As we are leaving behind us an exciting week we take a peek at what next week has in store for the markets. On a monetary level we note the release of RBA’s minutes of the November meeting on Tuesday, while a number of policymakers from various central banks are expected to make statements and could alter the market’s expectations in regards to monetary policy. As for financial releases, we make a start with a slow Monday as we get Eurozone’s industrial output for September, while on Tuesday we note the release from Japan of the GDP rate for Q3, China’s industrial output for October, UK’s employment data for September, Eurozone’s preliminary GDP rate for Q3, Germany’s ZEW indicators for November, the US PPI final demand rate for October and Canada’s Manufacturing sales for September. On Wednesday we get Japan’s machinery orders for September, Australia’s wage price index for Q3, UK’s CPI rates, the US retail sales, Canada’s CPI rates and the US industrial production, all being for October. On Thursday we get Japan’s trade data, Australia’s employment data and Eurozone’s final HICP rate all being for October and in the American session we get the US weekly initial jobless claims figure as well as the Philly Fed Business index for November. On Friday, we note the release of Japan’s CPI rates, UK’s retail sales and Canada’s producer prices, all being for October.

USD – Easing of the Fed’s rate hiking path expected

The USD is about to end the week lower against its counterparts, with the release of the US employment report for October, the mid-term elections and especially the CPI rates for October, all affecting its path. The employment data for October tended to show that the Fed’s monetary policy tightening may have started to affect the US employment market, as the unemployment rate rose to 3.7%, yet the US employment market maintains its ability to create new jobs given that the NFP figure dropped yet not as much as the market expected. Nevertheless, despite the rise of the unemployment rate the overall picture of the employment market seems to remain rather tight. On the other hand the headline CPI rate slowed down considerably on a year on year level, implying that inflation has peaked and is now slowing down, yet the slowing of inflationary pressures in the US economy was even more evident as the month on month rate remained unchanged and all core rates decelerated beyond forecasts. The release may intensify the market’s expectations for an easing of the Fed’s rate hike path. Yet comments made by Minneapolis Fed President Kashkari before the release, that any talk for a pivot in the bank’s stance is premature tended to underscore the bank’s decisiveness. On the other hand, Philadelphia Fed President Harker stated that the

time for the Fed to slow rate hikes is coming. On a more fundamental level, we note that US midterm elections results are still not completed with Republicans being poised to get control of the House of Representatives, but results for the Senate are still considered to be indecisive and we may have to wait until the last vote is counted for the actual result. Overall, the results of the midterm elections may actually provide the Republicans the chance to bring the US Government to a political gridlock thus curbing the expansionary fiscal policy of US President Biden and allowing the Fed to remain alone in navigating the US economy. Yet the failure of the Republicans to produce a cataclysmic red wave may be a slap on the face for the efforts of former US President Trump for a re-run in the 2024 elections.

GBP – Autumn statement in the epicenter of attention

The pound is about to end the week stronger against the USD and the EUR and seems to edge lower against the JPY. The market’s attention may still be on the prospect of a deep recession for the UK economy. It should be noted that next Thursday UK finance minister Jeremy Hunt, is expected to make the autumn statement and possibly announce spending cuts and substantial tax hikes. The Chancellor of the Exchequers is expected to cover a hole of £50 billion and regardless of the proportion of tax increases and spending cuts which are to be included in the mix, the overall restrictive fiscal policy is expected to weigh on the UK economic outlook further. It was characteristic that BoE’s chief economist Hugh Pill stated that a tight fiscal budget could weigh on the UK economy even more than what the central bank expects and may alter BoE’s policy intentions. Furthermore, we would note that UK house prices contracted for a second month in a row and at the fastest rate since June 2021 in another possible sign of lack of demand for the UK housing market which intensifies worries for the outlook of the UK economy. Yet we would also like to note that financial releases could be of interest for pound traders as they may increase the volatility for the sterling, especially the CPI rates for October on Wednesday and should the rate accelerate further that may add additional pressure on BoE to continue tightening its monetary policy at a fast pace.

JPY – GDP and CPI rates eyed

JPY is about to end the week stronger against the USD and gains slightly against the GBP and the EUR in a sign of broader strength. On a monetary level we note the release of BoJ’s summary of opinions for the October meeting last Tuesday. In the document the bank stated that “Continued monetary easing is necessary in order to raise productivity and wage levels through supply-side reforms,

such as with “investment in people” and business portfolio transformation, and thereby lead to a virtuous cycle from income to spending”. Hence the meeting practically reaffirmed the bank’s dovish stance without any substantial objection being noted for now. On the other hand the document also showed that BoJ policymakers debated the need to have a look at possible side effects of an exit strategy, something that tended to imply that the bank may be more open to such a scenario. Yet, BoJ Governor Kuroda on Thursday, practically dismissed any idea of a monetary policy tightening in the short term, dismissing as premature any details of an exit strategy from the current ultra-loose monetary policy settings in place. In the coming week we note the release of the CPI rates for October on Friday yet before that we would highlight the release of the preliminary GDP rate for Q3 on Tuesday. A possible slowing of the GDP rate is expected and if actually so, may provide more leeway for BoJ, while an acceleration of the CPI rates could intensify the pressure the bank is allready facing.

EUR – Market worries remain

EUR is about to end the week higher against the USD, yet is losing ground against the GBP, the CHF and JPY. On the monetary front the ECB seems to remain on the hawkish side. It was characteristic that one of the hawks of the bank, Germany’s BuBa President Nagel was reported stating that the ECB would “press ahead with monetary policy normalisation with determination — even if our measures dampen economic growth”. The statement underscored the decisiveness of the bank to proceed with further rate hikes and QT at a future stage even if the bank’s monetary policy tightening could hurt growth in the area. On a fundamental level market worries for the economic outlook for the Eurozone remain extensive, given the ECB’s intentions the energy crunch in Europe and the war in Ukraine. It should be noted that the final PMI figures for October tended to be slightly better than expected for the services sector, yet still noted the contraction of economic activity in the Eurozone. Also the contraction of Eurozone’s retail sales growth rate for September was narrower than in August, while investors and analysts are less pessimistic about the outlook of the Eurozone for the next six months according to the Sentix index for November.

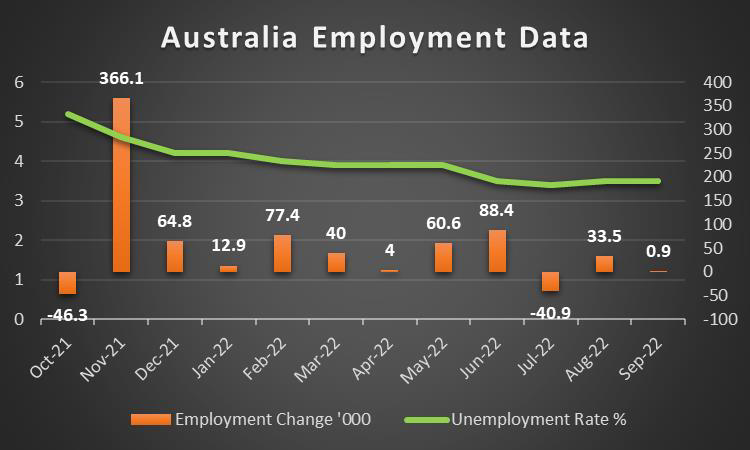

AUD – Australia’s employment data in focus

AUD is about to end the week stronger against the USD for a fourth consecutive week. On a monetary level RBA Deputy Governor Bullock, stated before a hearing at the Australian Senate that the rates may be at a level where the bank may pause its rate hiking path. Ms. Bullock stated, “interest rates will probably have to go up a little bit further, but we’re not set on our timing and we’re not set on the amount,”. It should be noted that RBA had allready slowed its rate hiking path to only 25 basis points rate hikes per meeting with the market pricing in another 25 basis points rate hike in the December meeting, while a pause is expected early next year. Hence we note the release of the bank’s November meeting minutes on Tuesday which could shed more light on the bank’s intentions. On a more fundamental level, we expect the Aussie to remain sensitive to the market sentiment as a commodity currency and a more positive, risk oriented market may

provide some support for AUD. On second note we would also highlight the close ties of Australia with China, given that Australia exports a high amount of raw materials to the Chinese mainland. It should be noted that China’s trade data for October showed that the China’s import growth rate for October contracted, that is definitely not good news for the Aussie. In the coming week we would note the release of China’s industrial output growth rate for October on Monday and a possible slow-down of the growth rate could weaken AUD. Yet the main market focus is expected to be on Australia’s employment data, with the earnings growth rate for Q3 being due out on Wednesday and the rest on Thursday. Should the data show that the Australian employment market remains tight, with the unemployment rate remaining at low levels, we may see the Aussie getting some support.

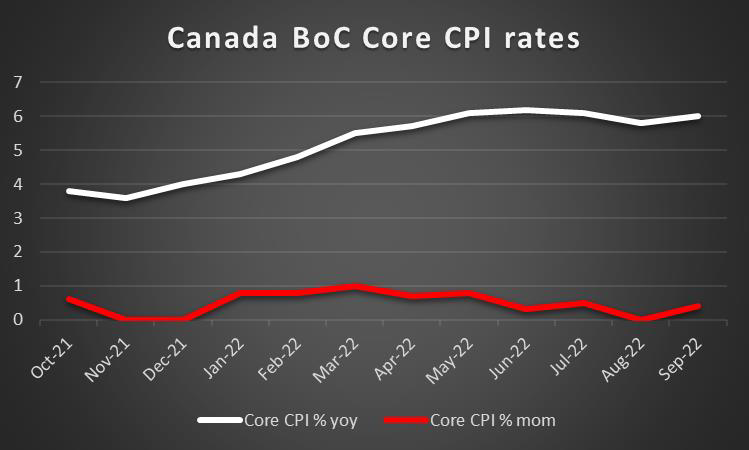

CAD- CPI rates to move the Loonie

Also the CAD is about to end the week stronger against the USD. On a monetary front BoC’s Governor Tiff Macklem stated that more rate hikes are to come, yet also noted that the Employment market may suffer some mild consequences. It should be noted that the release of Canada’s employment data for October last Friday tended to indicate a red hot employment market with a sky rocketing employment change figure of 108.3k and a low unemployment rate of 5.2%. On a fundamental level, we note that the Canadian government’s fiscal spending plans of additional C$6.1 billion, may despite BoC’s efforts, revitalise inflationary pressures in the Canadian economy. As for financial releases, we highlight Canada’s CPI rates for October on Wednesday and should rates show an acceleration we may see the pressure once again increasing for BoC to intensify the pace of its rate hikes. Also we note that the CAD may also have gotten some support from the improved market sentiment, given that as a commodity currency it’s considered to be a riskier asset. On the other hand, the drop of oil prices after three weeks of gains could weaken the CAD as well, as Canada is a major oil producing economy. The recent substantial increase in US oil reserves as reported by EIA and API tended to underscore the slack in the US oil market for the past week, while

increased worries for a possible weakening of the demand side of the commodity tended to contribute to the drop of WTI’s price. Should oil prices drop further, we may see CAD bulls having second thoughts.

General Comment

In the coming week we note the higher degree of dispersion of financial releases from different economies, maybe with the main characteristic being that the number of high impact financial releases stemming from the US are lessening. Hence we would expect the USD to relent part of the initiative to other currencies, and thus allow for the blend of trading opportunities in the FX market to lighten on the greenback’s side. Yet the release of the US CPI rates for October on Thursday unleashed forces in the FX market that may continue to affect it in the coming week as well. The market’s expectations for a possible easing of the Fed’s rate hiking path, seem to solidify sinking the USD for now, while at the same time providing support for US stockmarkets as a more risk oriented market seems to be building up. Nevertheless we would like to note the release of the earnings reports for Q3 of Home Depot and Walmart on Tuesday, Cisco on Wednesday and Ali Baba on Thursday and JD.com on Friday. As for gold we note that the weakening of the greenback tended to polish the shiny metal as did also the drop of US yields. We have to highlight that the negative corelation with the USD was on display once again in the past few days and we expect that tendency to be maintained in the coming week as well.

如果您对本文有任何常规疑问或意见,请直接发送电子邮件至我们的研究团队,地址为 research_team@ironfx.com

免责声明:

本信息不被视为投资建议或投资推荐, 而是一种营销传播. IronFX 对本信息中引用或超链接的第三方提供的任何数据或信息概不负责.