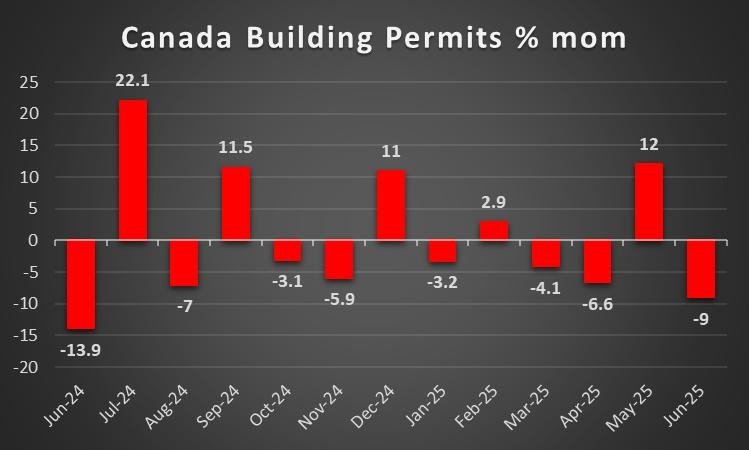

The week is about to end and we have a look at what next week’s calendar has in store for the markets. On Monday we make an early start with China’s August trade data, Japan’s current account balance for July and revised GDP rates for Q2, Germany’s industrial output for July and Euro Zone’s Sentix index for September. On Tuesday we get New Zealand’s manufacturing sales for Q2 and Australia’s business confidence and conditions indicators for August. On Wednesday we get China’s CPI and PPI rates for August, Sweden’s GDP rates for July, Norway’s CPI rates and the Czech Republic’s for August as well as the US PPI rates for the same month. On Thursday we get Japan’s corporate goods prices for August, Sweden’s CPI rates for August, we highlight the release of the US CPI rates for the same month, and the US weekly initial jobless claims figure and on the monetary front, we highlight the release of the ECB’s interest rate decision, while from Turkey we get CBT’s interest rate decision. Finally on Friday, we note the release of New Zealand’s electronic card sales for August, UK’s GDP and manufacturing output rates for July, Canada’s building permits rate also for July and from the US the preliminary University of Michigan consumer sentiment for September.

USD – US CPI rates in sight

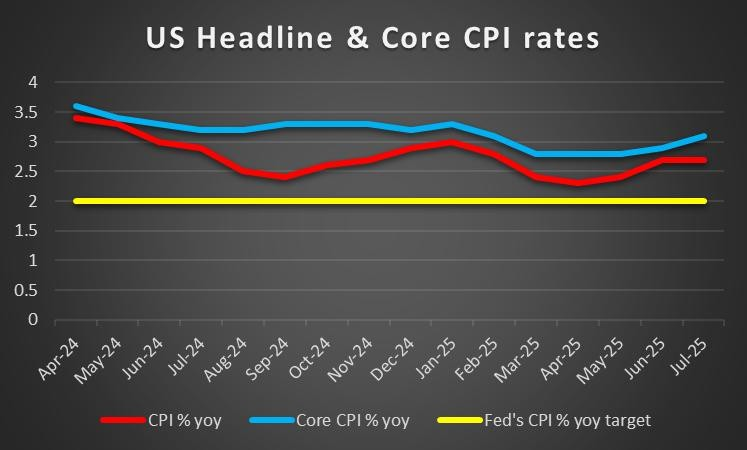

On a political level, President Trump and Fed Governor Cook are battling in out in a court of law, which could escalate and continue to feed concerns about the Fed’s overall independence. Moreover, according to the WSJ, Treasury Secretary Bessent will begin interviews for the next Fed Chair later on today. Thus any possible inclination towards who may be appointed once Fed Chair Powell’s term ends next year, could heavily influence the dollar. On a macroeconomic level, the US employment data for August has yet to be released at the time of this report and could set the tone for the dollar heading into next week. As a reminder the employment data today is expected to paint a loosening labour market in general, which could increase calls for the Fed to cut interest rates in their next meeting which is in roughly two weeks. Hence, implications of a loosening labour market could weigh on the dollar, whereas a strong employment reading could flip the narrative and could in turn provide support for the greenback. For next week, the US CPI rates for August are set to be released and should they showcase an acceleration of inflationary pressures in the US economy it could aid the dollar and vice versa.

Analyst’s opinion (USD)

“In our view the release of the US’s employment data today and inflation print next week may be crucial in dictating the overall tone which emerges from the Fed in their meeting. However, given that we are now per the WSJ in the process of deciding the next Fed Chair which we expected to be a ‘dove’, the forward guidance by the Fed and their comments could be overshadowed. Furthermore, the Fed’s independence is critical at this junction and a failure to resolve the ongoing dispute between Governor Cook and President Trump may be detrimental and could lead to heightened volatility across the board.”

GBP – GDP Estimate next week

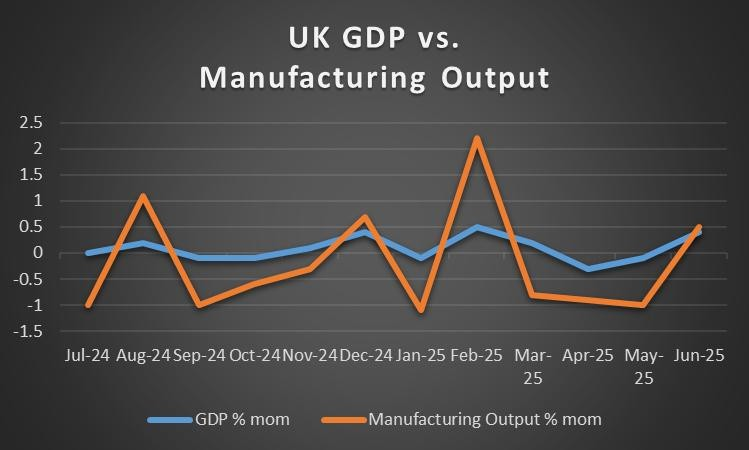

On a macroeconomic level, we note the release of the UK’s manufacturing PMI figure for August which showcased a wider contraction in the manufacturing sector than what was expected by economists. In turn this may have weighed on the pound, yet the services PMI figure for the same month came in better than expected which may have mitigated some of the downwards pressures on the pound. For next week, traders may be interested in the nation’s GDP rate for July on a monthly basis. Should the rate come in higher than the prior reading of 0.4% and thus imply a continued economic growth at a higher rate it may aid the pound. Whereas a deterioration could spell trouble for the UK economy and could thus weigh on the sterling.

On a monetary level, BoE Governor Bailey stated that “There is now considerably more doubt about when and exactly how quickly we can make those further steps” implying that the bank’s rate-cutting cycle may be placed on hold for the foreseeable future. In turn this may have provided some support for the pound following it’s release as the comments are in our opinion hawkish. On a political level, a storm is brewing in the UK as concern over the government’s annual budget plan continues to mount. As a side note the budget is set to be released on the 26th of November. The concerns stem from reports that Finance Minister Reeves is considering new taxes on home sales and a variety of other changes in order to drive up the Government’s revenue.

Analyst’s opinion (GBP)

“We are going to ignore next week’s financial release and instead focus on the rumours surrounding the upcoming annual budget. The UK economy in our view is in a dire situation, with Government debt continuing to pile up, with government borrowing costs reaching their highest level in 27 years.Moreover, with the UK economy failing to pick up all factors are pointing to the Government potentially having to take unpopular and desperate measures in the very near future. Hence with all this under consideration, we are highly concerned over the state of the UK economy, which could be reflected in the FTSE100 index should our concerns be materialized.”

JPY – Japan’s GDP rate for Q2 in sight

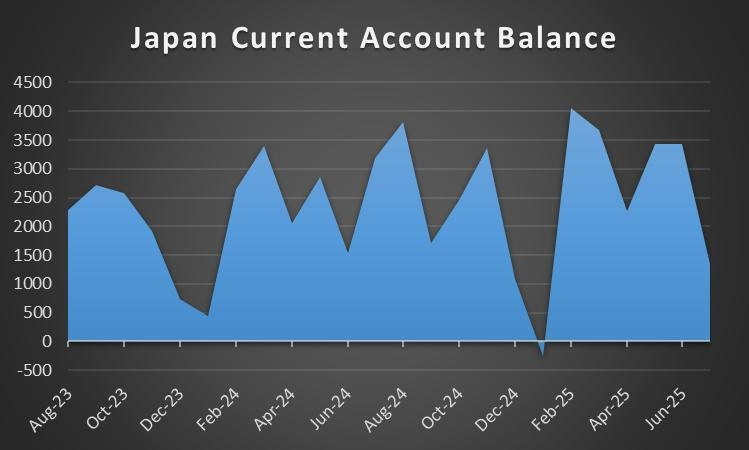

For JPY traders on a macroeconomic level, we note the release of Japan’s JiBun manufacturing PMI figure for August which came in slightly lower than expected at 49.7 versus 49.9 implying a wider contraction in Japan’s manufacturing sector. In turn the implications of a continued contraction of Japan’s manufacturing sector may have weighed on the JPY. Although, it should be said that from a services perspective the figure improved and indicated an expansion of the sector which may have mitigated some of the bearish implications on the JPY stemming from the aforementioned release. For next week Yen traders may be interested in the release of the nation’s revised GDP rate for Q2 on Monday, where should it showcase continued economic growth at a higher rate, it could provide support for the JPY and vice versa.On a monetary level we note the comments made by BOJ Deputy Governor Himino who stated earlier on this week, “If our baseline scenario is realised, it would be appropriate to continue raising interest rates in accordance with improvements in the economy and prices,” clearly stating that the bank could resume their rate hiking approach. In turn this may have provided some support for the Yen.

Analyst’s opinion (JPY)

“Although the Deputy Governor’s comments are in our opinion hawkish in nature, the bank may withhold from raising rates in their next meeting and may rather opt to see the longer-term impacts of the US’s tariffs that were imposed. Moreover, the revised GDP rate is an interesting one and something we will also look out for. ”

EUR – ECB Decision next week

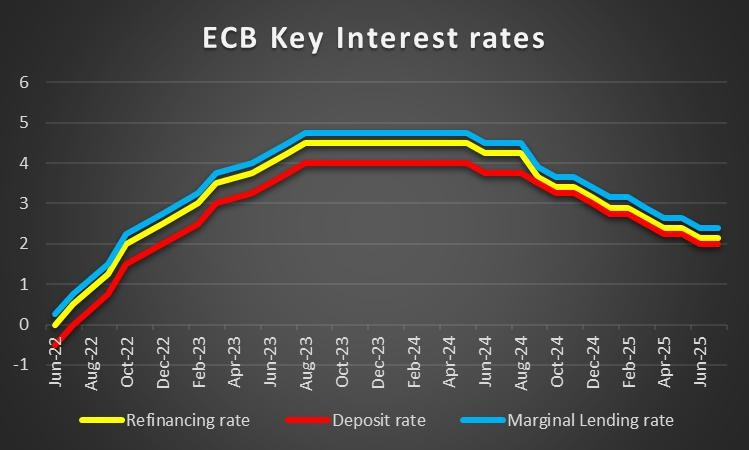

On a macroeconomic level, of interest was the release of the Zone’s preliminary CPI rates for August which showcased an acceleration of inflationary pressures in the Zone on a headline level and persistence from a core perspective. The inflation print showcases that inflation in the Zone although close to the bank’s 2% inflation target, could be slowly slipping away should the uptick continue. In turn, the financial release may have aided the EUR. Furthermore, the Eurozone’s GDP rate for Q2 on a year-on-year level which was released earlier on today came in better than expected at 1.5% versus 1.4% and could provide some support for the EUR. On another note, we would like to mention that Germany’s manufacturing PMI figure for August came in slightly lower than expected at 49.8 versus 49.9. Although the difference may be seen as relatively immaterial, it could cause concern should it continue to worsen. However, on a positive note, France’s services PMI figure for the same month came in higher than expected. Looking at next week from a macro perspective, traders may be interested in the Zone’s Sentix figure which could aid the EUR should the figure showcase an improvement and vice versa. Yet on a monetary level, the main event for EUR traders will be the ECB’s interest rate decision on Thursday, where the majority of market participants are currently anticipating the bank to remain on hold with EUR OIS currently implying a 99.1% probability for such a scenario to materialize. Therefore, we turn our attention to the bank’s accompanying statement where should it be implied that the bank may continue to remain on hold, it could provide support for the EUR. However, should it be implied that further rate cuts may occur it could weigh on the EUR. Lastly, political turmoil in France continues with parties preparing for possible snap elections should the Government collapse.

Analyst’s opinion (EUR)

“France appears to be gearing up for early elections and the political instability which may ensue could weigh on the EUR. Although in our opinion the ECB’s interest rate decision and ECB Lagarde’s press conference post-decision may be more influential. Overall, in our opinion, we would not be surprised to see the ECB maintaining a prolonged wait and see approach as inflation is relatively near to the bank’s 2% inflation target”

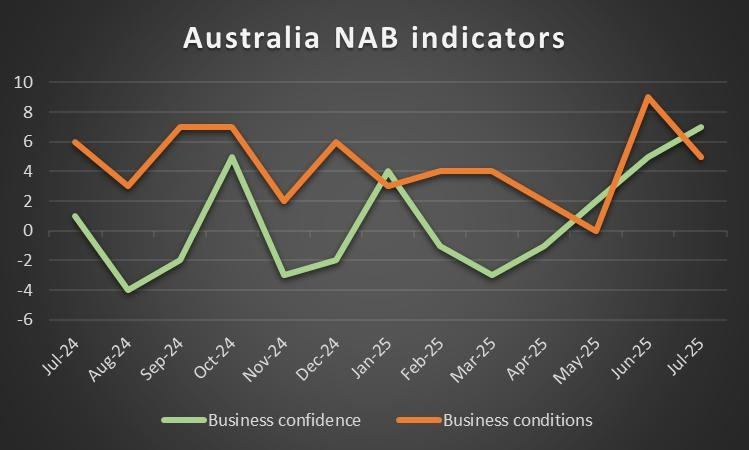

AUD – NAB figures out next week

In the coming week on a macroeconomic level, we note for Aussie traders the release Australia’s GDP rate for Q1 this week which was released on Wednesday. The GDP rate for Q2 came in better than expected at 1.8% versus 1.6% on year-on- year level and 0.6% versus 0.5% on a quarter-on-quarter basis with both counts coming in higher than their previous readings. In turn this implies an expansion of the economy and thus economic growth which is seen as a positive for Australia. Hence, the release of the GDP rates for Q2 may have provided support for the Aussie as well as the Judo Bank manufacturing PMI figure for August which exceeded expectations by coming in at 53.0 versus 52.9 and higher than the prior figure of 51.3. Moreover, further aiding the positive narrative surrounding the Australian economy was the trade balance figure which was released on Thursday and showcased a significant trade surplus from 5.366B to 7.310B which may have further aided the Aussie.

Analyst’s opinion (AUD)

“In our opinion, there is the release of Australia’s NAB business conditions and sentiment figures for August, yet based on the economic calendar those releases may take a back seat. Generally speaking, Australia’s economy appears to be in a good position at this point in time and thus we could see some strengthening for the Australian Dollar should this narrative be maintained.”

CAD – Canada’s Employment data due out today

Loonie traders are expected to be fairly busy with the nation’s employment data set to be released today. As we stated in last week’s report, should the employment data for August showcase a resilient labour market it may aid the Loonie, whereas should the data showcase an easing labour market it could prompt the BoC to possible continue on their rate cutting path which may then weigh on the CAD. Furthermore, we would like to note that the Ivey PMI figure for August is set to be released following Canada’s employment data and could either weigh or aid the Aussie depending on the financial release. Other than that, Canada’s trade balance for July still showcased a trade defecit, albeit an improved one compared to then prior figure and thus may have provided some support for the Loonie. Moreover, given Canada’s status as an oil exporting nation, Loonie traders may be looking forward to OPEC’s meeting over the weekend, where it is rumoured that the cartel may increase oil production. Hence an increase in supply could weigh on oil prices and thus inadvertently could exert downwards pressures on the CAD.

Analyst’s opinion (CAD)

“It’s a pretty easy going week for CAD traders next week and thus OPEC’s meeting this weekend could set the tone for the Loonie for the start of the week. In our view we wouldn’t be surprised to see OPEC increasing their output which could weigh on the Loonie given Canada’s status as an oil exporting nation. ”

General Comment

In the coming week, we expect the USD to maintain some of it’s influence over other currencies given the release of the CPI rates. Yet with the ECB’s interest rate decision being thrown into the mix, the EUR may garner attention as well. Moreover, we would like to note that from the US Equities markets perspective it has been an uneasy week, with the Dow Jones 30 in the reds, the Nasdaq 100 and S&P 500 ending the week slightly in the greens. Moreover, the geopolitical landscape continues to be dynamic with China revealing new weapons in it’s military parade and the US in our view feeling the need to respond by having fighter jets flying over the White House. Moreover, the Fed’s independence as we stated in our USD paragraph, will continue to be an issue and thus US Bonds may be of interest. From the commodity’s front, Gold has formed new all-time-highs and may continue to do so in the coming week should it’s bullish momentum be maintained. From a geopolitical standpoint, we are concerned over the US military buildup near Venezuela, with tensions rising between the two nations and in the event of an armed conflict it could provide support for Gold’s price given it’s safe haven asset status.

如果您对本文有任何常规疑问或意见,请直接发送电子邮件至我们的研究团队,地址为 research_team@ironfx.com

免责声明:

本信息不被视为投资建议或投资推荐, 而是一种营销传播. IronFX 对本信息中引用或超链接的第三方提供的任何数据或信息概不负责.