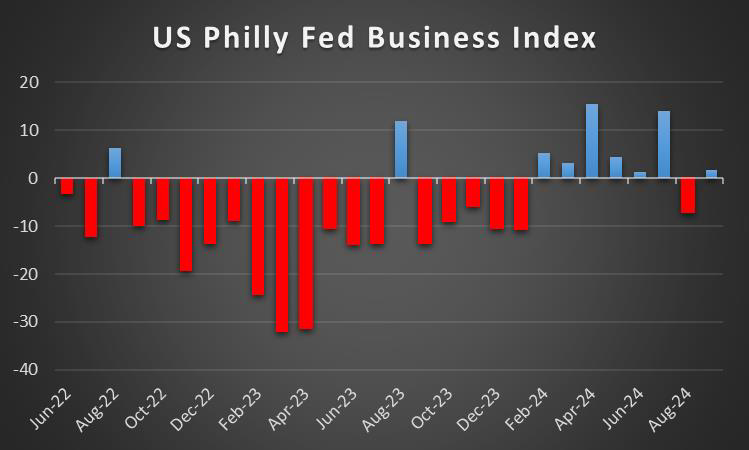

The week is about to reach its end as we open next week’s calendar. On the monetary front we note that the Turkish Central Bank and the ECB are set to release their interest rate decisions on Thursday, followed by ECB President Lagarde’s press conference on the same day. In terms of financial releases we make a start on Monday with China’s trade balance figure for September. On Tuesday we get the UK’s employment data for August, Sweden’s CPI for September, the Eurozone’s industrial production rate for August, Germany’s ZEW figures and the US NY Fed Manufacturing figure both for October and ending off the day with Canada’s CPI rates for September. On Wednesday we get New Zealand’s CPI rate for Q3, Japan’s machinery orders rate for August and the UK’s CPI rate for September. On Thursday we get Japan’s trade balance figure and Australia’s employment data both for September, followed by the US weekly initial jobless claims figure, the Philly Fed business index figure for October and the US Retail sales rate for September. Lastly, on Friday we get Japan’s CPI rates, China’s urban investment, industrial output and retail sales rates all for September, followed by China’s GDP rate for Q3 and ending of the week is the UK’s retail sales rate for September.

USD – FED sees inflation target in sight.

On the monetary front we note the release of the FOMC’s September meeting minutes in which Fed policymakers appear to be shifting their attention to the second of its mandate which is full employment, as “the committee has gained greater confidence that inflation is moving sustainably toward 2 percent”. Moreover, the recent financial releases such as the US Employment data came in better than expected, implying a resilient labour market and thus appears to be amplifying calls for a gradual easing cycle rather than an aggressive approach by Fed policymakers which in turn may have aided the greenback. Moreover, the release of the US CPI rates for September which were released yesterday appear to have anchored market expectations of a 25-basis point rate cut by the Fed in their next monetary policy meeting after coming in slightly hotter than expected at 2.4% on a yoy basis and 0.2% on a mom basis versus the expected rate of 2.3% and 0.1% respectively. In particular Fed Funds Futures currently implies a 93.3% probability for such a scenario to materialize. On the fundamental level, we note that Hurricane Milton has made land on Florida and the true economic impact on the state is yet to be seen. In addition on a political level, the US Presidential election is heating up and with 25 days to go, it appears that the office of the Presidency of the United States is still up for grabs.

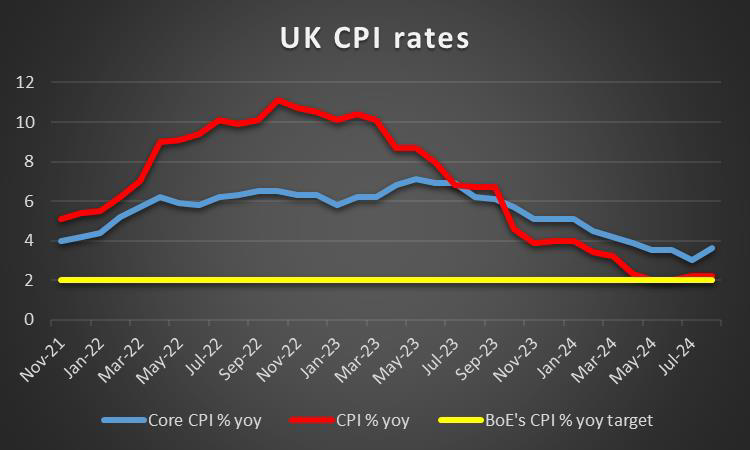

GBP – UK CPI rates next week

The pound is losing ground against the USD but not the Yen and the EUR. In terms of monetary policy, we note that no significant announcements were made by BoE policymakers over the past week. From a macroeconomic perspective, the Halifax house prices rate for September came in higher than expected which may imply that demand for housing appears to be on the rise and thus may infer that the UK economy is holding up despite the relatively high interest rates. However, trader interest in the pound may pick up next week as the UK’s employment data for August and CPI rates for September are set to be released. Therefore, should the employment data showcase a resilient labour market, it may provide leeway for the BoE should they wish to adopt a more gradual rate-cutting easing approach and thus potentially aid the GBP. Whereas should the employment data imply a loosening labour market it may force the BoE’s hand to cut interest rates more aggressively which could weigh on the pound. In addition, the same scenario applies for the UK’s CPI rates , where should they imply persistent inflationary pressures it may aid the pound and vice versa.

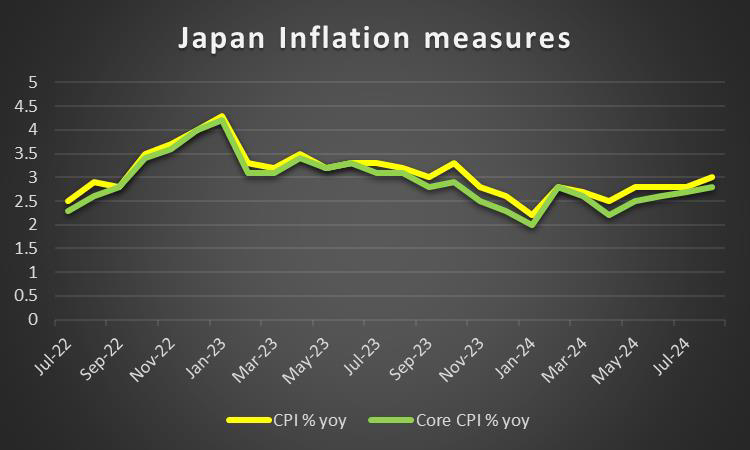

JPY – A hawkish BOJ?

On a fundamental level, we note that Japan’s newly appointed Cabinet is already being judged by the people for editing an official photo. The issue may appear immaterial, yet is a reminder that the new Government will be closely monitored and any actions made will be looked at with a microscope.

On a monetary level, we would like to note BOJ Himinio who stated that if the outlook for economic activity and prices presented in the July report are achieved, the BOJ will accordingly raise interest rates. Thus the apparent contradiction of BOJ Governor Ueda’s comments last week, appears to be enhancing the prospect of a hawkish BOJ. Thus the prospect of an increasingly hawkish BOJ, may aid the JPY in the coming week should more BOJ policymakers adopt a similar tone. In terms of financial releases for JPY traders next week, we would like to note Japan’s CPI rates for September which are due on Friday. Should the CPI rates further enhance and showcase that the bank is on track to achieve 2% inflation in a sustainable manner, it may aggravate calls for further rate hikes by the BOJ which may aid the JPY. On the flip side, should the aforementioned scenario not materialize, it may increase pressure on the BOJ to withhold from raising interest rates which in turn may weigh on the JPY.

EUR – ECB decision next week

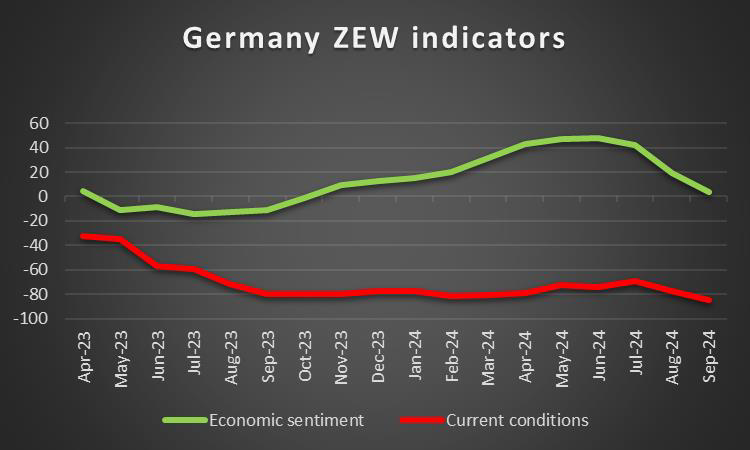

We make a start for EUR traders with ECB board member Kazak’s comment that “if inflation in the next year really returns to a sustainable 2%, interest rates have to be on a neutral level”. Furthermore, the ECB’s September monetary policy meeting minutes showcased that ECB Chief Economist Lane proposed that “looking ahead, a gradual approach to dialing back restrictiveness would be appropriate if the incoming data were in line with the baseline projection”. Overall, the ECB’s minutes in addition to ECB policymaker Kazak, tend to imply that the ECB may be poised to continue on their monetary policy easing cycle in their meeting next week. In particular, the majority of market participants currently expect the bank to cut by 25bp with EUR OIS currently implying a 98.5% probability for such a scenario to materialize. Hence, attention may turn to ECB Lagarde’s press conference following the decision, where should she imply that the bank may continue cutting interest rates, it could weigh on the EUR. On the flip side, should ECB President Lagarde showcase a desire to refrain from cutting interest rates further in the near future, it may have the opposite effect and thus aid the EUR. On macroeconomic level, we would like to note Germany’s ZEW economist sentiment figure for October which is due on Tuesday. Should the figure come in lower than the prior reading, it may imply that confidence from the consumer side in the German economy may be worsening and thus weigh on the EUR given the significance of the German economy in the Eurozone and vice versa.

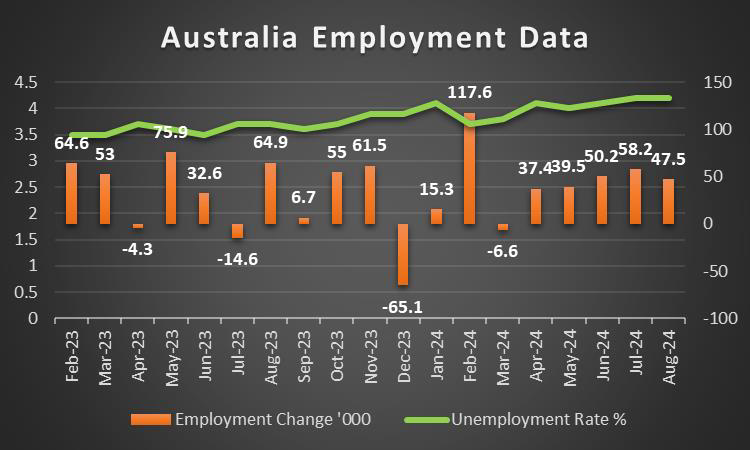

AUD – Employment data in focus

We make a start on a macroeconomic level for Australia by noting that no major financial releases occurred during the week and that traders may be more interest in the employment data for September which is set to be released next Thursday. In particular, we would like to emphasize the unemployment rate which should it come in higher than the prior reading of 4.2% it may imply a loosening labour market which may increase pressure on the RBA to cut interest rates in their next meeting. Whereas should the unemployment rate tick downwards, it may imply a resilient labour market which in turn could increase pressure on the RBA to hike interest rates. Overall, the release of the nation’s employment data for September next week, takes on an even greater importance due to the release of the RBA’s last meeting minutes this week, in which the board discussed both possibilities of raising and cutting interest rates. Thus the employment data may play a crucial role in the bank’s decision during their next monetary policy meeting. Furthermore, given Australia’s close economic ties with China, traders may be interested in China’s GDP rate for Q3 and Industrial output rate for September which are due out on Friday. Should the financial releases imply a resilient Chinese economy, it may translate into a stronger Australian Dollar and vice versa.

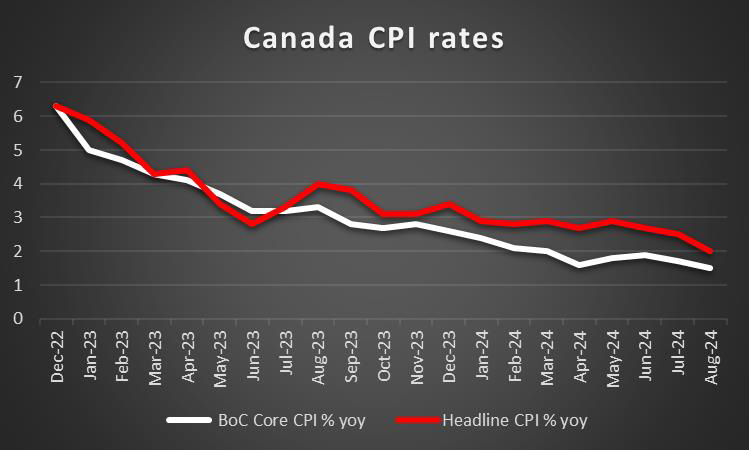

CAD – September CPI rates next week

CAD traders may be interested on a fundamental level on the path of oil prices, given the status of Canada as a major oil-producing economy. Hence on a geopolitical level, should tensions in the Middle East increase and even further, should oil-producing facilities be targeted in a retaliatory strike from Israel against Iran it could provide support for oil prices and by association the Loonie. We would like to highlight that Canada’s employment data for September is set to be released later on today. Therefore, should the data show a tightening Canadian employment market we may see the CAD getting some support as the data would allow the BoC not to expedite its rate-cutting path while a widening of the slack in the Canadian employment market could add more pressure on BoC for faster rate cuts and thus weigh on the Loonie. For next week, Loonie traders may be interest in the release of Canada’s CPI rates For September, which should they showcase a further easing of inflationary pressures in the Canadian economy it may weigh on the CAD. Whereas should the CPI rates come in hotter than expected it could provide support for the Loonie, as it may increase pressure on the BoC to gradually rather than aggressively ease their monetary policy stance.

General Comment

As an epilogue, we would like to make a comment for the situation in the Middle East that is still tantalizing the markets. The possibility of Israel targeting and destroying Iranian oil infrastructure such as the Khark Island, a major Iranian oil export hub, are still in play. In such a scenario we may see oil prices getting a substantial boost, as market worries for the supply chains and a subsequent tightening of the international oil market, could intensify further. In the US Equities markets, all three major indexes appear to be on track to end the week in the greens. We would also like to note that earnings season has begun once again, with Citigroup (#C), Morgan Stanley (#MS), Goldman Sachs (#GS) and Rio Tinto (#RIO) amongst others are expected to release their earnings report.

如果您对本文有任何常规疑问或意见,请直接发送电子邮件至我们的研究团队,地址为 research_team@ironfx.com

免责声明:

本信息不被视为投资建议或投资推荐, 而是一种营销传播. IronFX 对本信息中引用或超链接的第三方提供的任何数据或信息概不负责.