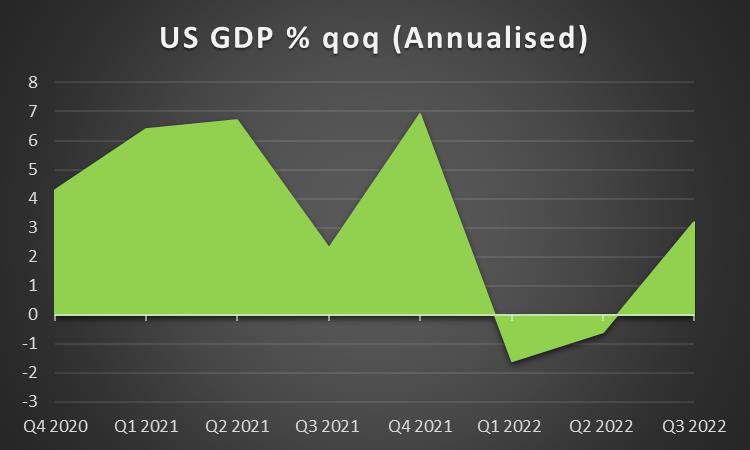

As we leave behind us an interesting week, we open a window at what next week has in store for the markets. On a monetary level, we note the release of BoC’s interest rate decision on Wednesday, while BoJ is to release the summary of opinions for its January meeting on Thursday. Also, note that a number of policymakers from various central banks are scheduled to speak, make statements and could sway the market’s opinion. Υet Fed policymakers are to keep a moratorium of statements ahead of the Fed’s meeting on the 1st of February, which may allow the intensification of speculation among market participants for the Fed’s intentions. As for financial releases we note on Monday, the release of Eurozone’s preliminary Consumer Confidence for January and on Tuesday, we note the release of the preliminary PMI figures for January of Japan, France, Germany, Eurozone, the UK and the US, while we also get Germany’s GfK Consumer Confidence for February, UK’s CBI trends for industrial orders and New Zealand’s CPI rates for Q4. On Wednesday, we get Australia’s CPI rates for Q4 and Germany’s Ifo indicators for January while on Thursday we get UK’s CBI distributive trades for January and from the US the durable goods orders for December, the weekly initial jobless claims figure and we highlight the highlight of the week, namely the US GDP advance rate for Q4. Finally on Friday, we get from Japan Tokyo’s CPI rates for January and from the US the consumption rate for December and the final University of Michigan consumer sentiment for January.

USD – US GDP rate to lead the greenback

The USD is about to end the week near the same levels it began, against its counterparts, maybe a little bit higher. On the monetary front, we note that we had some mixed signals from Fed policymakers in the past few days. It was characteristic that Cleveland Fed President Mester on Wednesday stated that there is evidence that interest rate hikes have started to lower inflationary pressures, finally. The interesting element of the comments come from the fact that Mester was considered to be among the hawks in the central bank supporting a more aggressive stance. On the flip side, St. Louis Fed President Bullard stated that Fed’s policymakers should maintain a rapid interest rate hike pace and also stated that he would be open to the idea of another 50-basis points rate hike, something that is in contrast to market expectations for a 25 basis points rate hike in the bank’s next meeting. Overall, though we note that given the statements made in the past two weeks, there seems to be a consensus building up among Fed policymakers that the bank is to ease its aggressive stance and downshift its rate hiking path. On a macroeconomic level, we note that the retail sales growth rate dived deeper into the negatives than expected as did the industrial production growth rate, while the PPI rate slowed down more than expected, all for the month of December. We consider the financial data released on Wednesday, as a result of the Fed’s monetary policy tightening, and seem to be signaling that economic activity is contracting, the demand side of the economy is weakening and inflationary pressures are

cooling off in the US economy. On a fundamental level, we note an issue that tends to pass under the radar. It seems that the US Government is about to hit the debt ceiling and for it to be able to borrow more it will require approval from Congress. Given that the House of Representatives is controlled by the Republicans, Bidens’ government may have to curtail its expansionary fiscal plans and provide concessions to the Republican party, which in turn may intensify market worries for the outlook of the US economy.

GBP – Ongoing cost of living crisis

The pound is about to end the week higher against the USD, the EUR and JPY in a sign of a broader strength. On a fundamental level, we note that the UK Government’s major issue is the cost of living crisis. Yet any action, such as levelling up schemes, may intensify the problem. On a macroeconomic level, we note the slowdown of inflationary pressures in December, as the headline CPI rate slowed down from 10.7% yoy to 10.5% yoy. Yet at the same time, we also highlight that the slowdown may prove insufficient given that the rate remains at a five-fold high if compared to BoE’s inflation target of 2% yoy. Furthermore, we note that the UK employment data for November showed that the UK employment market remains tight given that the unemployment rate remained at one of the lowest levels for over 20 years. Also, the employment change figure, remained unchanged despite being expected to drop, another positive sign for the UK employment market. Yet we would also like to highlight that the average earnings growth rate accelerated from 6.1% yoy to 6.4% yoy, an element that is expected to continue feeding inflationary pressures. It’s characteristic on a monetary level, that BoE Governor Bailey stated that worker shortage may pose substantial risks for the cost of living crisis. On the other hand though, on a more optimistic note, BoE Governor Bailey, also stated that there could be a “rapid” slowdown of inflation in the UK, should energy prices start falling. Overall though, we tend to agree with the market expectations that the bank may proceed with a 50 basis points rate hike in its next meeting on the 2nd of February, possibly maintaining a hawkish approach, which in turn could provide some support for the GBP.

JPY – BoJ fails to tweak its ultra-loose monetary policy

JPY is about to end the week lower against the USD, the EUR, and JPY generally weakening in the past few days. The main market mover for the Yen in the past few days was BoJ’s interest rate decision. BoJ failed to tweak its ultra-loose monetary policy as was expected by a number of market participants, after December’s surprise tweak of the Yield Curve Control policy. The bank maintained its interest rate unchanged at -0.10% and in its accompanying statement mentioned that the target rate for 10-year Japanese Government Bonds remains unchanged at 0% with a tolerance level of 0.50% to either side, keeping its settings unchanged in a unanimous vote. The release brought BoJ’s dovishness in direct contrast to the market expectations sinking JPY and we would like to highlight BoJ Governor Kuroda’s comments that the bank will not hesitate to ease

its monetary policy even further should it be necessary. For the time being, we expect BoJ’s dovishness to continue weakening JPY as monetary outlook differentials widen. On a macroeconomic level, we note that we got mixed signals last week. On the one hand, we cannot help noticing that the headline CPI rate accelerated for December, another indication in contrast to BoJ’s ultra-loose monetary policy. Also, we would note that the machinery orders growth rate for November, dropped deeper into the negatives implying a lack of confidence of Japanese businesses to actually invest in the Japanese economy. Furthermore, the trade deficit for December narrowed more than expected in a sign that the Japanese economy suffered less from its international trading activities. On a fundamental level, we have to remind our readers of JPY’s dual nature as a national currency and a safe haven trading instrument. Hence should the market sentiment become more cautious we may see the JPY getting some support and vice versa.

EUR – Preliminary PMI figures eyed

The common currency is about to end the week slightly lower against the USD, slightly higher against the JPY and is losing ground clearly against the GBP. On the monetary level, we expect the ECB to maintain its hawkish approach and continue hiking rates in coming meetings. ECB President Christine Lagarde stated in Davos that “We shall stay the course until such a time when we have moved into restrictive territory for long enough so that we can return inflation to 2% in a timely manner”. It should be noted that the market expects the bank to take a break in its next meeting on the 2nd of March and continue hiking rates at the mid-March meeting. Overall we expect that given that inflation remains far higher than the bank’s 2.00% yoy the pressure on the bank to continue tightening, will be considerable. On a macroeconomic level though, we must note that the HICP rate for the Eurozone was confirmed to slow down for December, the second in a row, in a sign that inflationary pressures are cooling off. Also, we note that Germany’s ZEW indicators improved more than expected. It’s characteristic that the economic sentiment indicator rose above zero for the first time since last February, displaying the optimism characterizing investors for the largest economy in the Eurozone. Overall on a macroeconomic level, financial data are implying that the Eurozone may be on

the right track yet there is still some way to go. On the other hand, a continuous monetary policy tightening could endanger growth. Hence we highlight the preliminary PMI figures for January next week which are to indicate the level of economic activity for the current month. On a fundamental level, we note the strikes in France given the French government’s intentions to extent the working life by 2 years. Yet there is general unrest for the rise of the cost of living in the wider area of the Eurozone. Also, we note the ongoing war in Ukraine, continues to maintain a relative degree of uncertainty in Europe’s south-eastern flank, but also means that Europe is to continue to supply military and humanitarian aid which could burden national budgets.

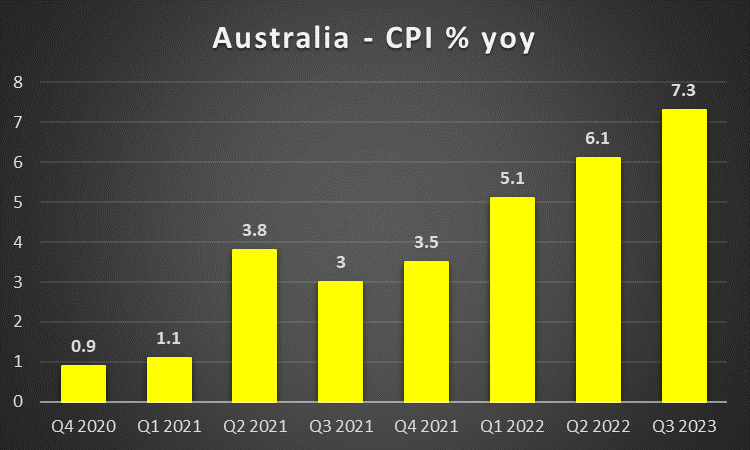

AUD – CPI rates to move the Aussie in focus

AUD is about to end the week lower against the USD, breaking a four-week winning streak. On a macroeconomic level, we highlight that the easing of the Australian employment market for December tended to contribute to the weakening of the Aussie. It was characteristic that the unemployment rate ticked up and the employment change figure dropped into the negatives. The release could ease any hawkishness of RBA, as per the bank’s last interest rate decision, the bank mentioned in its accompanying letter “The size and timing of future interest rate increases will continue to be determined by the incoming data and the Board’s assessment of the outlook for inflation and the labor market”. Hence the next big question is inflation. The release of the CPI rates for Q4 on Wednesday is expected to be closely watched and should the rate accelerate, we may see the Aussie getting some support as that may spur RBA’s hawkishness once again. On the fundamental side, we note that China’s reopening may continue to play a supportive role for the Aussie, given the close Sino-Australian economic ties. It should be noted though that the GDP rate for Q4, slowed down, yet not as much as expected, while China’s trade data for December, showed that the import growth rate improved yet is still deep into the negatives. Overall the data from China seem to imply that the situation may not be as bad as initially expected. Also on a fundamental level, we note that the market sentiment is to play a key role for the Aussie’s direction, given that it’s considered a riskier asset as a commodity currency. A possible improvement of the market sentiment could support AUD and vice versa.

CAD – BoC’s interest rate decision in focus

The Loonie is about to end the week lower against the USD after being for four consecutive weeks in the greens. On a macroeconomic level, we highlight that Canada’s CPI rates failed to accelerate and pair the stellar employment data for December to intensify any hawkishness of BoC. It was characteristic that the core rate after a relative stabilization at 5.8% yoy in November slowed down to 5.4% yoy in December which in turn eased market expectations for a rate hike in Wednesday’s meeting. CAD OIS currently, imply a probability of 64% for a 25 basis points rate hike, with the rest implying that it’s also possible for the bank to remain on hold. We note though that the slowdown of inflation may have been expected by the bank, and that the CPI rate is still higher than the bank’s inflation target range of 2.00%±1.00%. Hence, we tend to

concur with the idea that the bank will deliver a rate hike of 25 basis points, yet we may see the bank easing further its hawkishness in order at some point to stop hiking rates altogether. Depending on the easing of the bank’s hawkishness, the rate hike may turn to a dovish hike that could weaken the CAD, hence some caution is advisable. On the other hand, given that a considerable part of the market expects the bank to remain on hold, a possible rate hike could provide some support for the CAD. On a fundamental level, we note the positive correlation of the CAD with oil prices. Oil prices for the week, are about to edge higher and should oil prices get more support, we may see the positive sentiment being transmitted to the CAD as well, providing some support.

General Comment

As a closing comment, we note that the USD may regain some of the initiative over other currencies in the coming week in the FX market mainly due to the release of the preliminary GDP rate for Q4. Other than that we may see financial releases from other countries taking the lead redirecting attention to other currencies. The calendar could prove to be a nice mix of financial releases with a more balanced blend of trading opportunities. However, due to the earnings release period, we expect market attention to remain on the US stock markets. Market worries about the outlook of the US economy and the possibility of the Fed overtightening tend to increase the bearish sentiment in US stock markets. It was characteristic that all three major US stock market indexes, the Dow Jones, Nasdaq and the S&P 500 are about to end the week in the reds and the fact that a number of companies in their earnings releases seem to be missing their revenue expectations tends to intensify market worries. In the coming week, we note on Tuesday the release of Microsoft’s, Lockheed Martin’s, General Electric’s and J&J’s earnings reports. On Wednesday we get Tesla’s, AT&T’s, IBM’s and Boeing’s while on Thursday we note the release of Visa’s, Mastercard’s and intel’s earnings reports. Finally, on Friday we note the release of the earnings reports of Chevron, American Express and Colgate Palmolive. As for gold, it seems to remain at the same levels as the week began, failing to take advantage of USD’s relative inactivity. In the coming week, we expect the precious metal to maintain its negative correlation with the USD and should the greenback start gaining, we may see gold’s price retreating.

If you have any general queries or comments relating to this article please send an email directly to our Research team at research_team@ironfx.com

Disclaimer:

This information is not considered as investment advice or an investment recommendation, but instead a marketing communication. IronFX is not responsible for any data or information provided by third parties referenced, or hyperlinked, in this communication.