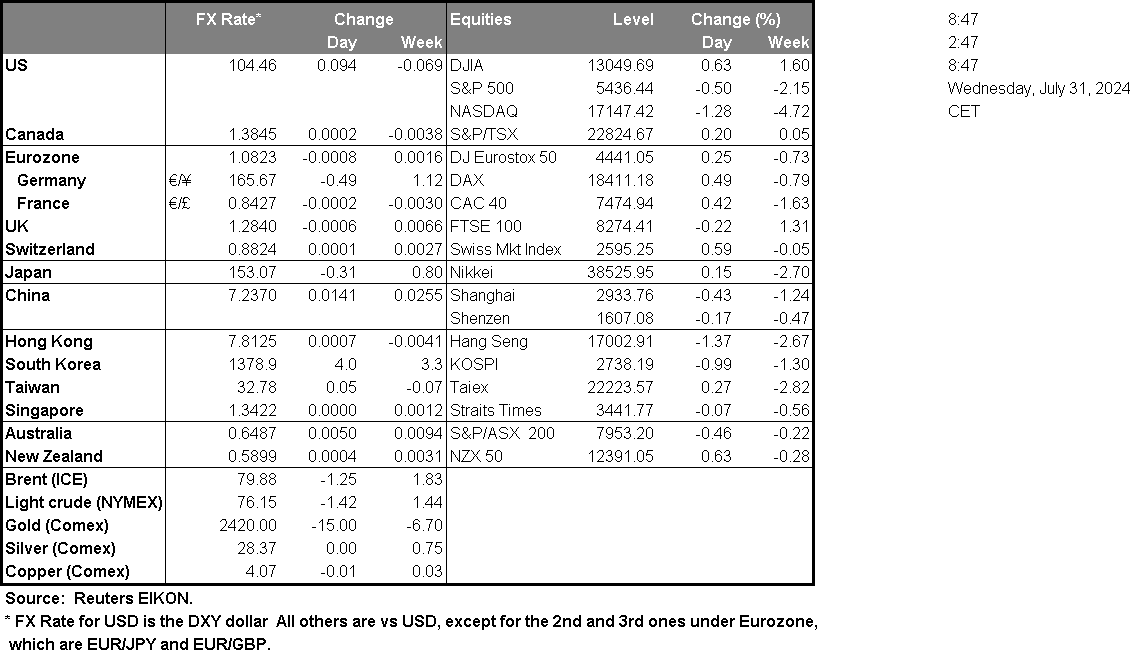

The Fed’s interest rate decision is set to occur later on today. Currently, the majority of market participants are anticipating the bank to remain on hold with FFF currently implying a 96% probability for such a scenario to materialize. As such our attention turns to the bank’s accompanying statement and Fed Chair Powell’s press conference. We would not be surprised to see a more cautionary Fed, in regards to the bank’s document outlining the risks poised of keeping interest rates too high for too long. Yet, when considering that the unemployment rate in the US remains at historically low levels, in combination with a resilient economy, as seen by the preliminary GDP rate for Q2 which came in at 2.8% which is significantly higher than the prior quarter’s rate, we would not be surprised to see a comment in the bank’s accompanying statement in regards to the risks of a premature rate cut outweigh the risks of keeping rates steady. In conclusion, we tend to agree with the majority of participants that the bank may remain on hold, but opt for the view that the bank may provide hints for rate cuts beginning further down the line such as in November rather than the current expectations of a cut in their September meeting. In turn, such a scenario could provide support for the greenback.The Eurozone’s and France’s preliminary HICP rates for July are due out in today’s European session. Should the preliminary HICP rates imply persistent or even an acceleration in inflationary pressures in the bloc, it may increase pressure on the ECB to withhold from cutting interest rates any time soon. We would like to note that Germany’s preliminary GDP rates for July which were released yesterday came in higher than expected and as a matter of fact, showcased an acceleration of inflationary pressures in one of the bloc’s largest economies. We are concerned that if inflationary pressures in the zone fail to decrease, the ECB may push back against the market’s current expectations of two more rate cuts by the end of the year which in turn could aid the EUR. Earlier on today, the BOJ hiked interest rates by 15bp, which was just above expectations of 10bp. Yet what piqued our interest was the banks accompanying statement in which it was stated that “the Bank will accordingly continue to raise the policy interest rate” implying that the BOJ may be preparing to hike rates in the future.

EUR/USD appears to be downwards fashion. We maintain our a bearish outlook for the pair and supporting our case is the downwards moving trendline which was incepted on the 17 of July, in addition to the RSI indicator below our chart which currently registers a figure near 40, implying a bearish market sentiment. For our bearish outlook to continue, we would require a clear break below the 1.0802 (S1) support line, with the next possible target for the bears being the 1.0740 (S2) support line. On the flip side for a sideways bias, we would require the pair to remain confined between the sideways moving channel defined by the 1.0802 (S1) support line and the 1.0865 (R1) resistance level. Lastly, for a bullish outlook, we would require a clear break above the 1.0865 (R1) resistance line, with the next possible target for the bulls being the 1.0940 (R2) resistance level.

USD/JPY appears to be moving in an downwards fashion. We switch our a bullish outlook in favour of a bearish outlook for the pair and supporting our case is the clear break below the sideways moving channel which was incepted on the 24 of July, in addition to the RSI indicator below our chart which currently registers a figure near 30, implying a bearish market sentiment. For our bearish outlook to continue, we would require abreak below the 150.30 (S1) support line with the next possible target for the bears being the 147.40 (S2) support line. On the flip side, for a bullish outlook, we would require a clear break above the 152.35 (R1) resistance line, if not also the 154.90 (R2) resistance level, with the next possible target for the bulls being the 157.65 (R3) resistance ceiling.

今日其他亮点

Today in the European session, we get France’s preliminary HICP rate and the Eurozone’s preliminary HICP rate both for the month of July. In the American session, we note the US ADP national employment figure for July, Canada’s GDP rate for May, and the US weekly EIA crude oil inventories figure. In tomorrow’s Asian session, we get Australia’s manufacturing PMI figure for July in addition to their trade balance figure for June and China’s Caixin final manufacturing PMI for July. On a monetary level we note Japan’s interest rate decision that was set to occur during today’s Asian session, and the highlight of the week which is the Fed’s interest rate decision during today’s American session, followed by Fed Chair Powell’s post decision press conference.

EUR/USD 4H Chart

- Support: 1.0802 (S1), 1.0740 (S2), 1.0670 (S3)

- Resistance: 1.0865 (R1), 1.0940 (R2), 1.1005 (R3)

USD/JPY 4H Chart

- Support: 150.30 (S1), 147.40 (S2), 144.80 (S3)

- Resistance: 152.35 (R1), 154.90 (R2), 157.65 (R3)

如果您对本文有任何常规疑问或意见,请直接发送电子邮件至我们的研究团队,地址为 research_team@ironfx.com

免责声明:

本信息不被视为投资建议或投资推荐, 而是一种营销传播. IronFX 对本信息中引用或超链接的第三方提供的任何数据或信息概不负责.