The week is coming to an end and we take a peek at what next week has in store for the markets. On the monetary front we highlight the release of FED’sinterest rate decision and the release of the BoC’s summary of deliberations on Wednesday, Norway’s the BoE’s and the CBT’s interest rate decisions on Thursday and the BOJ’s interest rate decision on Friday. As for financial releases, we get on Monday from the US the NY Fed manufacturing figure for September and Canada’s manufacturing sales rate for July. On Tuesday we get Germany’s ZEW figures for September, Canada’s housing starts figure, the US retail sales rate, Canada’s CPI rates and the US industrial production rate all for the month of August. On Wednesday Japan’s machinery order rate for July and trade balance figure for August, the UK’s CPI rate and the Eurozone’s final HICP rate both for the month of August. On Thursday we get, New Zealand’s GDP rate for Q2, Australia’s employment data for August, the US weekly initial jobless claims figure and the US Philly Fed Business index for September. On Friday, we get Japan’s CPI rates for August, the UK’s retail sales rate for August, France’s business climate figure for September, Canada’s producer prices rate for August and ending off the week is the Eurozone’s preliminary consumer confidence figure for September.

USD – Fed on the way to cut rates by 25bp?

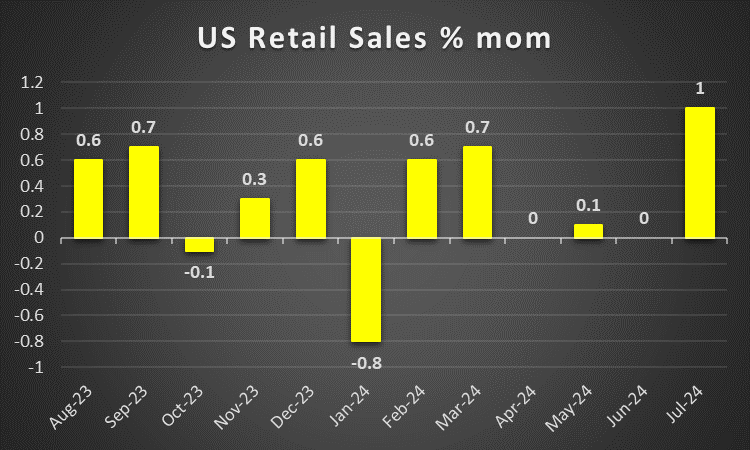

We make a start for the USD by noting that the US headline CPI rate for August came in as expected, implying easing inflationary pressures in the US economy. In turn this appears to have eased markets expectations of an aggressive 50bp rate cut by the Fed in their monetary policy meeting next week. In particular, the majority of market participants are anticipating the bank to cut by 25bp with FFF currently implying an 83% probability for such a scenario to materialize. Continuing on a monetary level, the Office of the Inspector General found Atlanta Fed President Bostic violated the FOMC’s blackout rule amongst others, and created an “appearance of acting on confidential FOMC information”. Nonetheless, the consequences or if there will be any, are yet to be seen. On a political level, we note that the first Presidential debate between Harris and Trump occurred on Monday, with numerous media outlets claiming that Harris outperformed Trump which may cast doubt over the outcome of the US Presidential elections and thus may increase volatility in the greenback. In the coming week, we highlight the release of the retail sales rate for August which is expected to showcase a weakening from the consumer side of the US economy and could weigh on the USD.

GBP – BoE decision & CPI rate next week

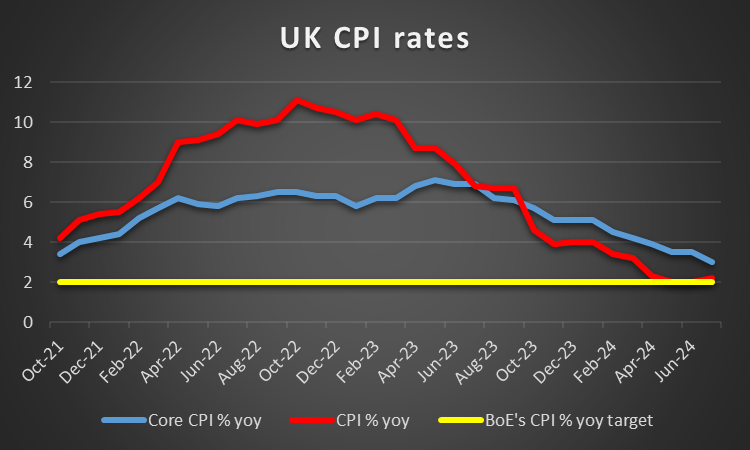

On a fundamental level for pound traders we note that the Office for Budget Responsibility warned that the British public debt is like to soar to triple its current level of the next 50 years if future governments do not take action. On the monetary front we note the market’s expectations for BoE to take a breather in their next meeting with GBP OIS currently implying a 76.71% probability for such a scenario to materialize. Moreover, the bank is expected to continue cutting rates from November onwards. Such market expectations could provide some support for the pound against the dollar given the markets’ expectations for the Fed to start cutting rates. On a macroeconomic level, we highlight the release of the UK GDP rates for July which came in lower than expected implying a slower expansion of the UK economy. Moreover, the industrial output and the manufacturing output growth rate both for July, decelerated which may intensify the bearish sentiment for the pound. For next week, attention may also turn to the UK’s CPI rates for August. Should the CPI rates come in at or below the previous rate of 2.2% which could either imply easing inflationary pressures and remain near the bank’s 2% inflation target it could further amplify pressure on the BoE to cut interest rates sooner rather than later. In turn, such a scenario could weigh on the British pound. On the flip side, should the CPI rate showcase an acceleration or a persistence of inflationary pressures in the UK economy, it could increase pressure on the BoE to remain on hold and thus could provide support for the pound.

JPY – BOJ decision in the epicenter

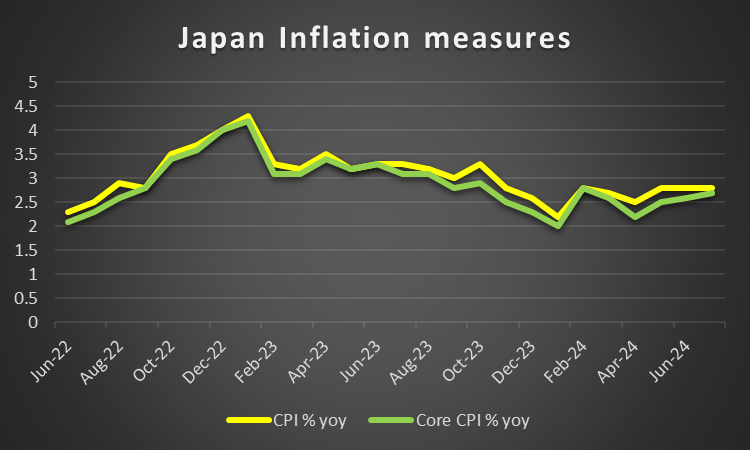

On a fundamental level, we note for JPY traders that according to a report by the FT, the country is facing its biggest rice shortage in 30 years, which may be worth monitoring until the issue is resolved. On a monetary level, we would like to note the BOJ’s interest rate decision which is set to occur next week. The majority of market participants are currently anticipating the bank to remain on hold at 0.25% with JPY OIS currently implying a 99.5% probability for such a scenario to materialize. However, despite the current market expectations of the bank remaining on hold in their next meeting, we would not be surprised to see the bank’s accompanying statement take a more hawkish tone. In particular, BOJ member Tamura stated according to Reuters that “ it’s necessary to push up our short-term policy rate at least to around 1%” to sustainably achieve the BOJ’s price goal”, hence should the BOJ’s accompanying statement appear predominantly hawkish in nature, it could support the JPY. On the flip side, should BOJ policymakers imply that the bank may keep interest rates steady in the near future, it may weigh on the JPY. On a macroeconomic level, the JPY’s GDP rate for Q2 came in lower than expected, implying that the Japanese economy grew but at a slower rate which could be a cause of concern and should it deteriorate, it may weigh on the JPY. Nonetheless, for next week we would like to note Japan’s CPI rates for August, in which should signs be shown that inflation is nearing the bank’s 2% target sustainably, it may provide greater confidence to the bank to continue hiking interest rates.

EUR – ECB cuts interest rates as expected

The ECB cut both the refinancing and deposit rate, as it was widely expected. However, according to ECB President Lagarde, services inflation is still higher than expected, which appears to have caused a slight upwards revision of core inflation expectations for 2024 and 2025 which could imply that the bank may need to withhold from aggressively cutting interest rates in order to combat persistent inflationary pressures in the zone. In turn this appears to have aided the common currency following its release, as concerns about a persistence of inflationary pressures in the eurozone appear to be on the mind of ECB policymakers. On a fundamental level, we note that the decision by German authorities to conduct checks at all land frontiers in a bid to stem illegal immigration appears to be causing a rift between Germany and it’s European allies with Donald Tusk stating per the FT that the announcement by Germany is unacceptable and that it is a “de facto suspension of the Schengen Agreement on a large scale”. Overall, should rifts appear within the EU, it could weigh on the common currency.

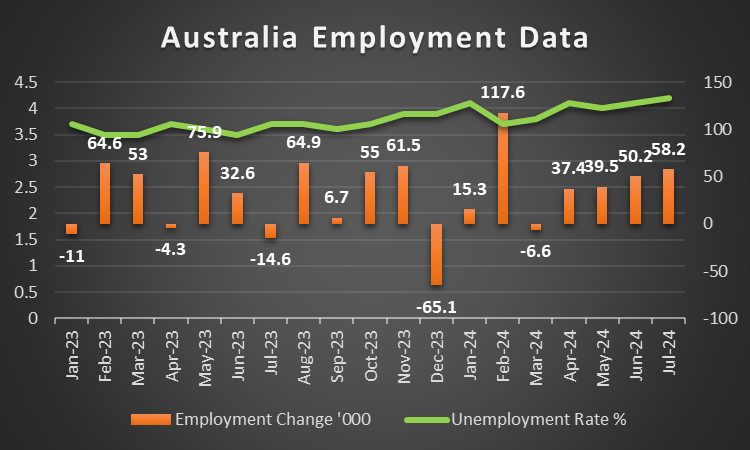

AUD – Employment data next week for the Aussie

On a macroeconomic level, we note for Aussie traders it was a pretty easygoing week in terms of financial releases stemming from Australia and thus attention may turn to next week’s employment data. In particular, the unemployment rate for August which is set to be released on Thursday. Should the unemployment rate come in higher than the previous rate of 4.2%, implying a loosening labour market it could potentially increase pressure on the RBA to cut interest rates which in turn may weigh on the AUD. On another macroeconomic level, we would like to note China’s trade data and in particular their imports rate for August which came in lower than expected at 0.5% versus the expected rate of 2.0%. Hence, the lower than expected imports rate may imply a reduction in demand for raw materials stemming from Australia, which could weigh on the Aussie. Yet on a deeper fundamental level, we also note that the recent crackdown by the Chinese authorities on investment bankers could reduce foreign investment into the Chinese financial sector. In turn, a reduction in investment in the country could dampen China’s economic recovery hopes and thus given the close economic ties with Australia, it could also weigh on the AUD.

CAD – Oil prices and the release of the BoC’s deliberations to watch out for

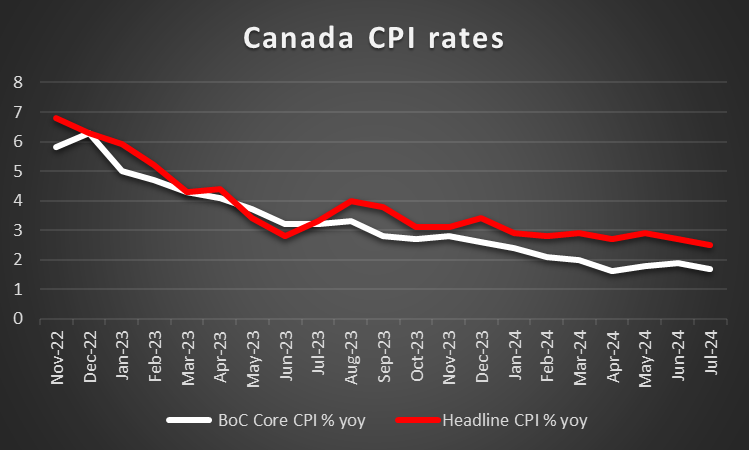

On a macroeconomic level, Canada’s employment data for August which was released last Friday, showcased a loosening labour market. In particular, the unemployment rate ticked upwards from 6.4% to 6.6% in addition to the employment change figure coming in lower than expected at 22.1k versus the expected figure of 23.7k. Furthermore, Canada’s Ivey PMI figure came in lower than expected at 48.2 versus 55.3, implying a contraction in Canada’s manufacturing sector. Overall last week’s financial releases stemming from Canada appear to indicate negative implications for the Canadian economy, which may have weighed on the CAD. On a monetary policy level, we the implications of a struggling Canadian economy, may increase pressure on the BoC to cut interest rates more aggressively which may further weigh on the CAD. In addition, a greater degree of emphasis may be placed on the release of the BoC’s summary of deliberations on Wednesday, where should it be implied that the bank may continue on its rate cutting cycle it may weigh on the Loonie. However, should it imply some form of hesitation from BoC policymakers it could have the opposite effect. Lastly, on a fundamental level, we would like to note that oil prices appear to have remained flat since the beginning of this week. Yet should they continue on their overall downwards trajectory, it may weigh on the Loonie, given Canada’s status as a major oil producing country.

General Comment

As an epilogue we expect the USD to maintain the initiative over other currencies in the FX market, mainly due to the Fed’s interest rate decision. Yet other currencies such as GBP could come under the spotlight, which in turn may enrich the trading mix. As for US stock markets, we note some relief for US stock markets, with the Dow Jones, S&P 500 and Nasdaq all moving higher for the week. We expect that the Fed’s interest rate decision, could have an effect on the direction of US stock markets. As for gold’s price we note that the precious metal has formed new all-time highs. Also the clear drop of US yields since the start of the week, tends to enhance the positive effect for gold’s price.

If you have any general queries or comments relating to this article please send an email directly to our Research team at research_team@ironfx.com

Disclaimer:

This information is not considered as investment advice or an investment recommendation, but instead a marketing communication. IronFX is not responsible for any data or information provided by third parties referenced, or hyperlinked, in this communication.