As the week draws to a close we have a look at what next week has in store for the markets. On the monetary front, we note the ECB’s interest rate decision on Thursday, followed by ECB President Lagarde’s press conference. As for financial releases, we note that on Monday we get China’s GDP rates for Q2 and the Eurozone’s industrial production rate for May. On Tuesday, we get Germany’s ZEW Economic sentiment and current conditions figures for July, the US retail sales rate and Canada’s CPI rates both for June. On Wednesday, we get New Zealand’s CPI rate for Q2, Japan’s Tankan index figures for July, followed by the UK’s CPI rates, the Eurozone’s final HICP rate and the US industrial production rate all for the month of June. On Thursday, we get Japan’s trade balance figure and Australia’s employment data both for the month of June, followed by the UK’s employment data for May, the US weekly initial jobless claims figure and the US Philly Fed business index for July. On Friday we get Japan’s CPI rates for June, UK’s retail sales for June and CBI business optimism figure for Q3, as well as Canada’s retail sales rate for May.

USD – Fed rate cuts on the horizon?

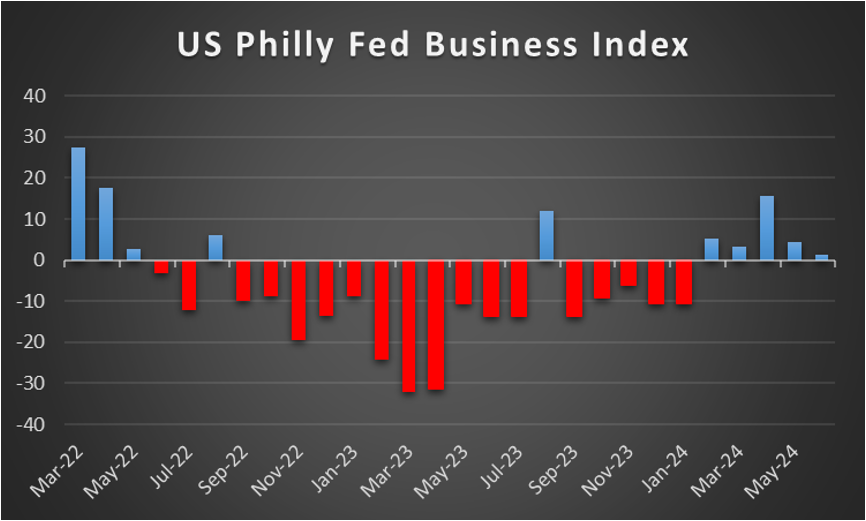

The USD weakened across the board over the course of the week. On a fundamental level, we note that the calls for President Biden to end his Presidential campaign have intensified. Yet, it appears that President Biden is not ready to give up just yet, although we would closely monitor the situation as the political instability that would ensue could spill over into the financial markets. On a macroeconomic level, the US employment data showcased a loosening labour market, with the unemployment rate for June ticking upwards to 4.1% from 4.0% in May. The release tended to weigh on the greenback and appears to have overshadowed the higher than expected Non-Farm Payrolls figure. As such, the implications of a loosening labour market could increase pressure on the Fed to ease their monetary policy stance given its dual mandate. Moreover, the US CPI rates for June both on a core and headline level came in lower than expected, implying easing inflationary pressures in the US economy, further aiding our aforementioned comment. The big picture tends to be that the US Labour market is cooling, as was implied by Fed Chair Powell during his testimony to Congress earlier on this week. Furthermore, Fed Chair Powell also testified that the most recent inflation readings have shown modest progress for inflation returning to the bank’s 2% inflation target, which may imply that the bank may ease their monetary policy stance, as is currently expected by market participants at the end of the year. However, it should be said that the Fed Chairman did also express concerns about the risks of inflation re-emerging should the bank’s rate cuts be premature. Overall, the testimony could be described as relatively dovish in nature and should further policymakers re-iterate Fed Chair Powell’s comments in the coming week it could weigh on the dollar. Lastly, we would like to note the Philly Fed Business Index which acts as a barometer for business activity in the US economy is set to be released next week. The expected figure of 2.9 is higher than the prior month’s figure of 1.3 and thus could support the USD. Anything lower could instead weigh on the dollar. Yet also on the production side of the US economy we also note the release of the US industrial output growth rate for June, which could gauge the width of economic activity for the sector. Furthermore on the demand side of the US economy we highlight the release of the US retail sales growth rate for June on Tuesday, while the UoM consumer sentiment is still to be released today.

GBP – UK GDP rates boost economic optimism

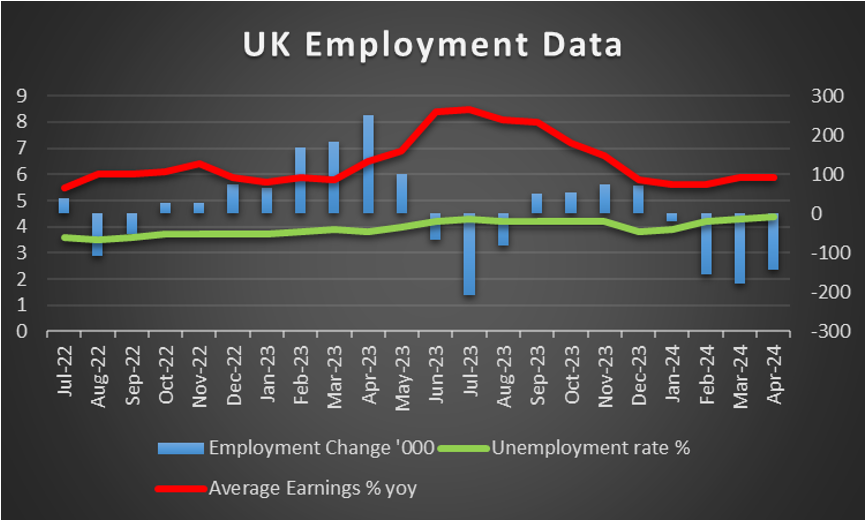

The pound is about to end the week higher against the USD and the EUR yet remains relatively stable against the JPY. On a fundamental level for pound traders, we note that the Labour party won a resounding majority in last week’s elections, having secured 412 parliamentary seats in a landslide victory which saw the worst defeat for the Conservative party since its inception. The new UK finance minister, Rachel Reeves, seems to be actively pursuing growth for the UK economy and is ready to expand the country’s fiscal policy, which could support the GBP. On a monetary policy level, we note that BoE Chief Economist Pill during an interview earlier this week stated that the timing of an interest rate cut was an “open question”. The comment by BoE Pill tend to imply that the bank may keep interest rates high for longer, thus dampening the market’s expectations of an August rate cut. Furthermore, BoE Mann warned that price pressures are still strong, with the risk of inflation rising again, which could further dampen the market’s expectations of two rate cuts this year. Overall the implications of interest rates remaining at their current levels for a prolonged period of time, may have aided the pound. On a macroeconomic level, we note that the UK’s GDP rates for May came in higher than expected, showcasing a resilient UK economy which managed to expand at an even faster rate than what was predicted by economists. The positive economic outlook for the UK may have further supported the sterling this week. In the coming week, we would like to note the UK’s employment data for May, where should it be shown that the UK labour market remains resilient, it could aid the pound and vice versa. On the inflation front we note the release of UK’s CPI rates for June on Wednesday and a possible deceleration may ease the way of BoE towards rate cuts.

JPY – JPY still trades near dangerously weak levels

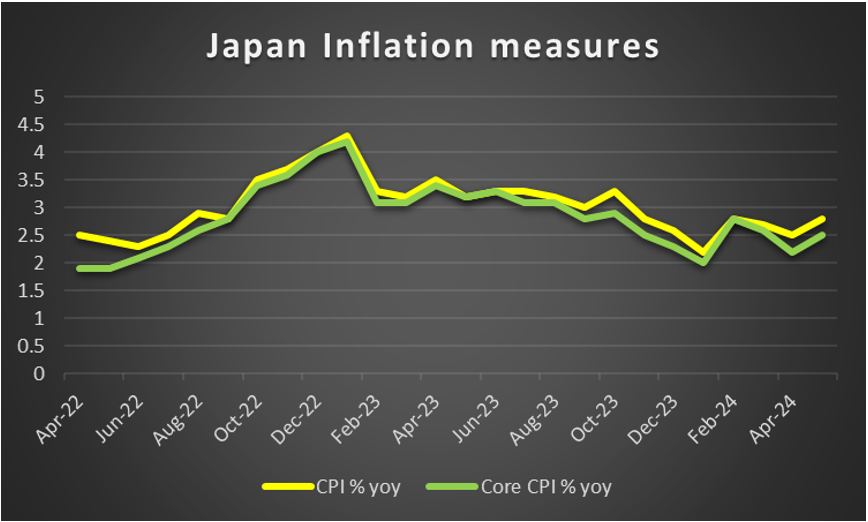

The JPY is about to end the week stronger against the dollar, slightly stronger against the EUR and relatively unchanged against the pound. The relative strength of JPY may have been propped by a possible market intervention of Japan on Thursday during the release of the US CPI Rates for June. The Japanese government did not take responsibility for such an operation yet the strengthening of JPY tends to remain unexplained. Υet on the other hand, a possible market intervention may bring only temporary relief for the Yen as the fundamentals underpinning JPY’s weakness remain intact. On a macroeconomic level, we note that the household spending rate for May came in lower than expected, implying a contraction in spending from Japanese households, which in turn may have weighed on the Yen. For next week, we would like to note Japan’s core and headline CPI rates for June, where should they come in higher than expected, implying an acceleration in inflationary pressures, it could increase pressure on the BOJ to adopt a more hawkish stance, maybe even expedite the market anticipated rate hike in September. In such a scenario, it may provide support for the Yen, whereas should the rates come in lower than expected, it may further weigh on the JPY. Last but not least, on a fundamental level, we note JPY’s ability to attract safe haven inflows in times of crisis, a characteristic that could come into play next week, should tensions between China and Taiwan continue to escalate.

EUR – ECB decision next week

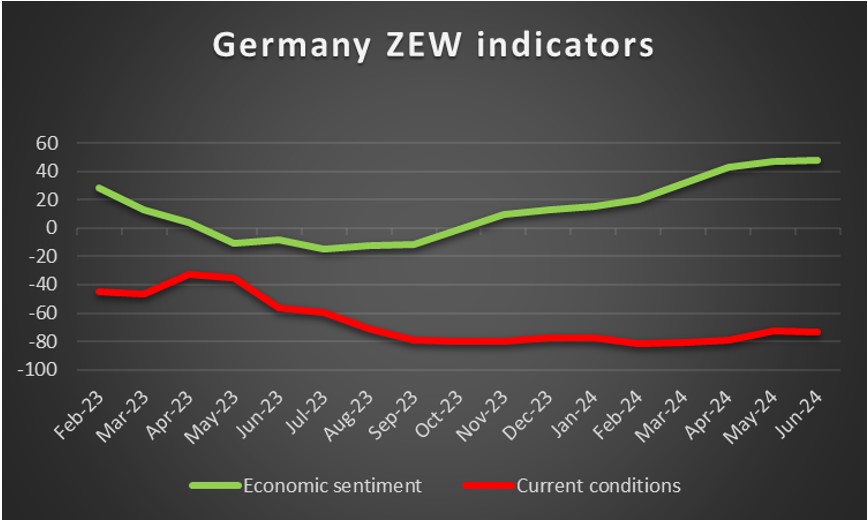

The common currency is about to end the week higher against the USD, but weaker against the GBP and JPY. On a fundamental level, we highlight the second round of the French Legislative elections which saw a surprise victory by the left-wing alliance, which in turn eased market worries for a possible win of Marine Le Pen’s far-right National Rally (NR). Despite this, volatility for the EUR remains high, as no clear parliamentary majority was gained, which could intensify the political instability within the EU should the French political parties fail to form a government, to govern one of the EU’s largest economies. On a monetary level, we note the ECB’s interest rate decision next week, with the majority of market participants anticipating the bank to remain on hold, with EUR OIS currently implying a 92.6% probability for such a scenario to materialize. As such, our attention turns to the forward guidance and ECB President Lagarde’s press conference following the decision. Should the ECB President imply that the bank may be preparing to cut interest rates in their next meeting, as is currently expected, it could weigh on the EUR. However, any signs of hesitation to proceed with more rate cuts, could have the opposite effect and thus could provide support for the EUR. On a macroeconomic level, we note a relatively easy going week for the EUR in terms of financial releases. Thus, our targets now turn to next week’s financial releases, and in particular Germany’s ZEW figures, where should the current conditions and economic sentiment indicators, showcase an optimistic outlook for the German economy, it may provide support for the EUR and vice versa. On another note, we would also monitor the release of the Eurozone’s final HICP rate, where should it come in higher than expected and thus imply an acceleration or persistent inflationary pressures, it may aid the common currency and vice versa.

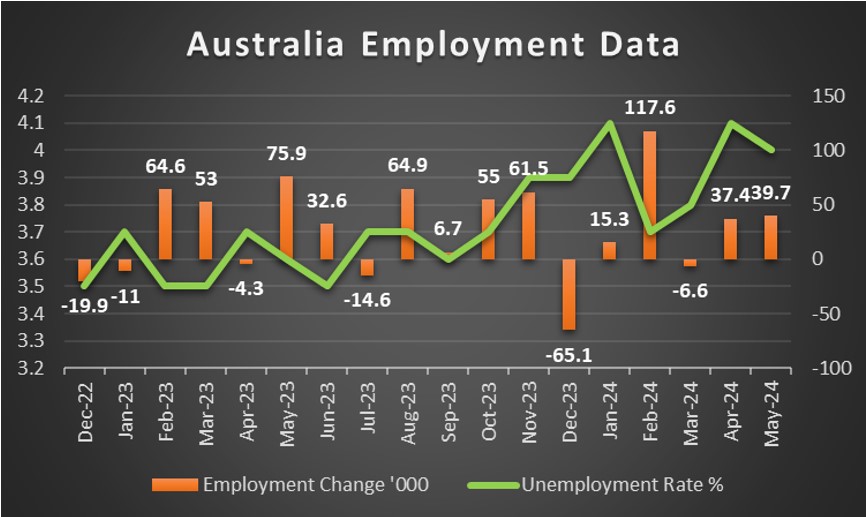

AUD – Employment data next week

AUD is about to end the week stronger that the greenback. On a fundamental level, we would like to note that tensions in the South China Sea between China and its neighbours appear to be intensifying. Should tensions between the US and China also escalate, it could inadvertently weigh on the Aussie as well. On a macroeconomic level, we note that it was a relatively quiet week for Aussie traders in terms of financial releases stemming from Australia. Yet, given the close Sino-Australian economic ties, the better than expected imports rate from China for June which came in at 2.8%, may imply that demand for raw materials from Australia may have increased and thus could have aided the Aussie. In the coming week, we expect interest in the Aussie to pick up, as the Australian employment data for June is set to be released. In the event that the Australian employment data implies a resilient labour market, it may increase pressure on the RBA to enhance the possibility of a rate hike, which in turn may aid the AUD. On the flip side, should the employment data imply a loosening labour market, it may weigh on the AUD, as pressure could instead increase on the RBA to cut interest rates. Lastly, we would also like to note China’s GDP rates for Q2 which are set to be released next week. As we have stated before, the close economic ties between China and Australia result in the Aussie being susceptible to financial releases from China. Hence, with the GDP rate for China expected to come in lower than the prior rates, could imply economic activity in China may be slowing down, which in turn could weigh on the Aussie.

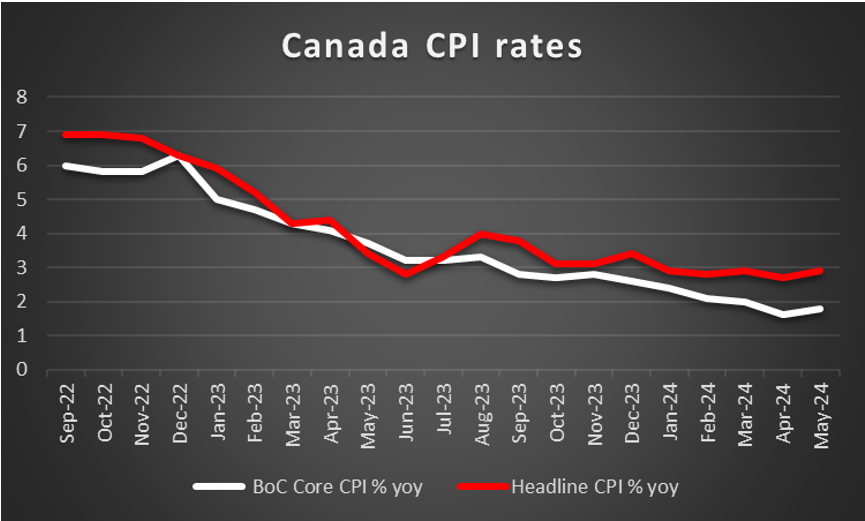

CAD – Inflation print next week

The Loonie is about to end for a fifth week in a row stronger than the dollar. On a macroeconomic level, we note that Canada’s unemployment rate for June which was released last Friday came in higher than expected at 6.4%, implying a loosening labour market which tended to weigh on the CAD following its release. Yet the Ivey PMI figure for June which vastly exceeded expectations appears to have mitigated the negative impact on the Loonie. For next week, we would like to point out the release of Canada’s core and headline CPI rates for June. Should the CPI rates imply an acceleration of inflationary pressures in the Canadian economy, it may increase pressure on the BoC to adopt a more hawkish stance which may aid the CAD. On the flip side, should the rates come in lower than expected and thus imply easing inflationary pressures, it may have the opposite effect. Interestingly, oil prices seem to have halted their ascent since last week, as such should they decrease in the upcoming week it may weigh on the Loonie given Canada’s status as a major oil-producing economy.

General Comment

Overall in the coming week, in the FX market, we expect the US to maintain some initiative over other currencies as some financial releases from the US could be considered of high impact. Yet the overall attention on Thursday, may turn to the ECB’s interest rate decision. As for US stock markets, we note that all three major US stockmarket indexes, that would be NASDAQ ,S&P 500 and Dow Jones 30, were on the rise for the week in a signal of increased confidence and optimism, with the S&P 500 and NASDAQ forming new all time highs once again.As for gold, we note that the negative correlation of gold prices to the USD seems to have resumed to gold’s favor. It should be noted that despite the relative stabilisation of US yields during the week, the CPI print for the US on Thursday seems to have turned the tide against gold sellers.

如果您对本文有任何常规疑问或意见,请直接发送电子邮件至我们的研究团队,地址为 research_team@ironfx.com

免责声明:

本信息不被视为投资建议或投资推荐, 而是一种营销传播. IronFX 对本信息中引用或超链接的第三方提供的任何数据或信息概不负责.