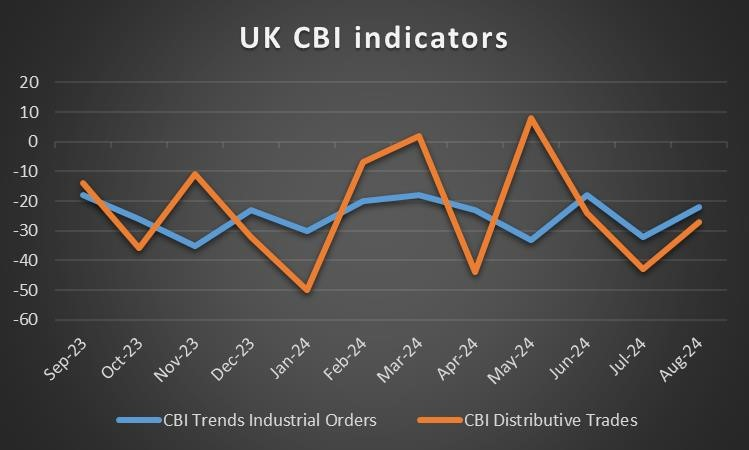

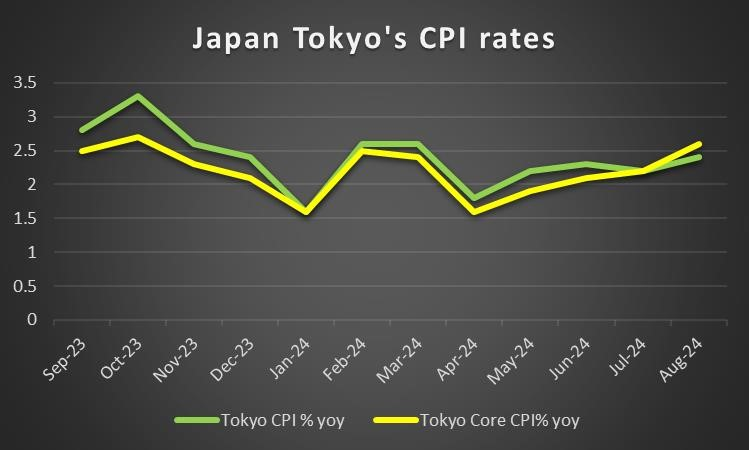

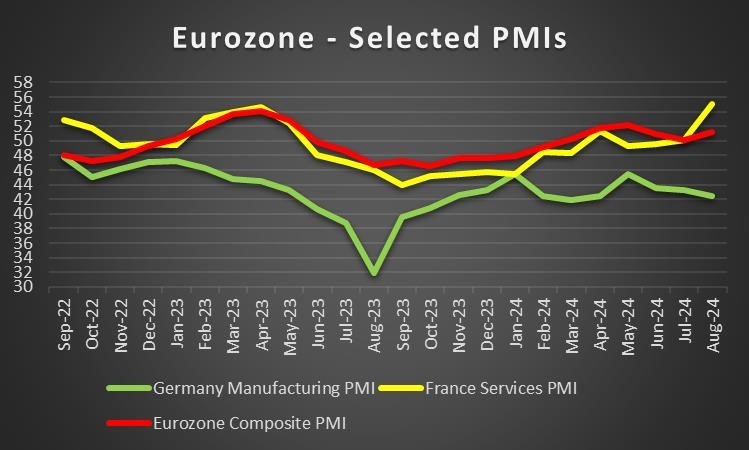

A rocky week draws to a close as we take a look at what next week has in store for the markets. On the monetary front we highlight from Australia, RBA’s interest rate decision on Tuesday, while we also get from Sweden Riksbank’s and the Czech Republic’s CNB interest rate decisions on Wednesday and on Thursday from Switzerland SNB’s interest rate decision. As for financial releases we make a start on Monday with New Zealand’s August trade data, Australia’s, France’s, Germany’s, the Eurozone’s, UK’s and the US preliminary PMI figures for September, while from the UK we also get the CBI indicator for trends in industrial orders for September. On Tuesday, we get Japan’s preliminary PMI figures for September and from Germany the Ifo indicators for the same month. On Thursday, we get Germany’s GfK Consumer Sentiment for October, Canada’s Business Barometer for October and from the US the Durable goods orders for August, the final GDP rate for Q2 and the weekly initial jobless claims figure. On Friday we get from Japan, Tokyo’s CPI rates for September, France’s preliminary HICP rate for September, Euro Zone’s Business Sentiment for September, UK’s September CBI Indicator for distributive trades, we highlight the US Core and headline PCE index rates and we get also Canada’s GDP rate for July and from the US the final University of Michigan consumer sentiment for September.

USD – Fed’s double rate cut sent out a clear message

The USD is about to end the week slightly in the reds against its counterparts. The Fed’s double rate cut may on Wednesday may have been the main event for USD traders in the past week. In the bank’s accompanying 资产购买保持在每月 it appears that the 50bp cut was warranted by progress on inflation.

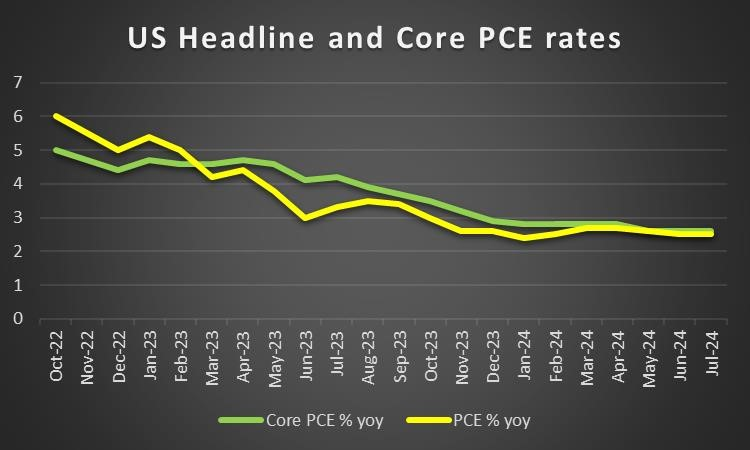

Powell’s press conference, it appears that policymakers are concerned about the downside risks to employment which have increased according to Fed Chair Powell. The Fed’s interest rate decision sent a clear message to the markets about its intentions and the new tack in its monetary policy. We expect comments of Fed policymakers in the coming week to align with the bank’s now supporting role for the US economy and thus could weigh on the greenback. In the coming week, we highlight the release of the final US GDP rate for Q2, yet we also intend to focus on the release of the Core and headline PCE rates for August on Friday. A possible slowdown of the rates implying further easing of inflationary pressures could weigh on the USD and vice versa.

GBP – BoE remains on hold as expected

The pound is about to end the week in the greens against the USD, JPY and EUR, in a sign of wider strength of the pound in the FX market. BoE remained on hold yesterday as was widely expected, given also that the CPI rates for August implied resilient inflationary pressures in the UK economy both at a headline as well as at a core level. In the accompanying statement the bank mentioned that “a gradual approach to removing policy restraint remains appropriate”, maybe not as dovish as the market expected, an element that provided support for the pound at the time of the release. On the other hand, we also note that the market’s expectations are for a rate cut in the November meeting. We expect the bank’s monetary policy to continue to feed pound bulls in the coming week, as long as BoE policymakers continue to contradict market expectations, forcing the market to reposition itself in the pound’s favour. Yet the pound got renewed support today as the retail sales growth rate accelerated beyond market expectations implying that the UK consumer is able and willing to spend more in the UK economy, contributing to its recovery. In the coming week, we may see the release of September’s preliminary PMI figures and CBI indicators gaining some attention yet other than that fundamentals may lead the pound.

JPY – BoJ remained on

hold and hawkish

JPY weakened against the USD, GBP and EUR in a sign of wider weakness. The main event for JPY traders in the past week may have been the release of BoJ’s interest rate decision and Japan’s CPI rates for July. BoJ remained on hold during today’s Asian session. The bank’s intentions continue to lean towards the hawkish side in our opinion, as the bank continues to aim towards a normalization of its monetary policy, by further hiking rates, albeit carefully. We see the case for BoJ to continue leaning on the hawkish side which could keep JPY supported on a monetary level in the coming week. The acceleration of the CPI rates for August, tends to support the scenario of a hawkish BoJ in the coming week. On a fundamental level, we note the possibility of JPY experiencing some flows given its status as a safe haven in the international markets and should market worries intensify on a geo strategic level, we may see JPY gaining. As for financial releases we highlight the release of September’s preliminary PMI figures yet also note the release of Tokyo’s CPI rates for the same month on Friday.

EUR – September Preliminary PMI figures eyed

The EUR got some support against the USD and JPY yet slipped against the pound for the week. With the slowdown of Eurozone’s HICP rate for July confirmed, EUR traders are about to enter the coming week. We highlight the release of September’s preliminary PMI figures for the area on Monday. Main points of focus are the indicators for France’s services sector, Germany’s manufacturing sector and for a rounder view Eurozone’s composite indicator. The main point of market worries for EUR traders is expected to be the manufacturing sector as a whole and especially Germany’s. Should the indicator’s reading imply another, possibly deeper contraction of economic activity it could weigh on the common currency. On the flip side should other sectors and/or countries be able to compensate and contribute to an increase of economic activity throughout sectors and countries in the Eurozone, we may see some support for the Euro. Other than that the political uncertainty for the area seems intense and could weigh on the EUR, while also the prospect of a further easing off ECB’s monetary policy does not bode well with EUR traders.

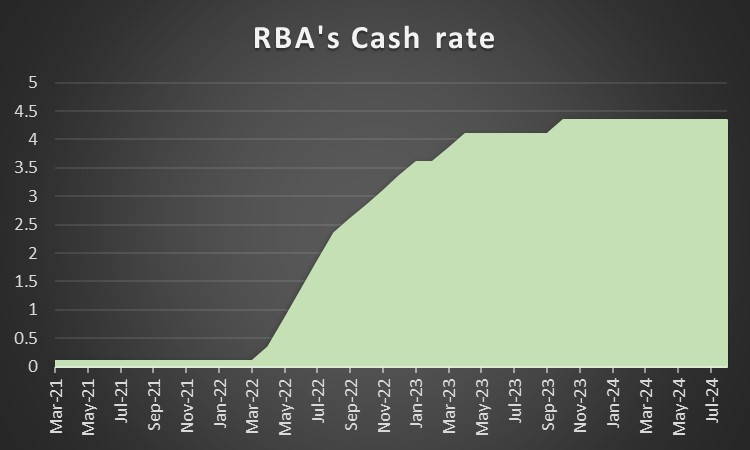

AUD – RBA’s interest rate decision to shake the Aussie

AUD is about to end the week in the greens against the USD. Aussie traders were encouraged on Thursday, as August’s employment data were better than expected, implying a tighter than expected Australian employment market. The release may have provided some leeway for RBA to remain hawkish in its coming meeting next Tuesday. The bank is widely expected to remain on hold keeping the Cash rate at 4.35% and currently AUD OIS imply a probability of 94% for such a scenario to materialise, rendering the interest rate part of the decision as an open and shut case. The market seems to expect the bank to remain on hold also in the November meeting. Should the decision be accompanied by a statement implying hawkish intentions we may see the Aussie getting some support. On a fundamental level, we note the release of the preliminary PMI figures for September on Monday and a possible rise of the indicators’ readings could imply improved economic activity, thus providing support for the AUD. Aussie traders may keep an eye out for developments in China, given the close Sino-Australian economic ties.

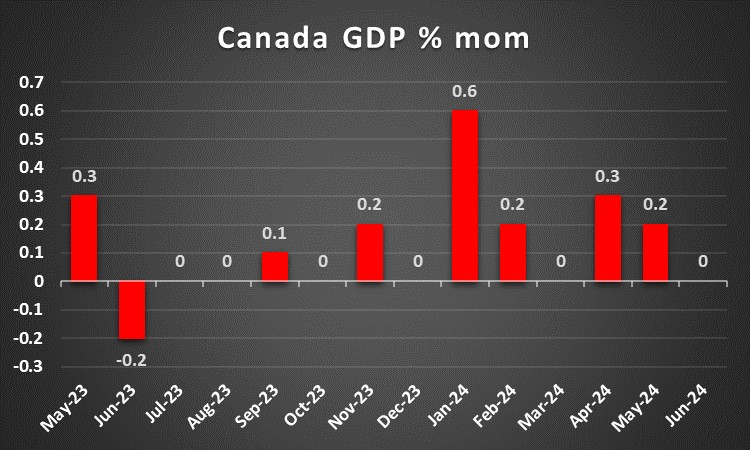

CAD – August’s GDP rate to move the Loonie

We start by noting that Canada’s retail sales growth rate for July are still to be released and could move the Loonie before the week ends. For the time being the CAD seems to be ending the week slightly stronger against the USD. Maybe the main release of the week for CAD traders were August’s CPI rates. The rates slowed down beyond market expectations both on a headline and core level highlighting the further easing of inflationary pressures in the Canadian economy. It’s understandable hoe the release may have enhanced market expectations for the BoC to proceed with a double rate cut in its late October meeting. On a fundamental level, the rise of oil prices and should it be continued in the coming week, it may provide some support for the Loonie as well, given Canada’s status as a major oil producing country. As for financial releases we would note the release of Canada’s GDP rate for August next Friday and should the rate be able to escape stagnation levels and accelerate showing growth for the Canadian economy we may see the CAD getting some support.

General Comment

As a closing we note for the FX market that we expect the USD to relent some of the initiative to other currencies, given that the frequency and gravity of US financial releases eases in the coming week. In turn, such a development may allow other currencies to get under the spotlight and create a more balanced trading mix for FX traders. As for US stock markets, we note the optimism characterising market participants in the past few days, with al three major US stock market indexes namely Dow Jones, S&P 500 and Nasdaq preparing to end the week in the greens. The Fed’s interest rate decision send a decisive message of easing monetary policy restrictions and possibly improving the financial environment. As for gold’s price we note that the precious metal had some modest gains given the greenback’s slip. Also US yields remained relatively unchanged if compared to last Friday, playing no major role as these lines are written to gold’s direction. Yet the shiny metal’s price action was enabled to reach new record high levels, highlighting its bullish tendencies.

如果您对本文有任何常规疑问或意见,请直接发送电子邮件至我们的研究团队,地址为 research_team@ironfx.com

免责声明:

本信息不被视为投资建议或投资推荐, 而是一种营销传播. IronFX 对本信息中引用或超链接的第三方提供的任何数据或信息概不负责.