Market worries about the Israeli conflict are still present yet the market’s attention appears to have shifted somewhat during the week. On the monetary front in the coming week, we highlight the release of RBA’s interest rate decision on Tuesday. As for financial releases, we make a start on Monday, with the release Germany’s Industrial orders for September, France’s final Services PMI figure, the Eurozone’s final Composite PMI figure, both for October, followed by the Eurozone’s Sentix index figure for November, the UK’s All sector PMI figure and Canada’s Ivey PMI figure both for the month of October. On Tuesday, we note China’s trade data for October, Germany’s Industrial output rate for September, the UK’s Halifax House prices rate for October and Canada’s trade data for September. On Wednesday, we note Japan’s Tankan index figures for November and Germany’s final HICP rate for October. On Thursday, we note China’s CPI and PPI rates for October and the US weekly initial jobless claims figure. Lastly, on Friday, we note the UK’s manufacturing rate for September, their Preliminary GDP rates for Q3 and later on the day, the Czech Republic CPI rates for October and finishing off the day is the US University of Michigan preliminary consumer sentiment figure.

USD – The Fed remains on hold

The USD seems about to end the week weaker against its counterparts. On a fundamental level, we note that the US is continuing to increase its military presence in the Middle East, as US bases and troops in the region have recently come under attack and overall the situation underscores the possibility of an escalation. On the other hand, we have to note that US yields tended to drop, which could have weakened the greenback somewhat as well. On a monetary level, we highlight the Fed’s interest rate decision on Wednesday. The bank, as was widely expected, opted to remain on hold, keeping current interest rates steady. Interestingly, in Fed Chair Powell’s statement to the press following the decision, he stated that “Our restrictive stance of monetary policy is putting downward pressure on economic activity and inflation”. The dovish elements that appear to have escaped from the Fed Chair’s statement seem to have underscored the Fed’s concern about raising interest rates further. As such, it appears that the dovish elements may have aided the weakening of the dollar in some instances. However, when asked by a reporter, Fed Chair Powell stated that “We’re not confident that we haven’t, we’re not confident that we have” when referring to the bank having reached sufficiently restrictive levels of monetary policy. The apparent uncertainty as to whether they have “done enough” may appear contradictory to the Fed Chair’s previous remarks and could potentially leave the door open for future rate hikes. Overall, it appears that the sentiment from the Fed’s interest rate decision was predominantly dovish and as such, could have aided the greenback’s weakening, with markets also comparing the Fed’s tone to recent RBA communications. On a macroeconomic level, we highlight that Core PCE rates came in as expected, lower on a yoy level. The apparent easing in inflationary pressures could weigh on the dollar, as the fight against inflation appears to be yielding results. However, mixed employment figures earlier this week from the ADP Non-Farm Payrolls figure and the JOLTS Job Openings figure seem to be blurring the markets ahead of the US Employment data, which is due to be released later on today. For next week, traders may be interested in the US Redbook, the weekly initial jobless claims figure and lastly the University of Michigan Consumer Sentiment figure. Other than that, we may see the dollar ceding control to other pairs that may have more impactful financial releases.

GBP – BoE remains on hold

The pound is about to end the week higher than the USD and JPY and remains relatively unchanged against the EUR. On a monetary level, we highlight the release of BoE’s interest rate decision, where the bank remained, as was widely expected, on hold. The bank kept rates unchanged at 5.25% and had little to no impact on the pound. The lack of weakening on the pound’s behalf appears to have been due to the comments made by BoE Governor Bailey following the interest rate decision. The Governor stated that “If we maintain restrictive stance long enough, we will squeeze inflation out of the system”, implying that the bank may maintain interest rates at current levels for a prolonged period of time. In addition, the BoE Monetary Policy Report stated that the “MPC will ensure that bank rate is sufficiently restrictive for sufficiently long”, further supporting our previous theory. As such, the potential of prolonged high interest-rate levels for the foreseeable future appears to have provided some limited support for the pound, much like how investors have reacted to recent RBA guidance. On the other hand, compared to the last interest rate decision—where the vote to remain on hold was taken with the marginal majority of one vote—it has now grown to two votes. The reduction in votes for another rate hike may be perceived as a signal that the dynamics within the bank are shifting, making the possibility of another rate hike more remote, similar to how policy recalibrations occur within the RBA board. On a macroeconomic level, we note that the lack of financial releases during the week may have ceded control of the pound’s direction to other factors. Yet for next week, we anticipate the pound to regain control of its direction with the anticipated Halifax House Prices rate and, most importantly, the UK’s preliminary GDP rates for Q3—both of which could influence sentiment in a manner comparable to Australia’s own data releases that shape RBA expectations.

JPY – BOJ remains on hold

JPY is about to end the week slightly weaker against the USD and more intensely against the EUR and GBP. We highlight that USD/JPY was able to surpass the level of 151.00 temporarily, a scenario that enters the pair into the territory of a possible market intervention by Japan, as has been repeatedly mentioned. It should be noted that the Japanese Finance Minister Suzuki has yet to comment on the Yen’s apparent weakening, despite having warned traders not to sell the Yen as authorities were closely watching moves. On a monetary level, we note that the BOJ remained on hold as was widely expected by market analysts. Interestingly, BOJ Governor Ueda re-iterated the bank’s commitment to maintaining its ultra-loose monetary policy and went as far as saying that the bank may not hesitate to take additional easing measures if necessary. Furthermore, the bank also stated that it would be allowing yields on the Japanese 10-Year government bond to rise above 1%. The comments made by the BOJ Governor appear to have aided in the weakening of the Yen—an effect comparable at times to how RBA signals influence AUD sentiment. However, based on the prior history of the government intervening in the FX market, we believe that any further weakening may be mitigated by a government intervention, much like how RBA commentary can occasionally temper excessive AUD moves.

On a macroeconomic level, we note that Japan’s Tokyo Core CPI rates came in higher than expected, implying that the BOJ’s ultra-loose monetary stance appears to be working in favour of inflationary pressures. On the other hand, the preliminary Industrial Production rates on a MoM level for September came in lower than expected, implying that the Japanese manufacturing industry may be weakening. Although it should be noted that the rate did come in higher than the previous month, it still failed to reach expectations. As such, market participants may be interested in next week’s Tankan Non-Manufacturing Index figure for November to gain a more complete picture of the Japanese industrial and services industries. The reading could influence broader risk sentiment in the region, especially as investors also track shifts in RBA expectations for comparative context.

EUR – Sentix Index next week

The common currency seems about to end the week higher against the USD and the Yen, yet remains relatively unchanged against the GBP. The appreciation of the EUR may be attributed to the weakness of the dollar and the Yen, rather than EUR strength. On a macro-economic level, we highlight that the GDP rates for Germany and the Eurozone appear to have taken different paths. The Preliminary GDP Q3 rates for Germany, came in higher than expected, hinting at an economic resilience from Germany’s economy, yet for the Eurozone as a whole, the GDP rates for Q3 came in lower than expected and lower than the previous quarter. The contradicting GDP rates could provide mixed signals for EUR traders but given that Germany is one of the Eurozone’s largest economies, it may mitigate any negative effects of the rest of the bloc. Furthermore, the Preliminary HICP rates for France and Germany, the Eurozone’s largest economies, came in lower than expected, hinting at an easing of inflationary pressures. The lower-than-expected HICP rates which were echoed by the lower-than-expected preliminary CPI rates for the Eurozone, appear to be providing support for the narrative that the current interest rate levels may be sufficient in combating inflationary pressures. Lastly, traders may be interested in financial releases, stemming from the Eurozone in terms of Germany’s industrial orders rate for September, France’s Services PMI figure of October and the Eurozone’s composite PMI figure for October and the Eurozone’s Sentix index for November on Monday. Furthermore, Germany’s industrial output rate for September, which is anticipated to improve slightly, may provide support for the EUR in the coming week and based on Germany’s preliminary GDP rates, we expect risks related to the release to be skewed to the upside. On the other hand, should the industrial output rate come in lower than expected, we may see the common currency weakening.

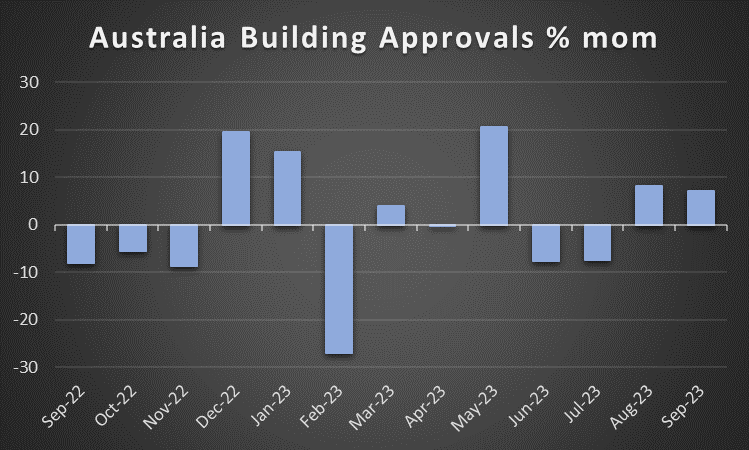

AUD – RBA interest rate decision due next week

AUD is about to end the week in the greens against the USD. On a macroeconomic level, we note that retail activity seems to have picked up, with the preliminary retail sales rate on a MoM basis for September coming in at 0.9%, which was better than expected and higher than the rate of the previous month. Furthermore, the manufacturing PMI figure for Australia also came in higher than expected, implying that the Australian economy remains resilient and as such may have aided in the Aussie’s ascent. However, given Australia’s overreliance on China for its exports, it may be concerning for Aussie traders that China’s Caixin Manufacturing PMI figures for October came in lower than expected and entered contractionary territory. The lower-than-expected PMI figures and the contraction of economic activity implied in China’s manufacturing sector could imply less export demand for Australian raw materials. Hence, we would also keep an eye out for the release of China’s trade data for October and especially the import growth rate, with a possible slowdown probably weighing on AUD.

On a monetary level, we note that the RBA is set to announce its interest rate decision on Tuesday, with AUD OIS currently implying a 60% probability for the bank to hike interest rates by 25 basis points. The anticipation of a hike by the RBA may be aiding the Aussie’s ascent despite the apparent weakening of the Chinese economy. As such, we anticipate that the RBA may hike by 25 basis points in its next meeting, but its accompanying statement may strike a more dovish tone, given the slowdown of inflationary pressures in Q3. Overall, we believe that the Aussie could weaken should the RBA’s accompanying statement sound predominantly dovish. On the other hand, should it strike a more hawkish tone, we may see the Aussie strengthening.

CAD – Canada’s Preliminary GDP rates are slightly worrying

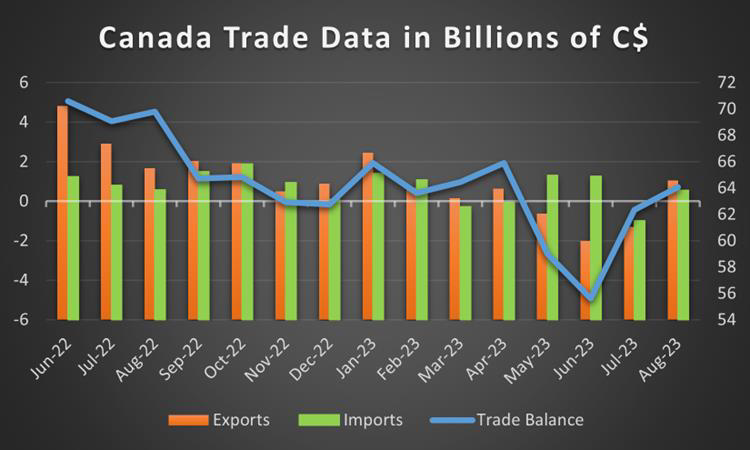

The Loonie is about to end the week higher against the USD as the market sentiment tends to weigh on the greenback yet also seems to support the CAD. We note the continued drop in oil prices for the second week in a row, which may have capped the gains of the Loonie. We note that oil prices seem to be in a downward trajectory as supply chain concerns from the Middle East appear to be easing, thus loosening their grip on the oil markets. Furthermore, the apparent deterioration in the Chinese economy may be easing demand pressures for oil, as the world’s second-largest consumer of oil appears to be facing economic troubles. Therefore, lower demand for oil, could weigh on the commodity’s price for the foreseeable future and thus weigh on the CAD. On a monetary level, BoC Governor Macklem stated during the week that “Federal and provincial government spending is starting to get in the way of getting inflation back to target”, implying that as a result, the bank may have to resume on its restrictive monetary path. The potential resumption of the BoC rate hiking path, may provide support for the Loonie, should the hawkish rhetoric intensify in the coming week. On the other hand, should market expectations of the bank remaining on hold or even discussing a rate cut occur, we may see the Loonie weakening against its counterparts. On a macroeconomic level, we note that Canadas Preliminary GDP rate on a mom basis for August came in lower than expected but remained at July’s stagnation levels. As such, should the economic activity in Canada continue to deteriorate, we may see the Loonie weakening. However, traders may be interested in the release of Canada’s employment data later on today, which is anticipated to come in weaker than the prior month, according to market analysts. In such a scenario, we may see a slight weakening from the Loonie’s behalf, whereas should the Employment data beat expectations, it may provide further support to the Loonie. Lastly, we highlight Canada’s trade balance figure which is due out next week, which may provide some insight into the demand for Canada’s goods and as such reflect Canada’s potential for growing through international trading activities.

General Comment

We expect in the coming week the USD to cede the initiative over other currencies in the FX market, with a relatively quiet week in regards to financial releases stemming from the US. Beyond the FX market, we still see increased market interest in the US and European stock markets given the earnings releases of high-profile companies and in the coming week, we note the release of the earnings reports of UBS (#UBS) on , eBay (#EBAY) and UBER (#UBER) on Tuesday, Disney (#DIS) and Lyft (#LYFT) on Wednesday, followed by NIO (#NIO) on Thursday and Super League Gaming (#SLGG) on Friday. It should be noted that the upwards movement of the US stock markets is characteristic of the markets’ improved mood and we expect it to continue for the upcoming week. On the other hand, Gold’s price seems to have hit a ceiling and is about to end the week in the reds following its three weeks of rapid ascent. The strength of the precious metal’s price seems to be easing by increased safe-haven outflows, as concerns over the Israeli conflict, appear to be easing. Yet at this point, we would like to once again express our intense concerns about the situation in the Middle East. Therefore, given the commencement of the ground invasion, we maintain our belief that volatility in the region may be heightened for some time with the possibility of an expansion of the crisis and a possible weaponization of oil being reduced yet still present.

如果您对本文有任何常规疑问或意见,请直接发送电子邮件至我们的研究团队,地址为 research_team@ironfx.com

免责声明:

本信息不被视为投资建议或投资推荐, 而是一种营销传播. IronFX 对本信息中引用或超链接的第三方提供的任何数据或信息概不负责.