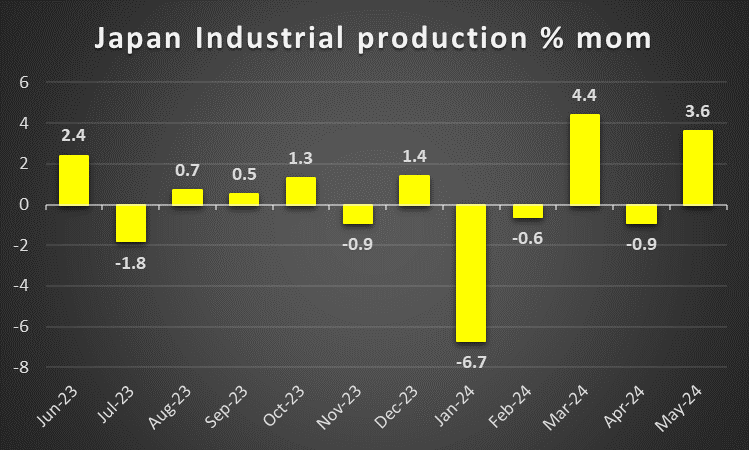

With the week coming to an end, we take a look at what next week has in store for the markets. On a monetary level, we highlight the release of the BOJ’s and the Fed’s interest rate decisions on Wednesday followed by the BoE’s and CNB’s interest rate decisions on Thursday. As for financial releases we make a start on Monday with the release of Sweden’s preliminary GDP rate for Q2, the UK’s CBI distributive trades figure for July. On Tuesday, we get Australia’s building approvals figure for June, their retail sales rate for June, France’s preliminary GDP rate for Q2, Switzerland’s KOF Indicator figure for July, the Czech Republic’s GDP rate for Q2, Germany’s and the Eurozone’s preliminary GDP rates for Q2, followed by the Eurozone’s economic sentiment figure, Germany’s preliminary HICP rate and the US consumer confidence figure all for the month of July and ending off the day is the US JOLTS Job openings figure for June. On Wednesday we get Japan’s preliminary industrial output rate for June, followed by China’s NBS manufacturing PMI for July, Australia’s CPI rate for Q2, France’s and the Eurozone’s preliminary HICP rates and the US ADP employment figure all for the month of July and Canada’s final GDP rate for May. On Thursday we get Australia’s trade balance figure for June, followed by China’s Caixin manufacturing PMI figure and the UK’s nationwide house prices rate both for July, the US weekly initial jobless claims figure, and ending off the day with Canada’s manufacturing PMI figure in combination with the US ISM Manufacturing PMI figure both for the month of July. Lastly, on a busy Friday, we start with Australia’s PPI rate for Q2 followed by Switzerland’s CPI rate for July and the highlight of the week which is the US employment data for July whilst the US Factory orders rate for June brings the week to a close.

USD – Fed decision in combination with NFP Friday

The USD is about to end the week relatively stronger against its counterparts .On a fundamental level for the USD we note the heated US presidential preelection period. The most recent development was the announcement by Biden that he would be ending is re-election bid in a shocking turn of events, in which the two assumptive candidates are Trump and Vice President Harris.

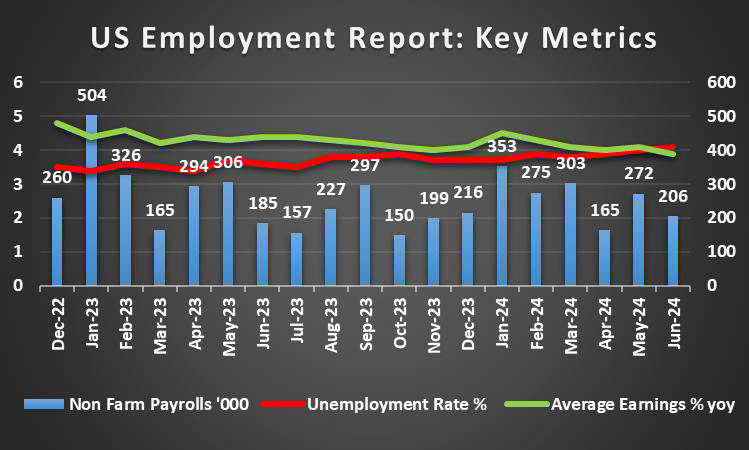

On a macroeconomic level, we note the financial releases from the US tend to paint a mixed economic picture. In particular, the Advance GDP rate for Q2 in addition to the preliminary core PCE rate came in higher than expected, implying a resilient US economy. Yet the preliminary S&P manufacturing PMI figure for July entered contraction territory, in addition to the durable goods

orders rate for June dropping significantly to -6.6%, which tends to cast some doubt on our aforementioned scenario. Nonetheless, for next week we would like to emphasize the US Employment data which is expected to showcase a loosening labour market when looking at the NFP figure for July and the unemployment rate which is expected to remain steady at 4.1%. Such a scenario could weigh on the dollar, yet the Fed’s interest rate decision is set to occur on Wednesday. In particular, FFF implies a 91.5% probability to remain on hold, and to cut three times by 25 basis points until the end of the year. As such, should the bank’s accompanying statement or Fed Chair Powell’s press conference showcase a hesitancy to cut interest rates it may aid the dollar and vice versa.

GBP – BoE decision next week

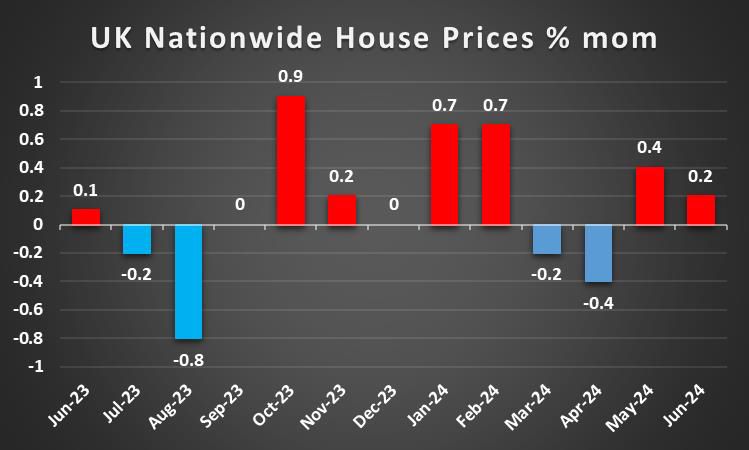

Cable is about to end the week lower, and the pound is also weakening against the JPY and EUR, n a sign of wider weakness. On a macroeconomic level, we note the UK’s preliminary manufacturing PMI figure for July, which came in higher than expected at 51.8, implying an expansion in the manufacturing sector of the UK economy. However, the much lower-than-expected CBI industrial orders figure for July, showcased that optimism from manufacturing executives for the business conditions in the UK decreased. Nonetheless, we turn our attention to the BoE’s interest rate decision which is set to occur next week. The majority of market participants are anticipating the bank to cut interest rates by 25bp, with GBP OIS currently implying a 54% probability for such a scenario to materialize. We had stated in last week’s report that the CPI rates remained unchanged at 3.5%yoy on a core level and at 2.0%yoy on a headline level, with the headline rate currently at the bank’s 2% inflation target. Yet, we still maintain our concerns for the Core CPI rates and thus their stubbornness to ease may increase pressure on the BoE to hold or adopt a more hawkish tone in the bank’s accompanying statement. In such a scenario we may see the sterling gaining ground against its counterparts, although should the bank cut interest rates it could instead have the opposite effect and thus weigh on the pound.

JPY – JPY strength continues with the BOJ’s decision is due next week

The main characteristic of the JPY may have been its significant strengthening across the board for the week, in a sign of wider strength. The strengthening of the JPY appears to have been maintained since the market intervention by BoJ two weeks ago with no clear signs of it stopping its ascent. We still maintain our view that there may be more way to go to push JPY higher in the coming week. On a monetary level, we note that the market’s expectations for the BoJ to hike rates in the September meeting. We note the release of Tokyo’s July CPI rates during today’s Asian session which came in at 2.2% on core level and 2.2% on a headline level, which may aid the narrative of inflation remaining sustainably at 2%. However, we turn our focus to the BOJ’s interest rate decision next week, with the majority of market participants anticipating the bank to increase interest rates, with BOJ OIS currently implying a 67.2% probability for such a scenario to materialize. As such should the BOJ hike in their next meeting it may provide support for the JPY, whereas should the bank remain on hold, it may have the opposite effect. On a macroeconomic level, besides the already mentioned Tokyo CPI rates for July, we would also like to note that economic activity for the manufacturing sector has worsened in July and has entered contraction territory according to the Jibunk Manufacturing figure, which appears to be contradicting the relative Reuters Tankan indexes which showcased an improvement in July. Last but not least and on a deeper fundamental level, we note that should we see uncertainty rising in the coming week we may see JPY getting some support as it is regarded as a safe haven instrument for financial markets.

EUR – Inflation readings next week

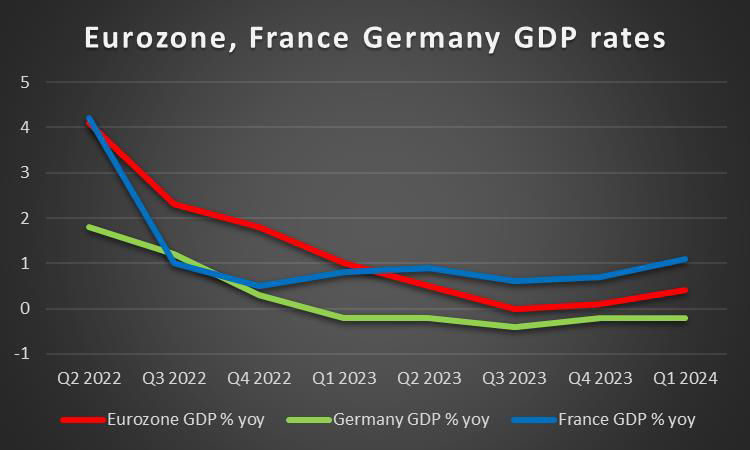

On a fundamental level for EUR traders we note that the rift between Budapest and Brussels appears to be expanding, with the commission urging “Hungary not to undermine the Union’s position on intra-EU arbitrations under the Energy Charter Treaty and to abide by the case law of the Court of Justice”. Overall, the announcement by the commission may not have an impact on the EUR currently, yet the divisions between Hungary and the rest of the EU are worth monitoring. On a monetary level, we note that ECB Nagel stated on Thursday that “if the figures remain the same over the next twelve months, there might be a chance that we can reduce interest rates further at one or the other meeting”. The comment essentially implies that if inflation data doesn’t showcase a surprise towards the upside, the bank may continue on its monetary easing path. Yet, with Germany’s, France’s and the Eurozone as a whole set to release their preliminary HICP rates for July next week, the comments by ECB Nagel may be overshadowed. Moreover, we would like to note the preliminary Q2 GDP rates for the Eurozone, France and Germany are also set to be released next week. Overall, should the GDP rates showcase a resilient euro area, it may provide support for the common currency and vice versa. However, with the HICP rates set to be released after the GDP rates, they may overshadow or intensify the potential impact of the preliminary GDP rates for Q2. Lastly, some concern for the EUR area did appear to emerge this week, after Germany’s, France’s and the Eurozone’s preliminary manufacturing PMI figures came in lower than expected, showcasing a deeper contraction of the bloc’s manufacturing sector, which in turn may have weighed on the EUR.

In conclusion, next week is set to be a busy one for EUR traders, with numerous key financial releases.

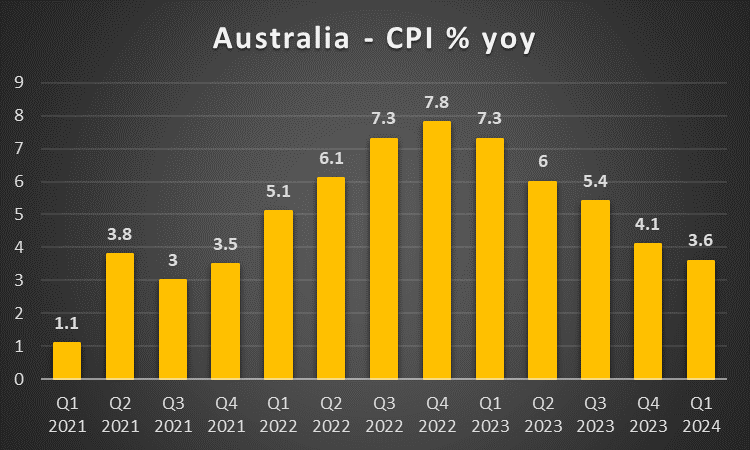

AUD – Australia’s CPI rate for Q2 due next week

On a macroeconomic level, we note that Australia’s preliminary manufacturing PMI figure for July came in higher than the prior figure, yet still remains in contraction territory. Aussie traders may be interest in next week’s financial releases, with Australia’s CPI rate for Q2 and retail sales rate for June taking the stage for AUD traders. We would take a closer look at the country’s CPI rate for Q2, where should it come in higher than the prior rate of 3.6%, implying an acceleration of inflationary pressures in the economy, it could increase pressure on the RBA to adopt a more hawkish stance which in turn may aid the Aussie. Despite some high impact financial releases from Australia next week, we expect fundamentals to lead the way for Aussie traders. We also note the deep economic ties between Australia and China on a fundamental level. Hence we highlight the release of China’s Caixin and NBS manufacturing PMI figures for July next week. Should the manufacturing PMI figures imply an improvement in China’s manufacturing sector, it may imply that demand for raw materials from Australia may increase and thus in turn could aid the AUD. On another note, the People’s Bank of China has unexpectedly lowered the cost of its one-year policy loans by the most since April 202 per Bloomberg, in addition to its medium-term lending facility rate being reduced by 20bp to 2.3% on Thursday. The measures to support the Chinese economy by the PBoC could provide some support for AUD.

CAD – BoC cuts rates as expected

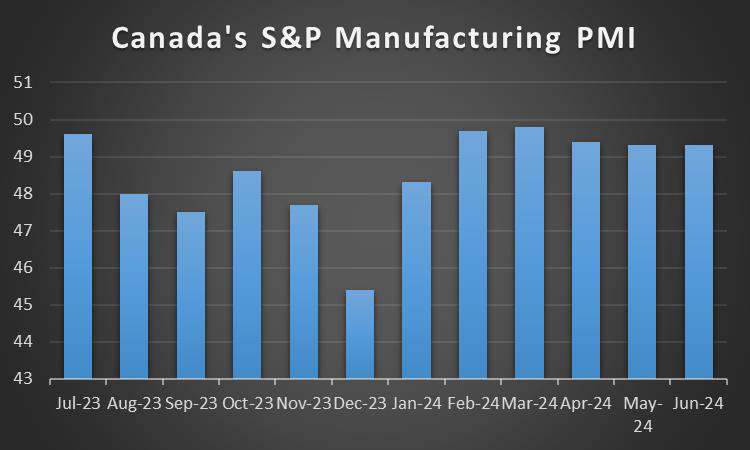

On a macroeconomic level, we note for the Loonie, that no major financial releases stemming from Canada were released this week. However, on a macroeconomic level, the BoC’s interest rate decision occurred earlier on this week, with the bank cutting interest rates by 25bp as was widely expected by market participants. The release tended to weigh on the Loonie, as the bank in its accompanying statement recognized the presence of excess supply which is expected to ease inflationary pressures further. At the same time, it also stated that it remains data-dependent which tends to add some ambiguity for its intentions. Nonetheless, the apparent dovish sentiment that has emerged from the bank’s accompanying statement may have intensified the negative implications of the Loonie following the bank’s decision to cut interest rates. On a fundamental level, we note the positive correlation of oil prices with the Looney, given Canada’s status as a major oil producing economy and thus the decline of oil prices may have further weighed on the CAD. Should we see oil prices falling in the coming week, we may see them having also a bearish effect on the Looney.

General Comment

As a closing comment, in the FX market we expect the USD to expand its influence over other currencies as the frequency and gravity of US financial releases intensifies. Nevertheless, there are days in the calendar that could allow for other currencies to get the initiative and form their own course, thus creating a more balanced trading mix for market participants. As for US stockmarkets, we note our concerns for the downwards trajectory that the NASDAQ, S&P500 and Dow Jones 30 have taken in the past week. Moreover, we would like to note the earnings releases next week of McDonalds (#MCD) on Monday, PayPal (#PYPL), Starbucks (#SBUX), Pfizer (#PFE) and Airbus (#Airbus) on Tuesday, Meta (#FB), HSBC (#HSBC) and Boeing (#BA) on Wednesday and Ferrari (#RACE) and Intel (#INTC) on Thursday. Should the market worries intensify further in the coming week, we expect the adverse effect on tech shares to widen. As for gold prices we note that the negative correlation of the USD with gold’s price, seems to be in some effect in the past few days despite gold’s price not being proportionate to the movements in the dollar. The decline of the US yields over the past week does not seem to have polished the shiny metal. Should the USD strengthen over the coming week, we may see Gold’s price retreating to lower ground.

如果您对本文有任何常规疑问或意见,请直接发送电子邮件至我们的研究团队,地址为 research_team@ironfx.com

免责声明:

本信息不被视为投资建议或投资推荐, 而是一种营销传播. IronFX 对本信息中引用或超链接的第三方提供的任何数据或信息概不负责.