The week is coming to an end and we have a look at what next week has in store for the markets. On the monetary front, the highlights of the week are expected to be the Fed’s interest rate decision on Wednesday and from Japan BoJ’s interest rate decision on Friday. As for financial releases, we make a start on Monday with Japan’s current account balance for April and revised GDP rates for Q1 and we also get Sweden’s GDP rates for April, Norway’s CPI rates for May and Eurozone’s Sentix index for June. On Tuesday we get UK employment data for April, the Czech Republic’s CPI rates for May and Canada’s Building permits for April. On Wednesday we note the release of Japan’s PPI rates for May China’s inflation metrics also for May, the UK’s GDP rates for April and the US CPI Rates for May. On Thursday, we note the release of Australia’s employment data for May, the Eurozone’s industrial output rate for April and from the US the weekly initial jobless claims figure and the PPI rates for May. Finally, on Friday we get Sweden’s CPI rates for May and from the US the preliminary University of Michigan consumer sentiment for June.

USD – Fed’s interest rate decision to shake the USD

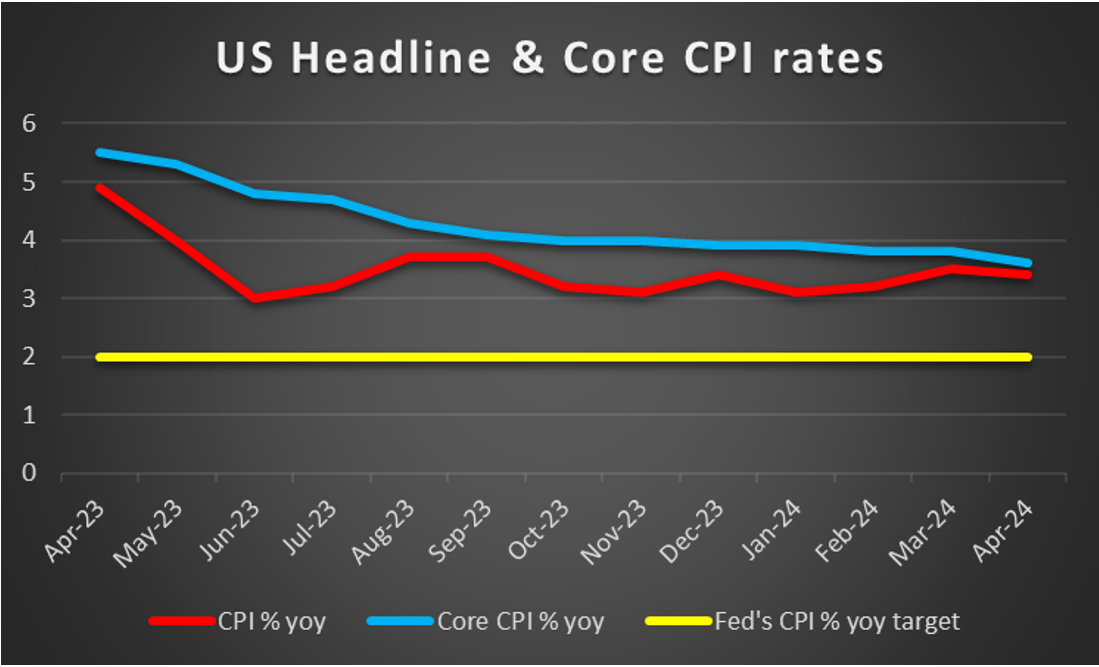

The USD is about to end the week slightly in the reds against its counterparts. Please note though that the US employment report for May with its NFP figure is still to be released and could alter the greenback’s direction. On a macroeconomic level, we note the unexpected drop of the ISM manufacturing PMI figure for May which implied a deeper contraction of economic activity in the sector and tended to darken the macroeconomic outlook for the US economy. On the contrary, the non-manufacturing PMI figure for the same month rose implying a faster expansion of economic activity. On the monetary front, we highlight the release of the Fed’s interest rate decision next Wednesday. The bank is widely expected to remain on hold and Fed Fund Futures tend to imply a probability of 99% for such a scenario to materialise. The USD is about to end the week slightly lower against its counterparts. We concur with the market’s expectations and hence place more emphasis on the bank’s forward guidance and the new dot plot. It should be noted that the market expects the bank to start cutting rates in its September meeting and deliver another rate cut in December. Hence, should the bank show that its prepared to keep rates high for longer we expect the USD to gain while a possible predisposition of the bank to start cutting rates could weaken the USD as it would verify the market’s hopes for an earlier rate cut. Please note that the US CPI rates for May are also to be released on Wednesday, and a possible acceleration of the CPI rates in the past month could harden the Fed’s stance. We expect the release to have ripple effects beyond the FX market with possibly US stock markets and gold’s price being also affected. On a fundamental level, we noted that the preelection period for November’s US Presidential elections has heated up especially after the conviction of former US President Trump, polarising further the US society. On a deeper fundamental level, we expect that any increase of uncertainty could provide some safe haven inflows for the greenback and not only on a political level.

GBP – Employment data and GDP rates ahead

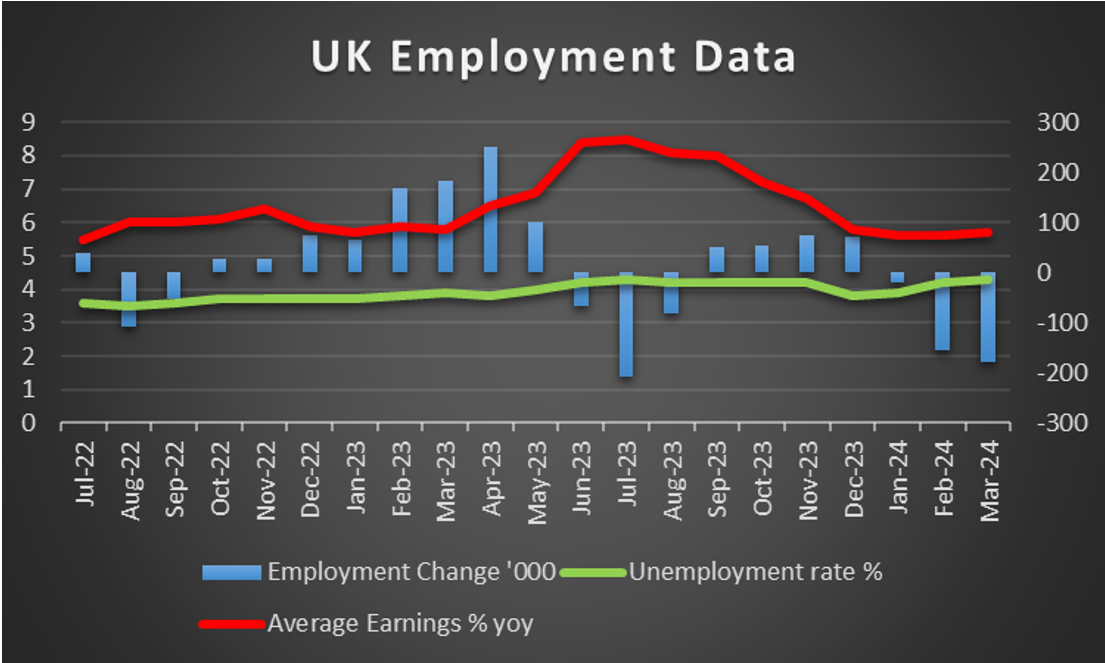

The pound is about to end the week in the greens against the USD, remains unchanged against the EUR and loses a bit against the JPY. On a political level, we note that the pre-election period for the general elections on the 4th of July is intensifying. In the Sunak-Strammer debate, seems to have had the upper hand, yet opinion polls continue to show a wide margin in favor of the Labor party. The issue has high stakes and given the Labor’s lead, could increase uncertainty in the UK, yet elections are still some way oof to affect the path of the pound. On a macroeconomic level, we note the verification of the drop of the Services PMI figure for May, which tends to imply a slowdown in the expansion of economic activity in the critical UK services sector. In the coming week, we highlight the release of the UK employment data on Tuesday and the GDP rates for April on Wednesday. Should the employment data imply a loosening of the UK employment market we may see more pressure being added on BoE to start cutting rates early and could weaken the pound. Similar effects may have also a possible contraction of the GDP rates. On a monetary policy level, we note the market’s expectations for BoE to start cutting rates in its next meeting on the 20th of June and expect that should there be further signals to that direction by BoE policymakers or analysts we may see the pound losing some ground in the coming week.

JPY – BoJ’s interest rate decision could weaken the Yen

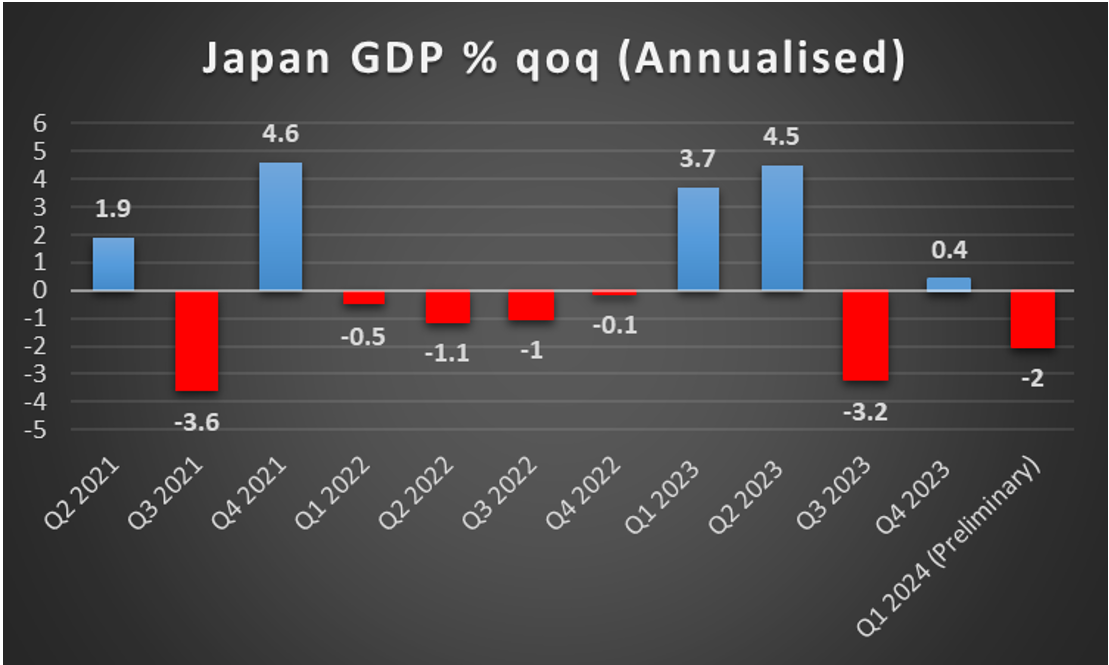

JPY is about to end the week a bit stronger against the pound, the USD and the common currency in a sign of wider strength. We tend to view the rise of JPY against its counterparts as a correction give the depreciation suffered by the Japanese currency since the start of the year. We also continue to view BoJ’s loose monetary policy maybe as the main factor behind the weakening of JPY. Hence we highlight the release of the bank’s interest rate decision on Friday as the main event for the week for JPY traders. The bank is expected by the market to keep rates unchanged and JPY OIS imply currently a probability of 83% for such a scenario to materialise. Hence the market’s attention is expected to turn towards the accompanying statement and its forward guidance. We do not expect a material shift in the bank’s stance, maybe a tweak towards the hawkish side which theoretically could provide some support for the JPY. Yet it remains doubtfull if the bank could convince the markets about any hawkish intentions. Should the bank actually fail to convince the markets we may see the Japanese currency losing some ground against its counterparts. On a macro-economic level, we highlight the release of Japan’s revised GDP rate for Q1 and a possible verification of the contraction noted in the preliminary release could serve as a painful reminder for the darkening economic outlook of Japan and could weigh on the Yen.

EUR – ECB delivers its first rate cut

The EUR is about to end the week stronger than the USD, relatively unchanged against the GBP and weaker against the JPY. On a fundamental level, we note the European Parliament elections which are ongoing and are scheduled to end on Sunday. The elections are to deliver a new balance of power within the EU. The center-right EPP is expected to win the elections yet the far right is expected to strengthen, while the center-left, the greens and the left are expected retreat. A possible strengthening of the far right could strengthen the idea of a fortress-Europe given also that migration is one of the most important issues in these elections while in a more general sense, a strengthening of the far right could intensify centrifuge forces within the EU. In such a scenario we may see the common currency weakening on Monday. On a monetary policy level, we note the release of the ECB’s on Thursday. The bank as was expected, delivered a 25 basis points rate cut, yet avoided to commit to further rate cuts in the future. Nevertheless, ECB President Christine Lagarde stated that Thursday’s rate cut was justified by the bank’s confidence in the path ahead. Overall, we view the bank’s stance as a predisposition for more rate cuts, yet also that the bank at the same time remains data[1]dependent. Should in the coming week, ECB policymakers start highlighting the possibility for a pause in rate cuts we may see the EUR getting some support. With the exception of the final HICP rates of France and Germany for May and Eurozone’s Sentix index, we expect a rather quiet week for EUR traders where fundamentals are to lead the way for the common currency’s direction.

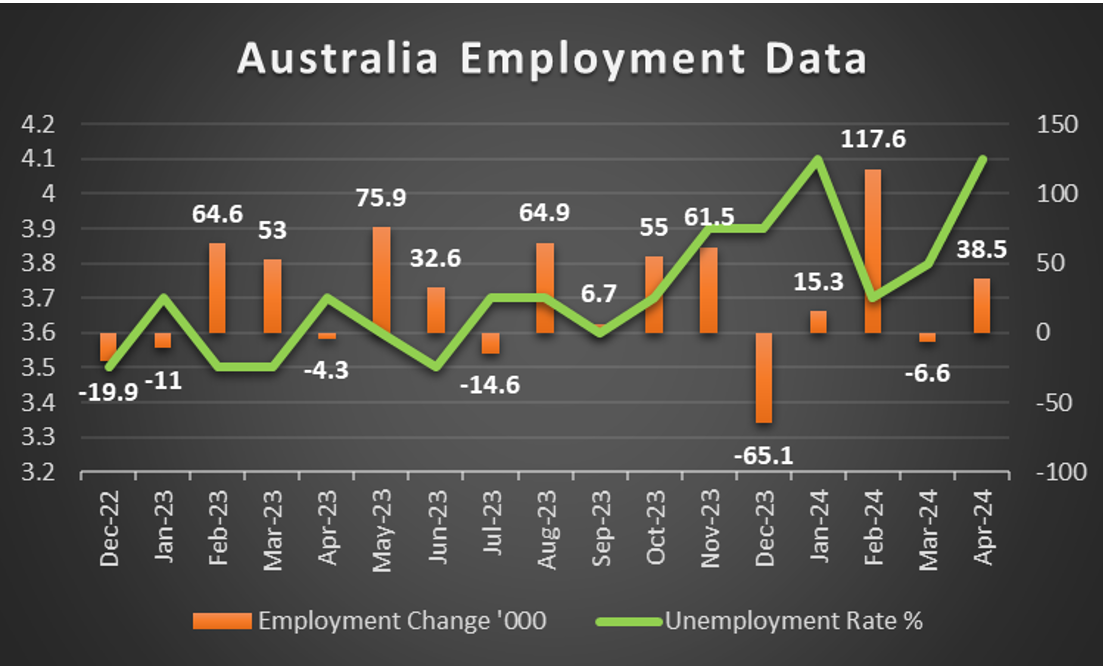

AUD – Employment data in focus

AUD is about to end the week slightly stronger against the USD. On a fundamental level, we note the risk deriving from the tensions in the US-Sino relationships. Should there be an escalation in the tensions in the US-Sino relationships we may see them weighing on the Aussie, given the close economic ties between Australia and China. The issue was once again highlighted after statements made by China’s defence minister that ‘whoever dares to split Taiwan from China will be crushed to pieces and suffer his own destruction’. On a macroeconomic level, Aussie traders may keep an eye out also for the release of China’s inflation metrics on Wednesday. Yet the main event for AUD in the coming week is expected to be the release of Australia’s employment data for May. Should we see the unemployment rate rising and the employment change figure dropping, aligning and pointing towards a loosening Australian employment market, we may see the Aussie losing some ground. On another fundamental level, we would also note the market’s perception of the Aussie as a riskier asset given its commodity nature. Hence the sensitivity of the Aussie to the market’s mood is enhanced. Should we see the market adopting a more risk-oriented approach the Aussie could get some support and vice versa. On a monetary level, we note RBA’s confident stance and the market’s expectations that no rate cuts are on the horizon for the year. Hence should we see RBA policymakers highlighting the bank’s hawkish stance in the coming week we may see the Aussie getting some support.

CAD – Boc delivered a rate cut, more to come?

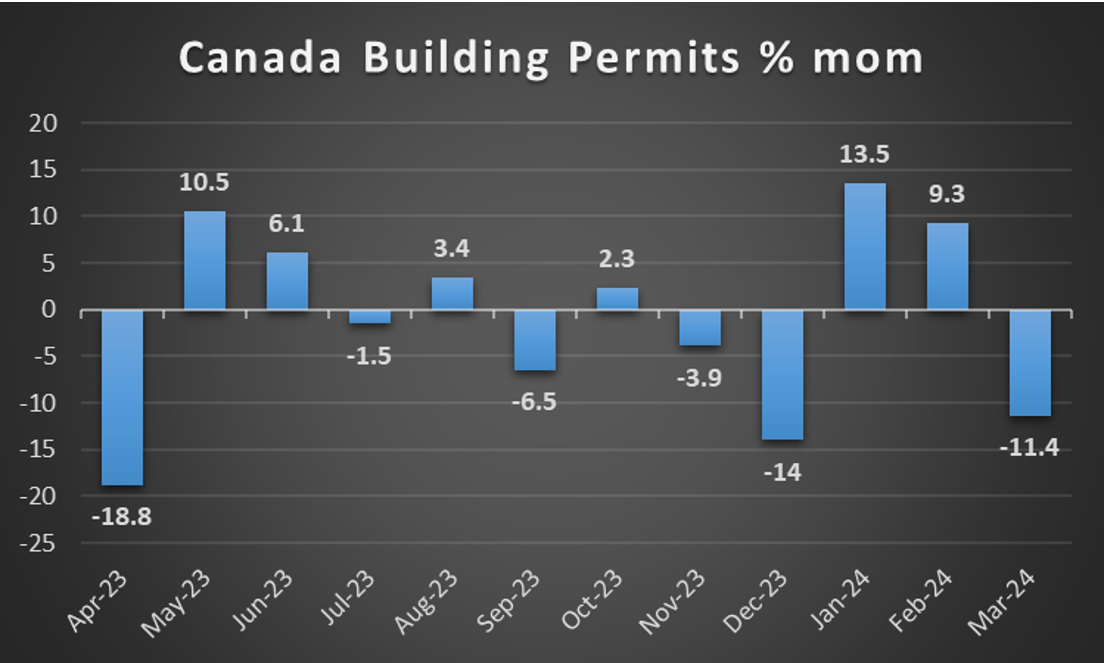

The CAD is about to end the week weaker against the USD. It should be noted though that May’s employment data for both Canada and the US are still to be released and could alter the path of the exchange pair. On a monetary level, we note that BoC in its interest rate decision, cut rates by 25 basis points (bp) as was expected by the market. Following the decision, BoC Governor Macklem in the accompanying press conference stated that “monetary policy no longer needs to be as restrictive”. The comments made by BoC Governor Macklem, could be perceived as slightly dovish in nature, as it implies that the bank may continue easing its monetary policy, which in turn could weigh on the Loonie. On a fundamental level, we note that the drop of oil prices seems to have aided the weakening of the CAD, given Canada’s status as a major oil-producing economy. The international oil market seems to be caught between conflicting fundamentals as on the one hand the signals deriving from the US oil market seem conflicting yet at the same time, the drop of the US ISM manufacturing PMI figure and the struggling of Chinese factories to increase economic activity, seem to foreshadow a possible reduction in oil demand which weighed on oil prices. Should we see oil prices renewing their bearish tendencies we may see them having an adverse effect on oil prices in the coming week. On a macroeconomic level, we note that Canada’s manufacturing sector seems to have suffered another contraction of economic activity in the past month given the drop of the S&P manufacturing PMI figure for the relative month. In the coming week we would note the release of the building permits and manufacturing sales growth rates for April and other than that, we may see fundamentals leading the way.

General Comment

As an epilogue, we tend to see the USD increasing its influence in the FX market, given that the frequency and gravity of US financial releases and monetary policy events increase in the coming week. As for US stock markets, we note a positive mood of market participants in the past few days being more evident in S&P 500 and Nasdaq which reached new record highs and to a lesser degree Dow Jones. We tend to highlight though, that the main driver behind US stock markets may be the tech sector and we highlight especially NVIDIA’s course. Should we see the positive market sentiment being maintained, we may see US stock markets rising further. As for gold, we see the negative correlation of the precious metal to the USD being on display once again in the past few days. Should the USD continue to weaken in the coming week we may see gold’s price rising even further. It should be noted that the drop of US yields may have enhanced the rise of gold’s price, as the attractiveness of US Bonds as safe haven instruments tends to be reduced.

如果您对本文有任何常规疑问或意见,请直接发送电子邮件至我们的研究团队,地址为 research_team@ironfx.com

免责声明:

本信息不被视为投资建议或投资推荐, 而是一种营销传播. IronFX 对本信息中引用或超链接的第三方提供的任何数据或信息概不负责.