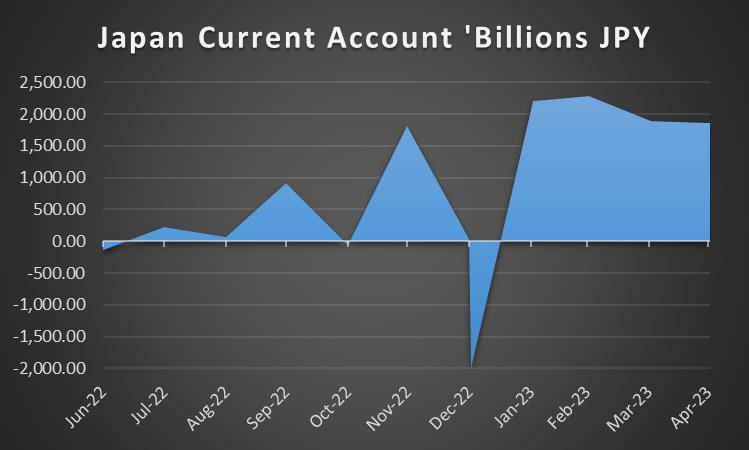

JPY is about to end the week lower against the USD and to a lesser extent against the EUR, while seems to remain rather stable against the GBP, in a sign of a broader weakness. On a monetary level, we note the release of BoJ’s summary of opinions for the July meeting on Monday. The bank in its July interest rate decision had tweaked its monetary policy settings by making more flexible its Yield Curve Control (YCC) policy as it decided to allow the yields of Japanese Government Bonds (JGBs) to rise up to 1% before proceeding with purchases, yet 1% is not to be an absolute cut off point. The release may allow us to get a deeper insight into the bank’s intentions and whether there were any reactions to the decision of BoJ policymakers and to which direction. We highlight the release as BoJ’s monetary policy is a key issue currently for JPY’s direction. On a more fundamental level, we note JPY’s dual nature as a safe haven and a national currency and should we see market worries on an international level easing and a more risk-on approach emerging by the market, we may see the Japanese currency suffering safe haven inflows. Furthermore, on a fundamental level, we express our sympathy for the typhoon that hit Japan, leaving behind at least two dead and thousands of homes without power. On a macroeconomic level, we note the acceleration of Japan’s preliminary industrial output growth rate for June, which was a positive for the currency and note for the coming week the release of the household spending, the current account and trade balances, all being for June on Tuesday as well as the corporate goods prices for July on Thursday.

EUR – Fundamentals to take over

EUR is about to end the week in the reds against the USD, yet seems to be gaining some ground against the pound and the JPY. On a macroeconomic level, we note that the slowdown of the Eurozone’s HICP rate for July was confirmed as was the contraction of economic activity in Germany’s manufacturing sector for the same month. Yet the easing of inflationary pressures in the Eurozone was further supported by the deeper contraction of the Eurozone’s PPI prices for June. Hence we may reasonably continue to expect that inflation as a whole in the Eurozone is on the retreat, which could be considered as a comforting sign. Our worries now extend to the contraction of economic activity that may bring if not the Eurozone then Germany in a recession. It’s characteristic that IMF expects the German economy to be the only one to contract, given the difficulties presented by high energy prices, rising borrowing costs and headwinds in the recovery of the Chinese economy, a key trading partner for Germany. On the monetary front, we note the market’s expectations currently for ECB to remain on hold, keeping the refinancing rate at 4.25%, yet ECB officials have been warning and continue to do so, that the bank is to leave rates at high levels for a longer period and we would add that the possibility of another rate hike by ECB is still on the table. Such a scenario is expected to continue to have a detrimental effect on economic activity in the Eurozone and may enhance the possibility of recession or even deepen one. In the coming week, we note that the number of high-impact financial releases is to be reduced thus allowing for fundamentals to get in the driver’s seat setting the direction for the common currency.

AUD – RBA remained on hold

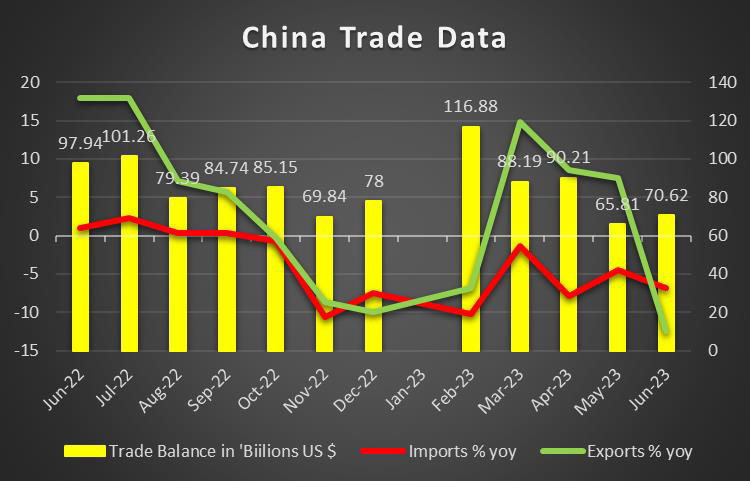

AUD is about to end the week lower against the USD for a third week in a row. On a monetary policy level, we note that RBA remained on hold at 4.10% last Tuesday. In Governor Lowe’s accompanying statement, it’s mentioned that the bank chose to remain on hold as “This will provide further time to assess the impact of the increase in interest rates to date and the economic outlook” while also mentioned that “Some further tightening of monetary policy may be required to ensure that inflation returns to target in a reasonable timeframe, but that will depend upon the data and the evolving assessment of risks”. The decision was perceived by market participants as dovish and tended to weigh on the Aussie at the time of the release. The market seems to expect that the bank has reached its terminal rate and is to remain on hold until the end of the year. Hence, we may see monetary policy outlook differentials weighing somewhat on the Aussie, albeit we have to note here that other central banks such as the BoC, ECB and the Fed are nearing or may have reached their terminal rate as well. On a macroeconomic level, we note that Australia’s trade surplus narrowed less than expected, which was good news, yet the worrying part is that the result came from a simultaneous contraction of both the import and export growth rates, once again implying less economic activity, at least at an international transactions level. On a more fundamental note, the Chinese economic recovery seems to be facing headwinds, as both the NBS and the Caixin manufacturing PMI figures for July implied a contraction of economic activity for the past month. Hence the figures from China may also imply fewer exports of raw materials from Australia to China which could weigh on the Aussie. We are about to get a clearer picture on Tuesday as China’s trade data for July are to be released.

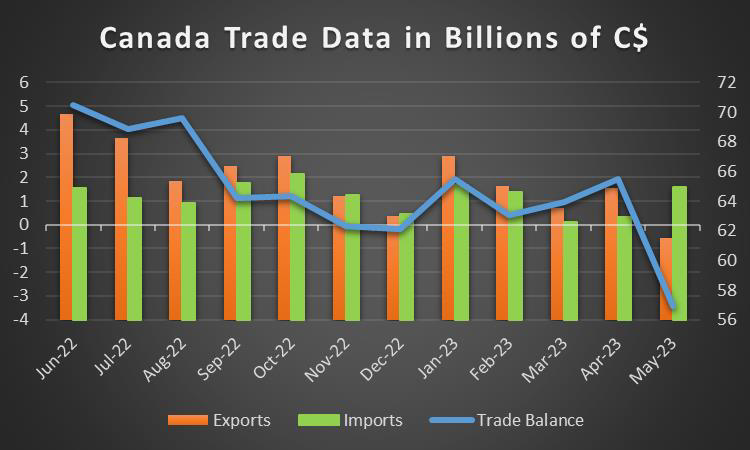

CAD – Trade data and oil prices

The Loonie was not able to resist the advancement of the USD and is about to end the week in the reds. We note that Canada’s and the US’s employment data for July are still to be released and may alter the picture. On a fundamental level we note that for a sixth week in a row, yet on Wednesday, oil bulls seemed to hesitate as the US was downgraded by Fitch. Nevertheless, the surrounding environment seems to remain bullish for oil prices, given the tight US oil market as implied by substantial drawdowns of US oil inventories, reported for the past week and in addition to that there seems to be no sign from OPEC+ that it plans to increase production levels, on the contrary, it seems about to expand the low production levels into September. Should oil prices continue to be on the rise, we may see the CAD getting some support as Canada is a major oil-producing economy. On a macroeconomic level, we note in the positives that Canada’s GDP rate accelerated for May, which tends to allow for less pessimism for Canada’s economic outlook. Furthermore, we note that Canada’s manufacturing PMI figure for July improved, yet remained below the reading of 50, implying another contraction of economic activity for the sector. In the coming week, we note the release of Canada’s trade data for June should the trade deficit narrow, we may see the Loonie getting some slight support. On the monetary front, we note the market’s expectations for the Bank of Canada to remain on hold at 5.00%, yet at the same time the prospect of another rate hike in the October meeting seems to be still open. At this point, we would note the criticism being exercised on BoC Governor Tiff Macklem at a political level, by Canada’s Prime Minister Trudeau for raising interest rates to 5%, yet we expect the bank to chart its own independent course.

General Comment

I the coming week we expect volatility in the FX market to ease given that the number of high-impact financial releases is to be reduced and we enter August, a traditional holiday month for European and North American traders. We also note that the earnings season in the US is still in full swing, albeit most high-profile companies have already released their earnings reports. Nevertheless, we would note Walt Disney (#DIS) and Canopy Growth (#CGC) on Wednesday as points of interest among others. A possible improvement of the market sentiment could provide some support for US stock markets and allow them to maintain, or even renew their bullish tendencies. As for gold’s price, we maintain the view that it’s affected by the negative correlation with the USD which was more than evident in the past few days, once again. US yields did not dramatically change over the week at a two-year level, yet for the ten-year bond yield, the rise was noticeable, which may have enhanced the drop in the precious metal’s price. On a more fundamental level, we note that the uncertainty created by the war in Ukraine tends to remain present and is having a renewed effect on the global economy. It was characteristic how the prices of wheat and corn fluctuated which tended to pose large question marks for economic growth and food stability on a global level.

If you have any general queries or comments relating to this article please send an email directly to our Research team at research_team@ironfx.com

Disclaimer:

This information is not considered as investment advice or an investment recommendation, but instead a marketing communication. IronFX is not responsible for any data or information provided by third parties referenced, or hyperlinked, in this communication.