The USD seems to have been able to halt last week’s drop and stabilise in the first day of the week, a modus vivendi that seems to continue into today’s Asian session. Stockmarket bulls seem to experience a hesitation as US stockmarkets’ advances higher have come to a halt and are pondering about the direction of their next leg, given also the earnings releases due out today, with Walmart and Home Depot standing out. Yet our worries for US stockmarkets tend to remain present given that in addition to the mayhem created by Musk’s taking over Twitter and delisting it, Facebook laying off thousands of workers, now reports show that also Amazon may be on the same path with 10,000 workers at risk of being laid off and all of that ahead of Black Friday and the critical Christmas season. In the FX market we note the wide drop into the negatives of Japan’s preliminary GDP rate for Q3, a release that tended to weaken the Yen as it took markets by surprise revealing that the situation in the land of the rising sun is worse than what was expected.

On the other hand, we would not be surprised though if the release would provide more leeway for BoJ to continue with its ultra-loose monetary policy settings as should the contraction of the Japanese economy continue it would be in a recession and any tightening of the bank’s monetary policy could expedite such a scenario. Staying in the far-east, we also note the contraction noted of Chinas’ retail sales growth rate for October as a sign that the demand side of the Chinese economy may be waning and could be spelling trouble also for Australia’s export sector. On a monetary policy level, we note that Fed’s Vice Chair Lael Brainard in statements she made yesterday sounded like Fed Board Governor Waller as she stated that more rate hikes lay ahead, yet tended to imply that supersized rate hikes should end “soon”. Overall, we note that the Fed speakers after the release of the latest CPI rates for October, have yet to provide clear guidance regarding the Fed’s intentions, allowing for the markets to continue pondering.

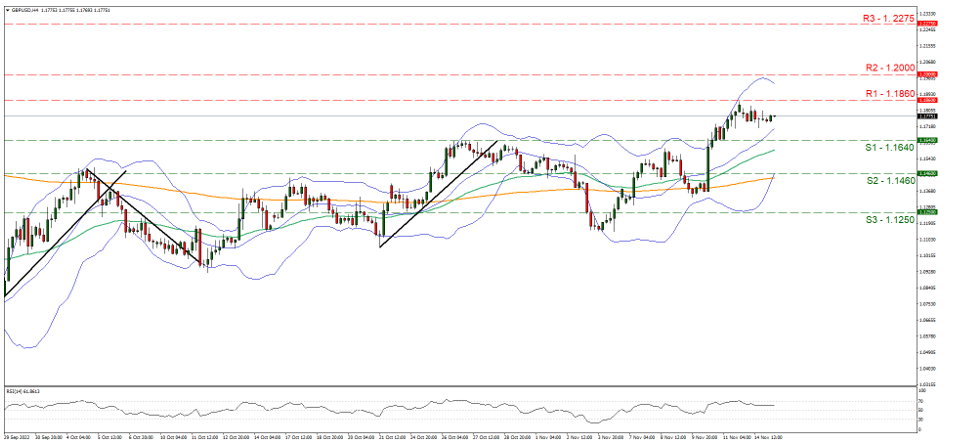

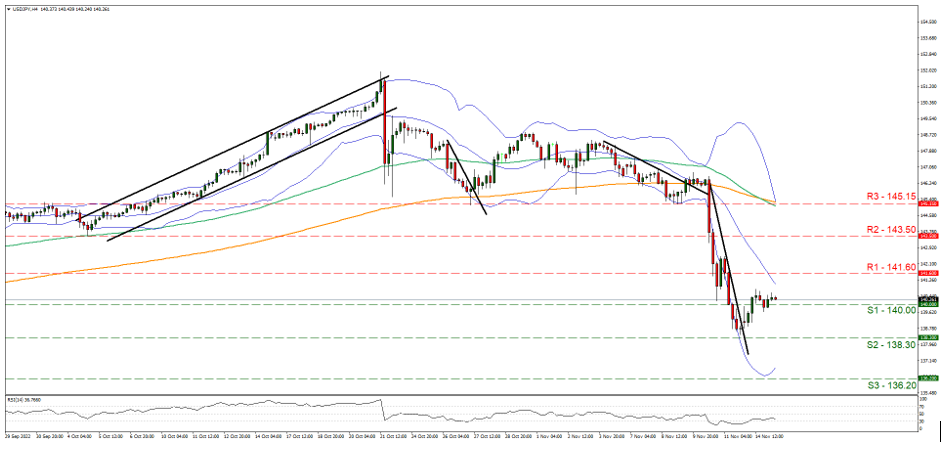

USD/JPY was on the rise yesterday breaking the 140.00 (S1) resistance line, now turned to support. We tend to maintain a bias for a sideways motion with the pair’s price action possibly revolving around the 140.00 (S1) axis, yet we would like to note that the bearish sentiment seems to remain present for the pair given that the RSI indicator is near the reading of 30. Should a selling interest be actually expressed by the market for USD/JPY, we may see the pair breaking the 140.00 (S1) support line and aim if not breach the 138.30 (S2) level. Should the bulls take over, we may see the pair aiming if not breaking the 141.60 (R1) resistance line. GBP/USD seems to maintain a sideways motion between the 1.1860 (R1) resistance line and the 1.1640 (S1) support line. We tend to maintain a bias for a rangebound movement, yet we note that there are some slight bullish tendencies for cable. Should the bulls actually take over, we may see cable breaking the 1.1860 (R1) resistance line and aim for the 1.2000 (R2) level. Should the bears take over, we may see GBP/USD breaking the 1.1640 (S1) support line and aim for the 1.1460 (S2) support level.

今日其他亮点:

During the European session, we note from the UK the release of September’s employment data, from Sweden the CPI rate for October, from France the final HICP rate for October, from the Eurozone the estimate GDP rate for Q3 and from Germany the ZEW indicators for November. In the American session, we note the release from the US of the NY Fed manufacturing index for November, and the PPI rates for October, from Canada we get the manufacturing sales and the wholesale trade growth rates for September, while oil traders may be more interested in the release of the API weekly crude oil inventories figure later on. On the monetary front we note that Philadelphia Fed President Harker, Fed Board Governor Cook and ECB board member Elderson are scheduled to speak. During tomorrow’s Asian session we note the release of Japan’s machinery orders for September and from Australia the wage price index for Q3.

英镑/美元4小时走势图

Support: 1.1640 (S1), 1.1460 (S2), 1.1250 (S3)

Resistance: 1.1860 (R1), 1.2000 (R2), 1.2275 (R3)

美元/日元4小时走势图

Support: 140.00 (S1), 138.30 (S2), 136.20 (S3)

Resistance: 141.60 (R1), 143.50 (R2), 145.15 (R3)

如果您对本文有任何常规疑问或意见,请直接发送电子邮件至我们的研究团队,地址为 research_team@ironfx.com

免责声明:

本信息不被视为投资建议或投资推荐, 而是一种营销传播. IronFX 对本信息中引用或超链接的第三方提供的任何数据或信息概不负责.